1. Important disclosures appear on the last page of this report.

1

Analysts

Michael Faraone

michael-faraone@uiowa.edu

Jeff Pomykala

jeffrey-pomykala@uiowa.edu

Brock Gilbert

brock-gilbert@uiowa.edu

Company Overview

Continental Resources is an independent crude oil and natural

gas exploration and production company headquartered in

Oklahoma City, Oklahoma. Continental’s strategy has been

focused on crude oil since the 1980’s, and it is on track to triple

its proved reserves by 2017. Continental is currently a top ten

petroleum producer and operates in the North, South, and East

regions of the United States. Its two highest producing leaseholds

are the Bakken for crude oil and the Anadarko Woodford for

natural gas. At year-end 2011, Continental Resources reported

revenues of $1.6 billion.

Stock Performance Highlights

52 week High $97.19

52 week Low $57.02

Beta Value 1.65

Average Daily Volume 1.05 m

Share Highlights yellow is yahoo

Market Capitalization $13.11 b

Shares Outstanding 179.80 m

Book Value per share $15.53

EPS (ttm) $4.45

P/E Ratio (ttm) 16.39

Dividend Yield N/A

Dividend Payout Ratio N/A

Company Performance Highlights

ROA 13.83%

ROE 33.64%

Sales 2.05 b

Financial Ratios

Current Ratio 0.86

Debt to Equity 29.36

Current Price: $69.48

Target Price Range: $90-96

An Expansion of Continental Proportion

Realizing Growth Potential: Continental has increased its

leasehold’s in the nation’s premiere oil plays by 51% in the

Bakken play and 113% in the Anadarko Woodford play since

2009.

Continuing to Explore: Through increasing their capital

expenditure’s budget to $3.4B for 2013, CLR continues to see

growth potential in their current and new oil play leaseholds.

Realizing Growth Potential: CLR is a leader in horizontal

drilling and other leading drilling technology; this in turn has

reduced cycle time by 25% to 50% and has increased overall rig

efficiency.

Production Growth: We project that Continental will grow

production from 36 MMBoe per year in 2012 to 95+ MMBoe per

year in 2020.

The Next Super-Independent: Through their focus on

high-margin projects and maintaining capital discipline,

becoming the next super-independent oil producer is more than

just a pipe dream.

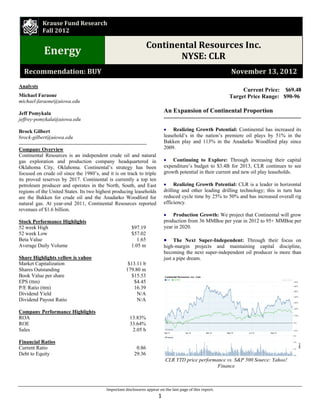

CLR YTD price performance vs. S&P 500 Source: Yahoo!

Finance

Krause Fund Research

Fall 2012

Energy

Continental Resources Inc.

NYSE: CLR

Recommendation: BUY November 13, 2012

2. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

2

Through company and industry-specific research, as well

as valuation models, we calculated the intrinsic value of

CLR common stock as $93.44, concluding that the market

price is undervalued. After our research, we placed a buy

rating on this stock. The following analysis and models

contained in this report explain our investment

recommendation

Key Economic Variables

Real GDP

The United States real GDP was 2% annualized growth for

the third quarter of 2012. The real GDP increased from the

second quarter, which was revised down to 1.3%, but still

fell short of the 2011 year end real GDP of 3%. The

increase between Q2 and Q3 was caused in large part by

the increase in personal consumption. The personal

consumption increase was led by purchases of durable

goods, indicating that consumers are more optimistic to

make these larger purchases, a positive sign for further

economic improvement looking forward. The energy

sector is a key driver of GDP with energy as an input for

all goods produced. We expect that the real GDP will

remain at 2% over the upcoming 6 month period and

slowly increase back to the average 3% within 3 years. Oil

& Gas Exploration and Production is expected to average

annual growth of 6.9%, compared to GDP growth forecasts

of 2.6% through 20151

.

