1. 1

Krause Fund Research

Fall 2015

Energy

Recommendation: HOLD

Analysts

Landon Kowalski

landon-kowalski@uiowa.edu

Matt Loochtan

matthew-loochtan@uiowa.edu

Company Overview

Tesoro Corporation (TSO) is a nation leading refiner

and marketer of petroleum products. Their expertise is

refining crude oil into fuel necessary for transportation,

such as gasoline, jet fuel, diesel fuel, as well as a few

other smaller grade products. Tesoro’s operations

include six refineries across the United States that

produce a combined 850,000 barrels per day. Their

products are sold in 17 states through commercial,

retail, and wholesale avenues. Revenue for the fiscal

year ended December 31st, 2014 was at $40.63 billion,

an increase from $37.6B the year prior.

Stock Performance Highlights

52-week High $116.89

52-week Low $64.16

Beta Value 1.56

Average Daily Volume 2.54 m

Share Highlights

Market Capitalization $13.44 b

Shares Outstanding 1.204 b

Book Value per share $43.84

EPS (as of FYE 12/31/14) $6.94

P/E Ratio 8.65

Dividend Yield 2.17%

Dividend Payout Ratio 14.25%

Company Performance Highlights

ROA 12.40%

ROE 25.74%

Sales $40.61 b

Financial Ratios

Current Ratio 1.63

Debt to Equity 95.64%

Tesoro Corp. (NYSE: TSO)

November 14, 2015

Current Price $111.66

Target Price $120.29

TSO Exhibits Growth Limitations

Tesoro’s sales have sky rocketed the past couple years,

along with their stock price. Their impressive growth will

not be sustained as they approach their crude oil refining

capacity of 850 mbpd. We forecast much smaller growth for

the years ahead.

We expect oil prices to make a slow recovery, so the

outlook for the oil refining and marketing industry is not as

strong because costs will increase and profit margins may

decrease.

Tesoro makes third party purchases of refined products

to meet demand requirements for their retailers. If these

purchases were to increase because they are not able to

produce enough, profit margins would be negatively

impacted.

We expect an increase in interest rates in December,

which would negatively impact Tesoro because they carry

an above average level of debt for the industry. Financing

costs would increase and we foresee investors reducing

exposure to stocks.

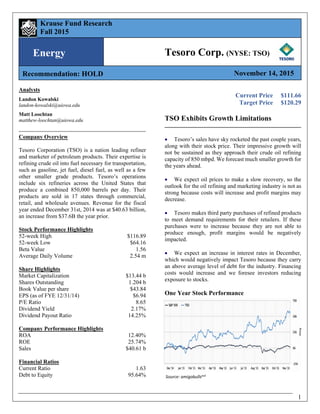

One Year Stock Performance

Source: amigobullsxvii

2. 2

Overview

There are many economic factors that drive the energy

sector, chief among them are crude oil prices and interest

rates. However, within the drivers of crude oil prices are still

more factors such as demand for oil and supply of oil. For

our economic outlook, we have broken down the indicators

that drive crude oil prices and have extensively covered

these “sub-drivers” since the energy sector is essentially

commodity based.

Oil Demand from OECD and Non-OECD Countries

Demand for oil is driven by global economic growth in both

developed countries (OECD) and developing and emerging

countries (Non-OECD). Consequently, world oil demand

has been fairly correlated with Real GDP growth, rising

between 1-2% annually.i

Source: EIAii

Above is a graph charting the consumption of all liquid fuels

(i.e. oil, LNG, gasoline, etc.) against WTI prices and world

GDP growth. Between Non-OECD and OECD countries,

growth in oil demand is strongest in developing and

emerging countries (Non-OECD). These countries tend to

rely extensively on manufacturing versus services and thus

demand more energy for consumption. According to the

Energy Information Administration (EIA), OECD demand

for oil actually declined between 2000 and 2010.ii

However,

growth in oil demand in countries such as China, India, and

Saudi Arabia, as well as other Non-OECD nations increased

by 40% over that period of time.ii

Future growth in world oil demand will likely stem from

these developing nations and have a larger influence on oil

prices over the next few decades. However, when taking

into account China’s lackluster growth and projected

growth rates, oil demand will have to stem from either a

pickup in Chinese growth and/or a shift towards Indochina

countries in the near future. In addition, oil prices will likely

recover at a slower pace for 2015 and 2016 as evidenced by

the EIA estimates provided below. World oil prices are

likely to recover from $41.55 bbl to $49 bbl by the end of

2015 and $51 bbl by 2016.ii

We estimate 2017 and 2018 oil

per barrel prices to be $60 and $70 bbl, respectively,

eventually stabilizing around $75-80 bbl by 2019, with

marginal growth in our CV year of 2020. This recovery will

be driven by a combination of higher demand from these

developing countries and a weakening of supply output in

North America, which will be discussed in the Supply of

OECD and Non-OECD Countries section.

