QNBFS Daily Market Report December 19, 2018

•

0 likes•133 views

The QSE Index declined 0.1% to close at 10,489.0.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to QNBFS Daily Market Report December 19, 2018

Similar to QNBFS Daily Market Report December 19, 2018 (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report December 19, 2018

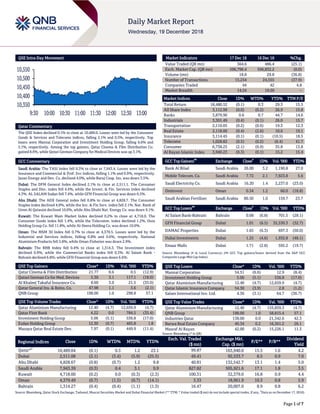

- 1. Page 1 of 7 QSE Intra-Day Movement Qatar Commentary The QSE Index declined 0.1% to close at 10,489.0. Losses were led by the Consumer Goods & Services and Telecoms indices, falling 2.1% and 0.5%, respectively. Top losers were Mannai Corporation and Investment Holding Group, falling 6.6% and 5.1%, respectively. Among the top gainers, Qatar Cinema & Film Distribution Co. gained 8.6%, while Qatari German Company for Medical Devices was up 3.1%. GCC Commentary Saudi Arabia: The TASI Index fell 0.3% to close at 7,943.4. Losses were led by the Insurance and Commercial & Prof. Svc indices, falling 1.1% and 0.9%, respectively. Jazan Energy and Dev. Co. declined 4.0%, while Buruj Coop. Ins. was down 3.5%. Dubai: The DFM General Index declined 2.1% to close at 2,511.1. The Consumer Staples and Disc. index fell 4.4%, while the Invest. & Fin. Services index declined 4.3%. AL SALAM Sudan fell 7.4%, while GFH Financial Group was down 6.5%. Abu Dhabi: The ADX General index fell 0.8% to close at 4,828.7. The Consumer Staples index declined 4.8%, while the Inv. & Fin Serv. index fell 2.1%. Nat. Bank of Umm Al Qaiwain declined 10.0%, while Abu Dhabi Nat. Energy Co. was down 9.1%. Kuwait: The Kuwait Main Market Index declined 0.2% to close at 4,718.0. The Consumer Goods index fell 1.4%, while the Telecomm. index declined 1.2%. Osos Holding Group Co. fell 11.8%, while Al-Deera Holding Co. was down 10.0%. Oman: The MSM 30 Index fell 0.7% to close at 4,379.5. Losses were led by the Industrial and Services indices, falling 0.8% and 0.6%, respectively. National Aluminium Products fell 5.8%, while Oman Fisheries was down 2.9%. Bahrain: The BHB Index fell 0.4% to close at 1,314.3. The Investment index declined 0.9%, while the Commercial Banks index fell 0.3%. Al Salam Bank - Bahrain declined 6.8%, while GFH Financial Group was down 6.6%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar Cinema & Film Distribution 21.77 8.6 0.5 (12.9) Qatari German Co for Med. Devices 5.30 3.1 117.1 (18.0) Al Khaleej Takaful Insurance Co. 8.60 3.0 21.5 (35.0) Qatar General Ins. & Reins. Co. 47.98 1.1 3.6 (2.1) QNB Group 198.00 1.0 298.8 57.1 QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Qatar Aluminium Manufacturing 12.40 (4.7) 12,659.9 (4.7) Qatar First Bank 4.22 0.0 784.5 (35.4) Investment Holding Group 5.06 (5.1) 536.8 (17.0) Ezdan Holding Group 12.30 (0.7) 465.8 1.8 Mazaya Qatar Real Estate Dev. 7.97 (0.1) 449.9 (11.4) Market Indicators 17 Dec 18 16 Dec 18 %Chg. Value Traded (QR mn) 364.6 486.4 (25.1) Exch. Market Cap. (QR mn) 596,796.4 596,832.2 (0.0) Volume (mn) 18.8 29.8 (36.8) Number of Transactions 15,254 24,555 (37.9) Companies Traded 44 42 4.8 Market Breadth 14:24 19:20 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,480.52 (0.1) 0.3 29.3 15.5 All Share Index 3,112.99 (0.0) (0.2) 26.9 15.8 Banks 3,879.90 0.6 0.7 44.7 14.6 Industrials 3,301.49 (0.4) (0.1) 26.0 15.7 Transportation 2,110.05 (0.2) (0.6) 19.3 12.3 Real Estate 2,118.00 (0.4) (2.6) 10.6 19.1 Insurance 3,114.45 (0.1) (0.1) (10.5) 18.5 Telecoms 1,028.82 (0.5) (0.2) (6.4) 41.7 Consumer 6,738.25 (2.1) (0.9) 35.8 13.8 Al Rayan Islamic Index 3,940.23 (0.3) (0.1) 15.2 15.4 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% Bank Al Bilad Saudi Arabia 26.00 3.2 1,190.8 27.0 Mobile Telecom. Co. Saudi Arabia 7.72 2.1 7,923.8 5.6 Saudi Electricity Co. Saudi Arabia 16.20 1.4 2,237.0 (23.0) Ominvest Oman 0.34 1.2 60.0 (18.8) Saudi Arabian Fertilizer Saudi Arabia 80.50 1.0 159.7 23.7 GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% Al Salam Bank-Bahrain Bahrain 0.08 (6.8) 701.5 (28.1) GFH Financial Group Dubai 1.01 (6.5) 35,530.3 (32.7) DAMAC Properties Dubai 1.65 (6.3) 697.3 (50.0) Dubai Investments Dubai 1.25 (4.6) 1,932.8 (48.1) Emaar Malls Dubai 1.71 (2.8) 595.2 (19.7) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Mannai Corporation 54.51 (6.6) 12.9 (8.4) Investment Holding Group 5.06 (5.1) 536.8 (17.0) Qatar Aluminium Manufacturing 12.40 (4.7) 12,659.9 (4.7) Qatar Islamic Insurance Company 54.30 (3.9) 2.8 (1.2) Salam International Inv. Ltd. 4.36 (3.1) 64.7 (36.7) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Qatar Aluminium Manufacturing 12.40 (4.7) 155,839.3 (4.7) QNB Group 198.00 1.0 58,815.4 57.1 Industries Qatar 138.00 0.0 21,342.6 42.3 Barwa Real Estate Company 40.34 0.2 16,361.2 26.1 Masraf Al Rayan 42.00 (0.2) 15,226.1 11.3 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar*# 10,489.04 (0.1) 0.3 1.2 23.1 99.87 163,940.0 15.5 1.6 4.2 Dubai 2,511.08 (2.1) (3.4) (5.9) (25.5) 49.41 92,533.7 8.5 0.9 7.0 Abu Dhabi 4,828.67 (0.8) (0.7) 1.2 9.8 40.81 132,542.7 13.1 1.4 5.0 Saudi Arabia 7,943.39 (0.3) 0.4 3.1 9.9 827.82 505,921.6 17.1 1.8 3.5 Kuwait 4,718.00 (0.2) 0.0 (0.3) (2.3) 100.31 32,379.0 16.8 0.9 4.4 Oman 4,379.49 (0.7) (1.5) (0.7) (14.1) 3.33 18,961.9 10.3 0.8 5.9 Bahrain 1,314.27 (0.4) (0.4) (1.1) (1.3) 16.47 20,007.0 8.9 0.8 6.2 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any, # Data as on December 17, 2018) 10,350 10,400 10,450 10,500 10,550 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QSE Index declined 0.1% to close at 10,489.0. The Consumer Goods & Services and Telecoms indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from GCC and non-Qatari shareholders. Mannai Corporation and Investment Holding Group were the top losers, falling 6.6% and 5.1%, respectively. Among the top gainers, Qatar Cinema & Film Distribution Company gained 8.6%, while Qatari German Company for Medical Devices was up 3.1%. Volume of shares traded on Tuesday fell by 36.8% to 18.8mn from 29.8mn on Monday. However, as compared to the 30-day moving average of 7.3mn, volume for the day was 156.9% higher. Qatar Aluminium Manufacturing Company and Qatar First Bank were the most active stocks, contributing 67.3% and 4.2% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 12/17 EU Eurostat CPI Core YoY November 1.0% 1.0% 1.0% 12/17 EU Eurostat CPI YoY November 1.9% 2.0% 2.0% 12/17 EU Eurostat CPI MoM November -0.2% -0.2% 0.2% 12/18 Germany IFO Institute IFO Business Climate December 101.0 101.7 102.0 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar Qatar’s corporate sector seen set for more listings in 2019 – Qatar’s corporate sector is slated to see more listings in 2019, indicating the growing confidence in the country’s bourse, which is the best performer in the Gulf so far this year. Several entities, which include family-owned firms, are making a beeline to get listed and it is learnt that two listings – one from the agriculture and another from the pharmaceuticals sectors are expected soon. Qatar Stock Exchange’s (QSE) CEO, Rashid Bin Ali Al-Mansoori said, “We are working on number of requests. We are keen to have more listings in 2019.” He added there are many (in the pipeline) and it is up to them to decide on when to get listed. Highlighting that Qatar Aluminium Manufacturing Company has set a benchmark; Al-Mansoori said the Qatar Petroleum company became public within six months of deciding to go in that direction and it will prompt others to follow suit. “At least one or two will be listed in the days to come, but it is up to them (as to when to enter the market),” he said, adding they are in healthcare /pharmaceutical and agriculture sectors. Fast growing domestic dairy major Baladna has already disclosed its plans to get listed and is now in the process of setting the books in order. There were reports that Qatar Pharma and Rayyan Water are also planning foray on the QSE. The new listings are expected to give a fillip to the market in terms of liquidity as well as depth and breadth; which in turn, has a direct bearing in on the exchange traded funds’ performance, according to market experts. (Gulf-Times.com) Qatar’s economy to expand 2.5% in 2018 – Qatari economy will expand 2.5% in 2018, 2.9% in 2019 and 3.3% in 2020, according to a survey conducted by Bloomberg News. CPI for 2018 forecasted at +0.9% YoY versus prior survey of +1%. CPI for 2019 forecasted at +2% YoY versus prior survey of +2.5%. (Bloomberg) Qatar’s Ministry of Finance explained tax overhaul for 2019 – Qatari Ministry of Finance explained the tax overhaul for 2019. The changes include: 1) A 100% selective tax rate on tobacco products and energy drinks. 