Historical GDP Growth. Source: Trading Economics

Interest Rates

Ben Bernanke recently announced implementation of QE3,

the difference of this round compared to other attempts is

that it is open-ended. Interest rates will remain depressed at

a range of 0 – 0.25% through 2015; a year longer than first

proposed, at a range of 0 - 0.25%. The depressed FFR will

likely keep market interest rates low. This is beneficial for

companies within the energy sector as it is a capital

intensive industry. With an enhanced ability to borrow at

lower costs, we expect many companies in the energy

sector to continue increasing their capital expenditure

programs. Low rates will also allow companies to

refinance current debt at lower costs, in-line with increased

capital expenditure programs. Mid-year mergers and

acquisitions were at 231 compared to 256 at the same time

period in 20112

. With the rates depressed, we expect that

M&A will still play a major role, but their impact will

continue to slow as interest rates in future years begin to

rise.

Historical Interest Rates. Source: Yahoo! Finance

U.S. Dollar Index

As indicated by the graph below, the U.S. dollar index has

an inverse relationship with oil prices, as do all

commodities. For oil being traded in U.S. dollars, this is

not an ideal situation. Other countries are able to purchase

more oil with a weakened dollar, increasing demand, and

therefore, price. Since the U.S. dollar index is positively

correlated with interest rates and the QE3 will keep interest

rates low through 2015, we should see the U.S. dollar

index remain stable in the short term; assuming no

European Union Collapse. The U.S. dollar index is

dependent on the outcome of the Eurozone crisis.

Depending on what becomes of the Eurozone crisis, there

may be an impact on the U.S. dollar index. The European

Central Bank’s recent bailout offers an unlimited amount

of bond buying in those countries still struggling to repay

debt. Spain and Greece remain threats, especially since

Spain has refused bailout help and continues to increase

debt. Another area of concern is the banks that suffered

losses from defaults and have decreased lending, further

hurting the European Economy. The bond buying program

has bought Europe roughly a year to solve their issues3

.

Investment Thesis

Economic Outlook

3. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

3

U.S.Dollar Index vs. Crude Oil Price. Source: Y-Charts

Unemployment Rate

The unemployment rate came in at 7.9% for the month of

October, a .1% increase over September’s figure. There

were also 171,000 jobs added to the economy in October.

The increase was caused in part by an increase in the labor

pool, with over 500,000 workers re-entering the job search

market4

. Though the numbers show improvement, they

remain high with below average growths in GDP. The

impending fiscal cliff plays a large role in determining

expectations for what unemployment will be in the short-

term. The Congressional Budget office warns that

unemployment could reach as high as 9.1% in 2013 if a

solution is not reached5

. We feel that a solution will be

achieved and that unemployment will stay right around the

8% mark for the next six months as the economy improves

slowly but surely. In the long term (2-3 years), we expect

unemployment to decrease to just below 7%. We expect

the energy sector to see benefits from the economic growth

predicted.

Historical Unemployment Rate. Source: Trading Economics

Consumer Confidence Index

The consumer confidence index forecasts how confident

consumers are with the economy and their current financial

situation. It is also an important measure of consumers’

trust in the future state of the economy. Consumer

sentiment measured 84.9 in November 2012; a 5-year high.

This marked the fourth month in a row that consumers

showed increasing confidence in the economy. After the

release of this data, oil futures increased 1.2%. The

increase in confidence means consumers are willing to

spend more money and an increase in spending stimulates

demand and spurs economic growth. This is unexpected as

we come ever closer to the fiscal cliff that will increase

taxes and decrease government spending. It seems that

consumers are confident that the government will find a

solution to avoid this fiscal cliff; at least for the time being.

We expect that consumer confidence will stay at these high

levels, further improving the economy in the short term. If

the fiscal cliff is avoided, we expect to see consumer

confidence levels reach close to 89, the average prior to

entering the recession6

. We also expect the economic

growth to increase demand amongst firms in the energy

sector.

Consumer Sentiment Index. Source: Advisor Perspectives

Over the past 5 years, the performance of this industry has

seen a lot of volatility. Through the year 2017, industry

revenue is expected to grow by 2.6% annually7

. However,

not every year is going to yield growth due to a variety of

factors such as volatile natural gas and crude oil prices.

