1. Page 1 of 7

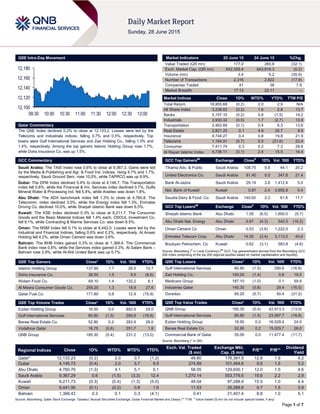

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 0.2% to close at 12,133.2. Losses were led by the

Telecoms and Industrials indices, falling 0.7% and 0.5%, respectively. Top

losers were Gulf International Services and Zad Holding Co., falling 1.5% and

1.4%, respectively. Among the top gainers Islamic Holding Group rose 1.7%,

while Doha Insurance Co. was up 1.5%.

GCC Commentary

Saudi Arabia: The TASI Index rose 0.6% to close at 9,367.3. Gains were led

by the Media & Publishing and Agr. & Food Ind. indices, rising 4.7% and 1.7%,

respectively. Saudi Ground Serv. rose 10.0%, while TAPRCO was up 9.9%.

Dubai: The DFM Index declined 0.4% to close at 4,146.7. The Transportation

index fell 0.8%, while the Financial & Inv. Services index declined 0.7%. Gulfa

Mineral Water & Processing Ind. fell 5.4%, while Arabtec was down 1.8%.

Abu Dhabi: The ADX benchmark index fell 1.3% to close at 4,760.8. The

Telecomm. index declined 3.5%, while the Energy index fell 1.3%. Emirates

Driving Co. declined 10.0%, while Sharjah Islamic Bank was down 6.5%.

Kuwait: The KSE Index declined 0.3% to close at 6,211.7. The Consumer

Goods and the Basic Material Indices fell 1.4% each. OSOUL Investment Co.

fell 9.1%, while Contracting & Marine Services Co. was down 8.5%.

Oman: The MSM Index fell 0.1% to close at 6,442.0. Losses were led by the

Industrial and Financial Indices, falling 0.6% and 0.2%, respectively. Al Anwar

Holding fell 4.2%, while Oman Cement was down 3.6%.

Bahrain: The BHB Index gained 0.3% to close at 1,368.4. The Commercial

Bank index rose 0.6%, while the Services index gained 0.3%. Al Salam Bank –

Bahrain rose 2.9%, while Al-Ahli United Bank was up 0.7%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 137.80 1.7 28.5 10.7

Doha Insurance Co. 26.50 1.5 9.5 (8.6)

Widam Food Co. 64.10 1.4 132.2 6.1

Al Meera Consumer Goods Co. 255.20 1.3 18.9 27.6

Qatar Fuel Co. 171.80 0.6 12.9 (15.9)

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 18.50 0.0 892.4 24.0

Gulf International Services 80.80 (1.5) 290.6 (16.8)

Barwa Real Estate Co. 52.80 0.2 283.9 26.0

Vodafone Qatar 16.75 (0.6) 251.7 1.8

QNB Group 185.30 (0.4) 231.2 (13.0)

Market Indicators 25 June 15 24 June 15 %Chg.

Value Traded (QR mn) 177.0 260.6 (32.1)

Exch. Market Cap. (QR mn) 642,359.4 643,816.3 (0.2)

Volume (mn) 3.4 5.2 (35.9)

Number of Transactions 2,316 2,822 (17.9)

Companies Traded 41 38 7.9

Market Breadth 17:13 22:11 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,855.68 (0.2) 2.0 2.9 N/A

All Share Index 3,238.62 (0.2) 1.6 2.8 13.7

Banks 3,157.10 (0.2) 0.8 (1.5) 14.2

Industrials 3,930.32 (0.5) 1.7 (2.7) 13.9

Transportation 2,463.69 (0.1) 0.4 6.3 13.6

Real Estate 2,821.25 0.1 4.9 25.7 9.9

Insurance 4,744.27 0.4 0.8 19.8 21.9

Telecoms 1,164.91 (0.7) 0.5 (21.6) 23.4

Consumer 7,411.74 0.3 0.2 7.3 28.8

Al Rayan Islamic Index 4,736.11 (0.1) 2.4 15.5 14.4

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Tihama Adv. & Public Saudi Arabia 108.75 9.8 44.1 20.2

