Top Rated Pune Call Girls Dighi ⟟ 6297143586 ⟟ Call Me For Genuine Sex Servi...

9 December Daily Market Report

1. Page 1 of 7

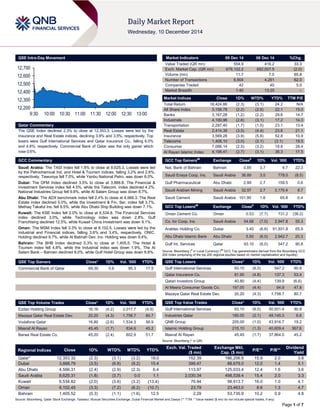

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 2.3% to close at 12,353.3. Losses were led by the Insurance and Real Estate indices, declining 3.9% and 3.5%, respectively. Top losers were Gulf International Services and Qatar Insurance Co., falling 6.0% and 4.8%, respectively. Commercial Bank of Qatar was the only gainer which rose 0.6%.

GCC Commentary

Saudi Arabia: The TASI Index fell 1.8% to close at 8,625.3. Losses were led by the Petrochemical Ind. and Hotel & Tourism indices, falling 3.2% and 2.6%, respectively. Tawuniya fell 7.0%, while Yanbu National Petro. was down 6.0%.

Dubai: The DFM Index declined 3.5% to close at 3,888.8. The Financial & Investment Services index fell 4.5%, while the Telecom. index declined 4.2%. National Industries Group fell 9.8%, while Al Salam Group was down 8.7%.

Abu Dhabi: The ADX benchmark index fell 2.4% to close at 4,566.3. The Real Estate index declined 5.0%, while the Investment & Fin. Ser. index fell 3.7%. Methaq Takaful Ins. fell 9.5%, while Abu Dhabi Ship Building was down 7.1%.

Kuwait: The KSE Index fell 2.0% to close at 6,534.8. The Financial Services index declined 3.0%, while Technology index was down 2.8%. Gulf Franchising declined 12.5%, while Kuwait China Investment was down 9.1%.

Oman: The MSM Index fell 3.3% to close at 6,102.5. Losses were led by the Industrial and Financial indices, falling 3.6% and 3.4%, respectively. ONIC. Holding declined 9.7%, while Al Batinah Dev. Inv. Holding was down 9.4%.

Bahrain: The BHB Index declined 0.3% to close at 1,405.5. The Hotel & Tourism index fell 4.8%, while the Industrial index was down 1.9%. The Al Salam Bank – Bahrain declined 8.0%, while Gulf Hotel Group was down 6.8%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Commercial Bank of Qatar

69.30

0.6

95.3

17.5

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group

16.16

(4.2)

2,017.7

(4.9) Mazaya Qatar Real Estate Dev. 20.20 (4.3) 1,758.7 80.7

Vodafone Qatar

16.80

(2.6)

1,534.3

56.9 Masraf Al Rayan 45.45 (1.7) 834.6 45.2

Barwa Real Estate Co.

45.20

(2.4)

802.9

51.7

Market Indicators 09 Dec 14 08 Dec 14 %Chg.

Value Traded (QR mn)

554.9

416.2

33.3 Exch. Market Cap. (QR mn) 678,102.2 692,007.5 (2.0)

Volume (mn)

11.7

7.0

65.8 Number of Transactions 6,904 4,261 62.0

Companies Traded

42

40

5.0 Market Breadth 1:40 13:25 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return

18,424.86

(2.3)

(3.1)

24.2

N/A All Share Index 3,158.78 (2.2) (2.9) 22.1 15.0

Banks

3,167.28

(1.2)

(2.2)

29.6

14.7 Industrials 4,100.96 (2.6) (3.1) 17.2 14.3

Transportation

2,287.40

(1.7)

(1.5)

23.1

13.4 Real Estate 2,414.39 (3.5) (4.4) 23.6 21.1

Insurance

3,569.28

(3.9)

(5.8)

52.8

10.9 Telecoms 1,408.10 (3.0) (2.1) (3.1) 19.5

Consumer

7,066.14

(2.5)

