Recommended

More Related Content

Similar to Basic of accounts

Similar to Basic of accounts (20)

More from Navratan Sharma

More from Navratan Sharma (20)

Recently uploaded

Recently uploaded (20)

Basic of accounts

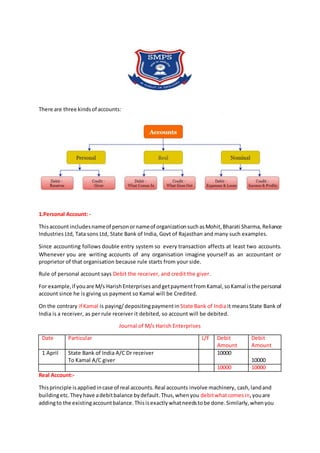

- 1. There are three kindsof accounts: 1.Personal Account: - Thisaccountincludesnameof personornameof organizationsuchasMohit,Bharati Sharma, Reliance Industries Ltd, Tata sons Ltd, State Bank of India, Govt of Rajasthan and many such examples. Since accounting follows double entry system so every transaction affects at least two accounts. Whenever you are writing accounts of any organisation imagine yourself as an accountant or proprietor of that organisation because rule starts from your side. Rule of personal account says Debit the receiver, and credit the giver. For example,if youare M/s HarishEnterprises andgetpaymentfromKamal,soKamal isthe personal account since he is giving us payment so Kamal will be Credited. On the contrary if Kamal is paying/depositingpaymentin State Bank of Indiait meansState Bank of India is a receiver, as per rule receiver it debited, so account will be debited. Journal of M/s Harish Enterprises Date Particular L/F Debit Amount Debit Amount 1 April State Bank of India A/C Dr receiver To Kamal A/C giver 10000 10000 10000 10000 Real Account:- Thisprinciple isappliedincase of real accounts.Real accounts involve machinery, cash, landand buildingetc.Theyhave adebitbalance bydefault.Thus,whenyou debitwhatcomesin,youare addingto the existingaccountbalance.Thisisexactlywhatneedstobe done.Similarly,whenyou

- 2. creditwhatgoesout, youare reducingthe account balance whena tangible assetgoesoutof the organization. For example M/sShri WaterLtd , buysa machinery foritsbusinesscostingRs40,000, here we find that machineryis real accountand it iscomingto our businesssoitwill be debitedwe are making paymentbycheque of SBI, SBI ispersonal accountand givingthe paymentsogiverwill be credited. Journal of M/s Shri Water Ltd. Date Particular L/F Debit Amount Debit Amount 1 April Machinery A/C Dr what comes in To State Bank of India credit the giver 40000 40000 40000 40000 Nominal Account: Thisrule isappliedwhenthe accountin questionisa nominal account.The capital of the companyis a liability.Therefore,ithasadefaultcreditbalance. Thisaccountincludes allexpenses /losses suchas rent,salary, commissionpaidand all income and gain such as commissionreceived,profitonsale of assets. Whenyoucreditall incomesandgains,you increase the capital andby debitingexpensesand losses,youdecreasethecapital.Thisisexactlywhatneedstobedoneforthesystemtostayinbalance. For example: Suppose M/s Shri water Ltd paid electricity bill for Rs 10000 here electricity exp is real account and expenses are debited. Cash is real account so credit what goes out. Journal of M/s Shri Water Ltd. Date Particular L/F Debit Amount Debit Amount 1 April Electricity Expense A/C Dr all expenses To State Bank of India credit the giver 10000 10000 10000 10000

- 3. Process of writing Journal Entries Nowbefore we startwritingjournal entries, we mustbe able toidentify nature of the accountand accountingrule beingfollowedafter everytransaction. Colourcodingenablesyoutounderstandthe journal comfortably. S.No Transactions Accounts Nature of accounts Rule Dr/Cr Entry 1 Rahul started businesswith cash Cash A/c Rahul’s capital A/c Real A/c Personal A/c Dr what comesin Cr the giver Dr Cr Cash a/c Dr To Rahul capital 2 Purchases goodsfrom Mohit andgave cheque of SBI Purchase A/c SBI A/c Nominal A/c Personal A/c Dr All expenses Cr the giver Dr Cr Purchase A/CDr To SBI A/C 3 Boughtmachine from M/s XYZ Co. Machine A/c M/s XYZ A/c Real A/c Personal A/c Dr what comesin Cr the giver Dr Cr Machine A/c Dr T0 M/s XYZ a/c 4 Commission Received fromM/s Bharati Entp.Rs10000 (cash) Commission is received in form of cash Cash A/c Commission A/c Real A/c Nominal A/c Dr what comesin Cr all incomes Dr Cr Cash A/c Dr To commission received a/c 5 Cash payment receivedform Mr Jack Cash A/c Mr Jack A/c Real A/c Personal A/c Dr what comesin Cr the giver Dr Cr Cash A/c Dr To Mr.Jack A/c From the followingtransactionswritethe journal of M/sAmishaMachineryPvtLtd,Jaipur 1. Started businesswithcashRs20,00,000/-, Building35,00,000/-, Deliveryvan5,00,000/- 2. Openedbankaccountand depositedcashRs10,00,000 intoSBI 3. Purchased10 small generatorscostingRs20,000/- fromM/s KirloskerEngineering. 4. Cheque issuedtoM/sKirloskarforRs 1,50,000/- 5. 3 generators soldforRs 30,000 each forcash. 6. PurchasedgoodsRs 1,50,000 and cheque givenforRs1,48,000 in full payment. 7.PaidelectricitybillbycashRs 1500/- 8. Soldgoodsto M/s RajasthanTradersRs 14000/- and cheque depositedintoSBI. 9. Paidsalary Rs 70,000 10. Soldoldoffice furniture Rs21000. Solution withdetailed explanations

- 4. 1. In firsttransactionswe have fouraccounts Cash,Building,DeliveryvanandAmishaCapital account. All assetsaccountsare real accountssince theyare comingintoto businesssoaspertheirnature that iswhat comesinwill be debited.Amishaisthe businessownerwhoisgivingcapital sorule is creditthe giverso Amishaa/cis credited. Cash A/CDR 200000 Buildinga/cDr 350000 DeliveryvanA/CDr 500000 To capital 600000 2. We have two accountsSBI and cash , SBIis the receiverandpersonal account& saysdebitthe receiversowill be debitedandcashisreal account and sayscreditwhat goesoutso cash is goingout of business. State Bank of IndiaA/C Dr 100000 To Cash 100000 3.There are twoaccounts Purchase andKirlosker,here generators are the purchasesasthe companyisengagedinsellingof machinerysogeneratorispurchase forthe company. Purchase isnominal accountsaysdebitall expensessowill be debitedandkirloskerisgiverof generatorssowill be credited. Purchases a/cDr200000 To Kirloskaer200000 4. Two accounts are effectedKirloskerandSBIaccount, cheque issuedmeansbankaccountthatis SBI isgiverof paymentwhere rule appliescreditthe giveranddebitthe receiverbothare personal account Kirloskerisreceiversowill be debited. 5.Two accountsare effected generatorssoldmeansSalesa/cthat isnominal accountas salesbrings income sorulesappliescreditthe income andcashisanotheraccount isreal account saysDr what comesin. Nowexplainthe entriesfrom6to 10 as have beenmentionedabovebytakingfollowingsteps. 1. Identifythe accountsinvolvedinthe transactions 2. Findthe accountsnature 3. Thinkwhat to Debitor credit 4. Explainthe transaction. 5. write the journal