QNBFS Daily Market Report November 21, 2021

•

0 likes•587 views

The QE Index in Qatar declined slightly by 0.1% led by losses in the industrial and insurance sectors. Regionally, most markets gained marginally except for Saudi Arabia which fell 1%. Volume on the Qatari stock exchange fell over 15% compared to the previous day. In company news, Qatar is in talks to acquire power plants in Pakistan and is well-positioned to support hosting the 2022 FIFA World Cup through its logistics infrastructure. Kahramaa held a workshop to increase cooperation with QRDI council. Qatar was also ranked among the top 10 countries in the Gulf for app development growth.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to QNBFS Daily Market Report November 21, 2021

Similar to QNBFS Daily Market Report November 21, 2021 (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report November 21, 2021

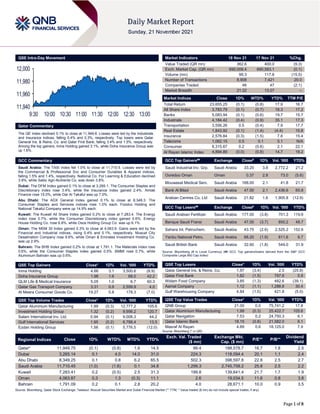

- 1. Page 1 of 8 QSE Intra-Day Movement Qatar Commentary The QE Index declined 0.1% to close at 11,949.8. Losses were led by the Industrials and Insurance indices, falling 0.4% and 0.3%, respectively. Top losers were Qatar General Ins. & Reins. Co. and Qatar First Bank, falling 3.4% and 1.5%, respectively. Among the top gainers, Inma Holding gained 3.1%, while Doha Insurance Group was up 1.6%. GCC Commentary Saudi Arabia: The TASI Index fell 1.0% to close at 11,710.5. Losses were led by the Commercial & Professional Svc and Consumer Durables & Apparel indices, falling 1.5% and 1.4%, respectively. National Co. For Learning & Education declined 3.9%, while Sabic Agri-Nutrients Co. was down 3.8%. Dubai: The DFM Index gained 0.1% to close at 3,265.1. The Consumer Staples and Discretionary index rose 3.4%, while the Insurance index gained 2.4%. Amlak Finance rose 15.0%, while Dar Al Takaful was up 7.0%. Abu Dhabi: The ADX General Index gained 0.1% to close at 8,349.3. The Consumer Staples and Services indices rose 1.0% each. Foodco Holding and National Takaful Company were up 14.9% each. Kuwait: The Kuwait All Share Index gained 0.2% to close at 7,283.4. The Energy index rose 0.7%, while the Consumer Discretionary index gained 0.6%. Energy House Holding Co. rose 6.8%, while Osos Holding Group Co. was up 6.1%. Oman: The MSM 30 Index gained 0.3% to close at 4,063.9. Gains were led by the Financial and Industrial indices, rising 0.4% and 0.1%, respectively. Muscat City Desalination Company rose 9.6%, while Oman & Emirates Investment Holding Co. was up 2.9%. Bahrain: The BHB Index gained 0.2% to close at 1,791.1. The Materials index rose 0.6%, while the Consumer Staples index gained 0.5%. BMMI rose 0.7%, while Aluminium Bahrain was up 0.6%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Inma Holding 4.66 3.1 3,500.6 (8.9) Doha Insurance Group 1.98 1.6 68.0 42.2 QLM Life & Medical Insurance 5.05 1.0 6.7 60.3 Qatar Gas Transport Company 3.31 0.9 2,559.9 4.0 Al Meera Consumer Goods Co. 19.27 0.8 178.3 (7.0) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Qatar Aluminium Manufacturing 1.99 (0.3) 12,777.2 105.6 Investment Holding Group 1.32 (0.2) 9,956.2 120.7 Salam International Inv. Ltd. 0.94 (0.1) 9,008.3 44.2 Gulf International Services 1.95 (0.2) 6,788.4 13.5 Ezdan Holding Group 1.56 (0.1) 5,776.5 (12.0) Market Indicators 18 Nov 21 17 Nov 21 %Chg. Value Traded (QR mn) 362.6 400.0 (9.3) Exch. Market Cap. (QR mn) 690,006.4 690,583.1 (0.1) Volume (mn) 99.3 117.6 (15.5) Number of Transactions 8,908 7,421 20.0 Companies Traded 46 47 (2.1) Market Breadth 21:22 13:27 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 23,655.25 (0.1) (0.8) 17.9 16.7 All Share Index 3,783.79 (0.1) (0.7) 18.3 17.2 Banks 5,083.94 (0.1) (0.6) 19.7 15.7 Industrials 4,184.42 (0.4) (0.9) 35.1 17.3 Transportation 3,556.26 0.5 (0.4) 7.9 17.7 Real Estate 1,843.92 (0.1) (1.4) (4.4) 15.8 Insurance 2,576.84 (0.3) (1.5) 7.6 15.4 Telecoms 1,062.15 0.5 0.1 5.1 N/A Consumer 8,315.67 0.2 (0.6) 2.1 22.1 Al Rayan Islamic Index 4,894.89 (0.0) (0.8) 14.7 19.2 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Saudi Industrial Inv. Grp. Saudi Arabia 33.20 3.8 2,772.2 21.2 Ooredoo Oman Oman 0.37 2.8 73.0 (5.6) Mouwasat Medical Serv. Saudi Arabia 168.00 2.1 41.8 21.7 Bank Al Bilad Saudi Arabia 47.00 2.1 2,436.6 65.8 Arabian Centres Co. Ltd Saudi Arabia 21.82 1.6 1,905.8 (12.9) GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Saudi Arabian Fertilizer Saudi Arabia 177.00 (3.8) 701.3 119.6 Banque Saudi Fransi Saudi Arabia 47.00 (3.7) 850.2 48.7 Sahara Int. Petrochem. Saudi Arabia 43.75 (2.6) 2,525.2 152.6 Yanbu National Petro. Saudi Arabia 68.20 (1.9) 811.6 6.7 Saudi British Bank Saudi Arabia 32.60 (1.8) 549.0 31.9 Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Qatar General Ins. & Reins. Co. 1.97 (3.4) 2.5 (25.9) Qatar First Bank 1.82 (1.5) 797.6 5.9 Widam Food Company 3.85 (1.3) 482.6 (39.1) Aamal Company 1.12 (1.1) 1,288.8 30.4 Gulf Warehousing Company 4.84 (1.0) 421.8 (5.0) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% QNB Group 21.00 0.0 75,741.2 17.8 Qatar Aluminium Manufacturing 1.99 (0.3) 25,422.7 105.6 Qatar Navigation 7.53 0.2 24,750.3 6.1 Qatar Islamic Bank 18.15 (0.8) 21,582.0 6.1 Masraf Al Rayan 4.89 0.6 18,125.0 7.9 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 11,949.75 (0.1) (0.8) 1.6 14.5 99.4 188,578.7 16.7 1.8 2.5 Dubai 3,265.14 0.1 4.0 14.0 31.0 224.3 118,094.4 20.1 1.1 2.4 Abu Dhabi 8,349.25 0.1 0.8 6.2 65.5 502.3 398,597.8 22.8 2.5 2.7 Saudi Arabia 11,710.45 (1.0) (1.6) 0.1 34.8 1,299.3 2,745,708.2 