(3.2)

18.8

28.4 Al Rayan Islamic Index 4,198.41 (2.7) (3.1) 38.3 17.5

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Nat. Bank of Bahrain

Bahrain

0.85

3.7

4.7

22.3 Saudi Enaya Coop. Ins. Saudi Arabia 36.89 3.5 778.0 (8.5)

Gulf Pharmaceutical

Abu Dhabi

2.99

2.7

159.5

0.6 Saudi Arabian Mining Saudi Arabia 32.57 2.7 3,170.4 8.7

Saudi Cement

Saudi Arabia

101.90

1.6

65.8

0.4

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Oman Cement Co.

Oman

0.53

(7.7)

731.2

(36.2) Co. for Coop. Ins. Saudi Arabia 54.68 (7.0) 2,947.8 55.3

Arabtec Holding Co.

Dubai

3.40

(6.6)

91,931.8

65.9 Abu Dhabi Islamic Bank Abu Dhabi 5.50 (6.0) 2,942.7 20.3

Gulf Int. Services

Qatar

93.10

(6.0)

547.2

90.8

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Gulf International Services

93.10

(6.0)

547.2

90.8 Qatar Insurance Co. 81.60 (4.8) 137.3 53.4

Qatari Investors Group

40.80

(4.4)

139.9

(6.6) Al Meera Consumer Goods Co. 197.00 (4.4) 94.9 47.8

Mazaya Qatar Real Estate Dev.

20.20

(4.3)

1,758.7

80.7

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Gulf International Services

93.10

(6.0)

50,931.4

90.8 Industries Qatar 180.00 (2.1) 49,145.3 6.6

QNB Group

205.00

(1.0)

43,916.7

19.2 Islamic Holding Group 215.10 (1.3) 40,609.4 367.6

Masraf Al Rayan

45.45

(1.7)

37,864.0

45.2

Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield

Qatar*

12,353.32

(2.3)

(3.1)

(3.2)

19.0

152.39

186,206.9

15.9

2.0

3.8 Dubai 3,888.79 (3.5) (6.8) (9.2) 15.4 399.47 88,679.0 12.0 1.4 5.1

Abu Dhabi

4,566.31

(2.4)

(2.9)

(2.3)

6.4

113.97

125,033.4

12.4

1.6

3.6 Saudi Arabia 8,625.31 (1.8) (3.7) 0.0 1.1 2,030.34 498,539.4 15.4 2.0 3.3

Kuwait

6,534.82

(2.0)

(3.6)

(3.2)

(13.4)

76.94

99,913.7

16.0

1.0

4.1 Oman 6,102.45 (3.3) (7.2) (6.2) (10.7) 23.79 23,463.0 8.6 1.3 4.7

Bahrain

1,405.52

(0.3)

(1.1)

(1.6)

12.5

2.29

53,735.9

10.2

0.9

4.8

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,20012,30012,40012,50012,60012,7009:3010:0010:3011:0011:3012:0012:3013:00

2. Page 2 of 7

Qatar Market Commentary

The QSE Index declined 2.3% to close at 12,353.3. The Insurance and Real Estate indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari shareholders.

Gulf International Services and Qatar Insurance Co. were the top losers, falling 6.0% and 4.8%, respectively. Commercial Bank of Qatar was the only gainer which rose 0.6%.

Volume of shares traded on Tuesday rose by 65.8% to 11.7mn from 7.0mn on Monday. However, as compared to the 30-day moving average of 13.6mn, volume for the day was 14.3% lower. Ezdan Holding Group and Mazaya Qatar Real Estate Development were the most active stocks, contributing 17.3% and 15.1% to the total volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Earnings and Global Economic Data

Global Economic Data Date Market Source Indicator Period Actual Consensus Previous

12/09

US

US Census Bureau

NFIB Small Business Optimism

November

98.1

96.5

96.1 12/09 US US Census Bureau Wholesale Inventories MoM October 0.40% 0.20% 0.40%