GDP Growth

OECD GDP growth rates have been forecasted at 2%, 2.2%,

and 2.3% for 2015, 2016, and 2017, respectively.iii

The

United States has forecasted GDP growth rates of 2.4%,

2.5%, and 2.4% for the same time period above.iii

We

believe these estimates are reasonable considering the

mature economies of most OECD participants as well as

troubling indicators in regards to deflationary pressure in

Europe and general lackluster growth. For these reasons, we

do not foresee a return to 3.5% GDP growth for at least the

next 5 years, and instead forecast stable GDP growth at

2.75% for our CV year.

We focused on China, India, and Indonesia’s GDP growth

rates since we believe the main sources of oil demand

growth will be derived by these three nations and their

general geographic areas. China’s GDP growth estimates

are 6.8%, 6.5%, and 6.2%, for 2015, 2016, and 2017,

respectively.iii

However, these GDP growth estimates are in

line with the Chinese governments reported forecasts and

we believe that these growth estimates are over-inflated.

Capital Economics, Citibank, Conference Board, and

Lombard Street have put the forward growth rates at about

3.8% to 4.9% for the next 5 years.iv

The declining forecasted

GDP growth rates provide insight into China’s sluggish

demand and are partly responsible for the decline in oil

prices since 2014.

India’s GDP growth rates are forecasted at 7.2%, 7.3%, and

7.4% for the corresponding period above. Indonesia’s GDP

growth rates are estimated at 4.7%, 5.2%, and 5.5% for the

same period.iv

Considering India’s reliance on services over

manufacturing as opposed to China’s economic makeup

favoring manufacturing, India is positioning itself as a

service economy with services making up 57.9% of its

current GDP growth.v

Thus, we agree with the estimates

provided. In regards to Indonesia, their resilient

manufacturing growth will be tested by the coming interest

rate rise by the United States Federal Reserve, but we

believe that the estimates provided have accounted for this

uncertainty in its growth rates.

The much higher growth rates provided by Non-OECD

countries, if realized, will be the main source of world oil

consumption growth moving forward and will likely result

Economic Outlook

3. 3

in a tightening of oil prices since oil prices rise with higher

demand, assuming constant supply.

Oil Output of Non-OPEC and OPEC Countries

Non-OPEC countries can roughly be seen as OECD

countries with the main exceptions being that Russia and

Brazil are not participants in OPEC. Non-OPEC countries

are currently responsible for producing 60% of the world’s

oil production, whereas OPEC is responsible for 40% of

production.vi

Source: EIAii

Above is a graph charting the production of liquid fuels by

Non-OPEC countries against the WTI price of oil. As can

be witnessed by the graph, Non-OPEC production has

increased dramatically in the last 5 years. The main cause

of increase has been the “fracking revolution” in North

America. Once uneconomical, shale and oil plays have now

become accessible through technological advances that

allow unconventional drilling (fracking and oil shale

drilling) to be profitable at estimates averaging at or above

$65 bbl. The massive growth in North American production

has acted as a catalyst for the 43% decline in oil prices since

2014.vii

We believe that higher-cost producing sub-industries, such

as unconventional companies along with off-shore drilling

companies will either slow down production or go bankrupt

due to lack of free cash flows and high long-term debt

payments maturing within the next 2-3 years. In the short-

term, however, many of the North American onshore high-

cost producers have shut down 60% of their drilling rigs

year to date, and have transitioned to low-cost, high-

producing oil plays.viii

Due to this transition, rig usage

declines have yet to cause a significant decrease in oil

production. Thus, we believe oil supplies will largely stay

bloated for the next 2 years, until these firms run into free

cash flow problems.ix

Source: EIAii

OPEC oil production is a different story all together. From

2005 to 2015, OPEC has consistently lost market share to

North American, Latin American, and Russian oil

companies, seeing a decline of 7% from 40% to 33% over

that period.xxi

In an effort to sustain their current market

share, they have decided on a strategy of stable production

growth that is contrary to the usual production cuts that

OPEC would have taken to prop up oil prices in the world

market. This strategy has contributed to the further erosion

of oil prices. We believe that OPEC will continue this

strategy until it is adequately satisfied that high-cost North

American companies will not pose a medium-term threat to

its market share in the future.