Due to low natural gas prices, many companies are shifting

away from natural gas exploration to drill for oil. This is

because there is an over abundant supply with low demand,

which has led to depressed prices.

Oil & Gas Exploration and Production

Companies in the Oil & Gas Exploration & Production

industry explore, develop, and work in offshore or onshore

oil and natural gas fields. The companies in this industry

focus on production of crude petroleum, mining and

extracting oil, producing natural gas, recovering sulfur

from natural gas, and recovering hydrocarbon liquids. The

Industry Analysis

Crude Oil Price

U.S. Dollar Index

4. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

4

oil is mined and extracted from oil shale and oil sands.

Primary activities and services in the oil & gas exploration

and production industry include crude oil extraction,

liquefied natural gas production (LNG), liquefied

petroleum production (LNP), natural gas extraction, oil and

gas extraction, and oil shale extraction7

.

Recent Developments and Trends

We currently have a positive outlook on the E&P industry

in the long term. Recently, we have seen a move towards

unconventional methods of extracting oil and natural gas

liquids. There is a high concentration of these liquids

located in Oklahoma, Montana, and North Dakota.

Currently, companies are competing for acreage along

these basins since there is high growth potential for E&P

participants. These new onshore discoveries have made the

U.S. one of the most active areas in the world7

.

CLR Areas of Operations. Source: Contres

The map above displays the more active oil plays within

the country. The highlighted areas are CLR’s areas of

leaseholds and operation. The oil fields located in Montana

and North Dakota are known as the Bakken and Three

Forks reservoirs. The Bakken is the largest oil

accumulation in the U.S. and is approximately 14,700

square miles. These two reservoirs are estimated to hold

approximately 24 billion barrels of crude oil equivalent. If

this estimation is correct, it would double the U.S. oil

reserves. Continental is currently the largest acreage holder

in the Bakken play, with 946,248 net acres. The other

highlighted oil field located in Montana, North Dakota and

South Dakota is known as the Red River Units play. It is

the 7th

largest onshore field in the lower 48 states, ranked

by proved reserves. The Niobrara formation, located in

Wyoming and Colorado, is an emerging oil play.

Continental currently holds 25,000 net acres in this region.

In Oklahoma, we see the Anadarko Woodford and Arkoma

Woodford plays, where competition for acreage has been

rapidly increasing due to previous drilling success in the

Anadarko play. The Arkoma Woodford play is a natural

gas producing reservoir, here Continental has completed

640-acres of exploratory and 80-acres of infield

development wells8

. At year-end 2011, production for

Continental was approximately 73% oil and 27% natural

gas9

. We expect that this mix will hold fairly constant over

the next few years.

CLR Product Mix. Source: Contres

Oil and gas prices have seen added volatility due to

numerous reasons. Continued turmoil in the Middle East

has added to the rise in oil prices, as well as, production

concerns in the North Sea. As domestic production

continues to increase, we project the price of crude oil to

increase by 4.5% through 20202

.

Markets and Competition

Companies involved in the E&P industry have a large

number of competitors. They compete against large

integrated energy companies like Chevron, Conoco

Phillips, and Exxon, as well as, smaller companies that

specialize specifically in the E&P industry of the energy

sector. In 2011, the Energy Information Administration

estimated that global oil demand rose by 1 MMBbl/day. As

of August 2012, we saw growth of 0.76 MMBbl/day, with

projected growth of 0.87 MMBbl/day in 2013. The U.S.

onshore production will become critical over the next

decade due to the new OPEC capacity of 35.03 million

barrels per day. This new capacity is 85% lower than

originally estimated by the IEA3

.

Supply vs. Demand Analysis

Estimates of world supply vary by source, but the

consensus is that the world oil supply is enough to last a

few more decades with current usage patterns3

. The

emerging economies of China and India are putting added

strain on the supply through increased energy demands. As

the supply continues to deplete, the long term price of oil

will begin to rise to reflect increased demand. To meet the

5. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

5

increasing energy demand, companies will need to shift

their focus to alternative energy sources.

E&PMarket Segmentation. Source: IBISWorld

The industries that consume the oil and gas produced by

the E&P industry can be seen in the pie chart above. As the

chart illustrates, the petroleum refining industry is the

largest purchaser of crude oil and is a critical component to

the success of the industry.