12/09

US

Bloomberg

Wholesale Trade Sales MoM

October

0.20%

0.10%

0.00% 12/09 US Bloomberg IBD/TIPP Economic Optimism December 48.4 47.0 46.4

12/09

France

Ministry of the Economy

Budget Balance YTD

October

-84.7B

–

-80.5B 12/09 France Federal Statistical Off Trade Balance October -4,608M -4,900M -4,721M

12/09

Germany

Federal Statistical Off

Labor Costs WDA YoY

3Q2014

2.30%

–

1.90% 12/09 Germany Federal Statistical Off Labor Costs SA QoQ 3Q2014 0.20% – 1.00%

12/09

Germany

Federal Statistical Off

Trade Balance

October

21.9B

18.9B

22.1B 12/09 Germany Deutsche Bundesbank Current Account Balance October 23.1B 18.0B 23.7B

12/09

Germany

Deutsche Bundesbank

Exports SA MoM

October

-0.50%

-1.70%

5.50% 12/09 Germany Office for National Statist Imports SA MoM October -3.10% -1.70% 5.20%

12/09

UK

Office for National Statist

Industrial Production MoM

October

-0.10%

0.20%

0.60% 12/09 UK Office for National Statist Industrial Production YoY October 1.10% 1.80% 0.80%

12/09

UK

Office for National Statist

Manufacturing Production MoM

October

-0.70%

0.20%

0.60% 12/09 UK Office for National Statist Manufacturing Production YoY October 1.70% 3.20% 2.20%

12/09

Spain

Bank of Spain

INE House Price Index QoQ

3Q2014

0.20%

–

1.70% 12/09 Spain Bank of Spain INE House Price Index YoY 3Q2014 0.30% – 0.80%

12/09

Spain

Bank of Spain

6M T-Bill Amount Sold

9-December

€683.0M

–

€1,190.4M 12/09 Spain Bank of Spain 6M T-Bill Average Yield 9-December 0.28% – 0.21%

12/09

Spain

Bank of Spain

6M T-Bill Bid/Cover Ratio

9-December

5.0

–

3.3 12/09 Spain Bank of Spain 12M T-Bill Amount Sold 9-December €3,819.5M – €3,334.3M

12/09

Spain

Bank of Spain

12M T-Bill Average Yield

9-December

0.4

–

0.3 12/09 Spain Bank of Spain 12M T-Bill Bid/Cover Ratio 9-December 2.0 – 2.0

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari

67.85%

56.39%

63,581,764.50 Non-Qatari 32.15% 43.61% (63,581,764.50)

3. Page 3 of 7

News

Qatar

QNB Group appoints Group CEO – QNB Group’s (QNBK) Board of Directors has appointed Mr. Ali Ahmad Al Kuwari as QNBK’s Group Chief Executive Officer effective from 9 December 2014. Mr. Al Kuwari held the position of Acting Group CEO since July 2013. (QSE)

OBG: Qatar cement demand is seen surging on construction boom – Oxford Business Group (OBG) in its latest Qatar report, citing the Ministry of Development Planning & Statistics data, said that the cement use is set to peak at 57mn tons over a four-year period up to 2017, driven by the construction sector. The country has two domestic producers of the material – Qatar National Cement Company (QNCD) and Al Khalij. QNCD, the larger among the two players with a domestic market share of around 70%, issued a tender for a new factory in April 2013 which is expected to be completed in 2015. Al Khalij also has plans to expand its capacity. The Qatar Primary Materials Company (QPMC) is also taking steps to facilitate imports and is working on a cement silo near its Mesaieed gabbro berths. The report said the consumption of other construction staples like gabbro – a rock aggregate used to make concrete is also set to rise. According to MDPS data, the state’s construction sector is set to use 265mn tons of the aggregate over the next few years. (Gulf-Times.com)