United Electronics Co. Saudi Arabia 81.40 5.0 347.8 21.4

Bank Al-Jazira Saudi Arabia 29.19 3.8 1,412.4 5.0

Nat. Bank of Kuwait Kuwait 0.87 2.4 3,955.8 0.4

Saudia Dairy & Food. Co. Saudi Arabia 140.00 2.2 61.6 17.7

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Sharjah Islamic Bank Abu Dhabi 1.59 (6.5) 1,600.0 (9.7)

Abu Dhabi Nat. Energy Abu Dhabi 0.67 (4.3) 542.5 (16.2)

Oman Cement Co Oman 0.53 (3.6) 1,222.0 2.3

Emirates Telecom Corp. Abu Dhabi 14.00 (3.4) 3,113.5 40.6

Boubyan Petrochem. Co Kuwait 0.62 (3.1) 583.8 (4.6)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Gulf International Services 80.80 (1.5) 290.6 (16.8)

Zad Holding Co. 100.00 (1.4) 0.6 19.0

Medicare Group 187.10 (1.0) 0.1 59.9

Industries Qatar 140.30 (0.8) 29.4 (16.5)

Ooredoo 85.20 (0.7) 50.4 (31.2)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

QNB Group 185.30 (0.4) 42,913.3 (13.0)

Gulf International Services 80.80 (1.5) 23,597.7 (16.8)

Ezdan Holding Group 18.50 0.0 16,528.4 24.0

Barwa Real Estate Co. 52.80 0.2 15,029.7 26.0

Commercial Bank of Qatar 55.00 0.0 11,477.4 (11.7)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,133.23 (0.2) 2.0 0.7 (1.2) 48.60 176,391.9 12.8 1.9 4.2

Dubai 4,146.73 (0.4) 2.0 5.7 9.9 274.89 101,494.6 9.6 1.5 5.2

Abu Dhabi 4,760.76 (1.3) 4.1 5.1 5.1 58.05 129,600.1 12.0 1.5 4.6

Saudi Arabia 9,367.29 0.6 (1.5) (3.3) 12.4 1,270.14 553,779.5 19.6 2.2 2.9

Kuwait 6,211.73 (0.3) (0.4) (1.3) (5.0) 48.04 97,288.9 15.5 1.0 4.4

Oman 6,441.95 (0.1) (0.2) 0.8 1.6 11.53 25,289.8 9.7 1.5 3.9

Bahrain 1,368.43 0.3 0.1 0.3 (4.1) 0.41 21,401.4 8.8 1.0 5.1

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,100

12,120

12,140

12,160

12,180

09:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QSE Index declined 0.2% to close at 12,133.2. The

Telecoms and Industrials indices led the losses. The index fell on

the back of selling pressure from non-Qatari shareholders

despite buying support from Qatari and GCC shareholders.

Gulf International Services and Zad Holding Co. were the top

losers, falling 1.5% and 1.4%, respectively. Among the top

gainers Islamic Holding Group rose 1.7%, while Doha Insurance

Co. was up 1.5%.

Volume of shares traded on Thursday fell by 35.9% to 3.4mn

from 5.2mn on Wednesday. Further, as compared to the 30-day

moving average of 14.7mn, volume for the day was 77.1% lower.

Ezdan Holding Group and Gulf International Services were the

most active stocks, contributing 26.5% and 8.6% to the total

volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Ratings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Bank Sohar

Capital

Intelligence

Oman

FSR/LT FCR/ST

FCR/SR

BBB/BBB+/A3/2 BBB/BBB+/A3/2 – Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

