QNBFS Daily Technical Trader Qatar - September 07, 2023 التحليل الفني اليومي ...

16 December Daily market report

1. Page 1 of 6

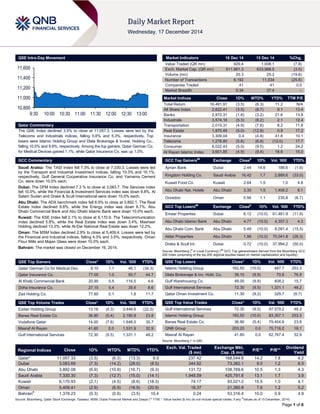

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 3.5% to close at 11,057.3. Losses were led by the Telecoms and Industrials indices, falling 5.6% and 5.3%, respectively. Top losers were Islamic Holding Group and Dlala Brokerage & Invest. Holding Co., falling 10.0% and 9.9%, respectively. Among the top gainers, Qatar German Co. for Medical Devices gained 1.1%, while Qatar Insurance Co. was up 1.0%.

GCC Commentary

Saudi Arabia: The TASI Index fell 7.3% to close at 7,330.3. Losses were led by the Transport and Industrial Investment indices, falling 10.3% and 10.1%, respectively. Gulf General Cooperative Insurance Co. and Yamama Cement Co. were down 10.0% each.

Dubai: The DFM Index declined 7.3 % to close at 3,083.7. The Services index fell 10.0%, while the Financial & Investment Services index was down 9.8%. Al Salam Sudan and Drake & Scull International were down 10.0% each.

Abu Dhabi: The ADX benchmark index fell 6.9% to close at 3,892.1. The Real Estate index declined 9.8%, while the Energy index was down 8.7%. Abu Dhabi Commercial Bank and Abu Dhabi Islamic Bank were down 10.0% each.

Kuwait: The KSE Index fell 2.1% to close at 6,170.9. The Telecommunication index declined 5.8%, while the Real Estate index was down 3.4%. Mashaer Holding declined 13.3%, while Al-Dar National Real Estate was down 12.2%.

Oman: The MSM Index declined 2.9% to close at 5,409.4. Losses were led by the Financial and Industrial indices, falling 4.3% and 3.5%, respectively. Oman Flour Mills and Majan Glass were down 10.0% each.

Bahrain: The market was closed on December 16, 2014.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar German Co for Medical Dev.

9.10

1.1

46.1

(34.3) Qatar Insurance Co. 77.00 1.0 50.7 44.7 Al Khalij Commercial Bank 20.90 0.5 116.5 4.6 Doha Insurance Co. 27.15 0.4 35.6 8.6 Zad Holding Co. 77.60 0.1 1.8 11.7

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group

13.18

(4.3)

3,449.6

(22.5) Barwa Real Estate Co. 36.90 (5.4) 2,190.8 23.8

Vodafone Qatar

14.00

(7.6)

1,648.0

30.7 Masraf Al Rayan 41.60 0.0 1,531.9 32.9

Gulf International Services

72.30

(9.5)

1,331.1

48.2

Market Indicators 16 Dec 14 15 Dec 14 %Chg.

Value Traded (QR mn)

929.4

1,008.1

(7.8) Exch. Market Cap. (QR mn) 611,961.3 633,988.5 (3.5)

Volume (mn)

20.3

25.2

(19.6) Number of Transactions 8,192 11,034 (25.8)

Companies Traded

41

41

0.0 Market Breadth 5:34 37:4 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return

16,491.91

(3.5)

(6.3)

11.2

N/A All Share Index 2,822.41 (3.5) (6.7) 9.1 13.4

Banks

2,972.31

(1.6)

(3.2)

21.6

13.8 Industrials 3,574.16 (5.3) (8.2) 2.1 12.4

Transportation

2,010.31

(4.9)

(7.8)

8.2

11.8 Real Estate 1,970.48 (5.0) (12.9) 0.9 17.2

Insurance

3,309.04

0.4

(4.8)

41.6

10.1 Telecoms 1,278.80 (5.6) (6.8) (12.0) 17.7

Consumer

6,022.43

(5.0)

(9.5)

1.2

24.2 Al Rayan Islamic Index 3,601.85 (4.9) (9.4) 18.6 15.0

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Ajman Bank

Dubai

2.44

14.6

188.6

(1.6) Kingdom Holding Co. Saudi Arabia 16.42 1.7 2,889.6 (33.0)

Kuwait Food Co.