Qatar plans chicken farm IPO to resolve poultry meat shortage – Qatar government is planning to lease 5.7mn square meters of land to private investors to develop a chicken farm for investors to buy into in 2015. According to Investment House CEO Hashem Aqeel al-Aqeel, the farm backed by Qatari investors will have the capacity to produce 45mn kilograms (99mn pounds) of chicken meat by 2018. Investment House is a Doha-based bank that is an adviser on the project. Institutional investors committed QR750mn, and an IPO is possible as early as 2015. Qatar’s only existing poultry producer, the Arab Qatari Company is 40% owned by Hassad Food, the agricultural investment arm of the Qatar Investment Authority, the country’s sovereign wealth fund. (Bloomberg)

VFQS receives top global information security certification – Vodafone Qatar (VFQS) is the first telecommunications operator in Qatar and the region to be awarded the prestigious ISO 27001:2013 certification, demonstrating the strength of the company’s information security management systems and operations in Qatar. The ISO 27001:2013 certification, awarded by the British Standards Institution (BSI), sets the international standard for best practice management and enhancement of information security systems in telecommunications and other data-driven industries. (Bloomberg)

Ashghal: Part of Khalifa Street closed for maintenance – The Public Works Authority (Ashghal) said a part of Khalifa Street from Al Markhiya Intersection to Al Gharafa Intersection will be closed from December 11, 2014. The closure will be for two days and is part of the ongoing maintenance works. (Peninsula Qatar)

International

Job openings point to sustained US payroll gains – The US Labor market continued to show traction in October as job openings held near the highest level in almost 14 years and the number of people quitting and getting hired remained elevated. The Labor Department reported that the number of positions waiting to be filled rose by 149,000 to 4.83mn, the second- highest level since January 2001. Other reports showed small companies were becoming more optimistic and wholesalers

boosted stockpiles. Increasing help-wanted ads, hiring and resignations paint a more vibrant picture amid signs that the labor market is improving as the US economy picks up. The readings are among those tracked by Federal Reserve Chair Janet Yellen and her colleagues to help policy makers decide when the expansion is strong enough to raise interest rates. (Bloomberg)

BofA, Citi expect lower trading revenue in 4Q2014; US extends scrutiny of StanChart on sanctions compliance – According to recent presentations made at an investor conference in New York, Bank of America Corp (BofA) and Citigroup Inc (Citi) expect weaker trading revenue in 4Q2014. BofA said its sales and trading revenue are expected to fall from both 3Q2014 and a year earlier. BofA did not provide any numbers for the quarter. Meanwhile, Citigroup Inc CEO, Mike Corbat said that the bank’s market revenue will fall by about 5% as it will record $2.7bn in litigation expenses and another $800mn in repositioning charges, leaving the third-largest US bank "marginally profitable" in 4Q2014. Corbat's announcement at a New York investor conference was the second time in six weeks the bank has had to tack on a massive legal charge. The costs stemmed from government investigations into possible manipulation of foreign exchange markets, setting of LIBOR interest rates and lax compliance of money laundering rules. Past legal charges have foreshadowed settlements of cases. Before the announcement, analysts had expected Citigroup would make about $3.4bn in 4Q2014, instead of a small profit. Meanwhile, Standard Chartered (StanChart) will face another three years of scrutiny by US prosecutors for compliance with government sanctions against certain countries. The original deferred prosecution agreements, struck with the US Justice Department and the Manhattan district attorney over the bank's violations related to US sanctions on Iran and other countries, was due to expire on December 10. The agreement to extend the deals means that the bank will face enhanced oversight for a longer period of time and could be hit with harsher penalties. (Reuters)

ONS: UK October factory output slides – The UK’s industrial output unexpectedly fell in October as manufacturing was dragged down by a sharp fall in production of electronic products, following a strong September. The Office for National Statistics (ONS) said the output for industry overall fell 0.1% in October having jumped by a revised 0.7% in September. The manufacturing output tumbled 0.7% – its biggest monthly decline since May – hit by a 4.5% fall in computer, electronic and optical products. The ONS said pharmaceutical and chemical goods also weighed on the factory sector. An ONS official said there was no sign of significantly different levels of demand for British exports, which economists have said could be hit by the slowdown in the Eurozone. (Reuters)

