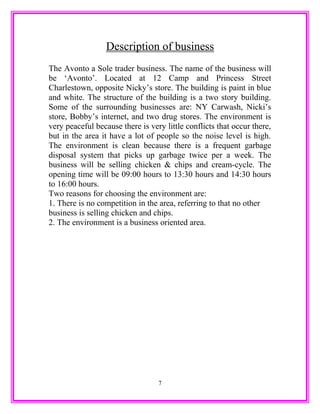

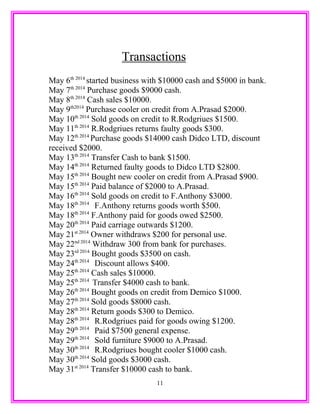

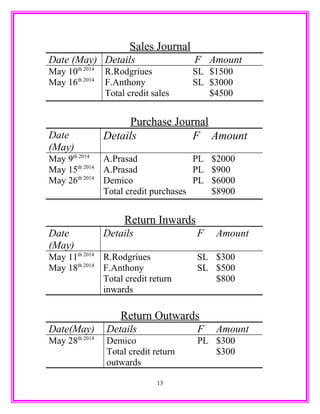

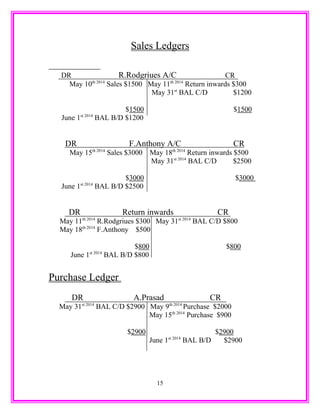

This document provides an overview of a sole proprietorship business called 'Avonto' that sells chicken, chips, and other foods. It includes sections describing the business, accounting procedures, sample transactions from May 2014, journals, ledgers, financial statements including a trial balance, income statement, and balance sheet. While the business faced some challenges with customers and storage, it was overall successful based on the $2,700 profit earned over the period.