2) A 50% selective tax rate on sugary drinks. 3) An income tax exemption for residents and citizens. 4) An exemption for shares listed on a stock exchange for specified industries. 5) The establishment of a general tax authority under the Ministry of Finance. The changes will be effective from January 1, 2019. (Bloomberg) Al-Kuwari: Qatar ties stronger despite blockade – Qatar, which has been under a blockade for one and a half years, strengthened relations with its global partners and put up an excellent performance, as evidenced by the remarkable economic growth this year, according to Minister of Commerce and Industry, HE Ali bin Ahmed Al-Kuwari. "Qatar’s foreign trade has risen by 16% despite the siege," he said. Highlighting that Qatar has accomplished a great deal during this period; he said the lessons that Qatar has acquired over the past 18 months would have taken a considerable period of time to assimilate, but numerous opportunities were created within the framework of the Qatar National Vision 2030 to accelerate the vision’s implementation. "Qatar has opened to the world and engaged the international community, which has reacted positively, noting that globalization and national interests should go hand-in-hand," he said, adding the world has turned into a small village where no country can thrive in isolation. Qatar’s openness to tourists and foreign companies looking to invest in the industrial sector are an essential part of the long- Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 42.99% 64.74% (79,315,274.22) Qatari Institutions 7.97% 13.59% (20,472,125.68) Qatari 50.96% 78.33% (99,787,399.90) GCC Individuals 0.77% 0.44% 1,210,682.84 GCC Institutions 0.76% 0.87% (396,305.24) GCC 1.53% 1.31% 814,377.60 Non-Qatari Individuals 10.66% 9.15% 5,510,697.99 Non-Qatari Institutions 36.85% 11.21% 93,462,324.31 Non-Qatari 47.51% 20.36% 98,973,022.30

- 3. Page 3 of 7 term journey that Qatar is pursuing, the Minister said, noting that these policies were unrelated to the blockade and adopted prior to the blockade. (Gulf-Times.com) WTO accepts Qatar request to set up panel in case against Saudi Arabia for violating IP rights – The World Trade Organisation (WTO) has agreed to Qatar’s request for the establishment of a WTO panel to rule in a case field against Saudi Arabia for violating intellectual property (IP) rights of Qatari citizens and companies including the rights of television broadcasters. This was decided at a WTO meeting for Settlement of Disputes, the Ministry of Commerce and Industry (MCI) stated. The complaint highlighted the various infringements and violations committed by Saudi Arabia against the IP rights of Qatari citizens and companies – including the rights of television broadcasters – and the piracy committed against beIN Media Group LLC. Additionally, the complaint outlined Saudi Arabia’s violation of its obligations to provide protection for IP rights holders under international treaties, as the Saudi authorities have prevented Qatari citizens and entities from exercising their most basic rights before law enforcement authorities in Saudi Arabia, in order to protect and defend their IP rights. (Gulf-Times.com) The Amir invited to attend Arab Summit in Tunisia – HH the Amir Sheikh Tamim Bin Hamad Al-Thani received a written message from Tunisian President, Beji Kayed Sibsi, inviting him to attend the 30th ordinary session of the Arab Summit to be held in Tunisia in March 2019. The meeting reviewed the fraternal relations and cooperation between Qatar and Tunisia and means of enhancing them. (Gulf-Times.com) FTSE Russell announces the fast entry of QAMC as a new constituent in FTSE All-World Index, FTSE Global Mid Cap Index and FTSE Emerging Index – FTSE Russell has published changes in FTSE indices regarding the fast entry of Qatar Aluminum Manufacturing Company (QAMC) as a new constituent in FTSE All-World Index, FTSE Global Mid Cap Index and FTSE Emerging Index. The changes to the FTSE Secondary Emerging Market index will be from December 24, 2018 (from start of trading). (QSE) Vodafone Qatar deploys 5G in Souq Waqif – In celebration of Qatar