German imports fall at fastest pace in almost two years – German imports posted their steepest drop in almost two years in October after a strong rise in September, while exports also fell, but economists remained upbeat about the prospects for Europe's largest economy. Seasonally-adjusted data from the Federal Statistics Office showed imports declining by 3.1% MoM, undershooting by far a consensus forecast for a 1.5% decrease. It was the sharpest fall since November 2012. Exports also dropped by 0.5% MoM, though that was a better reading than the 1.5% decline that a Reuters poll had forecasted. Exports rose to a record high of €103.9bn on an unadjusted basis, while imports also climbed to their highest level in two years. (Reuters)

4. Page 4 of 7

ECB: Falling oil price may push inflation below zero – European Central Bank (ECB) Executive Board member Peter Praet said falling oil prices could push the Eurozone inflation rate below zero, just as policy makers prepare to examine options for quantitative easing. Praet said given the dipping oil prices inflation may temporarily fall into the negative territory in the coming months. He further added that normally any central bank would prefer to look through a positive supply shock. After all, lower oil prices boost real incomes and may lead to higher output in the future. However, ECB may not have that luxury at present. The ECB intends to expand its balance sheet by as much as €1tn to flood the Eurozone with liquidity, and will review its current stimulus early in 2015. Plunging oil prices are putting further downward pressure on inflation that slowed to 0.3% in November, nudging the central bank toward the politically controversial path of large-scale government-bond buying. (Bloomberg)

China factory-gate deflation deepens as consumer prices slow – The factory-gate deflation in China deepened and consumer prices climbed at the slowest pace since 2009, signaling room for further monetary easing. The National Bureau of Statistics said the producer-price index dropped 2.7% YoY in November, compared with the median projection of a 2.4% decline in a Bloomberg survey. Consumer prices rose 1.4%, compared with the 1.6% increase in October. Falling oil and metals prices have cut costs for China’s factories, leading to lower export prices and adding to disinflation pressure across the world. China’s central bank cut interest rates for the first time in two years as the economy heads for its weakest full-year growth since 1990. (Bloomberg)

Regional

Arcadis to develop integrated water plan for Makkah – Arcadis has been awarded a major contract by the Saudi Arabian government to develop water, wastewater, treated sewage effluents and an asset management master plan for the region of Makkah. Under the 18-month contract, Arcadis will support the National Water Company (MCBU) in expanding and improving the city’s water supply and service. (GulfBase.com)

ICO: Saudi Arabia coffee market valued at SR15bn – According to statistics issued by the International Coffee Organization (ICO), coffee consumption has risen sharply in the Kingdom of Saudi Arabia with imports of 18,000 tons worth SR203mn. The growth in coffee processing has helped boost the Saudi market for cafes to a notable SR15bn. The report showed that 1.4bn cups of coffee are consumed a day worldwide. (GulfBase.com)

Dur Hospitality seeks financing for expansion – Saudi property & hotel developer Dur Hospitality Company is planning to tap financing from commercial banks as it expands in the Kingdom. Dur Hospitality’s CEO, Badr Albadr said that the company’s balance sheet is strong and under-leveraged, so the expansion will be done partially by company’s own cash flow. A bigger component will be from commercial bank loans. (Bloomberg)

Al Tayyar signs partnership deal with Amadeus – Al Tayyar Travel Group (Al Tayyar) has entered into an agreement with Amadeus, a global travel solutions provider to enhance its operational efficiencies with specially designed distribution services being provided to the group’s customers worldwide. Under the agreement, Al Tayyar will utilize the innovative Amadeus distribution technology to maintain its competitive edge in the tourism sector. (AmeInfo)

SAICO gets SAMA’s approval for insurance products – Saudi Arabian Cooperative Insurance Company (SAICO) has obtained the Saudi Arabian Monetary Agency’s (SAMA) temporary approval to use its insurance product. Approval has been given for the product ‘enhanced group personal accident and sickness insurance’ for six months starting from December 8, 2014. (Tadawul)

