Recommended

Recommended

More Related Content

Similar to Research Paper Outline and Sources Guide

Similar to Research Paper Outline and Sources Guide (20)

More from TawnaDelatorrejs

More from TawnaDelatorrejs (20)

Recently uploaded

Recently uploaded (20)

Research Paper Outline and Sources Guide

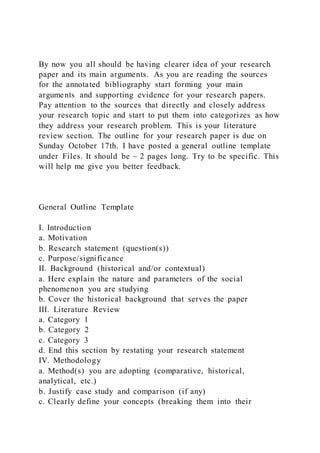

- 1. By now you all should be having clearer idea of your research paper and its main arguments. As you are reading the sources for the annotated bibliography start forming your main arguments and supporting evidence for your research papers. Pay attention to the sources that directly and closely address your research topic and start to put them into categorizes as how they address your research problem. This is your literature review section. The outline for your research paper is due on Sunday October 17th. I have posted a general outline template under Files. It should be ~ 2 pages long. Try to be specific. This will help me give you better feedback. General Outline Template I. Introduction a. Motivation b. Research statement (question(s)) c. Purpose/significance II. Background (historical and/or contextual) a. Here explain the nature and parameters of the social phenomenon you are studying b. Cover the historical background that serves the paper III. Literature Review a. Category 1 b. Category 2 c. Category 3 d. End this section by restating your research statement IV. Methodology a. Method(s) you are adopting (comparative, historical, analytical, etc.) b. Justify case study and comparison (if any) c. Clearly define your concepts (breaking them into their

- 2. measurable variables) d. Sources/data V. Main body (Arguments) a. Argument 1 i. Explain the argument ii. Supporting evidence and/or logic b. Argument 2 i. Explain the argument ii. Supporting evidence and/or logic c. Argument 3 i. Explain the argument ii. Supporting evidence and/or logic VI. Conclusion Chart of AccountsThis chart of accounts should help you identify the appropriate accounts to record to as you are analyzing and journaling transactions for this workbook. There is nothing to complete on this page; this is simply a resource for you.Asset AccountsLiability AccountsEquity AccountsAcct #Acct #Acct #Cash101Notes Payable201Common Stock301Baking Supplies102Accounts Payable202Dividends302Prepaid Rent103Wages Payable203Cost of Goods Sold303Prepaid Insurance104Interest Payable 204Baking Equipment105Office Supplies106Accounts Receivable107 Accumulated Depreciation108Merchandise Inventory109Revenue AccountsAcct #Bakery Sales401Merchandise Sales402Expense AccountsAcct #Baking Supplies Expense501Rent Expense502Insurance Expense503Misc. Expense504Business License Expense505Advertising Expense506Wages Expense507Telephone Expense508Interest Expense509Depreciation Expense510Office Supplies Expense511CashBaking SuppliesPrepaid RentPrepaid InsuranceBaking EquipmentOffice SuppliesAccounts ReceivableAccumulated DepreciationMerchandise

- 3. InventoryNotes PayableAccounts PayableWages PayableInterest Payable Common StockDividendsBakery SalesMerchandise SalesBaking Supplies ExpenseRent ExpenseInsurance ExpenseMisc. ExpenseBusiness License ExpenseAdvertising ExpenseWages ExpenseTelephone ExpenseInterest ExpenseDepreciation ExpenseOffice Supplies ExpenseCost of Goods Sold October Journal EntriesA CompanyGeneral Journal Entries October, 20xxDateAccountsDebitCredit1-Oct$$1-Oct3-Oct7- Oct10-Oct11-Oct13-Oct13-Oct14-Oct30-Oct31-Oct31-Oct31- OctTotal- 0- 0<== Do the debits equal the credits? (they should) November Journal EntriesA CompanyGeneral Journal Entries November, 20xxDateAccountsDebitCreditTotal- 0- 0<== Do the debits equal the credits? (they should) December Journal EntriesA CompanyGeneral Journal Entries December, 20xxDateAccountsDebitCreditBe sure to review the Inventory Valuation tab (Columns M-P) for all Inventory related journal entries as they are given to you! Total- 0- 0<== Do the debits equal the credits? (they should) Inventory ValuationFIFOPurchasesSalesEnding InventoryPurchasesDateNo. of ItemsUnit PriceTotal PriceNo. of ItemsUnit PriceTotal PriceNo. of ItemsUnit PriceTotal PriceDate Microsoft: Below are the journal entries for each inventory related transaction! All you need to do is copy and paste it into the correct dates on the December Journal tab! DrCr12/7: 10 boxes purchased at $67-Dec10$ 6.00$ 60.0010$ 6.00$ 60.007-DecMerchandise Inventory (10 x $6)60.0012/20: 20 boxes purchased at $6.10 Cash60.0012/30: 25 boxes purchased at $6.0515-Dec8$ 6.00$ 48.002$ 6.00$ 12.00Purchased inventorySales – selling price, $8.50 a box12/15: 8 boxes20- Dec20$ 6.10$ 122.002$ 6.00$ 12.0015-DecCash (8 x $8.50)68.0012/24: 18 boxes20$ 6.10$ 122.00 Merchandise Sales Revenue68.0022$ 134.00Record sale of inventory24- Dec2$ 6.00$ 12.0015-DecCost of Goods Sold (8 X