Kuwait

2.64

1.5

1.0

4.8 Abu Dhabi Nat. Hotels Abu Dhabi 3.35 1.5 1,409.2 8.1

Ooredoo

Oman

0.56

1.1

235.8

(6.7)

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Emaar Properties

Dubai

6.12

(10.0)

61,461.9

(11.9) Abu Dhabi Islamic Bank Abu Dhabi 4.77 (10.0) 4,357.3 4.3

Abu Dhabi Com. Bank

Abu Dhabi

5.49

(10.0)

8,091.4

(15.5) Aldar Properties Abu Dhabi 1.98 (10.0) 70,041.8 (28.3)

Drake & Scull Int.

Dubai

0.72

(10.0)

37,994.2

(50.0)

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group

162.50

(10.0)

487.7

253.3 Dlala Brokerage & Inv. Hold. Co. 39.10 (9.9) 70.6 76.9

Gulf Warehousing Co.

48.00

(9.8)

408.2

15.7 Gulf International Services 72.30 (9.5) 1,331.1 48.2

Qatar Oman Investment Co.

11.30

(9.2)

329.7

(9.7)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Gulf International Services

72.30

(9.5)

97,579.2

48.2 Islamic Holding Group 162.50 (10.0) 83,307.1 253.3

Barwa Real Estate Co.

36.90

(5.4)

79,404.8

23.8 QNB Group 203.20 0.0 75,716.2 18.1

Masraf Al Rayan

41.60

0.0

62,767.4

32.9

Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield

Qatar*

11,057.33

(3.5)

(6.3)

(13.3)

6.5

237.42

168,044.6

14.2

1.8

4.2 Dubai 3,083.69 (7.3) (14.2) (28.0) (8.5) 344.92 73,382.1 9.0 1.2 6.5

Abu Dhabi

3,892.08

(6.9)

(10.9)

(16.7)

(9.3)

131.72

108,769.6

10.5

1.3

4.3 Saudi Arabia 7,330.30 (7.3) (12.7) (15.0) (14.1) 1,948.59 425,791.6 13.1 1.7 3.9

Kuwait

6,170.93

(2.1)

(4.5)

(8.6)

(18.3)

74.17

93,021.2

15.5

1.0

4.1 Oman 5,409.41 (2.9) (6.9) (16.9) (20.9) 18.37 21,360.8 7.6 1.2 5.2

Bahrain#

1,378.23

(0.3)

(0.9)

(3.5)

10.4

0.24

53,316.4

10.0

0.9

4.9

Source: Bloomberg, Qatar Stock Exchange, Tadawul, MSM, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any #Values as of 15 December, 2014)

10,80011,00011,20011,40011,6009:3010:0010:3011:0011:3012:0012:3013:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index declined 3.5% to close at 11,057.3. The Telecoms and Industrials indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari shareholders.

Islamic Holding Group and Dlala Brokerage & Invest. Holding Co. were the top losers, falling 10.0% and 9.9%, respectively. Among the top gainers, Qatar German Co. for Medical Devices gained 1.1%, while Qatar Insurance Co. was up 1.0%.

Volume of shares traded on Tuesday fell by 19.6% to 20.3mn from 25.2mn on Monday. However, as compared to the 30-day moving average of 13.1mn, volume for the day was 54.4% higher. Ezdan Holding Group and Barwa Real Estate Co. were the most active stocks, contributing 17.0% and 10.8% to the total volume respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