06/25 US Markit Markit US Composite PMI June 54.6 – 56.0

06/25 US Markit Markit US Services PMI June 54.8 56.5 56.2

06/25 US Bloomberg Bloomberg Consumer Comfort 21-June 42.6 – 40.9

06/25 US Bureau of Eco. Analysis Personal Income May 0.50% 0.50% 0.50%

06/25 US Bureau of Eco. Analysis Real Personal Spending May 0.60% 0.50% 0.00%

06/25 US Bureau of Eco. Analysis PCE Deflator YoY May 0.20% 0.20% 0.20%

06/25 US Bureau of Eco. Analysis PCE Core YoY May 1.20% 1.20% 1.30%

06/26 EU European Central Bank M3 Money Supply YoY May 5.00% 5.40% 5.30%

06/26 EU European Central Bank M3 3-month average May 5.00% 5.10% 4.70%

06/26 France INSEE Consumer Confidence June 94.0 93.0 94.0

06/25 Germany GfK AG GfK Consumer Confidence July 10.1 10.2 10.2

06/26 Germany Destatis Import Price Index MoM May -0.20% 0.20% 0.60%

06/26 Germany Destatis Import Price Index YoY May -0.80% -0.40% -0.60%

06/25 Spain INE PPI MoM May 0.30% – 0.50%

06/25 Spain INE PPI YoY May -1.40% – -0.90%

06/26 Spain INE Total Mortgage Lending YoY April 0.30% – 7.30%

06/26 Spain INE House Mortgage Approvals YoY April 21.40% – 19.70%

06/26 Italy ISTAT Consumer Confidence Index June 109.5 105.6 106.0

06/26 Italy ISTAT Business Confidence June 103.9 103.8 103.4

06/26 Italy ISTAT Economic Sentiment June 104.3 – 101.8

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 61.71% 49.17% 22,206,492.78

GCC 6.96% 5.73% 2,168,600.50

Non-Qatari 31.33% 45.10% (24,375,093.28)

3. Page 3 of 7

News

Qatar

AHCS to disclose financials on July 15 – Aamal Company

(AHCS) will announce the financial reports for the period ending

June 30, 2015 on July 15, 2015. (QSE)

BMI: Positive outlook for consumer electronics market –

According to Business Monitor International (BMI), high

consumer spending power coupled with rapid population growth

will see Qatar’s consumer electronics market developing with

computer hardware sales projected at QR2.4bn by 2019.

Computer hardware sales currently account for around QR2bn.

BMI’s positive outlook for Qatar’s consumer electronics market

is underpinned by high consumer spending power, rapid

population growth from the influx of migrant workers and the

government’s continued commitment to investment in the ICT

sector, as part of its goal to reduce the country’s dependence on

hydrocarbons. The government’s expansionary policies have

resulted in a rapidly growing population of migrant workers to

support the construction and hospitality sectors. This in turn

drives volume growth in the consumer electronics market, while

an expanding tourism sector is boosting demand for audio/video

devices. Meanwhile, BMI said that there remain considerable

subscriptions and revenue growth opportunities for the country’s

telecom sector despite Qatar’s small population and one of the

highest mobile penetration rates in the region. BMI added that

Qatar’s mobile market served 4.125mn subscribers at the end of

2014, reflecting a YoY increase of 10.8% despite saturation.

BMI forecasts 3.053mn subscribers in 2019. Market weighted

average mobile revenue per unit (ARPU) depreciated by 2.7%

YoY in 4Q2014; ARPU is forecasted to sink to QR110.3 by

2019. (Gulf Times)

BP: Qatar ranked third in world natural gas reserves –

According to British Petroleum’s (BP) 'Statistical Review of

World Energy' report, Qatar holds about 13.1% of the world's

total proven gas reserves, and stands third in the world in terms

of natural gas reserves. Iran possesses the world's largest

proven natural gas reserves with 18.2%. Russia has the second

largest gas reserves with 17.4% and the Middle East holds

about 42.7% of the total gas reserves. The report said global

energy consumption slowed sharply to an increase of 0.9% in

2014. The slow growth of energy demand was largely due to

China's economy moving away from energy-intensive sectors.

(Zawya)

GISS: QP not to directly award contracts to affiliates – Gulf

International Services (GISS) announced that Qatar Petroleum

(QP) has decided not to assign contracts by direct agreement

with the concerned companies, including wholly or partly-owned

companies by QP or its subsidiaries. QP’s decision is part of its

role to emphasize the importance of strengthening the principals

of fair and equal competition by providing genuine participation

opportunities for all qualified parties. GISS, which has business

dealings with QP, welcomed the decision and considers it a

starting point for some of its subsidiaries, which have dealings

with QP, to strengthen their capabilities and resources as well

as expand functions and services provided in order for them to

be able, like all other companies working in the same field, to

compete in the local market. (QSE)

ictQatar plans law to protect digital privacy – The Ministry of

Information and Communications Technology (ictQatar) is

planning to issue a digital privacy law by the beginning of 2016.

The law will contain general rules regarding the protection of

personal information of internet users. (Peninsula Qatar)

Qatar to boost awareness of construction standards – Qatar

General Organization for Standardization (QS) has signed an

agreement with ASTM International, a leading US-based

standards development organization, to boost awareness of

international standards in the building & construction sector.