Crude Inventories

Crude inventories are an excellent indicator for viewing and

forecasting oil demand and supply in the world. When oil

inventories build up, either a lack of demand or

uneconomical oil prices are usually to blame. In either

event, the market tends to react negatively to upward trends

in crude inventories whereas a decrease in inventories

usually corresponds with growing demand, resulting in

higher oil prices. Unfortunately, for the 2015 year, crude

inventories have been steadily building up. However, since

we have forecasted oil prices to recover largely by 2019,

although not to their peak 2014 levels, crude inventories

should start to decrease moving forward.

Source: EIAii

4. 4

Interest Rates

Interest rates can be a positive or a negative for almost every

sector, especially for the high-capital intensive energy

sector. Most energy companies borrow heavily to both

magnify returns and help fund operations. When interest

rates are low, borrowing costs, or corporate bond yields,

generally drop as a response. Thus, there is a positive

correlation between interest rates and corporate bond yields

as demonstrated by the graph below.

Source: FREDxii

We believe that the Federal Reserve, in light of recent

positive economic data, will more than likely raise interest

rates in late December 2015 from a low of .25%.xiii

We

project the Fed Funds Rate will rise to 1% by the end of

2016, Janet Yellen’s goal, and then about 1% increases per

year to settle at 4% in 2019-2020. The main effect this rate

rise will have on the energy sector is to make refinancing

and further debt issuances more costly for borrowers. As we

have stated, we believe that higher-cost oil producers such

as fracking and tar sand companies will likely go out of

business with higher debt and interest repayments, but an

interest rate rise will act as a catalyst for this event to

happen. When interest rates rise, these companies will have

trouble financing their operations and will subsequently

either have to issue equity, sell off assets, or file for

bankruptcy. In any event, oil production should decrease as

more players leave the industry, which further justifies our

view that oil prices will rise when supply tightens in the next

2-3 years.

Conclusion

After taking into account the demand and supply equations

that are so prominent in understanding what drives crude

prices, and thus, the energy sector, we have concluded that

currently, the market is awash in oil supply and demand

from China is weak. The result: low oil prices. However,

when adjusting our view out 2-3 years, we forecast a pickup

in Chinese and Indochina demand as well as a decline in oil

production, largely stemming from North American output,

to put upward pressure on prices. We believe that these

forecasts and assumptions are reasonable and are generally

in line with the EIA and other analyst estimates.

Overview

Tesoro Corporation operates in the oil, gas, and

consumable fuels industry. More specifically, they are

a part of the oil refining and marketing sub industry,

which focuses primarily on the downstream side of the

energy business.

Recent Developments and Trends

Future Rebound in Oil Prices

As previously mentioned, crude oil supply levels have

been hitting record highs recently with production

outpacing slowing demand. We forecast crude oil prices

to rebound slowly the next five years, which will also

cause revenues to climb back. Given this industry is the

mature stage of its lifecycle; profit margins will most

likely remain fairly stable during this period. However,

there is a chance for profit margins to slightly decline

should the rise in price outpace the rise in demand,

which many industry experts are forecasting to happen.

Lower profits margins will hurt the industry with lower

net incomes and a potential sell off for investors.

Source:IBISWorldxiv

Standards and Regulations

Further revenue growth in this industry is likely to be

hindered by newly enforced regulations by the

Environmental Protection Agency (EPA). They will

require vehicles manufactured after 2016 to have a

higher minimum fuel efficiency of 36 mpg.xiv

These

regulations combined with the fact that more and more

consumers are deciding to purchase hybrid and electric

cars will lead to less demand at the pump.