12/16

US

US Census Bureau

Housing Starts

November

1,028K

1,040K

1,045K 12/16 US US Census Bureau Building Permits November 1,035K 1,065K 1,092K

12/16

US

Markit

US Manufacturing PMI

December

53.7

55.2

54.8 12/16 EU Markit Eurozone Services PMI December 51.9 51.5 51.1

12/16

EU

Markit

Eurozone Composite PMI

December

51.7

51.5

51.1 12/16 EU Markit Eurozone Manufacturing PMI December 50.8 50.5 50.1

12/16

EU

ZEW

ZEW Survey Expectations

December

31.8

–

11.0 12/16 EU Eurostat Trade Balance SA October 19.4B 18.4B 17.9B

12/16

EU

Eurostat

Trade Balance NSA

October

24.0B

21.0B

18.1B 12/16 France Markit France Manufacturing PMI December 47.9 48.6 48.4

12/16

France

Markit

France Services PMI

December

49.8

48.5

47.9 12/16 France Markit France Composite PMI December 49.1 48.3 47.9

12/16

Germany

Markit

BME Germany Manufacturing PMI

December

51.2

50.3

49.5 12/16 Germany Markit Germany Services PMI December 51.4 52.5 52.1

12/16

Germany

Markit

BME Germany Composite PMI

December

51.4

52.3

51.7 12/16 UK Office for National Statist CPI MoM November -0.30% 0.00% 0.10%

12/16

UK

Office for National Statist

CPI YoY

November

1.00%

1.20%

1.30% 12/16 UK Office for National Statist Retail Price Index November 257.1 257.7 257.7

12/16

UK

Office for National Statist

RPI MoM

November

-0.20%

0.00%

0.00% 12/16 UK Office for National Statist RPI YoY November 2.00% 2.20% 2.30%

12/16

UK

Office for National Statist

PPI Input NSA MoM

November

-1.00%

-1.50%

-1.50% 12/16 UK Office for National Statist PPI Input NSA YoY November -8.80% -9.20% -8.40%

12/16

UK

Office for National Statist

PPI Output NSA MoM

November

0.20%

-0.30%

-0.30% 12/16 UK Office for National Statist PPI Output NSA YoY November -0.10% -0.60% -0.50%

12/16

UK

Office for National Statist

PPI Output Core NSA MoM

November

0.50%

0.00%

0.10% 12/16 UK Office for National Statist PPI Output Core NSA YoY November 1.40% 1.00% 0.90%

12/16

UK

Office for National Statist

ONS House Price YoY

October

10.40%

11.40%

12.10%

12/16 Spain Bank of Spain 3M T-Bill Amount Sold 16-December €727.9M – €845.3M

12/16

Spain

Bank of Spain

3M T-Bill Average Yield

16-December

0.20%

–

0.07%

12/16 Spain Bank of Spain 3M T-Bill Bid/Cover Ratio 16-December 3.2 – 3.1

12/16

Spain

Bank of Spain

9M T-Bill Bid/Cover Ratio

16-December

2.7

–

1.8

12/16 Spain Bank of Spain 9M T-Bill Average Yield 16-December 0.37% – 0.30%

12/16

Spain

Bank of Spain

9M T-Bill Amount Sold

16- December

€1,820.4M

–

€3,261.8M

12/16 Italy ISTAT Trade Balance Total October 5,397M – 2,014M

12/16

Italy

ISTAT

Trade Balance EU

October

1,373M

–

487M

12/16 China Markit HSBC China Manufacturing PMI December 49.5 49.8 50.0

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari

65.68%

54.51%

103,758,382.49 Non-Qatari 34.32% 45.49% (103,758,382.49)

3. Page 3 of 6

News

Qatar

Al-Sada: Market volatility poses major challenge to gas producers – HE the Minister of Energy & Industry Dr. Mohamed Bin Saleh Al-Sada said the major challenge faced by gas producers was the “increasing volatility” of the energy market and urged the Gas Exporting Countries Forum (GECF) member countries to be fully alert to the situation. He further added that the price volatility was driven by a variety of reasons including economic and geopolitical elements, which may adversely affect market stability. Al-Sada said the GECF, was a “platform for cooperation”. Its existence and the successes achieved so far were a reflection of its members’ determination to cooperate. Al- Sada hoped that the benefits of cooperation and collaboration among the GECF member countries would be reflected on the global gas industry in a way that contributed toward realizing the interests of all concerned parties. Earlier, Al-Sada said OPEC countries and other oil-producing nations are closely watching developments in the global energy market, but he added that the market would “settle eventually”. (Gulf-Times.com)

