Recommended

Recommended

More Related Content

Similar to Implementation Quick Fixes in Germany

Similar to Implementation Quick Fixes in Germany (20)

Recently uploaded

Recently uploaded (20)

Implementation Quick Fixes in Germany

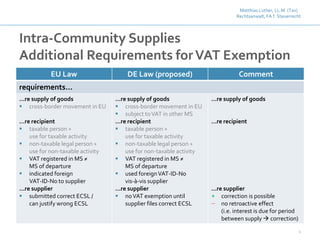

- 1. Matthias Luther, LL.M. (Tax) Rechtsanwalt, FA f. Steuerrecht 1 Intra-Community Supplies Additional Requirements forVAT Exemption EU Law DE Law (proposed) Comment requirements… …re supply of goods ▪ cross-border movement in EU …re recipient ▪ taxable person + use for taxable activity ▪ non-taxable legal person + use for non-taxable activity ▪ VAT registered in MS ≠ MS of departure ▪ indicated foreign VAT-ID-No to supplier …re supplier ▪ submitted correct ECSL / can justify wrong ECSL …re supply of goods ▪ cross-border movement in EU ▪ subject toVAT in other MS …re recipient ▪ taxable person + use for taxable activity ▪ non-taxable legal person + use for non-taxable activity ▪ VAT registered in MS ≠ MS of departure ▪ used foreignVAT-ID-No vis-à-vis supplier …re supplier ▪ noVAT exemption until supplier files correct ECSL …re supply of goods …re recipient …re supplier + correction is possible no retroactive effect (i.e. interest is due for period between supply correction)

- 2. Matthias Luther, LL.M. (Tax) Rechtsanwalt, FA f. Steuerrecht 2 Intra-Community Supplies Presumption re Cross-Border Movement EU Law DE Law (proposed) Comment requirements transport / dispatch … …by supplier ▪ 2 items of accepted evidence …by recipient ▪ 2 items of accepted evidence + “acquirer’s statement” …by supplier ▪ 2 items of accepted evidence ▪ 1 item of accepted evidence + invoice copy …by recipient ▪ 2 items of accepted evidence + “acquirer’s statement” ▪ 1 item of accepted evidence + invoice copy …by supplier + Germany continues to accept same evidence as in the past …by recipient + Germany continues to accept same evidence as in the past

- 3. Matthias Luther, LL.M. (Tax) Rechtsanwalt, FA f. Steuerrecht 3 Intra-Community Supplies Consignment Stock EU Law DE Law (proposed) Comment requirements… …re supply of goods ▪ cross-border movement in EU ▪ goods = business assets ▪ Supply to recipient after arrival ▪ sales contract prior departure …re recipient ▪ VAT registered in MS of arrival ▪ calls-off within 12 months ▪ records supply in stock register …re supplier ▪ not established + no fixed establishment in other MS ▪ transport or dispatches goods ▪ knows recipient and recipient’s VAT-ID-No in MS of arrival ▪ reports in ECSL ▪ records supply in stock register …re supply of goods ▪ cross-border movement in EU ▪ goods = business assets ▪ supply to recipient after arrival ▪ sales contract prior departure …re recipient ▪ VAT registered in MS of arrival ▪ calls-off within 12 months ▪ records supply in stock register …re supplier ▪ not established + no fixed establishment in other MS ▪ transport or dispatches goods ▪ knows recipient and recipient’s VAT-ID-No in MS of arrival ▪ reports in ECSL ▪ records supply in stock register …re supply of goods …re recipient …re supplier ! Some MS interpret Welmory broadly. Third party suppliers might be treated as fixed establishment. ➢ Would block consignment stock simplification.

- 4. Matthias Luther, LL.M. (Tax) Rechtsanwalt, FA f. Steuerrecht 4 Supply Chains EU Law DE Law (proposed) Comment scope… …re movement ▪ EU -> EU …re allocationVAT exemption ▪ transport/dispatch by middle party …re movement ▪ DE -> DE ▪ EU -> EU ▪ EU -> non-EU ▪ non-EU -> EU …re allocationVAT exemption ▪ transport/dispatch by 1st party ▪ transport/dispatch by middle party ▪ transport/dispatch by last party …re movement ! May not be accepted by CJEU ! May not be accepted by CJEU …re allocationVAT exemption ! ≠ CJEU’s jurisprudence -> might be helpful for appeal ! ≠ CJEU’s jurisprudence -> might be helpful for appeal CJEU allocates based on transfer of right to dispose of goods DE tax authorities allocate based on obligation to transport