Under the terms of the agreement, Qatar Construction

Standards (QCS 2014) will be linked to ASTM’s interactive

database by establishing an online version, including direct links

to the full text of ASTM Standards referenced in QCS 2014. This

is to help speed up users’ access to all referenced ASTM

Standards and make QCS accessible to building & construction

experts, scientists and professionals worldwide, in a first step

toward globalization of QCS. (GulfBase.com)

DHBK inaugurates representative office in South Africa –

Doha Bank (DHBK) Group CEO Dr. R Seetharaman said the

bank hopes to attract the support of key South African banks to

initially establish Nostro account relationships in Gulf

Cooperation Council (GCC) currencies and Indian rupees, as

well as affording them trade finance support, risk sharing, and

syndication loans. Seetharaman made the statement during the

inauguration of DHBK’s representative office in Johannesburg,

South Africa held on June 25 in the presence of dignitaries and

other officials of the bank. (GulfBase.com)

International

US, China highlight progress amid tensions as meeting

ends – US and Chinese officials highlighted incremental gains

on financial and environmental issues at the conclusion of the

annual diplomatic and economic talks, without papering over

differences on cyber-spying and tensions in the South China

Sea. US Treasury Secretary Jacob J. Lew said that China

committed during the annual Strategic & Economic Dialogue to

limit foreign-exchange intervention only to times of “disorderly

market conditions.” Chinese vice Premier Wang Yang said the

US pledged to respect International Monetary Fund procedures

on China’s efforts to win reserve-currency status for the yuan. At

the same time, there was little sign of progress over difficult

strategic issues, from the perennial clash over human rights to

China’s recent construction of islands in the contested South

China Sea, and the nation’s alleged role in the theft of US

government workers’ data. Also hanging over the talks was a

US-led trade agreement that excludes China, with Obama

warning in April that if the US cannot come to terms on the

Trans-Pacific Partnership, China will step in to write the rules.

(Bloomberg)

EU aims to boost growth with cut in cost of selling pooled

debt – The European Union (EU) plans to stimulate economic

growth by tapping markets kicked off on Friday with banking

regulators proposing to cut the cost of raising funds from

bundled debt. Asset-backed securities (ABS), which re-parcel

debt based on loans such as mortgages, have struggled to

regain favor in Europe after the sector unraveled in the US in

2007 to spark financial turmoil. However, kick-starting ABS is

core to European Union plans for a capital markets union (CMU)

to boost the amount of market-generated funds to aid economic

growth. The hope is that by increasing banks' ability to refinance

loans and sell them to investors, they will be more inclined to

boost lending that injects money into the economy. The

European Banking Authority (EBA) published recommendations

on Friday to cut capital charges on "simple, transparent and

standardized" securitized debt that also includes quality checks

on the underlying loans. (Reuters)

Greek parliament gives go-ahead to Tspiras' bailout

referendum – Greek lawmakers on Sunday authorized Prime

Minister Alexis Tsipras' proposed July 5th bailout referendum,

setting Greece on course for a plebiscite that has enraged

4. Page 4 of 7

international creditors and increased Greece's chances of

exiting the Eurozone. Greeks are due to vote on whether to

accept or reject the latest terms offered by creditors to Athens in

order to unlock billions of euros in bailout funds. The

government easily passed the 151-vote threshold needed to

authorize the referendum. European partners have reacted

negatively to the announcement of the referendum. On

Saturday, they rejected a request by Tsipras to extend the

current bailout in order to cover the period leading up to the

referendum. The rejection means Athens is likely to default on a

key payment to the International Monetary Fund on June 30,

2015. (Reuters)

China cuts lending rates to record low after stocks slump –

China’s central bank reduced its benchmark lending rate to a

record low and lowered reserve-requirement ratios for some

lenders after stocks plunged and local government bond sales

drained liquidity. The People’s Bank of China said the one-year

lending rate will be reduced by 25 basis points (bps) to 4.85%

effective June 28, in the fourth reduction since November. The

one-year deposit rate will fall by 25 bps to 2%, while the reserve

ratios for some lenders including city commercial and rural

commercial banks will be cut by 50 bps. The easing follows the

biggest two-week plunge in the stock market since December

1996 and a four-week rise in money-market rates as lenders

hoard cash. (Bloomberg)

Brazil unemployment rises above forecast in May – Brazil’s

unemployment rate rose in May more than analysts forecast as

higher rates and tighter fiscal policy stifle activity in Latin

America’s biggest economy. The national statistics institute said

that the jobless rate increased to 6.7% from 6.4% in April.

