The German Credit data provides variables that help classify observations as good credit vs bad credit. Multiple algorithms such as Logistic Regression, Classification tree, GAM, Neural Net and Linear Discriminant Analysis were used to compare the classification power of the models built.

Top profile Call Girls In dimapur [ 7014168258 ] Call Me For Genuine Models W...

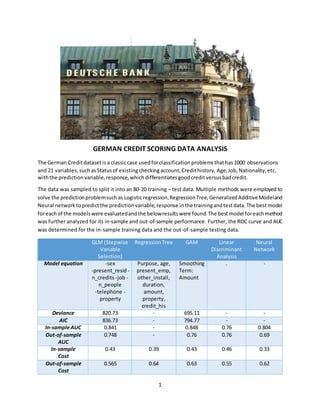

German credit data analysis

1. 1

GERMAN CREDIT SCORING DATA ANALYSIS

The German Creditdatasetisa classiccase usedforclassificationproblemsthathas1000 observations

and 21 variables,suchas Statusof existingcheckingaccount,Credithistory, Age,Job,Nationality,etc.

withthe predictionvariable,response,whichdifferentiatesgoodcreditversusbadcredit.

The data was sampled to split it into an 80-20 training – test data. Multiple methods were employed to

solve the predictionproblemsuchas Logisticregression,RegressionTree,GeneralizedAdditiveModeland

Neural networktopredictthe predictionvariable,response inthe trainingandtestdata.The bestmodel

foreachof the modelswere evaluatedandthe belowresultswere found.The bestmodel foreachmethod

was further analyzed for its in-sample and out-of-sample performance. Further, the ROC curve and AUC

was determined for the in-sample training data and the out-of-sample testing data.

GLM (Stepwise

Variable

Selection)

RegressionTree GAM Linear

Discriminant

Analysis

Neural

Network

Model equation -sex

-present_resid -

n_credits -job -

n_people

-telephone -

property

Purpose, age,

present_emp,

other_install,

duration,

amount,

property,

credit_his

Smoothing

Term:

Amount

. -

Deviance 820.73 - 695.11 - -

AIC 836.73 - 794.77 - -

In-sample AUC 0.841 - 0.848 0.76 0.804

Out-of-sample

AUC

0.748 - 0.76 0.76 0.69

In-sample

Cost

0.43 0.39 0.43 0.46 0.33

Out-of-sample

Cost

0.565 0.64 0.63 0.55 0.62

2. 2

GERMAN CREDIT SCORING DATA

BACKGROUND:

The GermanCreditdatasetisaclassiccase thatcanbe usedtoforclassificationproblems.Itwascollected

by the Prof.Hofmann in1994. The original file waseditedmultiple timesandseveral indicatorvariables

were addedtomake it suitable foralgorithmswhichcannotcope withcategorical variables. The dataset

classifies customers as good or bad credit risks based on a set of attributes.

ABOUT THE DATA:

The dataset contains 1000 observations and 21 variables, such as Status of existing checking account,

Credithistory, Age,Job,Nationality,etc. The data was furthersampledtosplitit into an 80-20 training–

test data using a seed value of 12420360.

MODEL SELECTION:

An asymmetriccostfunctionwasdefinedwithacut-off probabilityof 1/6. Essentially,the False

Negatives (actual 1butpredict0) were givenaweightof 5, while the False Positives (actual 1but predict

0) were givenaweightof 1.

1. GENERALIZED LOGISTIC REGRESSION:

I) Full Model:

For the full model,the responsevariable, responsewasmodeledagainstall the 20 explanatory

variables.The devianceof the full model wasfoundtobe 697.47 and the AIC 795.47.

Many of the variables were foundtobe significant,hencerequiringvariable selectionmethods.

Deviance AIC BIC

697.47 795.47 1025.02

II) Variable Selection (using AIC and BIC):

Employingstepwise variable selectionmethodstoidentifythe bestmodel topredict response,step-wise

variable selection inbothdirections wasused.The nullmodelwasbuiltwithaconstantandthe full model

was built with all variables. AIC and BIC were both explored as the criterion for the variable selection

method.

Using AIC:

The final model obtained as a result of Step-wise AIC had the below formula.

Final Model: response ~chk_acct + duration+ credit_his+purpose + amount + saving_acct+

present_emp+installment_rate +other_debtor+age + other_install +housing+

foreign

Deviance AIC BIC

708.72 780.72 949.37

3. 3

Using BIC:

The final model obtained as a result of Step-wise BIC generated a much simpler model with only 4

predictor variables.

Final Model: response ~chk_acct + duration+ age + other_install

Deviance AIC BIC

820.73 836.73 874.20

From the resultsof the step function,the bestmodel wasdeterminedusingAICcriterion withthe lowest

AIC value of 780.72.

Choosingthe stepwiseAICmodel asthe final model,predictionof the response variable wasdone to

calculate the in-sampleandout-of-sample error.Further, the ROCplotwasdrawn,andAUC was

calculatedforbothin-sample andout-of-sample.

