How to Get Started in Social Media for Art League City

LL 479

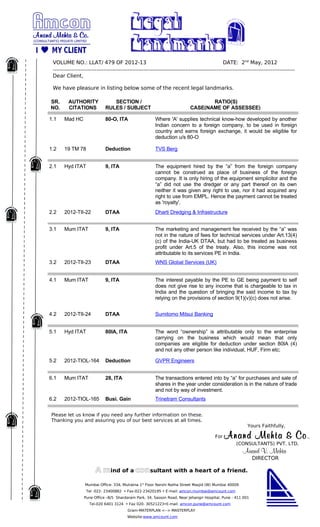

1. VOLUME NO.: LLAT/ 479 OF 2012-13 DATE: 2nd May, 2012

Dear Client,

We have pleasure in listing below some of the recent legal landmarks.

SR. AUTHORITY SECTION / RATIO(S)

NO. CITATIONS RULES / SUBJECT CASE(NAME OF ASSESSEE)

1.1 Mad HC 80-O, ITA Where 'A' supplies technical know-how developed by another

Indian concern to a foreign company, to be used in foreign

country and earns foreign exchange, it would be eligible for

deduction u/s 80-O

1.2 19 TM 78 Deduction TVS Berg

2.1 Hyd ITAT 9, ITA The equipment hired by the “a” from the foreign company

cannot be construed as place of business of the foreign

company. It is only hiring of the equipment simplicitor and the

“a” did not use the dredger or any part thereof on its own

neither it was given any right to use, nor it had acquired any

right to use from EMPL. Hence the payment cannot be treated

as 'royalty'.

2.2 2012-TII-22 DTAA Dharti Dredging & Infrastructure

3.1 Mum ITAT 9, ITA The marketing and management fee received by the “a” was

not in the nature of fees for technical services under Art.13(4)

(c) of the India-UK DTAA, but had to be treated as business

profit under Art.5 of the treaty. Also, this income was not

attributable to its services PE in India.

3.2 2012-TII-23 DTAA WNS Global Services (UK)

4.1 Mum ITAT 9, ITA The interest payable by the PE to GE being payment to self

does not give rise to any income that is chargeable to tax in

India and the question of bringing the said income to tax by

relying on the provisions of section 9(1)(v)(c) does not arise.

4.2 2012-TII-24 DTAA Sumitomo Mitsui Banking

5.1 Hyd ITAT 80IA, ITA The word “ownership” is attributable only to the enterprise

carrying on the business which would mean that only

companies are eligible for deduction under section 80IA (4)

and not any other person like individual, HUF, Firm etc;

5.2 2012-TIOL-164 Deduction GVPR Engineers

6.1 Mum ITAT 28, ITA The transactions entered into by “a” for purchases and sale of

shares in the year under consideration is in the nature of trade

and not by way of investment.

6.2 2012-TIOL-165 Busi. Gain Trinetram Consultants

Please let us know if you need any further information on these.

Thanking you and assuring you of our best services at all times.

Yours Faithfully,

For Anand Mehta & Co .,

(CONSULTANTS) PVT. LTD.

Anand V. Mehta

DIRECTOR

A mind of a consultant with a heart of a friend.

Mumbai Office- 334, Mulratna 1st Floor Narshi Natha Street Masjid (W) Mumbai 40009

Tel -022- 23400882 • Fax-022-23420195 • E-mail: amcon.mumbai@amcount.com

Pune Office –B/5 Shardaram Park, 34, Sasson Road, Near Jehangir Hospital, Pune - 411 001

Tel-020 6401 3124 • Fax 020- 30521223•E-mail: amcon.pune@amcount.com

Gram-MATERPLAN <--> MASTERPLAY

Website:www.amcount.com