ORDS’ fiber network marks major milestone – Ooredoo (ORDS) announced that it has reached another milestone as more than 200,000 customers in Qatar connected to its faster fiber network. The achievement was reached on December 13. ORDS’ achievement in providing Ooredoo Fiber – combined with ORDS’ recent launch of 4G Plus (Advanced LTE) – means that ORDS customers can stay connected to the fastest- available internet at home and while moving across the country. According to the UN Broadband Commission report, already in 2014, Qatar has the second highest percentage of household broadband of any developing country, after South Korea, with 96.4% penetration. ORDS has managed to accelerate the pace of people being connected to Fiber in 2014. Around 9,000 homes a month are now being linked to Ooredoo Fiber. Meanwhile, Ooredoo Algeria announced that it has reached 3.5mn 3G subscribers in less than a year after the launch of network in Algeria. (Gulf-Times.com, Bloomberg)

IBB shareholders approve name change to Al Rayan Bank – Islamic Bank of Britain’s (IBB) shareholders have formally granted their approval to change the UK’s only wholly Shari’ah- compliant retail bank, IBB to Al Rayan Bank. The change signifies the beginning of a new chapter for the bank as the European subsidiary of Masraf Al Rayan (MARK). (Bloomberg)

QTA to open offices in US, Turkey in 2015 – The Qatar Tourism Authority (QTA) is planning to open new overseas offices in the US and Turkey in 2015 to further promote the country’s tourism attractions. QTA currently has overseas offices in the UK, France, Germany (to cover the Europe market), Saudi Arabia (GCC), and in Singapore (Southeast Asia with focus on Hong Kong, Malaysia and Singapore), which opened about two weeks ago. (Gulf-Times.com)

International

US factory activity growth at 11-month low in December; Real Estate recovery uneven as housing starts fall – An industry report showed the manufacturing sector in the US continued to expand in December but its growth rate hit an 11- month low. Financial data firm Markit said its preliminary or "flash" US Manufacturing Purchasing Managers Index fell to 53.7 in December, matching the 2014 January low when severe weather impacted economic activity. The December output subindex fell to 54.7, also the lowest since January, from November’s 55.6 final reading. The employment subindex dipped to 52.8 from 55.1. It was the lowest since July, but also the 18th straight month of readings indicating growth in jobs.

Meanwhile, the residential real estate recovery in the US is best described as plodding, with the industry taking a step back in November for the first time in three months. The figures from the Commerce Department showed housing starts declined 1.6%, the first drop since August, to a 1.03mn annualized rate from a revised 1.05mn pace in October that was stronger than previously estimated. The decrease was led by a plunge in the South as other areas registered gains. Building permits also fell in November, indicating a surge in construction is probably not on the cards in the immediate future. (Reuters, Bloomberg)

UK inflation falls sharply in November to 12-year low – Inflation in the UK fell unexpectedly to its lowest level in more than 12 years in November, further easing a squeeze on consumers and leaving the Bank of England (BoE) under no pressure to raise interest rates soon. The Office for National Statistics (ONS) said the Consumer Price Index (CPI) rose by an annual 1.0% in November, compared with 1.3% in October reflecting a slide in global oil prices that has pushed down inflation around the world, and raised concerns about deflation in some countries. Economists taking part in a Reuters poll had expected the CPI to slip back only to 1.2%. Sterling hit a three- week low against the euro after the data and the yield on 10- year British government bonds fell to almost its lowest level since May 2013. BoE Governor Mark Carney said the falling oil prices was an "unambiguously net positive" for Britain's economy, but he also said the BoE would look through the direct effect of the dipping oil prices on inflation. (Reuters)

PMI: Eurozone private sector ends 2014 with weak growth, more price cuts – A recent survey showed Eurozone businesses are ending 2014 in slightly better shape than thought, but growth remains weak and firms are still cutting prices to encourage trade. Markit's Composite Flash Purchasing Managers' Index (PMI), based on surveys of thousands of companies and seen as a good growth indicator, rose to 51.7 from a 16-month low of 51.1. Inflation in the Eurozone cooled to a five-year low of just 0.3% in November, well within the European Central Bank's (ECB) "danger zone", adding to expectations for more policy easing. Weak growth and deepening concerns that plunging oil prices may send the Eurozone into a deflationary spiral will push the ECB to buy sovereign debt early next year, a Reuters poll found last week. A PMI covering the service industry rose to 51.9 from 51.1, beating expectations for 51.5, while the factory PMI posted a similar jump, coming in at 50.8. The Reuters poll had forecasted 50.5. An index measuring factory output that feeds into the composite PMI held steady at 51.2. (Reuters)