25.8 2.5 2.2 Kuwait 7,283.41 0.2 (0.5) 2.5 31.3 199.8 139,641.4 21.7 1.7 1.9 Oman 4,063.87 0.3 1.3 (0.3) 11.1 2.6 19,034.5 11.6 0.8 3.8 Bahrain 1,791.09 0.2 0.1 2.8 20.2 4.0 28,671.1 10.0 0.9 3.5 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 11,940 11,960 11,980 12,000 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 8 Qatar Market Commentary The QE Index declined 0.1% to close at 11,949.8. The Industrials and Insurance indices led the losses. The index fell on the back of selling pressure from Qatari and Arab shareholders despite buying support from GCC and foreign shareholders. Qatar General Ins. & Reins. Co. and Qatar First Bank were the top losers, falling 3.4% and 1.5%, respectively. Among the top gainers, Inma Holding gained 3.1%, while Doha Insurance Group was up 1.6%. Volume of shares traded on Thursday fell by 15.5% to 99.3mn from 117.6mn on Wednesday. Further, as compared to the 30-day moving average of 190.1mn, volume for the day was 47.7% lower. Qatar Aluminum Manufacturing Co. and Investment Holding Group were the most active stocks, contributing 12.9% and 10.0% to the total volume, respectively. Source: Qatar Stock Exchange (*as a % of traded value) Ratings, Earnings Releases and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Abu Dhabi Islamic Bank Fitch UAE LT-IDR/VR A+/bb A+/bb – Stable – Source: News reports, Bloomberg (* LT – Long Term, IDR – Issuer Default Rating, VR – Viability Rating) Global Economic Data Date Market Source Indicator Period Actual Consensu s Previou s 11-18 US Department of Labor Initial Jobless Claims 13-Nov 268k 260k 269k 11-18 US Department of Labor Continuing Claims 06-Nov 2080k 2120k 2209k 11-18 US Conference Board Leading Index Oct 0.90% 0.80% 0.10% 11-19 UK UK Office for National Statistics Public Sector Net Borrowing Oct 18.0b 12.4b 19.9b 11-19 Germany German Federal Statistical Office PPI MoM Oct 3.80% 1.90% 2.30% 11-19 Germany German Federal Statistical Office PPI YoY Oct 18.40% 16.20% 14.20% 11-19 Japan Ministry of Internal Affairs and Communications Natl CPI YoY Oct 0.10% 0.20% 0.20% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 32.79% 47.85% (54,614,569.5) Qatari Institutions 19.30% 23.14% (13,942,426.1) Qatari 52.09% 71.00% (68,556,995.6) GCC Individuals 0.70% 0.60% 374,545.2 GCC Institutions 3.09% 1.43% 6,009,604.2 GCC 3.79% 2.03% 6,384,149.3 Arab Individuals 8.35% 8.78% (1,559,095.3) Arab Institutions 0.00% 0.00% – Arab 8.35% 8.78% (1,559,095.3) Foreigners Individuals 2.10% 2.08% 74,506.8 Foreigners Institutions 33.66% 16.11% 63,657,434.8 Foreigners 35.77% 18.19% 63,731,941.6

- 3. Page 3 of 8 News Qatar CNBC Arabia: Qatar plans to buy Pakistan infrastructure assets – Qatar Investment Authority, the country’s sovereign wealth fund, is in advanced talks to acquire two state-run electric power plants in Pakistan CNBC Arabia reports, citing two unidentified sources. QIA hired JPMorgan as adviser. Plants owned by National Power Park; QIA could bid via a consortium or alone. (Bloomberg) GWCS’s expert knowledge, world-leading facilities will help Qatar capitalize on hosting the FIFA World Cup – The infrastructure developed by Gulf Warehousing Company (GWCS) will help Qatar deliver a memorable FIFA World Cup in 2022, the company said. The country will host the most compact version of the tournament in modern history. All the stadiums are in close proximity of one another, with the longest distance between venues just 75km, from Al Bayt Stadium in Al Khor to Al Janoub Stadium in Al Wakrah. The stadiums and other tournament venues, including training sites, are also in close proximity to GWCS’s nationwide logistics infrastructure, including numerous warehouses and vehicles, which are served by GWCS’s state-of-the-art IT systems and thousands of dedicated employees, who have built up relevant experience during a host of sporting events, including the FIFA Club World Cup, which Qatar hosted in both 2019 and 2021. In 2020, GWCS was named as the ‘Official Logistics Provider’ for the FIFA World Cup Qatar 2022 – an honor, which illustrates the company’s knowledge and expertise, along with its commitment to innovation and always delivering solutions for its clients across the globe. To be trusted by FIFA to support its flagship international tournament is a source of great pride for GWCS, as explained by its chairman, Sheikh Abdulla bin Fahad bin Jassem bin Jabor Al-Thani. (Gulf-Times.com) Kahramaa holds workshop to increase efficiency – The Qatar General Electricity & Water Corporation (Kahramaa) has held a brainstorming workshop to raise the level of cooperation and coordination between the corporation and Qatar Research, Development and Innovation (QRDI) Council. The workshop was held in the main building of the corporation. Cooperation will be achieved by opening the door for constructive discussions and using the best methods of research while thinking about the issues and challenges being faced by Kahramaa employees and projects, a statement noted. (Gulf- Times.com) Qatar among top 10 app developers in Gulf, says Strategy& Middle East – Qatar is one among the top 10 improvers in terms of growth in the number of apps published; suggesting that local output in the Gulf region’s digital innovation is increasing rapidly, according to a report of Strategy& Middle East. Qatar witnessed the highest growth of 41% in the number of apps published between 2010 and 2018 and was ranked second, said the report, quoting App Annie data. "Three GCC (Gulf Co-operation