Markets and Competition

Major integrated oil companies (IOCs) represent the

majority of the refining capacity in the US. These

companies, such as Exxon Mobile and Royal Dutch

Shell, have a competitive advantage with their huge,

customer ready retail segments and wide array of

refineries. However, these IOCs have really struggled

Industry Outlook

5. 5

in other large upstream areas of their business with this

huge drop in oil prices. On the other hand, the

performance and value in refiners have been increasing

as their costs have been very low. This can be seen in

the desirable positive year to date returns in the oil

refining and marketing industry. Going forward, with

oil prices likely to make a smooth recovery, we are not

confident this trend will hold as costs will go back up.

Success within this smaller group of oil refining

specific companies revolves around the ability to have

have a direct sales outlet through a large retail network,

large enough refining capacity to meet demand if

necessary, and low purchase prices of crude to

maximize profit margins.

The major players in this industry and how they

compare are shown in the table below:

Porter’s Five Forces

Threat of New Entrants

The oil and gas refining and marketing industry has

very difficult barriers to entry because of the inability

to build new refineries. Laws are in place restricting

where refineries can be built because they are extremely

undesirable to live near and significantly devalue

property. Companies must compete for the refineries

already in existence, should they need the extra capacity

to grow and fulfill demand requirements.

Threat of Substitutes

The threat lies in emerging alternative sources of energy

as we become more conscious of our impacts on the

environment. The large growth in electrically operated

vehicles and other fuel alternatives has already started

to have an impact on the demand and prices of oil.

Should these substitutes continue to grow at a fast pace,

it could spell trouble for the refining industry.

Power of Suppliers

Given that prices of crude oil are market based,

suppliers have little power over refineries. Refiners will

source out the cheapest price per barrel they could find

to keep costs low. The power is very much in the hands

of the refining companies because they can negotiate

costs and are never committed to one supplier.

Power of Buyers

The power of retailers and wholesalers is moderate to

low, since market prices are the main determinant.

Retailers and wholesalers will search and choose

whichever refiner offers them the cheapest prices;

however, many retailers are owned by refining

companies and, therefore, direct sales outlets.

Rivalry Among Competitors

Competition is very high among companies in this

industry on the basis of price and quality of the product.

They compete to purchase the lowest priced crude

possible from the suppliers in order to be able to charge

lower prices for their final products while maintaining

the same profit margin or greater.xiv

Overview:

Tesoro is a leading refiner and marketer of petroleum

products that has grown substantially the past few years.

Tesoro generates revenue mainly through refining, but

also has transportation and retail segments that assist in

sales. They own six refineries across the United States

that produces a combined 850,000 barrels per day.

Their products are sold in 17 states through commercial,

retail, and wholesale avenues. Revenue for the fiscal

year ended December 31st, 2014 was at $40.63 billion,

an increase from $37.6B the year prior.

Source: Item 1. 10Kxvi

Products

Tesoro refines crude oil to produce four different types

of fuels that are eventually sold to their consumers.

These products are gasoline, jet fuel, diesel fuel, and

heavy fuel oils/residuals and the percentage of total

production for each are shown in the chart below.

Company Analysis

6. 6

Source: Item 1. 10Kxvi

Note: these are 2014 numbers. Each year production can vary

slightly for all segments.

Given gasoline is 49% of Tesoro’s output; a large portion of

their revenues weighs on the sale of this product. It is vital

for gasoline sales to continue to consistently grow into the

future to supply Tesoro with growth in revenues and profits.

Recent Performance

In the third quarter of 2015, Tesoro reported earnings per

share of $6.13 beating the consensus estimates of $6.05. The

lower cost to obtain crude oil and the widening profit

margin drove the higher than expected EPS. Revenues for

the quarter were reported as $7.74 billion, which also came

in higher than the consensus of $7.1 billion, but are down

30.6% from the prior year’s third quarter. The lower

revenues from the year prior were attributable to lower oil

prices. Tesoro capitalized on these lower costs by increasing

their gross margins from 5.59% to 17.96%xv

. The graph

below shows a comparison of five-year cumulative returns

for Tesoro, the S&P 500, and its peer competitors

(Marathon, Phillips, Valero, and HollyFrontier.) The

returns for Tesoro have outpaced its industry competitors by

59% the past 5 years.