German private sector grows at slowest pace in 18 months in December – A recent survey showed private sector in Germany grew at the slowest pace in 18 months in December as a pickup in manufacturing activity failed to offset declining momentum in services. Markit's flash composite Purchasing Managers' Index (PMI), which tracks activity in the manufacturing and services sectors that account for more than two-thirds of the economy, fell to 51.4 in December from a final reading of 51.7 in November. That was above the 50 line denoting growth for the 20th month running, but it was the lowest reading since June 2013 and far below levels seen earlier in 2014. New business fell for a second consecutive month, with the subindex coming in at 49.0. The PMI index tracking services alone fell to a 17-month low of 51.4 from a final reading last month of 52.1, well below the consensus forecast in a Reuters poll of 52.5. The index for the manufacturing sector however rose to 51.2 from 49.5 in November, above a forecast for 50.4. (Reuters)

4. Page 4 of 6

Italy October global trade surplus rises on exports – A recent data showed Italy posted a trade surplus with the rest of the world of €5.39bn in October, rising from a surplus of €3.84bn in October 2013 as exports increased. National statistics office ISTAT said imports fell 1.6% YoY in October, while exports rose by 2.9%. With European Union countries, Italy registered an October trade surplus of €1.37bn, compared with a surplus of €1.04bn in October 2013. Exports to EU nations in October were up 4.7% YoY and imports rose 3.1%. ISTAT said during the first 10 months of 2014, Italy posted a global trade surplus of €33.60bn. (Reuters)

Japan exports rose less than forecast in November – Exports in Japan rose less than forecast in November, underlining challenges to Prime Minister Shinzo Abe’s efforts to steer the economy out of recession. The finance ministry said overseas shipments rose 4.9% YoY, below the Bloomberg median estimate for a 7% gain and less than October’s 9.6% increase. Imports slid 1.7%, leaving a trade deficit of 892bn yen. Abe faces increased pressure to boost growth after a win in an election he fought on a pledge to pursue his Abenomics policies. (Bloomberg)

China industrial activity shrinks in December; FDI rises in November – Activity in China's factory sector contracted in December for the first time in seven months, the latest in a string of weak economic indicators that will intensify calls for more stimulus measures to head off a hard landing. The flash HSBC/Markit manufacturing Purchasing Managers' Index (PMI) fell to 49.5 in December from November's final reading of 50.0 and below the 50.0 forecast by analysts. The new orders sub- index fell to 49.6, the first contraction since April 2014. Meanwhile, Foreign Direct Investment (FDI) in China rose on a cumulative basis in November, breaking four months of consecutive declines as foreign investors moved money into China's services sector at the expense of manufacturing. The Chinese services sector attracted $58.6bn of FDI in the first 11 months of 2014, up 7.9% YoY and significantly outperforming the manufacturing sector, which saw a 13.3% decline as the balance tipped amid a broad economic slowdown. The Ministry of Commerce said China drew $106.2bn in FDI in the first 11 months of 2014, up just 0.7% YoY. The ministry said China attracted $10.4bn in FDI in November alone, up 22.2% YoY. (Reuters)

Russian ruble suffers steepest drop in 16 years – The ruble plunged more than 11% against the dollar on December 16 in its steepest intraday fall since the Russian financial crisis in 1998 as confidence in the central bank evaporated after an ineffectual rate hike. The ruble opened around 10% stronger against the dollar after the central bank unexpectedly raised its benchmark interest rate by 650 basis points to try and halt the currency's slide, but it reversed gains in volatile trade and repeatedly set new record lows. It has now fallen close to 20% this week, taking its losses this year against the dollar to more than 50% and stirring memories of the 1998 crisis when the currency collapsed within a matter of days, forcing Russia to default on its debt. Although Russia's public finances and reserves are much healthier than in 1998, analysts say the country is on the brink of a full-blown currency crisis. (Reuters)

