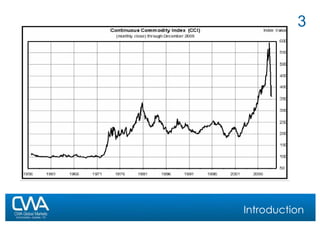

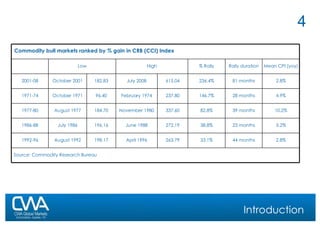

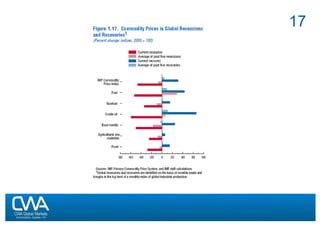

The document provides a chronological overview of major global events that have shaped global commodity markets since World War 2, including the Bretton Woods agreement, Nixon ending the gold standard, oil embargoes, economic recessions and recoveries, geopolitical conflicts, and the rise of emerging markets like China. It then notes that while commodity prices declined in real terms for many years after the 1970s, prices have risen since 2000 due to factors like rapid industrialization and income growth in China and other emerging markets outpacing supply growth, as well as a sustained decline in the US dollar value boosting commodity prices.