Fitch: Public spending offers favorable outlook for Saudi banks – Fitch Ratings stated the high public sector spending in the Kingdom will continue to offer a favorable macroeconomic outlook and business opportunities for Saudi banks in 2015. Saudi banks expanded their loan portfolios by an annualized 17.4% in 1H2014, as compared to 14% in 2013. Fitch, in its new special report, expects credit growth to remain strong in 2H2014 as well as in 2015. Despite the strong asset growth, Saudi banks continue to be well capitalized with an average core capital ratio of 16% during 1H2014. Their loan-to-deposit ratio is among the best in the region. However, Fitch said that given the growth in longer-term lending and that all banks have asset/liability maturity gaps, it believes the banks would benefit from diversifying their funding base by raising their long-term funding. (Reuters)

Bank of Sharjah plans to refinance $200mn loan – The Bank of Sharjah’s Executive Director, Varouj Nerguizian said that the UAE-based bank is planning to refinance a $200mn two-year loan maturing in 2015, with the hopes of benefitting from lower borrowing costs. Nerguizian stated the refinancing should be completed in 1Q2015, with the bank still to decide whether to raise the amount to $250mn and whether to extend the tenure on the new facility to 3-4 years. (Reuters)

AHG plans to spend AED2bn on Dubai projects – Al Habtoor Group (AHG) is planning to build two hotels, 74 homes and a polo club in Dubai in order to capitalize on the booming property market. The company, which is already constructing three hotels with 1,600 rooms in Dubai, will spend AED2bn on its new projects. The group is investing an overall AED15bn in Dubai on various projects to be completed by 2017-end. Although AHG has cast doubts over its plans for an imminent initial share sale, it expects revenues to more than double over the next five years helped by strong local economic growth. Reportedly, a number of local banks have been appointed to help arrange an initial public offering as 1Q2015, although Khalaf al-Habtoor indicated a deal might not be forthcoming any time soon. (GulfBase.com, Reuters)

Tiger Woods-designed golf course to be built in Dubai – Damac Properties has brought in renowned golfer Tiger Woods to design its new 18-hole championship golf course in Dubai, which will be operated by The Trump Organization. This update comes almost four years after another planned golf course was canceled in the wake of the city’s property market collapse. Damac said that the course will be a part of the Akoya Oxygen residential project and will include a clubhouse, restaurant and pro shop. The project is set to open by the end of 2017. (Bloomberg)

DEC urges to strengthen trade relationship with India – According to a report by the Dubai Economic Council (DEC), the Emirate should seek to establish its own bilateral trade and investment protection agreement with India, which is its top trading partner. The report outlined proposals for supporting sustainable economic growth. According to government data, the value of the Emirate’s foreign trade topped AED1.3tn in 2013, half of which was with Asia. According to HSBC, trade between the UAE and India reached $75bn in 2012-13, up from $43bn in 2009-10. The UAE is also India’s top export

5. Page 5 of 7

destination, accounting for more than 10% of exports. By 2030, India is expected to become the UAE’s top export destination and a bilateral agreement was signed last year to protect investments in both countries. (GulfBase.com)

Omniyat starts work on tower in Dubai Maritime City – Omniyat Group has begun work on a 48-storey tower in Dubai Maritime City. The developer valued the tower at AED600mn and predicted that it would be completed in 2017. Omniyat Group’s Chief Executive, Mahdi Amjad said the tower is 80-90% funded through equity from its shareholders, bank lending and off-plan sales. (Reuters)

Waha Capital to invest AED4bn across four sectors – Waha Capital is eyeing potential investments of up to AED4bn in infrastructure, energy, education and healthcare sectors, in order to build on its recent successful investments in AerCap and National Petroleum Services. The firm said that its investments in the oil, gas & energy sector may reach around AED2bn in the next two years, while investment in the power & infrastructure sector may touch AED1bn, and up to AED500mn has been assigned for both education and healthcare sectors. The firm forecasts that the average return on equity over the next three years will reflect significant improvement as compared to the average of the last three years. (GulfBase.com)

SAA CEO: Etihad may buy minority stake – According to South African Airways’ (SAA) Acting CEO, Nico Bezuidenhout, Etihad Airways could buy a minority stake in SAA. He said that a potential deal could also include closer commercial ties. The unprofitable airline is seeking to strengthen its commercial relationship with Etihad. (Bloomberg)