- 4. $6)48.0016$ 6.10$ 97.604$ 6.10$ 24.40 Merchandise Inventory48.0018$ 109.60Recorded the cost of goods sold30- Dec25$ 6.05$ 151.254$ 6.10$ 24.4020-DecMerchandise Inventory (20 x $6.10 )122.0025$ 6.05$ 151.25 Cash122.0029$ 175.65Net Inventory55$ 333.2526$ 157.6029$ 175.6524-DecCash (18 x 8.50)153.00 Merchandise Sales Revenue153.00Record sale of inventory24-DecCost of Goods Sold (2 x $6)+(16 x $6.10)109.60 Merchandise Inventory109.60Recorded the cost of goods sold30- DecMerchandise Inventory (25 x $6.05)151.25 Cash151.25 T-Accounts - autofilldateCashdatedateNotes PayabledateBusiness License expCommon Stock1-Oct$$ - 03- Oct10-Oct$ - 0$1-Oct3-Oct$ - 0$ - 013-Oct$ - 07-Oct$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 010-Oct$ - 0$ - 0$ - 0$ - 011-Oct$ - 013-Oct$ - 014-Oct$ - 031-Oct31-Oct$ - 0$ - 05-Nov8-Nov$ - 0$ - 010-Nov18-Nov$ - 0$ - 015-Nov$ - 020-NovAccounts Rec.$ - 020-Nov31-Oct- 0$ - 022-Nov- 08-Nov30-Nov$ - 0- 018-Nov$ - 01-Dec30-Nov- 0$ - 05- Dec- 08-Dec$ - 07-Dec31-Dec- 08-Dec$ - 0$ - 010-Dec$ - 0$ - 0$ - 013-Dec$ - 0$ - 015-Dec15-Dec$ - 0$ - 020- Dec$ - 020-Dec24-Dec$ - 0$ - 030-Dec31-Dec$ - 0$ - 0$ - 0$ - 0Misc. expenseBaking equipmentAdvertising expense11-Oct$ - 013-Oct$ - 013-Oct$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0Baking suppliesOffice suppliesRent expense1-Oct$ - 014-Oct$ - 07-Oct$ - 015- Nov$ - 022-Nov$ - 015-Nov$ - 011-Dec$ - 015-Dec$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0Prepaid rentPrepaid insuranceBakery Sales7-Oct$ - 031-Oct$ - 0$ - 031-Oct$ - 030-Nov$ - 031-Dec$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0Accounts payableSalary and wages expenseSalaries and wages payable$ - 01-Oct31-Oct$ - 0$ - 031-Oct$ - 031-Oct15-Nov$ - 05-Nov$ - 010-Nov$ - 030- Nov$ - 0$ - 015-Nov$ - 015-Nov15-Dec$ - 020-Nov$ - 020-Nov$ - 031-Dec$ - 0$ - 030-Nov$ - 030-Nov5-Dec$ - 010-Dec$ - 0$ - 0$ - 0$ - 015-Dec$ - 011-Dec$ - 020- Dec$ - 013-Dec$ - 0$ - 031-Dec$ - 0$ - 0$ - 0$ - 0$ -