Unemployment has spiked as the economy contracts with the

government tightening policy. That makes it a politically

inconvenient moment for President Dilma Rousseff’s

government to have restricted access to unemployment

insurance as part of its fiscal adjustment. Above-target inflation

is eating into real wages and further depressing sentiment, as

Rousseff’s approval rating plumbs new lows. (Bloomberg)

African Development Bank raises $1bn for infrastructure –

Donald Kaberuka, the outgoing President of the African

Development Bank said the institution raised almost $1bn in

contributions from regional governments for a fund to develop

roads, ports and energy projects. He said the bank now plans to

seek money from private African organizations, including

pension funds and insurance companies, and later investors

outside the continent. The lender has also asked African central

banks with “excess reserves,” and some having import-cover of

as many as 10 years, to invest part of that money in the fund.

The fund, known as Africa50 and endorsed last year by finance

ministers and central bank governors from across the region, is

targeting $3bn in initial fundraising and $10bn in the longer run.

Kaberuka said around $300mn will be spent on assessing the

financial viability of projects and preparing them for investment.

The fund, initially scheduled to be operational by March 2014,

will start working from July 2015. (Bloomberg)

Regional

GOIC: GCC SME investments reached $15.3bn in 2014 –

Gulf Organization for Industrial Consulting (GOIC) said that the

total investment by small & medium-sized enterprises (SMEs)

across the GCC countries reached $15.3bn in 2014. GOIC

Secretary General Abdulaziz bin Hamad al-Ageel said the

amount is equivalent to 4.1% of the total investments in the Gulf

industrial sector, which amounted to $380.1bn. He added that

$6bn of these investments were in small-scale industries and

$9.4bn in medium industries. He also said the number of small &

medium-sized factories in GCC countries was 13,480 in 2014,

including 10,809 small factories and 2,671 medium factories.

These factories represent 82.7% of the total number of

manufacturing industries in the GCC region estimated at 16,292.

GOIC data showed that small & medium-sized factories

accounted for 82.7% of the total number of factories operating in

manufacturing industries in 2014. (Gulf Times)

Alpen Capital: GCC construction sector foresees growth for

next three years – According to a GCC Construction Industry

report published by Alpen Capital, the GCC construction

industry foresees growth for the next three years, encouraged

by factors such as favorable macroeconomics, positive

demographics, and rising tourism activities. In Saudi Arabia,

efforts to boost religious tourism have translated into higher

budget allocations toward the hospitality, retail, and

infrastructure sectors. The need to create affordable housing

options and the recent law allowing for mortgages are expected

to result in an increase in construction activities in the near

future. Optimistic forecasts for the UAE's construction sector for

the next few years is based on an economic recovery, safe-

haven status, liberal investment climate, relatively advanced real

estate regulatory framework, as well as a buoyant infrastructure

project pipeline as part of the country’s strategic vision 2021.

The outlook for the Qatar’s residential, hospitality, and

infrastructure construction markets appears optimistic due to

healthy population growth, mega events, and the economy

picking up pace. Oman’s construction industry is expected to

remain robust driven by a significant increase in infrastructure

projects planned by the government, tourism projects, an

undersupplied residential market, as well as the construction of

commercial space. In Kuwait, the construction industry is set to

thrive driven by the infrastructure sector, new projects from the

private sector to address the need for affordable housing, and

an increase in demand for commercial space. Developing its

infrastructure and reducing its affordable housing shortage

remain the principal focus of the government of Bahrain in the

coming years. (GulfBase.com)

KHC, CDCIC to launch SR1.5bn jointly managed fund –

Kingdom Holding Company (KHC), an investment firm owned by

billionaire Prince Al Waleed bin Talal and Caisse des Dépôts

International Capital (CDCIC), have signed a deal to launch a

SR1.5bn jointly managed fund. Following establishment of the

investment fund, KHC and CDCIC will contribute SR375mn

each to the fund. As a later step, third party investors will be

invited to invest a total amount of SAR1.1bn and CDCIC has

already committed to contribute SR375mn for such second

round. After both rounds the total value of the fund will be

SR1.5bn. The investment strategy of the investment fund will be

to seek attractive investment opportunities in small & medium

size enterprises in Saudi Arabia with the participation of large

French corporate enterprises, in addition to diversifying KHC 's

investment portfolio. (GulfBase.com)

Saudi Aramco to raise stake in Luksar to 50%, plans

expansion at Shaybah oilfield – Saudi Arabian Oil Company

(Saudi Aramco) is planning to raise its share in Luksar, a joint

venture with Russia's Lukoil, to 50%. Lukoil has a majority stake

in Luksar but industry sources had said in April 2015 that the

company was likely to pull out from Saudi Arabia as the

economics of its search for gas have been crushed by the

collapse in oil prices. Meanwhile, Saudi Aramco is implementing

expansion plans at Shaybah field in the empty quarter to

increase oil production capacity and natural gas liquids (NGL) at

an estimated cost of SR186.75bn. Saudi Aramco's joint projects

in the field of refining and petrochemical production are

estimated at SR131.25bn. (GulfBase.com)