ADFG acquires New Scotland Yard for £370mn – Abu Dhabi Financial Group (ADFG) has bought London’s New Scotland Yard for £370mn. The alternative investment company has paid £120mn more than the original price estimate. The firm is planning to build homes on part of the site about half a mile away from the Buckingham Palace. (Bloomberg)

Dnata expects revenue to double from travel service companies – UAE-based Dnata’s President, Gary Chapman said that Dnata expects revenue contribution from its travel services companies to more than double in FY2014-15. Chapman said that travel services accounted for around 10% of its revenue, over a year ago. In FY2014-15, this revenue will be over 20% because of the new investments the company has made. Dnata’s division of travel service companies saw their revenue increase by 161% to AED873mn in the six months to September 30, 2014. The Emirates Group subsidiary has acquired assets in the UK including Stella Travel Services and Gold Medal Travel Group this year. (GulfBase.com)

KIPCO changes name to KAMCO Investment Company – KIPCO Asset Management Company’s shareholders have agreed to change the name of the company to KAMCO Investment Company. Shareholders at an extraordinary general assembly approved all resolutions on the agenda for KAMCO, which included modification of item no. 2 in the articles of association and item no. 1 in the memorandum of incorporation relating to the company’s commercial name. (GulfBase.com)

NBK: Kuwait records 7.7% YoY credit growth in September 2014 – According to the National Bank of Kuwait’s (NBK) economic report, the total credit in Kuwait grew 7.7% YoY, while a relatively large monthly gain was registered in September 2014. These gains were led by household credit and lending for the purchase of securities. Money supply (M2) growth dropped to its slowest pace in two years, as M2 shrank in September 2014 on declines in Kuwaiti Dinar time and FX deposits.

Household debt was up KD138mn, though growth continued to ease to 12.7% YoY. Credit to non-bank financials saw its largest monthly increase in five years as it gained by KD57mn. However, the sector, which has been deleveraging since 2009, saw its credit shrinking by 9.2% YoY. Securities lending gained by KD144mn with growth rising to 7.2% YoY. Other sources of growth were trade, real estate and industry, while some weakness came from a decline in the construction sector. (GulfBase.com)

Investment Dar eyes second debt-for-assets deal – Kuwait- based Investment Dar hopes to complete its second debt-for- assets deal with creditors by the end of March 2015. Investment Dar will circulate a draft framework for the deal next week, so that lenders can review the documentation and hold bilateral discussions with Investment Dar's adviser, before an all-creditor meeting on January 21, 2015. (Reuters)

NCSI: Oman registers 0.95% YoY inflation in November 2014 – According to a report issued by the National Center for Statistics & Information (NCSI), the rate of inflation in Oman stood at 0.95% in November 2014, when compared with November 2013. Additionally, inflation increased by 0.1% on a MoM basis. Food & non-alcoholic beverages rose by 1.2% on an annual basis, while housing, water, electricity, gas and others grew by 0.32%. Furnishings, household equipment & routine household maintenance grew by 6.23%. During November, education costs recorded an increase of 4.51%, while, health costs increased by 4.96% and communications costs rose by 5%. Hotel & restaurant costs rose marginally by 0.66%, while tobacco prices increased by 1.72%. The monthly increase in inflation is attributed to the rise of food & non-alcoholic beverages by 0.36%, while prices for housing, water, electricity, gas and other fuels rose by 0.03%. In addition, tobacco prices increased by 0.7%, transport costs rose by 0.06% and hotels & restaurants costs grew by 0.03%. On the other hand, costs of health declined by 0.04%, while communication costs declined by 0.02%. Recreation & culture prices declined by 0.03% and miscellaneous goods & services declined by 0.06%. (GulfBase.com)

DRA opens office in Oman – DRA, a South Africa-based engineering group, has opened an office in Oman. DRA is a multi-disciplinary engineering group that delivers mining, minerals processing and infrastructure services right from concept to commissioning along with comprehensive operations and maintenance service. (GulfBase.com)