Source: 10kxvi

Production

Tesoro purchases their crude and other feedstock from both

domestic and foreign suppliers. As of 2014, oil sourced

from domestic and foreign suppliers are 59% and 41%

respectively2

. As previously mentioned, they refined an

average of 825,000 barrels per day (mbpd) in 2014, just

25,000 below capacity. The two California refineries are

responsible for the largest amount of volume, which was

523 mbpd in 2014. Second is the Pacific Northwest

refineries that refined 171 mbpd total. The mid-continent

refineries produce the least amount with a total of 131

mbpd. The table below shows the gross refining margin

($/Throughput barrel) in 2014 for each region:

California $10.76

Pacific Northwest $10.43

Mid-Continent $23.44

Source: Income Statement 10Kxvi

Many companies like to expand or make their current

refineries more efficient to increase capacity should

capacity limit their growth, such as in Tesoro’s case.

Being that their pacific-northwest refineries currently

have some of the lowest capacities and the largest

profit margin, we believe they will look to increase

capacity should they choose to do so. This margin

would be extremely advantageous leading to large

increases in net income.

Distribution channels

In 2013, Tesoro acquired a logistics company, capitalizing

on the opportunity to significantly cut transportation costs

and provide a more efficient way to distribute their

products. This midstream division, which is now known as

Tesoro Logistics LLC, owns 3,500 miles of pipelines, 28

truck and marine terminals, and over 9 million barrels of

storage capacity. This division provides Tesoro with a huge

competitive advantage because they have a faster, more cost

effective method of delivering their products and increasing

customer satisfaction.

Competition

Tesoro has competition with other major refining

companies like Valero, HollyFrontier Corp, Alon USA

Energy Inc., and Sunoco. With refined barrels per day for

each company at:

Valero 2,900,000

HollyFrontier Corp 443,000

Alon USA 217,000

Sunoco 900,000

Tesoro 850,000

Source: Company’s homepage

Tesoro produces the third highest number of barrels per day

between companies that only focus on refining and

marketing. Producing a smaller amount of barrels per day

for Tesoro will ultimately limit their sales. Areas of concern

for these companies are not just the price per barrel, but the

7. 7

Valuation Analysis

effect of supply and demand. The more consumer demand

the more revenue the companies will bring in.

Brand awareness is a big competitive factor in marketing to

retailers. Volume of production, availability of finished

goods, and ease of transportation to the retailers all affect

competition. Since Tesoro produces less barrels then

Sunoco and Valero, they may lose out on potential deals

with bigger retailers due to lack of supply.

Dividend Payout

Tesoro recently upgraded their dividend to shareholders.

They are paying out $2.00 per share each year with this

updated release, which puts them above the competitors in

payout to investors. Valero pays $1.60 per share,

HollyFrontier pays $1.32 per share, and Alon USA pays

$.60 per share. Tesoro is confident in their ability to keep

generating greater profits and shows appreciation towards

investors believing in them as well.

Competitive advantage

As stated before, Tesoro has their own logistics company

TLLP (Tesoro Logistics) that delivers the refined oil to the

retailers. The revenues that the logistics partner creates are

an extra benefit for Tesoro’s revenue. As of FYE 2014,

TLLP saw $600 million in revenues with $206 million in

operating income, giving Tesoro a boost of about $400

million in realized profits. In general, Tesoro Logistics

charges on a fee-based schedule for gathering, processing,

and transporting crude and refined oil for other companies.

However, with Tesoro having their own partnership, they

are able to save on all the costs usually incurred by their

competitors. By carrying out this method, they try to

channel to the consumer better and cheaper.

Tesoro’s recent expansion into the Basin area of North

Dakota allows them to someday pump the oil out of the

dense oil fields in which the basin area is located. However,

we do not foresee Tesoro making any more big acquisitions

or expansions through 2020, which limits Tesoro from

growing larger.

Catalysts for Growth/Change

If oil prices continue to drop slowly or even keep steady for

a couple years, Tesoro’s value could see a constant increase.

Since Tesoro is a refiner and marketer, the oil prices seems

to have very little affect on the oil prices.

Tesoro’s growth may take a halt this year as their refining

yield is over capacity. The past three years, the yield has

gone up on average 150 thousand barrels per day. But as of

this year, the refining yield cannot get much higher for the

forecasted years to come.

The U.S has many government regulations and public

concerns for the environment and, therefore, it would be

hard to build a new refinery. The only way to continue

growth for Tesoro would be capital spending towards the

increase of capacity.