In the recent IEA Word Energy Outlook publication, it is

stated that the world energy flows will shift in the long

term. The United States will become a net exporter of oil

by 2035 and will almost be self-sufficient in energy. We

expect the U.S. to also become a net exporter of natural gas

by 2020; this will be driven by the construction of natural

gas exporting facilities10

.

The potential for the U.S. to become energy self-sufficient

is positive for Continental. Its current positioning will

allow it to capitalize on this opportunity by increasing its

production potential. By continuing to increase its

leasehold’s and proved reserves, it will be able to increase

production to better meet demand. The current growth

strategy being implemented gives Continental a long-term

advantage to profit from increasing domestic energy

demands.

Price Analysis

The key economic drivers of the E&P industry are the

world prices of crude oil and natural gas. Currently, there is

an abundant supply of natural gas in the U.S. Therefore,

the price of natural gas has become very depressed.

Without an increase in demand, we expect the price levels

to remain low. On April 16, 2012, The Federal Energy

Regulatory Commission (FERC) approved the construction

of the first LNG exporting facility, to be constructed by

Cheniere Energy, Inc. The price of natural gas could

benefit from the approval of this facility, especially with

high natural gas demand in China. However, construction

on the first facility is scheduled to start in 201511

.

Consequently, there will be no short-term benefit reflected

in the gas price. Since Continental focuses a large portion

of its operations on crude oil, this would not have a big

impact on the company. The relationship between

Continental and the WTI crude oil spot price can be seen

on the graph below.

CLR vs. WTI Oil Spot Price. Source: Y-Charts

As the figure above illustrates, Continental’s stock price

performance has a high correlation with the WTI crude oil

spot price. Over the past five years, we have witnessed a

large increase in the price of oil, as seen above. Many

factors have contributed to this increase such as continued

tension in the Middle East, difficulty of extraction,

increased demand, etc. The main factor tempering the price

of oil is increased competition from alternative energy

sources, most notably, natural gas. Although alternative

sources of energy continue to be developed, crude oil is a

commodity in high demand with healthy margins. Looking

forward through 2020, we predict that the price of oil will

increase at an average rate of 4.5%. This is due to

increasing demand from emerging economies, supply

depletion, unpredictable OPEC activity, and increased

regulation3

.

Company Overview

Continental Resources is an independent oil and gas

exploration and production company headquartered in

Oklahoma City, Oklahoma. Continental is currently a top

ten petroleum liquid producer in the U.S. and has focused

their growth strategy on crude oil since the 1980’s. In

2011, the company reported $1.6 Billion in total revenues

and is currently on track to triple reserves by 201712

. They

Continental Resources Analysis

6. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

6

operate in the United States with inland properties located

in the North, South, and East regions. The north region

includes property in the North Dakota and Montana

Bakken, Red River units, and Niobrara in Colorado and

Wyoming. Kansas and all properties south of Kansas and

west of the Mississippi including Anadarko Woodford and

Arkoma Woodford in Oklahoma comprise the south

region. The Illinois Basin and the state of Michigan make

up the east region. At year-end 2011, production averaged

61,865 barrels of oil equivalent per day8

.

Products and Markets

The Oil & Gas Exploration and Production industry has

two main products; crude oil and natural gas. Based on

estimates, crude oil is projected to account for 58.4% of the

industry revenue with natural gas at 41.6% in 2012.

Revenue Breakdown for E&P Industry. Source: IBISWorld

A majority of the crude oil produced by Continental is sold

to end users in major market centers. Select midstream

marketing companies or crude oil refining companies in the

lease are also sold to in lower volume. A majority of oil

produced is transported by rail or truck, and then delivered

to the most efficient point on a pipeline system. It is then

delivered to a point of sale downstream on another

connected pipeline. For the years 2011, 2010, and 2009,

Marathon Oil Company was the largest purchaser of

Continental’s crude oil at 41%, 57%, and 56%,

respectively. All other purchasers accounted for less than

10% of sales9

.

Production and Distribution

CLR employs multiple drilling methods to extract oil and

natural gas. These methods include Hydraulic Fracturing,

Horizontal Drilling, and Eco-Pad® drilling8

. Eco-Pad® is

the most efficient way to extract oil and gas from the earth,

as well as the most environmentally friendly.