National Day, Vodafone Qatar has deployed its 5G network in Souq Waqif as the business continues to develop its 5G footprint around the country. Souq Waqif becomes the latest popular city centre location to be covered by Vodafone’s 5G network and closely follows the 5G deployment last week in Katara Cultural Village, allowing thousands of visitors to experience the superfast, seamless connectivity. The news builds on Vodafone Qatar’s extensive investment and commitment to date in supporting world-class infrastructure in Qatar and bringing new technologies to life. In support of the Qatar National Vision 2030, the company’s development of 5G services will accelerate the country towards becoming one of the most technologically advanced in the world, unlocking the transformative potential of 5G, thus enhancing the quality of lives and helping to drive economic growth and productivity in Qatar. (Gulf-Times.com) Qatar Airways’ CEO: Qatar Airways added 23 new destinations in 18 months – Qatar Airways has added some 23 new destinations over the past 18 months, something which has never been achieved by any other airline, according to Qatar Airways’ CEO, Akbar Al-Baker. “This is a key indicator of the airline’s sustainability and resilience”, Al-Baker said. The award-winning airline has launched 23 destinations since the start of the blockade, and continues with its significant program of expansion of new routes to further connect passengers around the globe. Al-Baker also addressed the airline’s proven track record of creating a large hub in the midst of tough competition, and emphasized the tremendous potential the airline sees in launching new routes to under- served countries in Africa and Asia, to connect passengers around the world via the airline’s home and hub, Hamad International Airport (HIA). (Gulf-Times.com) International BoAML: Investors gloomiest in a decade about world economy – Investor outlooks have deteriorated to their most pessimistic in a decade, Bank of America Merrill Lynch’s (BoAML) December investor survey showed. A net 53% of investors surveyed, who manage $694bn in assets, stated they expect global growth to weaken over the next 12 months, according to the poll. (Reuters) Asian business confidence wallows near three-year low on trade worries – A very cautious optimism remains among Asian companies in the fourth quarter as they wait to see whether there will be any breakthrough in a trade dispute between the US and China, a Thomson Reuters/INSEAD survey showed. Representing the six-month outlook of 84 firms, the Thomson Reuters/INSEAD Asian Business Sentiment Index edged up to 63 in the October-December quarter, slightly above a near three-year low of 58 seen in the previous period. However the latest result still marks one of the lowest readings since a rout in Chinese stocks in mid-2015 rattled world markets. (Reuters) US housing starts rise; single-family segment still weak – US homebuilding rebounded in November, driven by a surge in multi-family housing projects, but construction of single-family homes fell to 1-1/2-year low, pointing to deepening housing market weakness that could spill over to the broader economy. The report from the Commerce Department also showed housing starts fell in October instead of rising as previously reported. Underscoring the housing market weakness, single- family home completions dropped for a third straight month in November to their lowest level in more than a year. Housing starts increased 3.2% to a seasonally adjusted annual rate of 1.256mn units last month. Data for October was revised down to show starts dropping to a rate of 1.217mn units instead of the previously reported pace of 1.228mn units. (Reuters) UK’s economy set for slowest growth since 2009 as Brexit nears – British economic growth this year and in 2019 looks set to be the weakest since the country’s last recession, due to a freeze in business investment and weak consumer demand ahead of Brexit, the British Chambers of Commerce (BCC) forecasted. The business lobby said growth in 2018 was likely to slow to 1.2% before inching up to 1.3% in 2019, which would be the two weakest years since Britain emerged from recession in 2009 after the global financial crisis. (Reuters) Eurozone’s November inflation revised down to ECB target, October trade surplus falls – Eurozone’s headline inflation was at the European Central Bank (ECB) target in November and the