S.W.O.T Analysis

Strengths

Tesoro has a strong presence in the northwestern part of the

United States while most competitors are in other locations.

Tesoro is also the second largest refinery and marketing

company in the United States.

The recent expansion of logistics into the Bakken Formation

of North Dakota, Montana, and Canada helps to increase the

number of retailers they have readily available. Also, the

expansion increases the revenues from the Logistics

Partnership that they own.

Earnings were unbelievable for Tesoro by more than

doubling net income from the previous year at $224 million

to $586 million.

Weaknesses

Tesoro only produces and ships within the United States,

which limits connections and opportunities around the

world.

Massive increase in growth from the past three years are

going to sustain themselves and level out to a lower than

average rate.

Opportunities

The Refining and Marketing oil companies have become the

only positive trading companies in the oil industry YTD.

This situation is due to the decrease in oil prices that is

lowering revenues and outlooks for other subsectors.

Threats

The recent oil price decrease can eventually have an affect

on the oil industry as a whole, but has yet to cause too much

trouble.

Government regulations are becoming more non-refinery

friendly because of the push for cleaner air and less harm to

our ozone layer and earth.

Summary

We are issuing a HOLD rating for Tesoro after

reviewing the results from our model. We used methods

such as enterprise DCF, economic profit, relative

valuation, and the dividend discount model to value

Tesoro. We calculated a price target of $120, which is

only 7.8% shy of where it is trading now, so it doesn’t

8. 8

Sensitivity Analysis

provide much room for profits. In essence, the most

significant factors of our model are the sales/revenue

forecasts, the forecasts for profit margins,

Revenue Decomposition

Tesoro’s revenues are decomposed into the following

three segments: refining, transportation, and retail. The

refining segment is responsible for approximately

93.8% of all revenues when taking into account

intersegment sales. The major growth limitation is

Tesoro’s refining capacity. Unless they are able to

acquire more refineries, which we cannot predict, their

growth will be extremely limited to non-existent.

Refining throughput for 2014 was only 25,000 barrels

of crude oil per day below their capacity, so our forecast

shows little growth. Operating at full capacity day in

and day out is not realistic due to unforeseeable

circumstances, so we had to take that into consideration

as well.

Product sales growth could still outpace changes in

production if Tesoro decides to increase third party

purchases to meet demand requirements. Although the

boost in the products sales leads to higher revenues,

these sales would be on lower profit margins providing

Tesoro with miniscule increases to net income or even

decreases.

WACC

We calculated Tesoro’s WACC to be 6.94%. We used the

yield to maturity on the 30-year U.S. Treasury bond to

calculate our risk free rate at 2.9%. Also used the U.S.

geometrical average as the market risk premium of

4.62%. Tesoro’s beta was calculated by averaging different

time frames, and averaged 1.168. This high beta means

Tesoro is more volatile than the actual market. With this

information we were able to calculate the cost of equity and

cost of debt of 8.3% and 3.9% respectively from our CAPM

model.

DCF/EP Model

We believe the DCF model delivers the most accurate

estimates for our intrinsic price value because of our

changing FCF, and our small CV growth rate. We chose a

growth rate of 0.5% after 2020 due to the mature lifecycle

that the oil refineries are in.

The DCF model produced an intrinsic price per share value

of $120.35. We have strong beliefs that Tesoro should trade

at this price due to positive FCF on hand. After FYE 2017

we expect a positive return on FCF due to a strong increase

in invested capital.

Relative Valuation Models

We chose to include smaller direct competitors to Tesoro

that had similar EPS or P/E ratio for 2015. The average P/E

ratio for its competitors in 2015 and 2016 came to be $14.4

and $15.3, respectively. While in the same years Tesoro

produced P/E ratios of $13.1 and $28.3, respectively. Due

to drop in EPS for 2016 by 54% or $4.56 the outlook for

relative P/E in 2016 is substantially increased. All the

calculations came out to an intrinsic price of $122.40. It

shows that Tesoro trades at a premium compared to other

companies in the forecasted model.

DDM Model

The DDM model came up with a little bit lower price than

the other models had given us, at an adjusted price of

$96.96, on November 15,2015. This number was mainly

based on our ROE of 13.55% and our CV EPS of $10. This

model expects dividends to keep increasing through CV

date due to the consistent increase Tesoro has had in

dividends each year. It is still difficult to predict future

dividends, therefore, predicting future price using this

model can still be unclear.