5. Page 5 of 7

Saudi Aramco plans cleaner fuels for Ras Tanura, Rabigh

refineries – According to sources, Saudi Arabian Oil Company

(Saudi Aramco) has revived plans to add a clean fuels unit at its

biggest oil refinery in Ras Tanura and more environmentally-

friendly units to its Rabigh refinery. Earlier, in January 2015,

Saudi Aramco had suspended plans to develop the $2bn project

in Ras Tanura due to the drop in oil prices. The company

invested $2.5bn with its partner Exxon Mobil to upgrade a

refinery on the Red Sea coast of Saudi Arabia to produce

cleaner fuels and is also upgrading its Riyadh refinery. Bidding

for construction in Ras Tanura is due to start in August 2015,

and ends in November 2015, with an award expected in March

2016. The completion of the plant is due in October 2019. On

the Red Sea coast, the company and Rabigh Sumitomo

Chemical in PetroRabigh are planning to build a hydro-

desulphurization unit and sulphur recovery unit as well as a new

polyols plant which will have a capacity of 220,000 tons per

year. The contracts are likely to be awarded in 1Q2016.

(Reuters)

Saudi Yasref refinery reaches full capacity milestone –

Yanbu Aramco Sinopec Refining Company (Yasref) said that its

new refinery had achieved milestone processing crude at full

capacity of 400,000 barrels per day (bpd). Yasref is a joint

venture between Saudi Arabian Oil Company (Saudi Aramco)

and China Petrochemical Corporation (Sinopec).

(GulfBase.com)

MasterCard: UAE tops MEA region for inclusive growth –

According to MasterCard’s 2015 Middle East and Africa

Inclusive Growth report, the UAE has topped countries in the

Middle East and Africa (MEA) region for inclusive growth, with a

score of 57.58. The report, which covers 34 countries, aims to

benchmark developing nations in the MEA region against the

developed countries of the Organisation for Economic

Cooperation and Development (OECD). As per the report, the

UAE’s score is 6.8 points behind the OECD average of 64.38,

and was followed by Qatar, with an index score of 55.2, Bahrain

(54.56), Saudi Arabia (51.45) and Oman (50.9). Factors

including the UAE’s diversification of its economy away from oil

& gas, encouragement of entrepreneurship and the

development of its education, healthcare and tourism sectors,

creating more jobs, have resulted in the county’s higher ranking

for inclusive growth, or sustainable output growth that is broad-

based across economic sectors, creating productive

employment opportunities and reducing poverty. (GulfBase.com)

UNCTAD: UAE remains second top FDI recipient in Middle

East – The United Nations Conference on Trade and

Development (UNCTAD), in its World Investment Report, said

that the UAE remained the second largest recipient of foreign

direct investment (FDI) in the Middle East after Turkey in 2014.

FDI flows into the UAE and Saudi Arabia the region’s second

and third largest recipients – registered slight declines and

remained about $10bn and $8bn respectively as Middle East

sustained its downward FDI trend in 2014 for the sixth

consecutive year, decreasing by 4%to $43bn. FDI remained

sluggish in the GCC countries, the region’s main FDI destination

(61% in 2009–2014). It was down by 4% to $22bn in 2014,

despite these states remaining relatively unscathed by political

unrest and enjoying robust economic growth in recent years.

(GulfBase.com)

UAE money supply increased during May 2015 – The Central

Bank of the UAE (CBUAE) said that money supply aggregate

M1 increased by 1.9% to AED482.8bn at the end of May 2015.