- 4. Page 4 of 7 inflation measure crucial for monetary policy decisions eased again after rising the previous month, revised data showed. The European Union’s statistics office stated consumer prices in the 19 countries sharing the Euro eased 0.2% MoM in November for 1.9% YoY increase, revised down from the previously reported 2.0%. The ECB wants to keep headline inflation below, but close to 2% over the medium term. Separately, Eurostat stated the Eurozone’s trade surplus with the rest of the world was EUR1.4bn in October, down from EUR17.8bn a year earlier as exports jumped 11.4% YoY in October while imports surged 14.8%. (Reuters) German economy faces lean Christmas as business morale sinks; economy cooling but no recession looming – German business morale fell in December, a survey indicated, suggesting that concerns among company executives about the growth outlook for Europe’s biggest economy are rising. The Munich-based Ifo economic institute stated its business climate index fell for the fourth month in a row to 101.0, its lowest level in more than two years. This was weaker than a Reuters consensus forecast of 101.8. The German economy is cooling but there is no recession in sight, an economist at Ifo stated after the institute’s monthly survey showed the business climate in Europe’s largest economy deteriorating. (Reuters) Japan’s exports slow to crawl on global growth woes, trade tensions – Japan’s export growth slowed to a crawl in November as shipments to the US and China weakened sharply, in a sign slowing external demand and a Sino-US trade dispute may leave the world’s third-largest economy underpowered over the next year. The 0.1% YoY rise in exports undershot 1.8% annual increase expected by economists in a Reuters poll, and was well below 8.2% jump in October. In volume terms, exports fell 1.9% in the year to November. Analysts expected exports to be a drag on the economy over the coming quarters as external demand ebbs. Policy makers will also have to consider the risks from the China-US trade war which have yet to play out in Japan’s shipment figures. (Reuters) Japan cuts GDP, CPI forecasts on disasters and trade war – Japan’s government revised down its forecasts for economic growth and consumer prices for the current and next fiscal years as natural disasters and weakening export demand weighed on the economy, the Cabinet Office stated. The forecast cuts follow disappointing data on quarterly gross domestic product and machinery orders, highlighting the growing downside risks posed by a trade war between the US and China. The government will use the forecasts to finalize the state budget for the next fiscal year starting in April, which could present policymakers with a host of challenges as they prepare to raise the nationwide sales tax. Japan’s economy will grow 0.9% in fiscal 2018, which ends in March, the Cabinet Office stated. That is down from its previous projection of 1.5% growth. In fiscal 2019 the economy will expand 1.3%, also down from the previous forecast of 1.5% growth. (Reuters) Regional MENA sees rise in Chinese contracts in oil & gas – The MENA region saw an estimated $287bn-worth of major contract awards in the oil, gas and petrochemicals sectors from January 2012 to September 2017, according to MEED Projects. In 2016, project activity in the MENA region witnessed the lowest spending since 2008, with the value of contract awards declining to $36.2bn from $59.9bn in 2015. Project awards significantly fared better in 2017, region’s leading market intelligence platform noted. (Peninsula Qatar) Gulf petrochemical companies earnings rise to $7.6bn in 2018 – The earnings of GCC petrochemical companies for the year surged by 2% to $7.57bn compared to the last year's figures of $7.45bn, a report released ahead of ArabPlast 2019 in Dubai stated. (GulfBase.com) Saudi Arabia's 2019 budget deficit projected at SR131bn – The 2019 spending is estimated at SR1.106tn and budget deficit at SR131bn. The revenues for 2019 is estimated at SR975bn. The government has decided to increase its