OMPET to produce PET bottles in Sohar – Sohar Port & Freezone has signed a deal with Oman International Petrochemical Industry Company (OMPET) to build a fully renewable manufacturing facility that will produce 1.5mn tons of eco-friendly packaging materials. The plant will complement the port's existing petrochemicals supply chain and will feed into a global beverage industry that is currently valued at approximately $1.3tn. Under the agreement, OMPET will lease a 330,000-square-meter land at Sohar for the production of 250 kilotons of polyethylene terephthalate (PET), which is used to manufacture PET bottles. (GulfBase.com)

Sun Metals awards $400m steel plant contract to Posco E&C – Posco Engineering & Construction (Posco E&C), a unit of South Korean steelmaker Posco, has won a $400mn contract from Sun Metals to build a steelmaking and rolling mill plant at Sur industrial complex. The plant will have a capacity to manufacture 2.5mn tons of billets, steel bars and special steel. Work on the project and is likely to be completed by the middle of 2016. (GulfBase.com)

6. Page 6 of 7

SICO appoints COO, finance head – Securities & Investment Company (SICO) has announced new management appointments. Anantha Narayanan, who joined SICO in 2008 as the Head of Internal Audit, will be taking over as COO. Meanwhile, the company has appointed Wissam Haddad as the Head of Corporate Finance. (Bahrain Bourse)

7. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only.

It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this

report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make

any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Nov-10 Nov-11 Nov-12 Nov-13 Nov-14

QSE Index S&P Pan Arab S&P GCC

(1.8%)

(2.3%)

(2.0%)

(0.3%)

(3.3%)

(2.4%)

(3.5%)

(4.2%)

(3.6%)

(3.0%)

(2.4%)

(1.8%)

(1.2%)

(0.6%)

0.0%

Saudi Arabia

Qatar

Kuwait

Bahrain

Oman

Abu Dhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD%

Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,230.92 2.3 3.2 2.1 MSCI World Index 1,721.97 (0.3) (1.0) 3.7

Silver/Ounce 17.09 4.4 4.9 (12.2) DJ Industrial 17,801.20 (0.3) (0.9) 7.4

Crude Oil (Brent)/Barrel (FM

Future)

66.84 1.0 (3.2) (39.7) S&P 500 2,059.82 (0.0) (0.7) 11.4

Crude Oil (WTI)/Barrel (FM

Future)

63.82 1.2 (3.1) (35.2) NASDAQ 100 4,766.47 0.5 (0.3) 14.1

Natural Gas (Henry Hub)/MMBtu 3.60 3.1 5.2 (17.1) STOXX 600 340.48 (1.7) (2.2) (6.8)

LPG Propane (Arab Gulf)/Ton 52.50 4.5 (9.1) (58.5) DAX 9,793.71 (1.6) (2.1) (7.9)

LPG Butane (Arab Gulf)/Ton 69.50 (0.7) (9.2) (48.8) FTSE 100 6,529.47 (1.9) (2.6) (8.4)

Euro 1.24 0.5 0.7 (10.0) CAC 40 4,263.94 (1.9) (2.7) (10.8)

Yen 119.69 (0.8) (1.5) 13.7 Nikkei 17,813.38 0.5 1.3 (3.7)

GBP 1.57 0.1 0.6 (5.4) MSCI EM 965.41 (1.2) (2.1) (3.7)

CHF 1.03 0.5 0.7 (8.1) SHANGHAI SE Composite 2,856.27 (5.6) (3.3) 32.0

AUD 0.83 (0.0) (0.3) (7.0) HANG SENG 23,485.83 (2.4) (2.2) 0.8

USD Index 88.69 (0.4) (0.7) 10.8 BSE SENSEX 27,797.01 (1.5) (2.5) 31.0

RUB 54.24 0.8 2.6 65.0 Bovespa 50,193.47 0.6 (3.6) (11.3)

BRL 0.39 0.3 (0.1) (8.8) RTS 857.51 (1.5) (5.6) (40.6)

177.5

135.1

124.5