Money Supply aggregate M2 also increased by 1.4%, to

AED1.198tn at the end of May 2015 and following the same

trend money supply aggregate M3 increased 0.4% to AED1.38tn

at the end of May 2015. The increase in M1 and M2 was

attributed to AED8.6bn increase in monetary deposits and

AED7.7bn increase in quasi-monetary deposits, which was also

carried forward to M3. In May 2015, deposits rose by 4.8% YoY

to reach AED1.446bn. In the same month, government deposits

decreased by 6.2% YoY and constituted 12.6% of the total

deposits. As per the CBUAE’s released monthly report, gross

bank assets, including bankers’ acceptances, increased by

0.4%, to AED2.39tn at the end of May 2015, while the total bank

deposits rose by AED5.3bn reaching AED1.45bn, mainly due to

AED7.4bn increase in resident deposits. (GulfBase.com)

Union Properties Director resigns – Union Properties Director

Mr. Mana Al Mulla has resigned from his position, which was

duly accepted by the board. (DFM)

Mazaya secures KD25mn Islamic loans – Mazaya Holding

Company has signed two agreements with a Kuwaiti Bank to

obtain KD25mn Islamic financial facility. The first KD10mn three-

year Islamic facility is set to serve real estate investment, while

the second ten-year KD15mn facility will be used to settle a

bank loan of KD12.5mn and the remaining KD2.5mn will be

invested in the real estate sector. (DFM)

Emaar Misr IPO’s second tranche oversubscribed by 36

times – Emaar Misr for Development, the Egypt-based

subsidiary of Emaar Properties, announced that the second

tranche of its $2.3bn IPO was oversubscribed by about 36

times. The company offered 90mn shares last week in the

second tranche of its IPO, the largest flotation on the Egyptian

Stock Exchange since 2007. Traders said it drew subscriptions

for 3.23bn shares. (GulfBase.com)

TEM mulls South America expansion – Topaz Energy &

Marine (TEM) CEO Rene Kofod-Olsen said that the company is

planning to expand into South America in the next two years as

it looks beyond the current difficulties in the sector caused by

lower oil prices. He said TEM reported an 88% slump in

1Q2015, and expects earnings to continue to be disappointing

through the rest of 2015. The company has finance to back its

plans, having signed a $550mn seven-year loan in April 2015 to

refinance existing debt at a cheaper rate and to back expansion.

As for merger and acquisition plans, Kofod-Olsen said TEM was

open to opportunities to build its presence in each region.

(GulfBase.com)

DEWA receives bids for 25 new substations – The Dubai

Electricity and Water Authority (DEWA) has received 18 bids for

a long-term project to supply, install, test, and launch 25

substations. The utility has awarded contracts worth AED1.2bn

for 15 132/11kV substations. The project is in line with its plan to

increase the efficiency of transmission networks to meet

economic growth. (GulfBase.com)

RAK FTZ opens Business Center in Boulevard Downtown –

Ras Al Khaimah Free Trade Zone (RAK FTZ) has opened its

new Business Center in Boulevard Downtown Dubai. This

initiative is part of RAK FTZ’s ongoing efforts to enhance the

one-stop-shop experience for investors in top-notch facilities that

allow them to achieve their highest levels of success.

(GulfBase.com)

Agthia appoints Acting CFO – Agthia Group has appointed

Mr. Fatih Yeldan as its Group Acting Chief Financial Officer

(CFO).

TAQA marketing $3bn five-year loan to banks – According to

sources, Abu Dhabi National Energy Company (TAQA) is

marketing a $3bn, five-year loan to banks after receiving initial

commitments from eight local and international banks. The loan

amount, which will be used to consolidate existing debts into

6. Page 6 of 7

one facility with a lower rate of interest, is smaller than the

$3.5bn that sources indicated last month the energy firm was

looking to raise. Reportedly, the overall size of the facility could

be increased depending on the response from banks invited to

back the deal. (GulfBase.com)

ADNOC finalizes July 2015 to June 2016 diesel term

contracts – Traders said that Abu Dhabi National Oil Company

(ADNOC) has finalized July 2015 to June 2016 diesel term

contracts with several buyers and traders. The company has

finalized the term contracts at a premium of $2.35 a barrel over

Middle East quotes. Overall volumes were not certain but buyers

include Total, BP, Shell, Vitol, Petrobas and Swiss Singapore.

(Reuters)

ADIB plans $1bn Sukuk issue – According to sources, Abu

Dhabi Islamic Bank (ADIB) is planning to raise about $1bn of

perpetual bonds and is talking to banks on the deal. The bank

has received approval from the UAE central bank for the Islamic

debt sale and may issue in later 2015. (GulfBase.com)