Council) countries — Qatar, the UAE, and Saudi Arabia — are among the top 10 improvers in terms of growth in number of apps published," the report said, adding the GCC economies could add between $138bn and $255bn to regional gross domestic product (GDP), depending upon how far they advanced. As per the App Annie data, the UAE was in the third position with it reporting 37% growth in the number of apps published during the review period and Saudi Arabia ranked ninth with 24% growth. (Gulf-Times.com) Oxford Economics: Doha's FDI attractiveness remains high – Qatar and the UAE still have the highest foreign direct investment (FDI) attractiveness in the Gulf and the wider Mena (Middle East and North Africa) regions, according to Oxford Economics. The key factors behind the top scoring countries are business environment and the quality of infrastructure, Oxford Economics said in its latest research note. The scorecard examines the relative FDI attractiveness of Mena economies based on factors influencing business operability in a country and potential domestic and export market growth. "The GCC overall spends 4-10% of GDP on infrastructure, which is comparable to spending by some Asian economies," it said, adding as a result, the quality of infrastructure in the GCC is ranked relatively high. In terms of the quality of the infrastructure, the report forecasted Qatar's infrastructure spending to be 10.4% of the gross domestic product by 2025 against 7.2% in Oman, 6.3% in Saudi Arabia, 4.9% in Bahrain, 4.1% in the UAE and 2.5% in Kuwait. According to the World Bank’s Logistical Performance Index, the UAE’s infrastructure is on a par with Singapore, with Israel, Qatar, Oman, Turkey and Saudi Arabia not far behind. The GCC economies are likely to continue to invest in improving their infrastructure. They have ambitious growth and diversification plans and the financial resources to undertake investment. The private-public partnership (PPP) market could help support infrastructure investment across the wider region, it said. (Gulf-Times.com) Qatar’s rising exports – Qatar's trade surplus, which represents the difference between total exports and imports, has once again showed a rising trend which is a good sign for ongoing economic recovery. The trade surplus has been rising consistently over the past few months which demonstrate the strength of country’s economy. According to the figures released by the Planning and Statistics Authority, Qatar recorded a merchandise trade surplus of QR57.8bn in the third quarter (3Q) of this year compared to QR19.6bn in 3Q of previous year. The rising trend in the trade surplus has also been witnessed in the past months. The positive growth indicates that the Qatari economy has witnessed a remarkable recovery from the negative impacts of COVID-19 pandemic. The healthy growth in trade surplus also demonstrates that the pace of economic recovery in Qatar’s economy has gained strong momentum and the recovery will continue in coming months. In the third quarter of 2021, the value of Qatar’s total exports (including exports of domestic goods and re-exports) amounted to QR82.6bn, increased by QR41.5bn (101%) compared to the third quarter of 2020 which amounted total exports of QR41.1bn and increased by nearly QR11.7bn or 16.5% compared to the second quarter of 2021. Qatar’s foreign merchandise trade balance showed a surplus of QR19.6bn in July 2021, reflecting an increase of about QR13.3bn or 213.4% compared to July 2020. When compared month-on-month, the surplus increased by nearly QR2.6bn or 15.5% compared to June 2021. The foreign merchandise trade balance had showed a surplus of QR19.2bn in August 2021, showing an increase of about QR12.3bn or 177.4% compared to August 2020. (Peninsula Qatar) Realty trading volume exceeds QR373mn during November 7-11 – The total value of real estate transactions in the sales contracts registered with the Real Estate Registration Department of the Ministry of Justice from November 7 to 11, reached QR373,507,402. The types of real estate traded included vacant lands, houses, residential buildings, a commercial building and multi-purpose buildings. Most of the trading took place in the municipalities of Al Rayyan, Doha, Al Wakrah, Umm Salal, Al Da’ayen, Al Shamal, Al Khor and Al Dhakhira. (Peninsula Qatar) Qatar announces completion of 7th tournament-ready venue for FIFA World Cup 2022 – Stadium 974 has been officially unveiled and will host its first match on 30 November when the United Arab Emirates and Syria go head-to-head on

- 4. Page 4 of 8 the opening day of the FIFA Arab Cup. Stadium 974 is the seventh tournament venue to be completed by the Supreme Committee for Delivery & Legacy (SC) and follows Khalifa International, Al Janoub, Education City, Ahmad Bin Ali, Al Bayt and Al Thumama in being declared ready to host matches during the FIFA World Cup 2022, which will kick off on November 21 next year. (Gulf-Times.com) Formula 1 Ooredoo Qatar Grand Prix kicks off on Friday – The Formula 1 Ooredoo Qatar Grand Prix kicked off on Friday in Doha for a period of three days at the Losail International Circuit with the participation of the most prominent world champions. Losail International Circuit will host the Formula 1 championship for the first time this year and will do so for the next ten years, starting from 2023. It will take a permanent place on the calendar of the Formula 1 seasons, according to the contract signed by the Qatar Motor and Motorcycle Federation (QMMF) with Formula 1. The Qatar GP will take place from November 19-21. On Friday, the first of three practice races will begin at 1:30pm for a duration of one hour. A second free practice will take place at 5pm for one hour as well. On Saturday, the third final practice will take place at 2pm for one hour. Qualifying for Sunday's race will be held at 5pm for a period of one hour, which determines the drivers' starting position. On Sunday at 5pm, the Formula 1 race will begin. They will race for 57 laps or for two hours. (Gulf-Times.com) Lusail Marina ready to host QNB Asia Triathlon Cup Doha 2021 next weekend – Some of the world’s top athletes will feature in this week’s QNB Asia Triathlon Cup Doha 2021, organizers Qatar Triathlon Federation (QTF) confirmed on Saturday. The two-day event – with $20,000 up for grabs in prize money - will be held at Lusail Marina where 59 athletes from 21 countries will cover World Triathlon’s Olympic distances in swimming, cycling and running. (Qatar Tribune) A new air route has been opened in the direction of Almaty – Doha – The opening ceremony of a new international flight on the route Almaty - Doha of the Qatar Airways airline took place today.The event was attended by Chairman of the Civil Aviation Committee Talgat Lastayev, Deputy Akim of Almaty Serik Kusainov, Qatar Ambassador to Kazakhstan Abdulaziz Sultan Al-Rumayhi, Senior Vice President of Qatar Airways for Eastern Regions Marwan Kolelait, President of Almaty Airport Alp Er Tunga Ersoy. The flights will be operated with a frequency of 2 flights per week on Airbus A320 aircraft with a capacity of 132 seats (12 business class, 120 economy class). Passengers will be able to use Qatar Airways' route network consisting of more than 140 destinations via Hamad International Airport in Doha. (Gulf-times.com) International US economy regaining speed as unemployment claims fall; manufacturing surges – The number of Americans filing new claims for unemployment benefits fell close to pre-pandemic levels last week as the labor market recovery continues, though a shortage of workers remains an obstacle to faster job growth. The weekly unemployment claims report from the Labor Department on Thursday, the most timely data on the economy's health, also showed jobless benefits rolls declining to a 20-month low in early November. The economy is regaining momentum following a lull over the summer as a wave of COVID-19 infections driven by the Delta variant battered the nation. Initial claims for state unemployment benefits slipped 1,000 to a seasonally adjusted 268,000 for the week ended Nov. 13. That was the lowest level since the start of the coronavirus pandemic in the United States more than 20 months ago. Unadjusted claims dropped 18,183 to 238,850. The decrease was led by Kentucky, likely due to automobile workers returning to factories after temporary layoffs as motor vehicle manufacturers deal with a global semiconductor shortage. There were also big declines in Michigan, Tennessee and Ohio, states that also have a strong presence of auto manufacturers. (Reuters) JP Morgan: US to start raising interest rates from September 2022 – The US Federal Reserve will start raising interest rates from September 2022, economists at the country's biggest bank said in a 2022 outlook note. JPMorgan expects the central bank to raise rates by 0.25% from the third quarter of next year and keep raising them by 25 basis points every quarter "at least until real rates are at zero," the team led by chief economist Mike Feroli wrote. Ten-year inflation-adjusted yields or "real yields" stood at minus 1.12% on Thursday . The bank's forecast for the first Fed rate hike is a little more conservative than at some rivals, such as Deutsche Bank, which expects the first US hike as early as July 2022. Money markets expect the first increase at a similar time. JPMorgan's economists expect U.S. economic growth to average 3.5% in 2022, compared to 5.5% in 2021, and full employment to be achieved by mid-2022. Inflation is also expected to slow in the coming quarters, with core prices projected to average 2.2% by the third quarter of 2022 compared to 4.2% in the fourth quarter of 2021. (Reuters) BoE's Pill sees growing case for December rate rise, but no guarantee – Bank of England chief economist Huw Pill said the weight of evidence was shifting towards a rise in interest rates next month but that he had not made a decision, and markets would do better to focus on the longer term. Speaking to reporters at an economics conference in Bristol, Pill also cautioned against the widespread assumption that the BoE's first policy move would be to raise interest rates by 15 basis points to 0.25%, as he was open to other options. The BoE wrong-footed many investors this month when it did not lift interest rates from their record low 0.1%, following comments from Governor Andrew Bailey in late October which markets interpreted as a signal that a rate rise was very near. Since then, inflation has risen to a 10-year high of 4.2% and jobless data has not pointed towards higher unemployment after the end of the furlough scheme - a key concern that stayed the BoE's hand at the start of this month. Further unemployment data will come before the BoE's next meeting on December 16. "The burden of proof is perhaps a little bit in the other direction..., so now I'm looking perhaps for reasons not to hike rates," he said. Two of the BoE's policymakers voted to raise rates to 0.25% this month. Asked if