Sensitivity analysis becomes an important part of

valuation with the DCF/EP model due to the nature of

small changes having big affects on a company’s value.

CV ROIC vs. WACC

Since we use the DCF model to ultimately make our

decision about our intrinsic price it is important to

understand how each variable can affect our price.

These two are important in estimating our future cash

flows. A 1% increase in the WACC will lead to an

increase in price of $17.59, or 15% of the original value.

However, a decrease by the same percent leads to a

decrease in price of $15.12, or 13%. When the ROIC

changes in our table it has a less of affect in a price

change. With 1 percent change higher and lower the

equivalent price change becomes 0.5% and -0.07%

respectively. The ROIC is reliant on the consistency of

a company’s NOPLAT and beginning invested Capital.

If NOPLAT continues to rise as beginning invested

capital lowers, the chain affect is a higher ROIC and a

more valued company. Tesoro is expected to increase

their value due to the predicted CV ROIC to stay above

the WACC for the upcoming years.

9. 9

Beta vs. Market risk Premium

The beta and market risk premium table shows how

companies fluctuate based on relativity to the market

and common risk rates. If Tesoro were to be completely

correlated with the market it would have an increased

stock price. Also the higher market risk premium is the

lower the stock price would be and vice versa for lower

risk premium. With each decrease in beta of .1 the stock

seems to increase to 7%. This is due to less risk

associated with higher correlation in market risk. Since

Tesoro on average has beaten the S&P for yearly

returns, the risk associated with Tesoro is at a premium

from that of the S&P.

CV growth of EPS vs. Cost of Debt

Due to the already use of maximum capacity that

Tesoro has in 2014, this restricts more growth than

at the present time. Having predicted a lower

growth rate for EPS has a big affect on intrinsic

stock price. Increasing the CV growth rate by 150

basis points would grow the intrinsic stock $18.63

higher. This affects our DCF model intuitively due

to the more growth a company has the higher it

would be valued at. Cost of debt is a big factor in

increasing and decreasing the WACC. With an

increase in 50 basis points of cost of debt our stock

price decreases by 2.5% and a decrease of the same

number increases price by 2.6%.

Market Risk Premium vs. Risk Free Rate

With Interest rates at record lows right now, the

correlated risk free rate is also very low. But as the

Fed talks about hiking interest within the next year

it is imperative for the risk free rate to increase as

well. Due to a high debt to equity ratio that Tesoro

takes on the interest rate spike would have a

daunting affect on its earnings. Either they have to

lower their D/E or the interest rates are going to

lower the intrinsic price of the company. The rate

increase will deliberately lower our valuation price

because of the 95.64% of D/E that Tesoro utilizes.