spending by 7% next year. (Bloomberg) Saudi Arabia collects twice as much VAT as expected in 2018: budget document – Saudi Arabia collected SR45.6bn from value-added tax (VAT) in 2018, more than double its initial estimate, budget documents showed. The Saudi Arabia’s budget expects total tax revenues of SR166bn this year, up from an initial estimate of SR142bn, the document showed. The Saudi Arabian government has stated that it expects VAT, which was introduced earlier this year, to be one of the main generators of non-oil revenue. (Reuters) Saudi Arabia’s finance minister says PIF policy is based on medium to long-term investments – Saudi Arabia’s finance minister, Mohammed Al-Jadaan said that the policy of the country’s sovereign fund, Public Investment Fund (PIF), is based on medium to long-term investments, and it did not contribute revenues to 2018 and 2019 budgets. PIF, which is chaired by Crown Prince Mohammed bin Salman, manages over $250bn in assets including stakes in Uber Technologies. (Reuters) Saudi Arabia’s crown prince expects non-oil revenue to rise 9% in 2019 – Saudi Arabia’s Crown Prince Mohammed bin Salman said that the government expects non-oil revenue to increase to SR313bnin 2019, up from SR287bn in 2018, according to state news agency SPA. (Reuters) JODI: Saudi Arabia’s oil refinery output falls to 2.63mn bpd in October – The JODI-Oil World Database in Riyadh has published country data on refined oil balance for October stating that Saudi Arabia’s total oil refinery output fell 7.7% to 2.63mn in October from 2.848mn bpd in September, and fell 12.4% YoY. The gas and diesel oil output fell 13.6% to 0.97mn bpd in October, and fell 15.7% YoY. Saudi Arabia exported 2.069mn bpd of refined oil in October. (Bloomberg) Utilities digitization powers growth of KSA’s largest industrial cities – The Saudi Arabian utility sector undergoes digital transformation to optimize its operations, modernize its infrastructure, and reshape offerings, all aligned with Saudi Arabia’s Vision 2030, Saudi Arabian utilities provider, Marafiq, has embarked on enhancing its digital intelligence with SAP. Marafiq provides power and utility infrastructure to industrial cities within Saudi Arabia, which hosts some of the world’s largest hydrocarbon conglomerates in Yanbu and Jubail. Digital transformation presents a strong growth opportunity in leveraging innovative approaches and refreshed business directions. Marafiq plays a prominent role in powering the next- wave of growth for the Saudi Arabia’s Vision 2030 industrial

- 5. Page 5 of 7 ventures through the establishment of intelligent, digital power, and utility facilities. (GulfBase.com) Saudi Arabia's Falih discusses joint refining projects with Reliance – India’s Reliance, operator of the world’s biggest refining complex, and top oil exporter Saudi Arabia will explore joint investments in refining and petrochemicals in the two countries, Saudi Arabian Energy Minister Khalid Al-Falih said. Al-Falih said that he met Reliance Industries chairman Mukesh Ambani and they discussed joint investment opportunities and cooperation in petrochemicals, refining and telecoms in their two countries. Reliance’s two oil refineries in western India have a combined capacity to process 1.4mn barrels per day of crude and the company has set a target to raise capacity by a further 600,000 bpd. (Reuters) UAE's Utico plans stock market listing, hires ENBD Capital – The UAE’s utility Utico Middle East has hired Emirates NBD Capital for a potential share sale and public listing, the company stated. Utico, the only privately-owned utility in the UAE, also stated that a trans-Emirate water pipeline built at a cost of $100mn was now operational. Demand for water and power in the UAE is expected to grow by 5% to 6% annually in the next few years as the population grows and industrialization spreads, according to estimates by state- owned utilities. “We are looking at a public listing in the near future,” CEO of Utico, Richard Menezes said. (Reuters) UAE's Mubadala, EGA & Dubal Holding to develop water & power plant in Dubai – Emirates Global Aluminium (EGA), Mubadala Investment Co. and Dubal Holding announced plans to develop a power and water desalination plant at EGA’s smelter