it was safe to assume that, whenever it came, this would be the BoE's first tightening step, Pill said he could not confirm this. (Reuters) UK consumers turn more confident despite inflation worries – People in Britain turned more confident this month despite worries about inflation and they were more willing to purchase expensive items, according to a survey that will be welcome news to retailers preparing for the Christmas season. The GfK Consumer Confidence Index rose for the first time in four months to -14 in November from -17 in October which was its lowest level since an early-2021 coronavirus lockdown. Joe Staton, GfK's client strategy director, said views on the economy had improved despite rising inflation and the prospect of higher interest rates although consumers were less buoyant about their personal finances. The rise in GfK's measure of consumers' propensity to make a major purchase to -3 from -10 left it 25 points higher than it was in November last year. The Bank of England has said the rise in inflation and other squeezes on household finances, including the end of emergency pandemic welfare support for many households, could slow Britain's economic recovery from the coronavirus crisis. The BoE is due to announce on Dec. 16 whether it is raising interest rates from

- 5. Page 5 of 8 their all-time low after it wrong-footed many investors on Nov. 4 when it kept borrowing costs on hold despite forecasting inflation would climb to around 5%. British consumer inflation hit a 10-year high of 4.2% - more than double the BoE's 2% target - in the 12 months to October, according to data published on November 17. (Reuters) Auction houses and clothes shoppers lift UK retail sales – Auction houses and shoppers seeking new clothes for the Christmas holidays lifted British retail sales last month by more than expected, adding to recent signs that a slowdown in the economy might have abated slightly. Retail sales volumes rose by 0.8% month-on-month in October, the Office for National Statistics said. A Reuters poll of economists had pointed to a 0.5% increase. Retail sales are now 5.8% above the level of February 2020, before the COVID-19 pandemic. Auction houses were an especially strong driver of retail sales growth in October, the ONS said. Last month a Banksy picture by British artist Banksy - which in 2018 was half-sliced by a shredder concealed in its frame when it was sold at auction - fetched 18.6mn Pounds ($25.1mn) when it went back under the hammer in the same room in London. Separate data showed the government borrowed more than expected last month although borrowing for the year to date is more than 100bn Pounds below its level in April-October 2020, when the economy felt the full force of the pandemic. With inflation surging, the BoE has said it will raise rates in the coming months if the evidence shows Britain's economy has not been impaired by the end of the COVID-19 job job-protecting furlough scheme, which closed last month. The retail sales data - and an improvement in the GfK measure of consumer confidence this month - suggested the economy has not worsened of late after slower-than-expected growth in the third quarter. The ONS said clothes sales rose by 6.2% in October, helped by an early Christmas trading boost to sales. Sports, games and toy stores also had a good month. Separate data showed British public borrowing was higher than expected in October at 18.8bn Pounds, 200mn Pounds lower than a year earlier and above economists' forecasts in a Reuters poll of a fall to 13.8bn Pounds. (Reuters) OECD: France needs long-term spending rule to restore finances – France needs a multi-annual spending rule to bring its post-COVID public finances under control, the Organization for Economic Cooperation and Development said on Thursday as it raised its growth forecasts. The recovery of the euro zone's second biggest economy has surpassed most expectations this year as consumer spending bounded back following a mass vaccination campaign. Growth is now set to reach 6.8% this year and 4.2% in 2022, the OECD said in an in-depth report on the French economy. It had previously penciled in forecasts of 6.3% this year and 4.0% next year. The government's support measures for the economy during the crisis left the public finances severely strained and debt at record levels, just as France plans major investments to decarbonize the economy and faces growing costs from an aging population. With public spending already among the highest the world at nearly 60% of GDP, the OECD said France needed a multi-annual spending rule, which it said had a positive track record in curbing deficits in other high spending countries like Sweden. It said that would force the government to rationalize spending with in-depth reviews to ensure that money is well spent, which the OECD said was not always the case given the myriad of public bodies at different levels. (Reuters) Japan unleashes record stimulus package, bucking global tapering trend – Japan unveiled a record $490bn spending package on Friday to cushion the economic blow from the COVID-19 pandemic, bucking a global trend towards withdrawing crisis-mode stimulus measures and adding strains to its already tattered finances. Spending has ballooned due to an array of payouts including those criticized for being unrelated to the pandemic, such as cash handouts to households with youth aged 18 or below, and will likely lead to additional bond issuance this year. The massive spending