Regional

IMF: GCC does not need to cut spending even as oil falls – According to the International Monetary Fund’s (IMF) Head of Mission for the UAE, Harald Finger, although the oil price plunge is likely to have a major impact on state revenues in the GCC nations, they have big reserves so they will not need to cut state spending significantly. Finger said GCC countries should rein in

state spending, but they should do it in a gradual way to avoid hurting economic growth. Finger also said the UAE might have to tap into its foreign assets if oil prices stayed at current levels or went lower. (Reuters)

Fitch: Stable outlook for most Middle East banks in 2015 – Fitch Ratings has maintained a Stable Outlook on all banks in the GCC region, largely driven by the probability of sovereign support. While public spending on major projects is increasing in Kuwait, Fitch believes it needs to be sustained to feed through into banks' ‘Viability Ratings’. Fitch also expects a positive impact from economic growth in Saudi Arabia, although this is less likely to have an impact on their Viability Ratings, considering their current high levels. Capital levels are expected to remain sound, unless there is significant loan growth. Within the GCC, the banks also enjoy ample liquidity, supported by substantial deposits placed by the governments and related entities. On the other hand, a deeper-than-expected fall in oil prices could put negative pressure on the sector outlook in some of the smaller GCC countries. (Reuters)

Kering explores Puma sale to Mideast, Asian investors – According to sources, Kering SA, the owner of Puma brand is exploring a sale of the German sportswear maker, as efforts to revive the struggling brand drag into the fifth year. Kering, which also owns Gucci, contacted potential buyers earlier this year to gauge interest. Sovereign wealth funds from the Middle East such as Qatar as well as Asian investors have been approached. Kering owns around 86% of Puma, which is valued at about $3.1bn based on the remaining traded shares, is revamping athletic shoes and stepping up marketing as it seeks to reorient the company’s positioning around performance gear. (Bloomberg)

GASCO BoD recommends SR41.25mn dividends for 4Q2014 – The National Gas & Industrialization Company’s (GASCO) board of directors has recommended the distribution of 5.5% dividend (SR0.55 per share), amounting to SR41.25mn for 4Q2014. Shareholders, who are registered with the Securities Depository Center (Tadawul) as on December 21, 2014, will be eligible to receive the dividend. The dividend will be distributed on December 28, 2014. (Tadawul)

Experts: Saudi Arabia 2015 budget likely to be SR800bn – According to experts, Saudi Arabia’s budget would be around SR800bn in 2015 if the oil price ranges between $50-60 per barrel. The Kingdom would possibly adopt an austerity budget or resort to its huge cash reserves. Ihsan Bohaliga, an economics expert, said the government might cut its spending by 20-30% (SR200bn), as compared to its 2014 budget. This would not affect mega projects, some of which have already been delayed in the previous budget plan. However, if the oil price falls below $60 per barrel, the Kingdom may resort to using its reserves to allocate SR855bn as an estimated spending target for 2015. Isam Khalifa, a member of the Saudi Economy Association, said it is likely that the government would base its budget on an oil price of around $65 per barrel, which means it would be 20% lower in 2015 as compared to 2014. The second challenge would be to manage the expected deficit due to huge spending plans, which might be covered by the country’s financial reserves worth SR3tn. (GulfBase.com)

UAE to keep spending despite fall in oil prices – The UAE’s Economy Minister, Sultan bin Saeed al-Mansouri said that the large fiscal reserves built up by the country will allow it to maintain it spending on various development projects in coming years despite the recent plunge in oil prices. According to economists, the drop of Brent crude to near $60 a barrel will

5. Page 5 of 6

cause the UAE to post a moderate budget deficit in 2015. (Reuters)

Dubai SFC: Dubai economy coping well with global difficulties – The Dubai Supreme Fiscal Committee’s (SFC) Chairman, Sheikh Ahmed bin Saeed Al-Maktoum said that the Emirate’s economy is coping well with a difficult global environment and is expected to grow about 4.5% in 2014, with growth rising above that level in coming years. He further said that the government would seek to control inflation to keep the Emirate competitive in business terms. Inflation has been boosted in 2014 by surging house rents. Annual consumer price inflation stood at 4.2% in November 2014, down slightly from 4.4% in October 2014, which was the highest since May 2009. The Dubai government is keen to control its spending and avoid budget deficits. (GulfBase.com)