in Jebel Ali in Dubai. The 25-year agreement is worth more than $272.5mn, the companies stated. The joint venture will install a combined cycle power facility at EGA’s Jebel Ali site capable of generating over 600 megawatts of electricity. (Reuters) Dubai DED issues 1,748 new licenses in November – Dubai Department of Economic Development (DED) stated that the business registration and licensing (BRL) has issued a total of 1,748 new licenses in November even as the Emirate remains a destination of choice for investment in diverse business sectors. Out of these new licenses issued, 62.3% were commercial, 35.2% professional, 1.3% related to tourism and 1.2% industry, DED stated. (GulfBase.com) DP World, SMS to deploy smart storing system at Dubai port – Dubai-based global marine terminal operator DP World stated that an international joint-venture formed with industrial engineering specialists SMS group will revolutionize the way that containers are handled in ports. As part of its plan to deploy disruptive technology to radically improve operations, DP World will apply the new intelligent storing system at Jebel Ali Terminal 4, in time for the Dubai Expo 2020 world fair. The High Bay Storage system was originally developed by SMS group subsidiary Amova for round the clock handling of metal coils that weigh as much as 50 tons each in racks as high as 50 meters, DP World stated. Amova is the first company to transfer this proven technology to the port industry. Instead of stacking containers directly on top of each other, which has been global standard practice for decades, the system places each container in an individual rack compartment, it stated. (GulfBase.com) Ajman clears ‘zero-deficit budget’ – Supreme Council Member and Ruler of Ajman, HH Sheikh Humaid Bin Rashid Al Nuaimi approved the general budget of the Ajman Government for 2019 to 2021. The budget amounts to AED4.140bn, a growth of 17%. The general budget for the 2019 fiscal year was also approved, as part of a financial plan valued at AED1.380bn and without a deficit. Crown Prince of Ajman and Chairman of the Ajman Executive Council, Sheikh Ammar Bin Humaid Al Nuaimi said that the Ajman Government’s budget reflects the directives of Sheikh Humaid and the Ajman Vision 2021, to achieve the well- being and happiness of the Emirate’s citizens and residents, as well as to provide the best services and ensure fiscal sustainability and the Emirate’s competitiveness, in line of the UAE 2021 National Agenda. The budget aims to promote investment in the Emirate’s infrastructure and community facilities, through providing social support and serving citizens and residents, he added. (GulfBase.com) JODI: Kuwait’s crude oil exports fall to 2.058mn bpd in October – The crude oil exports fell 0.4% to 2.058mn bpd in October from 2.067mn bpd in September, and rose 3.7% YoY. Kuwait produced 2.733mn bpd of crude oil in October. The crude oil output fell 0.7% from 2.752mn bpd in September, and rose 1.2% YoY. Refinery intake fell 1.8% to 0.665mn bpd in October, and declined 2.2% YoY. (Bloomberg) MoCI: Kuwait’s non-oil exports up to 25.2% in November – Kuwait’s non-oil exports went up to 25.2% in November compared to November 2017, Kuwait’s Ministry of Commerce and Industry (MoCI) stated. Total exports were about KD13.4mn during November compared to KD7.9mn in November 2017, the ministry stated. Arab countries accounted for 83% of Kuwait’s total exports with KD11.1mn. The rest of the world accounted for 17% with KD2.2mn. Qatar was the highest ranked country to import at KD4.3mn, after that Saudi Arabia with KD2.6mn. (GulfBase.com) Oman's bonds tumble as Fitch cuts credit rating to junk – Oman’s Dollar-denominated government bonds fell after Fitch became the second major rating agency to cut the country to ‘junk’. Fitch’s move leaves Moody’s as the only firm to rate Oman as investment grade, a level key for keeping a country’s debt in the major indexes tracked by fund managers. (Reuters) Oman seeks international investment to develop ultra-heavy oilfield – Oman’s Ministry of Oil & Gas stated that it will open its ultra-heavy oilfield at Habhab in south Oman to investment and development by international players with the technological and financial