Problem 11 - 43 flexible budgeting; variances; impact on behavior

1. Problem 11-43:

Flexible budgeting; variance; impact on behavior

LawnMate Company manufactures power mowers that are sold throughout the United States

and Canada. The company uses a comprehensive budgeting process and compares actual

results to budgeted amounts on a monthly basis. Each month, LawnMate’s accounting

department prepares a variance analysis and distributes the report to all responsible parties. Al

Richmond, production manager, is upset about the results for May. Richmond, who is

responsible for the cost of goods manufactured, has implemented several cost cutting

measures in the manufacturing area and is discouraged by the unfavorable variance in variable

costs.

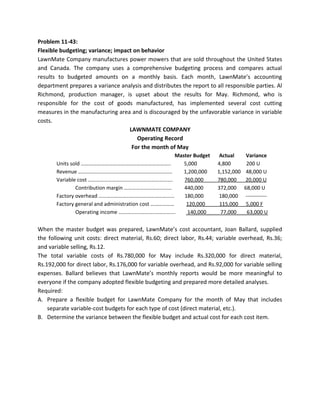

LAWNMATE COMPANY

Operating Record

For the month of May

Master Budget

Units sold …………………………………………………………..

5,000

Revenue ……………………………………………………………..

1,200,000

Variable cost ……………………………………………………….

760,000

Contribution margin ………………………………

440,000

Factory overhead ………………………………………………...

180,000

Factory general and administration cost ………………

120,000

Operating income …………………………………….

140,000

Actual

4,800

1,152,000

780,000

372,000

180,000

115,000

77,000

Variance

200 U

48,000 U

20,000 U

68,000 U

-----------5,000 F

63,000 U

When the master budget was prepared, LawnMate’s cost accountant, Joan Ballard, supplied

the following unit costs: direct material, Rs.60; direct labor, Rs.44; variable overhead, Rs.36;

and variable selling, Rs.12.

The total variable costs of Rs.780,000 for May include Rs.320,000 for direct material,

Rs.192,000 for direct labor, Rs.176,000 for variable overhead, and Rs.92,000 for variable selling

expenses. Ballard believes that LawnMate’s monthly reports would be more meaningful to

everyone if the company adopted flexible budgeting and prepared more detailed analyses.

Required:

A. Prepare a flexible budget for LawnMate Company for the month of May that includes

separate variable-cost budgets for each type of cost (direct material, etc.).

B. Determine the variance between the flexible budget and actual cost for each cost item.

2. Solution:

Actual

4,800

Revenue units sold

Variable costs

Direct material

Direct labor

Variable overhead

Variable selling

Total Variable cost

Contribution margin

Fixed cots

Fixed overhead

Fixed general and administrative cost

Total Fixed cost

Net income

Flexible

4,800

Variance

------------

1,152,000

------------

320.000

192,000

176,000

92,000

780,000

372,000

288,000

211,200

172,800

57,600

729,600

422,400

32,000 UF

19,200 F

3,200 UF

34,400 UF

50,400 UF

50,400 UF

180,000

115,000

295,000

77,000

180,000

120,000

300,000

122,400

------------5,000 F

5000 F

45,400 UF

1,152,000