- 5. 0$ - 0Telephone expenseDividendsCOGS 30-Oct$ - 01-Dec$ - 015-Dec$ - 030-Nov$ - 0$ - 0$ - 024-Dec$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0$ - 0Merchandise Sales RevenueMerch. Inv. FIFO$ - 015-Dec7-Dec$ - 0$ - 024- Dec$ - 015-Dec20-Dec$ - 0$ - 0$ - 0$ - 024-Dec$ - 030-Dec$ - 0$ - 0$ - 0$ - 0 Adjusting EntriesA CompanyAdjusting Journal Entries 20XXDateAccountsDebitCredit31-DecDepreciation ExpenseAccumulated Depreciation<== Interest adjustment goes here<== Interest adjustment goes here<== Insurance adjustment goes here<== Insurance adjustment goes here<== Baking supplies adjustment goes here<== Baking supplies adjustment goes here<== Office supplies adjustment goes here<== Office supplies adjustment goes here- 0- 0<== Do the debits equal the credits? (they should) Trial BalanceA CompanyTrial Balance20xxUnadjusted trial balanceAdjusting entriesAdjusted trial balanceAccountDebitCreditDebitCreditDebitCreditCash- 0Baking Supplies- 0Merchandise InventoryPrepaid RentPrepaid Insurance- 0Baking EquipmentAccumulated Depreciation- 0Office Supplies- 0Accounts ReceivableNotes PayableInterest Payable- 0Accounts PayableWages PayableCommon StockDividendsBakery SalesMerchandise SalesBaking Supplies Expense- 0Rent ExpenseInterest Expense- 0Insurance Expense- 0Depreciation Expense- 0Misc. ExpenseOffice Supplies Expense- 0Business License ExpenseAdvertising ExpenseWages ExpenseTelephone ExpenseCOGSRetained EarningsTotal:- 0- 0- 0- 0- 0- 0Do these two columns tie to the debits and credits on the adjusting entries tab?Debits should equal creditsDebits should equal creditsDebits should equal credits` Income StatementA CompanyIncome StatementFor Qtr. Ending 12/31/20XXRevenues Total Revenues- 0<== Don't forget the COGS!Gross Profit- 0Operating Expenses:Baking Supplies Expense- 0Total Operating Expenses:- 0Net Income- 0 Statement of Stockholder EquityA CompanyStatement of Stockholder's EquityFor Qtr. Ending 12/31/20xxCommon

- 6. StockRetained EarningsTotalBeginning Balances, September 30000Issued Common StockNet IncomeDividendsMake sure your dividends are negative so the formula subtracts themEnding Balances, December 31:- 0- 0- 0 Balance SheetA CompanyBalance SheetAs of December 31, 20XXAssetsLiabilities and Owners' EquityCurrent Assets:Current Liabilities:Total Current Liabilities- 0Long Term Liabilities:Total Current Assets- 0Total Long Term Liabilities:- 0Total Liabilities:- 0Shareholder's Equity:Non- Current Assets: Microsoft: show number as negative as the total formula will subtract it for you. Total Equity - 0Baking Equipment (Net)- 0Total Assets:- 0Total Liabilities & Equity - 0<== Do the debits equal the credits? (they should) Closing EntriesA CompanyClosing Entries Qtr ending 12/31/20xxDateAccountsDebitCreditNote** We are closing out the same accounts that are listed on the income statement31- DecBakery SalesMerchandise Sales Retained Earnings31- DecRetained Earnings Baking Supplies Expense Rent Expense Wages Expense Misc Expense Business License Expense Office Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense COGS 31-DecRetained Earnings Dividends Post-Closing Trial BalanceA CompanyPost-Closing Trial BalanceQtr. Ending 12/31/20xxUnadjusted Trial BalanceAccountDebitCreditCashNote** These are the same accounts that are listed on the balance sheetBaking SuppliesMerchandise Inventory Prepaid RentPrepaid InsuranceBaking EquipmentAccumulated Depreciation<== Accumulated depreciation goes in the debit column - as a reduction of the assets (so be sure it is a negative number!) just as you have on the balance sheet.Office SuppliesAccounts ReceivableAccounts PayableWages PayableInterest PayableNotes PayableCommon StockRetained Earnings Total-