Malaysia fund's $4.5bn rescue may weigh on IPIC – Abu

Dhabi's International Petroleum Investment Company (IPIC) has

been loaded with extra debt that may worry investors in its

bonds. Earlier, in May 2015, IPIC, an investment company

owned by Abu Dhabi's government, had come to the aid of

Malaysia's loss-making 1MDB, whose poor record and $11.6bn

of debt are a source of political pressure on Prime Minister Najib

Razak. IPIC agreed to provide 1MDB with $1bn in cash,

allowing the Malaysian fund to repay a $975mn loan to a global

banking syndicate. The Abu Dhabi firm also agreed to assume

$3.5bn of 1MDB debt, and forgive an undisclosed amount of

debt owed to IPIC by 1MDB, in exchange for assets which have

not been named. IPIC's aid to 1MDB illustrates some of the risks

of investing in state-owned companies in the Gulf: although they

have the backing of wealthy governments, they are not always

completely transparent. (Reuters)

OCC extends maintenance of kiln 3 – Oman Cement

Company (OCC) announced that it has prolonged the shutdown

of its kiln with 4,000 tons per day clinker production capacity due

to operational difficulties. OCC technical teams assisted by

external experts are working to resolve the defects. However,

this is resulting in lower production and sales during June 2015,

thus having an impact on the company’s performance during

2Q2015. (MSM)

MDT wins major Orpic contract – Germany’s MAN Diesel &

Turbo (MDT) has won a large shutdown engineering project

contract from Oman Oil Refineries & Petroleum Industries

Company (Orpic) for its refinery in Sohar. Under this multi-

million dollar contract, MDT will support Orpic’s major

maintenance turnaround during 1Q2016. The scope of work

includes replacement of a regenerator head with a huge

diameter and a steel weight of 250 tons besides installation of

internal domes. (GulfBase.com)

TISCO wins BP Khazzan camp facilities contract –

Renaissance Services announced that its fully-owned

subsidiary, Tawoos Industrial Services Company (TISCO) has

been awarded the contract for Consolidated Camp Facilities

Management by BP. The contract is for the provision of catering,

maintenance and related facilities management services to the

BP Khazzan project camps in Oman. The 29 months contract

(with an additional option of two years extension) is scheduled to

commence in August 2015. (GulfBase.com)

CIO: Bahrain 1Q2015 GDP growth slows to 2.8% YoY –

According to Central Informatics Organisation (CIO), Bahrain's

real GDP growth slowed to 2.8% YoY in 1Q2015 from 4.0% in

4Q2014. (Reuters)

7. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

May-11 May-12 May-13 May-14 May-15

QSE Index S&P Pan Arab S&P GCC

0.6%

(0.2%) (0.3%)

0.3%

(0.1%)

(1.3%)

(0.4%)

(2.0%)

(1.0%)

0.0%

1.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,175.55 0.2 (2.1) (0.8) MSCI World Index 1,776.22 (0.3) 0.1 3.9

Silver/Ounce 15.80 (0.4) (1.9) 0.6 DJ Industrial 17,946.68 0.3 (0.4) 0.7

Crude Oil (Brent)/Barrel (FM

Future)

63.26 0.1 0.4 10.3 S&P 500 2,101.49 (0.0) (0.4) 2.1

Crude Oil (WTI)/Barrel (FM

Future)

59.63 (0.1) 0.0 11.9 NASDAQ 100 5,080.51 (0.6) (0.7) 7.3

Natural Gas (Henry

Hub)/MMBtu

2.77 (0.8) (1.5) (7.6) STOXX 600 396.85 (0.3) 1.2 6.8

LPG Propane (Arab Gulf)/Ton 41.12 1.8 17.5 (16.1) DAX 11,492.43 (0.3) 2.4 7.6

LPG Butane (Arab Gulf)/Ton 56.25 3.2 19.4 (14.1) FTSE 100 6,753.70 (0.8) (0.2) 3.9

Euro 1.12 (0.3) (1.6) (7.7) CAC 40 5,059.17 (0.1) 3.3 9.2

Yen 123.85 0.2 0.9 3.4 Nikkei 20,706.15 (0.5) 1.6 14.4

GBP 1.57 (0.0) (0.9) 1.1 MSCI EM 980.63 (0.8) 0.6 2.5

CHF 1.07 0.4 (1.6) 6.6 SHANGHAI SE Composite 4,192.87 (7.4) (6.4) 29.6

AUD 0.77 (1.1) (1.5) (6.4) HANG SENG 26,663.87 (1.8) (0.4) 13.0

USD Index 95.47 0.3 1.5 5.8 BSE SENSEX 27,811.84 (0.4) 1.6 0.6

RUB 54.81 0.2 1.4 (9.8) Bovespa 54,016.97 1.3 (0.9) (8.5)

BRL 0.32 (0.0) (1.0) (15.3) RTS 943.01 0.2 (2.5) 19.3

142.1

121.3

117.4