Eco-Pad® refers to the process by which Continental

simultaneously drills 4 different wells on a single drilling

pad, which benefits the company and the environment. It

also cuts down on the transportation of drilling equipment

because the same machine does not need to be broken

down and reconstructed at 4 different sites. Continental

sees a fiscal benefit from the efficiency of the process. It is

estimated that each Eco-Pad® carries a cost savings of

roughly 10% per well, which is approximately $2.5 million

dollars for 4 wells (one Eco-Pad®). The speed at which

each well is drilled is reduced by 2-3 days, which

contributes to the cost savings as well. Currently,

Continental employs this method in the Bakken play in the

North region of the country. They have increased their

leasehold’s in the Bakken region by 51% and have

increased their leasehold in Anadarko Woodford by 113%

since year-end 2009. As they further improve this

technology, they will employ it in the other regions where

they hold leases8

.

CLR Leasehold Increases Since YE2009. Source: Contres

In 2011, the net production of natural gas and crude oil was

36,671 MMcf and 16,469 MBbls, respectively. Average

sales price for crude was $88.51/Bbl and $5.24/Mcf for

natural gas on a total company level. The production cost

on a total company level was $6.13/Boe9

. Hedging activity

consisted of approximately 27% of total production. We

can expect Continental to continue hedging between 20% -

30% of total production in the future. We project

production costs to rise through 2020, due to added

difficulty of reaching the underground resources and added

competition for labor and well equipment. Continental puts

more emphasis on the production of crude oil because it

has better margins and is more profitable overall for the

company. At year-end 2011, production was 73% crude oil

and 27% natural gas9

. We project the product mix to be

roughly 75% crude oil and 25% natural gas through 2020.

7. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

7

Competition

The E&P industry is a highly competitive environment.

Direct competitors of CLR vary by which region they are

producing in. The most competitive segment of the E&P

industry is locating a feasible oil field to begin drilling.

Some of CLR’s competitors have more cash on hand,

which allows them to pay higher prices for viable land and

acquire more acreage along oil rich deposits. There is also

substantial competition in acquiring capital to purchase

these plots of land along with high rig costs associated with

extracting oil and gas. The high cost associated with

extracting oil makes the E&P industry highly capital

intensive. This leads many companies to finance ventures

through high levels of debt. This also causes volatile

earnings due to higher fixed costs and interest expenses.

The table below compares CLR to 6 of its competitors

based on market capitalization.

CLR vs. Competitors by Market Cap. Source: Yahoo! Finance

One thing to note is that Continental puts a larger focus on

oil production than its competitors. This better positions

them in the industry moving forward due to the more

attractive profit margins associated with oil. Also, limiting

exposure to natural gas is going to be beneficial in the

short-term due to a depressed natural gas market. As there

is a push towards alternative sources of energy, the product

mix of Continental may shift towards a focus on natural

gas, however, that shift would happen past our forecast

horizon. From the table, we can also see that CLR has

lower cash on hand than some of its competitors.

Therefore, funding for future expansion will require debt

which they fund through their revolving credit facility and

bond issues. They currently have 2.943 billion of long term

debt on their books with a weighted average interest rate of

roughly 6.8%9

.

Some direct competitors to Continental based on market

capitalization include: Noble Energy, Inc. (NBL), Pioneer

Natural Resources Co. (PXD), Southwestern Energy

(SWN), Chesapeake Energy Corporation (CHK), Range

Resources Corporation (RRC), and Linn Energy, LLC

(LINE) 13

. The chart below compares the year to date stock

price performances of Continental, four of its competitors,

and the S&P 500.

CLR Performance vs. Competitors. Source: Yahoo! Finance

Growth Potential

A recent discovery of oil shale in Oklahoma may add as

much as 1.8 billion barrels of oil equivalent to the

company’s proven reserves. This play is known as SCOOP,

or the South Central Oklahoma Oil Province. Continental

currently holds 170,600 acres of leaseholds on this play

and has been continuously adding to this figure.