would underscore the resolve of Prime Minister Fumio Kishida - once considered a fiscal conservative -to focus on reflating the economy and redistributing wealth to households. The package, finalized at a cabinet meeting on Friday, included 55.7tn Yen ($490bn) in spending for items ranging from cash payouts to households, subsidies to COVID-hit firms and reserves set aside for emergency pandemic spending. The size of spending was much bigger than the 30-40tn Yen estimated by markets, and will be mostly funded by an extra budget of around 32tn Yen to be compiled this year. The remainder will likely be funded by next year's budget. (Reuters) Japan's consumer prices extend gains as fuel costs surge – Japan's core consumer prices rose for the second straight month in October, as fuel costs accelerated at the fastest pace in more than a decade and pressures from raw materials shortages gradually passed through to retailers. Consumer inflation is expected to pick up in coming months due to higher fuel costs, though any price rises in the country will likely be moderate compared with other advanced economies as weak wage growth limits firms from passing on hikes. The core consumer price index (CPI), which excludes volatile fresh food prices but includes fuel costs, rose 0.1% YoY in October, government data showed. That matched the median forecast in a Reuters poll and followed a similar rise in September, which was the first uptick since March last year. Overall energy prices soared 11.3% from a year earlier in October, posting their biggest rise since September 2008, thanks largely to a jump in fuel costs, which surged 21.4% YoY, their largest gain since August 2008. The data will be among factors the Bank of Japan will scrutinize at its last policy meeting of the year, scheduled for the middle of next month. (Reuters) China set to keep lending benchmark steady as policymakers eye property risks – China is set to keep its benchmark lending rate steady at its monthly fixing on Monday, a Reuters survey showed, as policymakers seek to limit risk taking in the property sector. A snap poll of 23 market participants this week found 21 expected no change in either the one-year Loan Prime Rate (LPR) or the five-year tenor at next week's setting. That would be the 19th straight month that no change will be made to the rate and follows the People's Bank of China's (PBOC) decision this week to keep the interest rate on its medium-term loans unchanged. The remaining two respondents forecast a marginal cut of 5 basis points to the one- year LPR and expected no change to the five-year tenor, which influences the pricing of mortgages. The one-year LPR is currently at 3.85% and the five-year rate is at 4.65%. The central bank fully rolled over maturing medium-term lending facility (MLF) due this month, keeping the borrowing cost unchanged for the 19th straight month. The MLF serves as a guide for the LPR and many traders and analysts say any adjustment to the LPR should mimic changes to the borrowing cost of MLF loans. (Reuters) China's land sales slump for 4th month as property woes worsen – The Chinese government's revenue from land sales slumped for a fourth month in October compared with year-ago levels, as cash-strapped developers moved cautiously on land buying after tighter regulatory curbs on new borrowing. The value of government land sales in October declined 13.14% from a year earlier to 573.7bn Yuan ($89.90bn), after suffering a drop of 11.15% in September, according to Reuters calculations of data released by the finance ministry. Many developers

- 6. Page 6 of 8 including China Evergrande Group have grown desperately short of cash since authorities last year unveiled the "three red lines" - a policy of President Xi Jinping that imposes limits on liabilities-to-assets, net debt-to-equity, and cash-to-short-term borrowing ratios. Poor demand among developers at urban land auctions risks squeezing regional finances, pressuring local governments to scramble for other income to fund investment and support the economy, including the issuance of more bonds that increase their debt obligations, say some analysts. (Reuters) Regional US again presses OPEC+ as it weighs reserve release – The White House on Friday pressed the OPEC producer group again to maintain adequate global supply, days after US discussions with some of the world's biggest economies over potentially releasing oil from strategic reserves to quell high energy prices. The Biden administration has asked a wide range of countries, including China for the first time, to consider releasing stocks of crude. President Joe Biden faces slipping approval figures as Americans cite inflation as a growing problem. White House spokeswoman Jen Psaki said the administration wants to "ensure that the OPEC member countries and OPEC as an organization meets the demand needs that are out there with the adequate supply. That is something we've pressed them on in the past." (Reuters) Vortexa: OPEC+ may run out of spare oil output capacity in 1 year – OPEC+’s spare oil production capacity may be used up in the next 12 months if demand returns to 2019 levels and producers don’t ramp up oil fields, Vortexa analyst David Wech wrote in a note. Current spare capacity is “at best” 3mn bpd, with as much as 2m bpd in Saudi Arabia and rest in Russia and UAE. OPEC+ has been ramping up production and exports, reducing spare capacity. Saudi Arabia and UAE are already exporting ~500k bpd more than pre-Covid