Abraaj sells 21% stake in IDH – Private equity firm Abraaj Group sold a 21% stake in Integrated Diagnostics Holdings (IDH), a healthcare diagnostics service provider, to emerging markets private equity firm, Actis. Abraaj declined to reveal the value of the deal or the size of its remaining stake in IDH. (Reuters)

CBRE Group: Dubai home-price gains slowed in 2H2014 – According to CBRE Group, Dubai home-price gains slowed in 2H2014, after the government took steps to cool the market. Matthew Green, Head of the UAE Research said average prices climbed 18% in 2014-YTD, compared with an increase of 30% in 2013. He said 1H2014 saw a strong growth in residential sales and leasing, while the market stabilized in the second half. (Bloomberg)

DSE wins AED82.5mn healthcare project in Abu Dhabi – Drake & Scull Engineering (DSE), the engineering subsidiary of Drake & Scull International (DSI), has won an AED82.5mn healthcare project in Abu Dhabi. The project boosts DSI’s total project awards in 2014-YTD to AED5.6bn and the total projects backlog to an all-time high of AED15.3bn across MENA, Europe and Asia. (DFM)

Limitless to sell land to repay a $1.2bn loan – Limitless, the Dubai-government controlled property developer has proposed selling land near Dubai’s main port to help repay its $1.2bn loan as it seeks a second debt restructuring deal with creditors. The company has proposed to pay its lenders in three installments in 2016, 2017 and 2018, instead of the three years through 2016. Rental income from a commercial property near the port in Dubai’s Jebel Ali area will also support payments. Limitless delayed debt payments after asset prices slumped and credit markets froze during the financial crisis. The developer reached a deal with creditors in 2012 to begin repaying the $1.2bn Islamic loan in 2014, around four years after it was due. Emirates NBD, National Bank of Abu Dhabi, Dubai Islamic Bank, Mashreqbank, and Arab National Bank are among its creditors. (Bloomberg)

Ali & Sons to invest AED100mn in Mussafah – Ali & Sons Audi are set to begin the construction of the company’s new Audi Workshop & Service Centre in Mussafah, early in 2015, continuing their strategic expansion plans across Abu Dhabi. This follows approval of the project by the Abu Dhabi Municipality. The exclusive Audi car workshop, being developed at a cost of AED100mn, will allow customers across the capital an easier access to vehicle service facilities. The new facility will also house the largest Audi-approved used car showroom in the Middle East, with as many as 60 pre-owned cars on display. (GulfBase.com)

NBAD stands third in GCC for bond sales in 2014 – The National Bank of Abu Dhabi (NBAD) jumped five spots in the GCC region in terms of bond sales in 2014 to match its highest ranking ever. The Abu Dhabi-based lender underwrote $2.46bn of sales in 2014 to be placed at the third place, the same ranking as in 2012. NBAD stood behind HSBC Holdings and Standard Chartered for debt deals in the GCC region. HSBC remained the Gulf region’s top bond arranger in 2014 for the eighth year running, underwriting $5.5bn of deals, more than double the amount of NBAD, while Standard Chartered underwrote $2.53bn of bonds during the year. (Bloomberg)

ADGM engages Hector Sants as adviser – The Abu Dhabi Global Market (ADGM), Abu Dhabi's new financial free zone has engaged Hector Sants, former Chief Executive of Britain's Financial Services Authority, to advise it as the zone prepares to begin its operations. Sants will advise ADGM until at least mid- 2015 on areas including the creation of its regulatory framework and its strategy. (Reuters)

Oman Air raises capital base to OMR546mn – Oman Air has raised its capital base to OMR546.05mn from OMR471.05mn by injecting an additional OMR75mn received from the government. The additional capital will enable the airline to invest in fleet and route expansion programs. The state-run Oman Air is embarking on a massive expansion program to enhance its fleet strength to 55 planes and to fly to 50 destinations by 2017. Oman Air currently operates to 45 destinations. Oman Air also plans to carry 6mn passengers in 2015, against 5mn passengers in 2013, mainly supported by its route expansion program and heavy investment in technology. (GulfBase.com)