wherewithal to unlock the field’s promising, but technically challenging, resources. Habhab, a large, heavy and very viscous oil accumulation that currently forms part of the Block 6 concession of Petroleum Development Oman (PDO), is proposed to be carved out and offered up to international energy firms with the knowhow to harness the reservoir’s almost bitumen-like hydrocarbons. According to Director General of Management of Petroleum Investments at the Ministry, Salman bin Mohammed al Shidi, Habhab will be “packaged separately” to companies that have the technical capabilities to handle heavy oil resources. “We will be open to companies that have the technical might and the investment,

- 6. Page 6 of 7 firstly to study the reservoir and then to put together a proposal to unlock its heavy oil,” he said. (GulfBase.com) Oman awards Blocks 51, 65 to Oxy, OOCEP – Occidental of Oman, the local subsidiary of Occidental Petroleum (Oxy), signed Exploration and Production Sharing Agreements (EPSA) for two new hydrocarbon blocks, effectively ramping up its expanding portfolio of upstream investments in the Sultanate. Under the EPSA pacts, Oxy Oman acquires a 100% interest in Block 51, covering a 10,133 sq km area in the northeast of the country. Separately, a joint venture of Oxy Oman and Oman Oil Company Exploration & Production (OOCEP) has been awarded Block 65, a small 1230 sq km concession located in the interior of Oman. Minister of Oil & Gas, Mohammed bin Hamad al Rumhy signed the agreements. (GulfBase.com) Oman sells OMR31.57mn 91-day bills; bid-cover 1.02x – Oman sold OMR31.57mn of bills due on March 20, 2019 on December 17. Investors offered to buy 1.02 times the amount of securities sold. The bills were sold at a price of 99.42, having a yield of 2.335% and will settle on December 19. (Bloomberg) Moody's changes outlook on Bahrain's rating to stable, affirms ‘B2’ rating – Moody's Investors Service has changed the outlook to ‘Stable from ‘Negative’ on the Government of Bahrain's issuer ratings and affirmed the ratings at B2. The key driver of the outlook change to stable is Moody's assessment that Bahrain's government and external liquidity risks, while remaining elevated, have materially reduced following the announcement of a $10bn financial support package from Bahrain's Gulf Cooperation Council (GCC) neighbors. Financial support and the fiscal consolidation measures (the Fiscal Balance Program, FBP) that are set to accompany it will support investors' confidence and help to reduce the government's financing needs. In turn, this will slow a further weakening in Bahrain's public finances in a way that is consistent with a ‘B2’ rating. (Moody’s)

- 7. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa QNB Financial Services Co. W.L.L. Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg,( # Data as on December 17, 2018) Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 45.0 70.0 95.0 120.0 Nov-14 Nov-15 Nov-16 Nov-17 Nov-18 QSE Index S&P Pan Arab S&P GCC (0.3%) (0.1%) (0.2%) (0.4%) (0.7%) (0.8%) (2.1%)(2.4%) (1.6%) (0.8%) 0.0% 0.8% SaudiArabia Qatar# Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,249.42 0.3 0.9 (4.1) MSCI World Index 1,908.16 (0.3) (1.8) (9.3) Silver/Ounce 14.64 (0.2) 0.4 (13.6) DJ Industrial 23,675.64 0.4 (1.8) (4.2) Crude Oil (Brent)/Barrel (FM Future) 56.26 (5.6) (6.7) (15.9) S&P 500 2,546.16 0.0 (2.1) (4.8) Crude Oil (WTI)/Barrel (FM Future) 46.24 (7.3) (9.7) (23.5) NASDAQ 100 6,783.91 0.4 (1.8) (1.7) Natural Gas (Henry Hub)/MMBtu 3.70 (2.6) (7.3) 19.7 STOXX 600 340.46 (0.7) (1.4) (17.3) LPG Propane (Arab Gulf)/Ton 64.25 (4.8) (6.9) (35.1) DAX 10,740.89 (0.2) (0.6) (21.4) LPG Butane (Arab Gulf)/Ton 66.75 (5.0) (7.9) (38.5) FTSE 100 6,701.59 (0.9) (1.6) (18.6) Euro 1.14 0.1 0.5 (5.4) CAC 40 4,754.08 (0.9) (1.5) (15.4) Yen 112.52 (0.3) (0.8) (0.2) Nikkei 21,115.45 (1.6) (0.6) (7.3) GBP 1.26 0.1 0.4 (6.5) MSCI EM 962.98 (0.5) (0.9) (16.9) CHF 1.01 0.0 0.6 (1.8) SHANGHAI SE Composite 2,576.65 (0.8) (0.5) (26.5) AUD 0.72 0.0 0.1 (8.0) HANG SENG 25,814.25 (1.1) (1.2) (13.8) USD Index 97.10 0.0 (0.3) 5.4 BSE SENSEX 36,347.08 1.8 3.1 (3.3) RUB 67.29 0.8 0.8 16.8 Bovespa 86,610.49 (0.1) (1.0) (3.9) BRL 0.26 (0.4) 0.2 (15.3) RTS 1,106.05 (0.7) (0.9) (4.2) 83.6 80.0 77.7