levels, when comparing shipments in October and first half of November with avg. 2019 levels. (Bloomberg) Saudi Arabia's crude oil exports hit eight-month high in September – Saudi Arabia's crude oil exports rose in September for a fifth month in a row to their highest since January, the Joint Organization Data Initiative (JODI) said on Thursday. The kingdom's crude oil exports increased to 6.516mn bpd in September, from 6.450mn bpd in August. Total exports including oil products stood at 7.84mn bpd. The world's largest oil exporter's crude output rose by 100,000 bpd MoM to 9.662mn bpd in September, its highest since April 2020. (Reuters) Saudi Aramco, India's Reliance reevaluating oil-to- chemicals stake purchase – Reliance Industries Limited has said they will be reevaluating a proposal by Saudi Aramco to acquire a stake in the Indian company's chemical business. “Due to [the] evolving nature of Reliance’s business portfolio, Reliance and Saudi Aramco have mutually determined that it would be beneficial for both parties to re-evaluate the proposed investment in O2C business in light of the changed context. Consequently, the current application with NCLT for segregating the O2C business from RIL is being withdrawn,” Reliance said in a statement on Friday. The firms signed a letter of intent in 2019 for Aramco, the world’s top oil exporter, to acquire a 20% stake of the oil-to-chemicals (O2C) business of Reliance. Reliance said Aramco will continue to be a preferred partner for investments in India and will work with it and SABIC for investments in the Kingdom. (Zawya) ONGC, Aramco sign MOU to study long term oil, Petchem deals – Oil and Natural Gas Corp. signed a Memorandum of Understanding with Saudi Aramco to explore long-term supply contracts of crude oil, refined petroleum and petrochemical products, according to a statement from India’s state-run refiner Thursday. Both sides will also look at the demand and supply of low carbon energy as part of this pact: statement. (Bloomberg) World's no. 1 oil exporter lures ESG investors with green bonds – With the biggest member of the world’s No. 1 oil cartel readying its first-ever green bond, sustainable investors are debating what to make of it. Saudi Arabia’s plan to enter the market for green bonds marks a watershed moment. Some investors say it represents an encouraging step for the oil- addicted Gulf state to plot a path away from fossil fuels. Others are asking for credible evidence the debt will genuinely be green. The upshot, though, is that the biggest oil exporter on the planet is likely to find plenty of buyers for a bond it says will be climate friendly. Both the Saudi government itself and the kingdom’s sovereign wealth fund are preparing to sell green bonds in the coming months. (Bloomberg) Saudi's Tourism Enterprises Company votes on 48% capital reduction on December 9 – Tourism Enterprise Co. shareholders will vote on a 48.21% capital reduction on December 9 during an Extraordinary Assembly Meeting, according to a bourse filing. The capital after reduction will amount to SR52.57mn compared to SR101.5mn before reduction, the company said in a statement on the Saudi Stock Market (Tadawul), on Thursday. The number of shares after the reduction is set to be about 5.26mn shares, compared to 10.15mn shares before the move. (Zawya) Nayifat to begin trading on Saudi's Tadawul on November 22 – Nayifat Finance Co. (NFC) will begin trading on the Saudi Exchange (Tadawul) as of Monday, November 22, according to a bourse filing on Thursday. The stock will have +/- 30% daily price fluctuation limits and +/- 10% static price fluctuation limits, the company said on Tadawul. These fluctuation limits will be applied during the first three days of listing, and from the fourth trading day onwards, the daily price fluctuation limits will revert to +/- 10% and the static price fluctuation limits will no longer apply. (Zawya) UAE September M3 money supply falls 1% YoY – The UAE's M3 money supply fell 1% YoY in September versus -0.9% in August, according to The Central Bank of the UAE. (Bloomberg) UAE's Etisalat Group to acquire online grocery platform elGrocer – UAE’s Emirates Telecommunications Group Company (Etisalat Group) has signed an agreement to acquire Dubai-based online grocery platform elGrocer DMCC, the telecom operator said on Thursday. The transaction will be funded by cash and support the company’s strategy to diversify its product portfolio, Etisalat Group told the Abu Dhabi Securities Exchange (ADX), where its shares are listed. “This acquisition will support Etisalat’s digital ambitions by enriching its services, bringing it closer to the daily lives of the consumers and unlocking synergies that drive a diversified and integrated product portfolio,” the disclosure said. (Zawya) Dubai investor close to $600mn Saudi dental clinics deal – A Dubai-based investment company is nearing a $600mn deal to buy a majority stake in Saudi Arabia’s largest provider of dental and dermatology care, according to people familiar with the matter. Gulf Islamic Investments LLC., also known as GII, is set to buy the 70% stake owned by private equity firm Jadwa Investment Co. in Almeswak Dental Clinics, said the people, who asked not to be identified because the information is private. Emirati health-care company United Eastern Medical Services owns the rest of the shares. Jadwa acquired the stake in Almeswak in 2017, according to information on its website. (Bloomberg)