- 7. 0- 0<== Do the debits equal the credits? (they should) Accounting Data Appendix 1. The following events occurred in October: October 1: The business owner used $25,000 from their personal savings account to buy common stock in their company. October 1: Purchased $8,500 worth of baking supplies from vendor, on account. October 3: The company borrowed $10,000 in cash, in exchange for a two-year, 6% note payable. Interest and the principal are repayable at maturity. October 7: Entered into a lease agreement for bakery space. The agreement is for one year. The rent is $1,500 per month; the last month’s rent payment of $1,500 is required at the time of the lease agreement. The payment was made in cash. Lease period is effective October 1 of this year through September 30 of the next. October 10: Paid $375 to the county for a business license. October 11: Purchased a cash register for $250 (deemed to be not material enough to qualify as depreciable equipment). October 13: The owner has baking equipment, including an oven and mixer, which they have been using for their home-based business and will now start using in the bakery. You estimate that the equipment is currently worth $5,000, and you transfer the equipment into the business in exchange for additional common stock. The equipment has a five-year useful life. October 13: Paid $200 for business cards and flyers to use for

- 8. advertising. October 14: Paid $300 for office supplies. October 15: Hired a part-time helper to be paid $12 per hour. One pay period is the first of the month through the fifteenth, and the other is the sixteenth through the end of the month. Paydays are the twentieth for the first pay period and the fifth of the following month for the second pay period. (No entry required on this date—for informational purposes only.) October 30: Received telephone bill for October in amount of $75. Payment is due on November 10. October 31: Paid $1,200 for a 12-month insurance policy. Policy effective dates are November 1 through October 31. October 31: Accrued wages earned for employee for period of October 16 through October 31. (See Wage Calculation Data table at the end of this document.) October 31: Total October bakery sales were $15,000 ($5,000 of these sales on accounts receivable). 2. The following events occurred in November: November 5: Paid employee for period ending October 31. November 8: Received payments from customers toward accounts receivable in amount of $3,800. November 10: Paid October telephone bill. November 15: Purchased additional baking supplies in amount of $5,000 from vendor, on account.

- 9. November 15: Accrued wages earned for employee from period of November 1 through November 15. (See Wage Calculation Data table at the end of this document.) November 15: Paid rent on bakery space. November 18: Received payments from customers toward accounts receivable in amount of $1,000. November 20: Paid $8,500 toward baking supplies vendor payable. November 20: Paid employee for period ending November 15. November 22: Purchased $300 in office supplies. November 30: Received telephone bill for November in amount of $75. Payment is due on December 10. November 30: Accrued wages earned for employee for period of November 16 through November 30. (See Wage Calculation Data table at the end of this document.) November 30: November bakery sales total was $20,000 ($7,500 of this total on accounts receivable). 3. Many customers have been asking for more allergy-friendly products, so in December the bakery started carrying a line of gluten-free products on a trial basis. The information below relates to the purchase and sales of the new products. Use the perpetual inventory method with the FIFO valuation method. Please see the “Inventory Valuation” tab in your workbook for purchase and sales information.

- 10. The following events occurred in December: December 1: Paid dividends to self in amount of $10,000. December 5: Paid employee for period ending November 30. December 7: Purchased merchandise for resale. See the “Inventory Valuation” tab for details. December 8: Received payments from customers toward accounts receivable in amount of $4,000. December 10: Paid November telephone bill. December 11: Purchased baking supplies in amount of $7,000 from vendor on account. December 13: Paid on supplies vendor account in amount of $5,000. December 15: Accrued employee wages for period of December 1 through December 15. December 15: Paid rent on bakery space $1,500. December 15: Recorded merchandise sales transaction. See the “Inventory Valuation” tab for details. December 15: Recorded impact of sales transaction on COGS and the inventory asset. See the “Inventory Valuation” tab for details. December 20: Paid employee for period ending December 15. December 20: Purchased merchandise inventory for resale to customers. See the “Inventory Valuation” tab for details.

- 11. December 24: Recorded sales of merchandise to customers. See the “Inventory Valuation” tab for details. December 24: Recorded impact of sales transaction on COGS and the inventory asset. See the “Inventory Valuation” tab for details. December 30: Purchased merchandise inventory for resale to customers. See the “Inventory Valuation” tab for details. December 31: Accrued employee wages for period of December 16 through December 31. December 31: Total December bakery sales were $25,000 ($6,000 of these sales on accounts receivable). 4. On December 31, the following adjustments must be made: · Depreciation of baking equipment transferred to company on October 13. Assume half month of depreciation in October using the straight-line method. Assume no salvage value. · Accrue interest for note payable. Assume a full month of interest for October. (6% annual interest on $10,000 loan) · Record insurance used for the year. · Actual baking supplies on hand as of December 31 are $1,100. · Office supplies on hand as of December 31 are $50. Wage Calculation Data Month Hours Rate Pay 31-Oct 10