Sohar Freezone leasing plans progressing well – Sohar Port & Freezone’s Executive Commercial Manager, Edwin Lammers said that the first phase of the Sohar Freezone is filling up fast and the second phase expansion plans are being assessed technically and financially. Currently, 227 hectares are occupied with a further 158 hectares committed, representing 80% of the first phase. Both the first and the second phase are a part of a master plan to develop around 4,500 hectares in different phases. (Gulfbase.com)

Omasco appoints MD – Oman Marketing & Services Company (Omasco) has appointed Hussain Mohammed Al Lawati as its Managing Director (MD). He joins Omasco from the Omani Qatari Telecommunications Company, Nawras, where he served as the chief officer of government relations and director of business sales. (Bloomberg)

CBB’s BHD20mn Sukuk issue subscribed 385% – The Central Bank of Bahrain (CBB) announced that the latest monthly issue of short-term Islamic leasing bonds, Sukuk Al Ijara, has received subscription to the tune of 385%. Subscriptions worth BHD77mn were received for the BHD20mn issue. The expected return on the Sukuk is 0.82%, the same as the previous issue on November 13, 2014. The issue begins on December 18, 2014 and carries a maturity of 182 days. (GulfBase.com)

6. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only.

It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this

report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make

any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg (*Value as of 15 December, 2014)

Source: Bloomberg (* Market closed on 16 December) Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Nov-10 Nov-11 Nov-12 Nov-13 Nov-14

QSE Index S&P Pan Arab S&P GCC

(7.3%)

(3.5%)

(2.1%)

0.3%

(2.9%)

(6.9%) (8.6%) (7.3%)

(7.0%)

(5.4%)

(3.8%)

(2.2%)

(0.6%)

1.0%

Saudi Arabia

Qatar

Kuwait

Bahrain*

Oman

Abu Dhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD%

Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,196.93 0.3 (2.1) (0.7) MSCI World Index 1,655.52 0.1 (1.2) (0.3)

Silver/Ounce 15.72 (2.7) (7.7) (19.2) DJ Industrial 17,068.87 (0.7) (1.2) 3.0

Crude Oil (Brent)/Barrel (FM

Future)

59.86 (2.0) (3.2) (46.0) S&P 500 1,972.74 (0.8) (1.5) 6.7

Crude Oil (WTI)/Barrel (FM

Future)

55.93 0.0 (3.3) (43.2) NASDAQ 100 4,547.83 (1.2) (2.3) 8.9

Natural Gas (Henry

Hub)/MMBtu

3.56 (2.6) (0.5) (18.0) STOXX 600 328.88 2.3 (0.1) (9.1)

LPG Propane (Arab Gulf)/Ton 54.75 (1.6) (0.2) (56.7) DAX 9,563.89 3.0 0.1 (9.2)

LPG Butane (Arab Gulf)/Ton* 65.75 0.0 (0.4) (51.6) FTSE 100 6,331.83 3.1 0.7 (10.8)

Euro 1.25 0.6 0.4 (9.0) CAC 40 4,093.20 2.8 0.0 (13.6)

Yen 116.41 (1.2) (2.0) 10.5 Nikkei 16,755.32 (1.3) (2.6) (7.9)

GBP 1.58 0.7 0.2 (4.9) MSCI EM 909.98 (1.5) (3.0) (9.2)

CHF 1.04 0.6 0.4 (7.0) SHANGHAI SE Composite 3,021.52 2.3 2.8 39.6

AUD 0.82 0.1 (0.4) (7.8) HANG SENG 22,670.50 (1.6) (2.5) (2.7)

USD Index 88.13 (0.4) (0.3) 10.1 BSE SENSEX 26,781.44 (2.3) (4.1) 22.5

RUB 67.91 5.7 16.5 106.6 Bovespa 47,007.51 (1.8) (4.7) (21.3)

BRL 0.37 (1.6) (3.0) (13.7) RTS 629.15 (12.4) (21.3) (56.4)

158.9

116.9

108.4