Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Venture Capitalist competition Analysis Team Lollapalooza

Similar to Venture Capitalist competition Analysis Team Lollapalooza (20)

More from doshihardik

More from doshihardik (17)

Venture Capitalist competition Analysis Team Lollapalooza

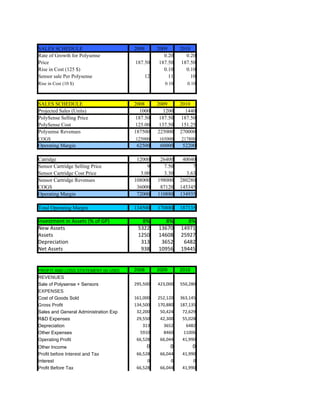

- 1. SALES SCHEDULE 2008 2009 2010 Rate of Growth for Polysense 0.20 0.20 Price 187.50 187.50 187.50 Rise in Cost (125 $) 0.10 0.10 Sensor sale Per Polysense 12 11 10 Rise in Cost (10 $) 0.10 0.10 SALES SCHEDULE 2008 2009 2010 Projected Sales (Units) 1000 1200 1440 PolySense Selling Price 187.50 187.50 187.50 PolySense Cost 125.00 137.50 151.25 Polysense Revenues 187500 225000 270000 COGS 125000 165000 217800 Operating Margin 62500 60000 52200 Catridge 12000 26400 40040 Sensor Cartridge Selling Price 9 7.50 7 Sensor Cartridge Cost Price 3.00 3.30 3.63 Sensor Cartridge Revenues 108000 198000 280280 COGS 36000 87120 145345 Operating Margin 72000 110880 134935 Total Operating Margin 134500 170880 187135 Investment in Assets (% of GP) 8% 8% 8% New Assets 5322 13670 14971 Assets 1250 14608 25927 Depreciation 313 3652 6482 Net Assets 938 10956 19445 PROFIT AND LOSS STATEMENT (in USD) 2008 2009 2010 REVENUES Sale of Polysense + Sensors 295,500 423,000 550,280 EXPENSES Cost of Goods Sold 161,000 252,120 363,145 Gross Profit 134,500 170,880 187,135 Sales and General Administration Exp 32,200 50,424 72,629 R&D Expenses 29,550 42,300 55,028 Depreciation 313 3652 6482 Other Expenses 5910 8460 11006 Operating Profit 66,528 66,044 41,990 Other Income 0 0 0 Profit before Interest and Tax 66,528 66,044 41,990 Interest 0 0 0 Profit Before Tax 66,528 66,044 41,990

- 2. Provision for Tax 23285 23115 14697 Profit After Tax 43,243 42,929 27,294 Provision for Dividend 313 313 313 Retained Earnings 42,930 42,616 26,981 BALANCE SHEET (in USD) 2008 2009 2010 SOURCES OF FUND Shareholder's Fund Share Capital - Promoters 2,500 2,500 2,500 Share Capital - VC 1,071 1,071 1,071 Share Premium 26,929 26,929 26,929 Reserves and Surplus 42,930 42,616 26,981 Net Worth 72,359 72,045 56,410 Loans Funds TOTAL LIABILITIES 72,359 72,045 56,410 APPLICATION OF FUNDS Fixed Assets Gross block 1,250 14,608 25,927 Accumulated Depreciation 313 3652 6482 Net Fixed assets 938 10956 19445 Investments 0 0 0 Current Assets Sundry Debtors 59,100 84,600 110,056 Cash in Hand & Bank 44521 26913 -462 Current Liabilities Sundry Creditors 32,200 50,424 72,629 Net Current Assets 71,421 61,089 36,965 TOTAL ASSETS 72,359 72,045 56,410 Ratio Analysis 2008 2009 2010 ROE 59.33% 59.15% 47.83% Sales/ Book Value 4 7 15 EPS assumin 1 share of 1$ 12.02 11.93 7.55 Operating Margin 46% 40% 34% Overhead Expenses to Opeating Exp 46% 56% 72% Gross Profit/ Net Profit 32% 25% 14% Return on Net Assets 60% 70% 73% Current Ratio 3.22 2.21 1.51 Cash to Net Assets 62% 44% -1% Break Even Analysis 2008 2009 2010 Sales 295,500 423,000 550,280 Variable cost 161,000 252,120 363,145 Semi- Variable Cost 38,110 58,884 83,635 Contribution 96,390 111,996 103,500 Contribution Per Unit 96 93 72 Fixed Cost 29,863 45,952 61,510

- 3. Break Even (Units) 310 492 856

- 4. Assumptions 2008 2009 2010 Growth 20% 20% Selling Price would not increase 187.5 187.5 187.5 Rise in COGS (%) 0% 10% 10% Sensor Sale per Machine would decrease in years 12 11 10 Rise in COGS of Sensor (%) 0% 10% 10% Sales Projection on Realistic basis 1000 1200 1440 Selling Price of Cartridge (it would kep reducing) 9 7.5 7 COGS of Sensor would increase 0% 10% 10% We assume that investment in miscelleaneus assets on % of GP 8% 8% 8% Depreciation WDV 25% 25% 25% Valuation Pre Investment 2008 2009 2010 PAT 43,243 42,929 27,294 Depreciation 313 313 313 Cash Flow 43,555 43,241 27,606 Year 1 2 3 Discounting Rate 0.12 0.12 0.12 Discounting Factor 0.89 0.8 0.71 PV of Cash Flows 38888.73 34471.55 19649.63 Other expenses are taken as percentage of sale @2% 2% Sum Of Present Values 93009.91 Purchase 30% Value - Equity Err:502

- 5. Investment Strategy 2008 2009 2010 Equity 28000 Debt Commitment (with conditions) @10 % 50000 50000 75000 Rate of Interest 10% PLR+2.25% PLR+2.25% We would embed a real option into the debt converting debt into equity within a period of two years from the date of debt given but only till Dec 2011 as last Valuation of company for converting debt into equity would be Years 2008 2009 2010 Increment for Valuation in future years 40% 60% 80% Valuation of Company for these years 130667 149333 168000 Example Date of loan given Dec-08 Nov-09 Mar-10 Debt given 50000 50000 50000 Rate of Interest 10% PLR+2.25% PLR+2.25% Exercising Right Valid Till Dec-10 Nov-11 Dec-11 Debt conversion in the following years 50000 40000 40000 Equity 38% 27% 24% UPPER Cap on VC shareholding would not be more than 60% at any point of time Investment Plan 2008 2009 2010 Equity 28000 Debt Commitment 50000 50000 75000 Key Benchmarks to achieve Sales of minimum Machines 800 960 1100 Sensors 6400 14080 22880 Minimum Level of ROE 30% 30% 30% R&D expenses Both the Products are to be evalued and stage of development would be considered Rating of UNICEF would be takeninto consideration Equity Dilution Any stake dilution would not be permisible without the consent of VC The VC would have "First right of Refusal" THe Promoter cannot engage in any other business with the same kind of research Any dealings with Bhat Bio- Tech India Pvt Ltd would have to be cleared from the director of VC

- 7. Cost of Manufacturing Annual Increase in Cost of Goods Sold* 10% Sales & General Expenses as proportion of Cost of Goods Sold 20% Sundry Debtors as % of Sales 20% Sundry Creditors as % of Cost of Goods sold 20% Initial Assets (Testing Eqpt and Electrode Mfg Eqpt) 50000 Annual Rate of Depreciation 25% Reducing Balance Method used for Depreciation Tax Rate (Corporate tax) 35% R& D Investment as % of Sales 10% Interest Rates Long term Debt 10% Provision for dividend (Including CDT) 12.50%