Deviance AIC BIC

708.72 780.72 949.37

Fig 4. ROC plots for the Final Logistic Regression Model

In - sample Out – of – sample

MCR Cost AUC MCR Cost AUC

0.32 0.43 0.841 0.365 0.565 0.748

2. CLASSIFICATION TREE:

The CART technique separatesthe datasetintobinsbyprogressivelyaddingvariable-valuecombinations

to the sequence,ensuringthatat each stepthe splitincreasesthe homogeneityof the resultingsubsets

of observations.All 800 observationsinthe trainingdatasetwere fedintothe classification tree andthe

below tree was observed.

4. 4

Fig 4. Classification Tree

Calculatingthe AsymmetricMisclassificationcostandthe misclassificationrate forthe Classificationtree

for the in-sample andout-of-sampledatageneratedthe followingresults.

In-sample Out-of-sample

MCR Cost MCR Cost

0.32 0.39 0.42 0.64

3. GENERALIZED ADDITIVE MODELS:

A generalizedadditive model wasbuiltwithanon-linearcomponenttothe variables –duration,amount

and age, the only numerical fields. From the summary of this GAMmodel, the edf of duration and age

were foundtobe 1, indicatingnopolynomialrelationshipwiththe responsevariable,response.The GAM

generated the below plots showing the polynomial relationship with the response.

Fig 5. GAM Plots

For the final GAMmodel builtafterretainingthe polynomialrelationshipforthe amountvariable,the

deviance,AICandBICwas calculated.

5. 5

Deviance AIC BIC

695.11 794.77 1028.20

The model wasalsotestedforthe in-sample misclassificationcostand AUCwiththe 80% trainingdata

and the out-of-sample misclassificationcostandAUC withthe 20% trainingdata. Anoptimal cut-off

probabilityof 1/6was usedforthe out-of-samplepredictioncut-off.

In - sample Out – of – sample

MCR Cost AUC MCR Cost AUC

0.32 0.43 0.848 0.395 0.63 0.76

Fig 6. ROC plots for the Final GAM Model

4. LINEAR DISCRIMINANT ANALYSIS:

To performa lineardiscriminantanalysis,the response variable,response wascodedasafactor.The LDA

was performed using the lda() and in-sample and out-of-sample misclassification cost and AUC were

calculated.

In - sample Out – of – sample

MCR Cost AUC MCR Cost AUC

0.32 0.46 0.76 0.37 0.55 0.76

Fig 7. ROC plots for the Final LDA Model

6. 6

5. NEURAL NETWORK:

Toimplementtheneural networkalgorithm,adatapreprocessingstepisrequired.The datapreprocessing

step is necessary to ensure that the algorithm converges. The independent variables were normalized

with the max-min scaling using x = (X-Xmin)/(Xmax-Xmin).

Choosing8hiddennodestorunthe neuralnetwork,the asymmetricmisclassificationcostwascalculated.

In - sample Out – of – sample

MCR Cost AUC MCR Cost AUC

0.24 0.33 0.804 0.34 0.62 0.69

Basedonthe MSPE valuescalculatedforthe Neuralnetwork,the modelperformsthe bestincomparison

with all the models run. The below ROC curves were generated for the Neural network. Clearly neural

networks don’t perform the best for this data set.

Fig 7. ROC plots for the Neural Network Model

CONCLUSION:

Summarizing the results from all the models run for the prediction problem, the below table was

populated.Fromthe belowtable,comparisonsin the performance betweenin-sample measurescanbe

done usingAIC,In-sample MSPE,while betweenthe out-of-sample measurescanbe done usingthe out-

of-sample MSE.

GLM (Stepwise

Variable

Selection)

RegressionTree GAM Linear

Discriminant

Analysis

Neural

Network

Model equation -sex

-present_resid -

n_credits -job -

n_people

Purpose, age,

present_emp,

other_install,

duration,

Smoothing

Term:

Amount

. .

7. 7

-telephone -

property

amount,

property,

credit_his

Deviance 820.73 - 695.11 - -

AIC 836.73 - 794.77 - -

In-sample AUC 0.841 - 0.848 0.734 0.804

Out-of-sample

AUC

0.748 - 0.76 0.69 0.69

In-sample

Cost

0.43 0.39 0.43 0.46 0.33

Out-of-sample

Cost

0.565 0.64 0.63 0.55 0.62

Fig 9. ROC plots comparing the in-sample, out-of-sample measures for all models

From the table above,it’sclearthatthe GAM model performsthe bestintermsof the in-sample and

out-of-sample AUCmeasures.Thisisalsobettervisualizedusingthe plotsbelow.

However,intermsof the misclassificationcost,the GAMprovesveryexpensive.Withrespecttothe

cost, the LDA performsbest.However,strikingabalance betweenthe AUCandcost,the Logistic

Regressionmodelworksbestforthe GermanCreditData.