Downloaded 54 times

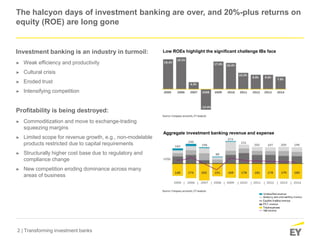

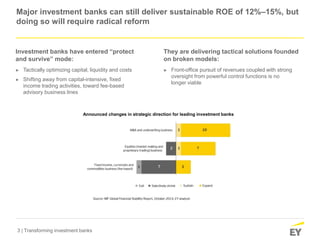

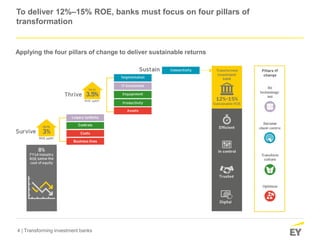

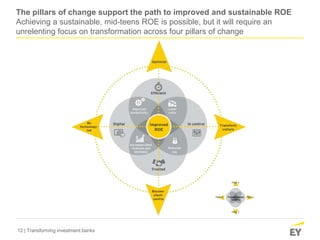

The investment banking industry is facing significant challenges, including low returns on equity, productivity crises, and eroded trust. To achieve sustainable returns of 12%-15%, banks must implement radical reforms across four key pillars: optimizing costs, transforming culture, becoming client-centric, and embracing technology. These transformations require a shift from traditional methods to more innovative, technology-driven approaches while focusing on long-term profitability and client satisfaction.