- 7. Page 7 of 8 ADNOC secures $3bn loan from JBIC and four other banks – State oil firm Abu Dhabi National Oil Company (ADNOC) signed a $3bn loan agreement with Japan’s export credit agency and four other lenders, the agency said on Thursday. The Japan Bank for International Cooperation (JBIC) is providing $2.1bn and Sumitomo Mitsui Banking Corporation (SMBC), the Tokyo branch of HSBC, Mizuho and MUFG are providing the rest, JBIC said in the statement. “This facility is intended to provide necessary support to ADNOC in ensuring stable imports of crude oil by Japanese companies,” JBIC said. (Reuters) Abu Dhabi's ADNOC awards $1.46bn EPC contracts for Dalma Gas Project – The Abu Dhabi National Oil Company (ADNOC) has awarded two engineering, procurement and construction (EPC) contracts totaling $1.46bn for the Dalma Gas Development Project. Abu Dhabi is looking at ways to boost its gas output as it targets self-sufficiency in the coming decades. As part of its integrated gas strategy launched in 2018 to become a key exporter of natural gas in the coming years, ADNOC is looking at new technologies to expand into unconventional gas, tap into gas caps and unlock new reservoirs. The two EPC contracts have been awarded to National Petroleum Construction Company (NPCC) and a joint venture (JV) between Técnicas Reunidas and Target Engineering, the state-owned energy producer said in a statement on Thursday. (Zawya) Mubadala's new asset management subsidiary starts operations – Mubadala, the Abu Dhabi-based sovereign investor managing a global portfolio of assets valued at $243bn, has announced the formal commencement of operations of Mubadala Capital as a wholly-owned asset management subsidiary within its Disruptive Investments portfolio. Established in 2011, Mubadala Capital has grown significantly in scale over the past decade, and today manages over $15bn of assets, including over $9bn in third-party capital vehicles on behalf of over 50 institutional investors. Mubadala Capital, which is headquartered in Abu Dhabi and has offices in New York, London, San Francisco, and Rio de Janeiro, comprises four integrated businesses - private equity, public equities, venture capital, and a Brazil focused business. (Zawya) Abu Dhabi's Response Plus to acquire Health Tech for AED9.8mn – Response Plus Holding, the UAE-based private onsite medical service provider, said its board approved plans to initiate the acquisition of 100% of Health Tech Training Center LLC for up to AED9.8mn. The chairman of the Response Plus Holding disclosed an ownership interest of 49% shares in Health Tech and therefore abstained from voting on the approval, the Abu Dhabi Securities Exchange listed Response Plus said in a bourse disclosure. The board also approved the company's three-year business plan. (Zawya) Adnoc logistics, AD ports to develop new port at Ta’ziz in UAE – Adnoc Logistics & Services and Abu Dhabi Ports signed an agreement to develop a new port and logistics facility at Ta’ziz, the chemicals production and industrial hub currently under development at Ruwais in the UAE.The companies will develop a liquids terminal and logistics facility to support tenants of the Ta’ziz Industrial Chemicals Zone. Facility will be a critical part of the supply chain for feedstock and will store and load final products for export. (Bloomberg) Fitch affirms Abu Dhabi Islamic bank at 'A+'; outlook stable – Fitch Ratings has affirmed UAE-based Abu Dhabi Islamic Bank's (ADIB) Long-Term Issuer Default Rating (IDR) at 'A+' with a Stable Outlook and Viability Rating (VR) at 'bb'. Fitch has withdrawn ADIB's Support Rating and Support Rating Floor as they are no longer relevant to the agency's coverage following the publication of our updated Bank Rating Criteria on 12 November 2021. (Bloomberg)

- 8. Contacts QNB Financial Services Co. W.L.L. Contact Center: (+974) 4476 6666 info@qnbfs.com.qa Doha, Qatar Saugata Sarkar, CFA, CAIA Shahan Keushgerian Head of Research Senior Research Analyst saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 8 of 8 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns, # Market was closed as on November 19,2021) 60.0 80.0 100.0 120.0 140.0 160.0 Oct-17 Oct-18 Oct-19 Oct-20 Oct-21 QSE Index S&PPan Arab S&PGCC (1.0%) (0.1%) 0.2% 0.2% 0.3% 0.1% 0.1% (1.5%) (1.0%) (0.5%) 0.0% 0.5% Saudi Arabia Qatar Kuwait Bahrain Oman Abu Dhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,845.73 (0.7) (1.0) (2.8) MSCI World Index 3,219.90 (0.2) (0.1) 19.7 Silver/Ounce 24.62 (0.8) (2.8) (6.8) DJ Industrial 35,601.98 (0.7) (1.4) 16.3 Crude Oil (Brent)/Barrel (FM Future) 78.89 (2.9) (4.0) 52.3 S&P 500 4,697.96 (0.1) 0.3 25.1 Crude Oil (WTI)/Barrel (FM Future) 76.10 (3.7) (5.8) 56.8 NASDAQ 100 16,057.44 0.4 1.2 24.6 Natural Gas (Henry Hub)/MMBtu 4.90 (1.2) 0.6 105.0 STOXX 600 486.08 (1.0) (1.5) 12.6 LPG Propane (Arab Gulf)/Ton 108.38 (3.0) (14.7) 44.0 DAX 16,159.97 (1.0) (0.9) 8.3 LPG Butane (Arab Gulf)/Ton 127.75 (2.5) (16.0) 83.8 FTSE 100 7,223.57 (0.8) (1.4) 10.2 Euro 1.13 (0.7) (1.4) (7.6) CAC 40 7,112.29 (1.0) (1.0) 18.4 Yen 113.99 (0.2) 0.1 10.4 Nikkei 29,745.87 0.7 0.4 (1.8) GBP 1.35 (0.3) 0.3 (1.6) MSCI EM 1,269.22 (0.4) (1.3) (1.7) CHF 1.08 (0.3) (0.8) (4.7) SHANGHAI SE Composite 3,560.37 1.1 0.5 4.8 AUD 0.72 (0.6) (1.3) (6.0) HANG SENG 25,049.97 (1.1) (1.1) (8.4) USD Index 96.03 0.5 0.9 6.8 BSE SENSEX# 59,636.01 – (1.5) 23.0 RUB 73.48 0.5 0.8 (1.3) Bovespa 103,035.00 0.2 (5.3) (19.9) BRL 0.18 (1.0) (2.8) (7.5) RTS 1,723.74 (2.2) (3.4) 24.2 159.5 148.5 144.1