WACC

$120.29 5.53% 6.03% 6.53% 7.03% 7.53% 8.03% 8.53% 9.03%

8.74% 181.08$ 156.23$ 135.56$ 118.10$ 103.18$ 90.28$ 79.03$ 69.13$

9.24% 181.80$ 156.87$ 136.13$ 118.62$ 103.65$ 90.71$ 79.42$ 69.49$

9.74% 182.45$ 157.44$ 136.64$ 119.08$ 104.07$ 91.09$ 79.77$ 69.82$

10.24% 183.03$ 157.96$ 137.11$ 119.50$ 104.45$ 91.44$ 80.09$ 70.11$

10.74% 183.56$ 158.43$ 137.53$ 119.88$ 104.79$ 91.75$ 80.38$ 70.37$

11.24% 184.04$ 158.85$ 137.91$ 120.22$ 105.10$ 92.04$ 80.64$ 70.61$

11.74% 184.48$ 159.24$ 138.26$ 120.54$ 105.39$ 92.30$ 80.88$ 70.83$

12.24% 184.88$ 159.60$ 138.58$ 120.83$ 105.65$ 92.54$ 81.10$ 71.03$

12.74% 185.25$ 159.93$ 138.87$ 121.10$ 105.90$ 92.76$ 81.30$ 71.22$

13.24% 185.60$ 160.24$ 139.15$ 121.34$ 106.12$ 92.96$ 81.49$ 71.39$

13.74% 185.91$ 160.52$ 139.40$ 121.57$ 106.33$ 93.15$ 81.66$ 71.55$

CV ROIC

Beta

120.29 0.668 0.768 0.868 0.968 1.068 1.168 1.268 1.368 1.468

3.42% 224.48 208.11 193.40 180.10 168.01 156.98 146.87 137.57 128.98

3.82% 211.54 194.83 179.90 166.49 154.38 143.37 133.34 124.14 115.69

4.22% 199.65 182.70 167.66 154.22 142.14 131.22 121.29 112.24 103.94

4.62% 188.68 171.58 156.50 143.09 131.09 120.29 110.51 101.61 93.48

5.02% 178.52 161.35 146.28 132.95 121.06 110.40 100.78 92.05 84.10

5.42% 169.09 151.90 136.89 123.66 111.92 101.42 91.97 83.42 75.64

5.82% 160.32 143.15 128.23 115.14 103.55 93.21 83.94 75.57 67.98

6.22% 152.13 135.03 120.22 107.28 95.85 85.70 76.60 68.41 60.99

Market Risk Premium

CV growth of EPS

120.29 ‐1.50% ‐1% ‐0.50% 0% 0.50% 1% 1.50% 2% 2.50%

3% 120.10 124.15 128.79 134.16 140.42 147.84 156.77 167.71 181.43

4% 114.96 118.62 122.79 127.58 133.17 139.74 147.59 157.13 168.98

5% 110.15 113.45 117.20 121.50 126.47 132.30 139.23 147.58 157.87

6% 105.63 108.61 111.99 115.84 120.29 125.47 131.59 138.92 147.88

7% 101.38 104.07 107.11 110.57 114.54 119.15 124.57 131.02 138.84

8% 97.37 99.80 102.53 105.63 109.19 113.29 118.10 123.78 130.63

9% 93.57 95.76 98.22 101.01 104.19 107.85 112.11 117.13 123.13

Cost of Debt

Risk Free Rate

120.29 2.50% 2.60% 2.70% 2.80% 2.90% 3.00% 3.10% 3.20% 3.30%

3.42% 169.98 166.60 163.31 160.10 156.98 153.93 150.96 148.06 145.24

3.82% 154.92 151.93 149.01 146.16 143.37 140.66 138.01 135.42 132.89

4.22% 141.54 138.87 136.26 133.71 131.22 128.78 126.40 124.07 121.79

4.62% 129.57 127.17 124.83 122.53 120.29 118.09 115.93 113.83 111.76

5.02% 118.80 116.64 114.51 112.44 110.40 108.41 106.45 104.54 102.66

5.42% 109.06 107.09 105.16 103.27 101.42 99.60 97.82 96.07 94.35

5.82% 100.19 98.40 96.64 94.91 93.21 91.55 89.92 88.31 86.74

6.22% 92.09 90.45 88.84 87.25 85.70 84.17 82.66 81.19 79.74

Market risk Premium

10. 10

Important Disclaimer

This report was created by students enrolled in the

Security Analysis (6F:112) class at the University of

Iowa. The report was originally created to offer an

internal investment recommendation for the University

of Iowa Krause Fund and its advisory board. The report

also provides potential employers and other interested

parties an example of the students’ skills, knowledge and

abilities. Members of the Krause Fund are not registered

investment advisors, brokers or officially licensed

financial professionals. The investment advice contained

in this report does not represent an offer or solicitation

to buy or sell any of the securities mentioned. Unless

otherwise noted, facts and figures included in this report

are from publicly available sources. This report is not a

complete compilation of data, and its accuracy is not

guaranteed. From time to time, the University of Iowa,

its faculty, staff, students, or the Krause Fund may hold

a financial interest in the companies mentioned in this

report.

20. Weighted Average Cost of Capital (WACC) Estimation

Tesoro Corporation

Market Value of Debt 5,496

LT debt 4,254

ST debt 0

PV of Operating Leases 1242

Pretax cost of Debt 6.00%

Marginal Tax Rate 35%

After‐Tax Cost of Debt 3.90%

Average Weight of Debt 28.84%

Market Value of Equity 13,559

Risk Free Rate 2.90%

Market Premium 4.62%

Beta 1.168

Cost of Equity 8.30%

Average weight of Equity 71.16%

Market Value of Preferred Stock 0

Value of Capital(D+E+PFD) 19,055

WACC 7.03%