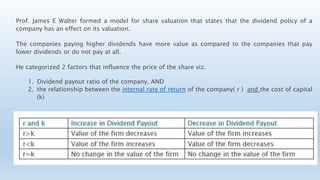

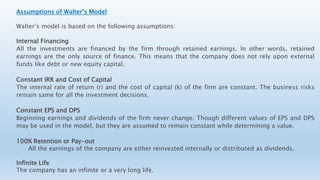

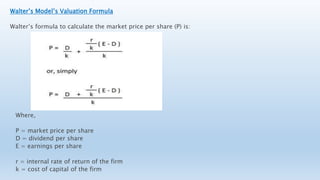

Walter's model states that a company's dividend policy impacts its valuation, with higher-dividend companies valued more than lower- or no-dividend companies. The model uses two factors - dividend payout ratio and the relationship between internal rate of return and cost of capital - in its valuation formula. The formula calculates share price as the present value of infinite dividend and retained earnings flows. The model implies different optimal payout ratios depending on a company's growth phase: 0% for growth companies, no optimum for normal companies, and 100% for declining companies.