Continental has also dedicated $136 million of their capital

expenditure budget to exploring two other, non-disclosed

oil plays in 2013. Current plans are to drill as many as 300

new wells in 201314

. The current expansion of Continental

demonstrates strong growth potential through the

acquisition and exploration of new leasehold’s on oil rich

land. This expansion of leasehold’s will allow for future

drilling and production to increase. With a projected

growth in the price of oil over the long term, acquiring oil

rich land now at fair market value will prove to be an

advantage in the long term.

Regulation

The E&P industry is a heavily regulated industry;

regulations are put into place by the federal, state, and local

governments. Regulation comes in many forms, like

regulation of sales and transportation of crude oil and

natural gas liquids, production, derivative trading

regulation (Dodd-Frank Act), Energy Policy Act of 2005,

Company

Market

Cap (B) Oil

Natural

Gas

Natural

Gas

Liquids

Proven

Reserves 2012

Cash on

Hand

(million)

Noble Energy, Inc. (NBL) 16.91 29.9% 63.1% 7.0% 1,209.0 MMBoe 1455

Continental Resources, Inc. (CLR) 12.85 73.0% 27.0% 0.0% 508.4MMBoe 54

Pioneer Natural Resources Co. (PXD) 12.80 33.7% 47.6% 18.7% 1062.9 MMBoe 537

Southwestern Energy Co. (SWN) 11.95 1.0% 99.0% 0.0% 5.9 tcfe 16

Chesapeake Energy Corporation (CHK) 10.97 1.4% 45.0% 53.6% 18.8 tcfe 351

Range Resources Corporation (RRC) 10.55 6.2% 76.8% 17.0% 5.1 tcfe 0

Linn Energy, LLC (LINE) 7.80 35.0% 47.4% 17.6% 3.4 tcfe 1

Catalysts for Growth/Change

8. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

8

and environmental, health, and safety regulation. These

regulation laws are frequently amended and can be

interpreted in various ways, making compliance with all

regulation difficult. There are also hefty fines associated

with not complying with all regulation, which can

adversely affect the bottom line. Some regulation

infractions carry penalties of up to $1,000,000 per day until

the company can comply with the law9

. In the long term,

we expect regulation to continue to be more thorough.

Climate changes associated with global warming and CO2

content in the atmosphere has led to concern with the

sustainability of fossil fuels and their negative impact on

the environment. However, we do not expect drastic policy

changes until 2025 or later.

Prices

Continental’s profitability relies heavily on the overall

economy, as well as, the market price for crude oil and

natural gas. Since these prices are determined by the

market and have historically been volatile, cash flows and

overall revenue are also subject to this volatility. However,

Continental participates in the derivatives market in order

to hedge their business. This also brings added risk if the

market trends in an unexpected direction. The large

influencers of the prices of crude oil are macro-economic

conditions, the actions of OPEC, weather conditions, and

the political conditions surrounding the industry9

.

Land and Rig Costs

In 2011, Continental invested $2.2 billion in their capital

program and budgeted $1.75 billion for 2012 with a

projected budget of $3.4 billion for 2013. Financing for

these expenditures comes from cash generated from

operations, issuance of debt and equity securities, and

borrowing under a revolving credit facility. These capital

expenditures are subject to the prices of the market; if the

commodity price drops, capital expenditures will decrease,

and vice versa. Access to capital is also subject to changes

in proved reserves, volume of production in current wells,

and the ability to secure credit. The use of a revolving

credit facility is advantageous to Continental. The terms

surrounding the agreement give CLR a borrowing base of

up to $2.25 billion at a rate equal to LIBOR for the term of

the loan, plus 175 to 275 basis points9

.

As of year-end 2011, Continental reported proved reserves

of 508,438 Mboe, the PV-10 value of these proved reserves

is $9.2 billion. Net developed acres were 665,317 and net

undeveloped acres were 1,229,266. As Continental

continues to discover new oil plays, as well as acquiring

new leasehold’s, we can expect these figures to grow. With

the recent discovery of the potential of the SCOOP play,

CLR may be able to increase proved reserves by as much

as 1.8 billion barrels of oil equivalent8

.

Investment Overview

Positives

Continental is a top ten petroleum liquid producer in the

United States and the largest leaseholder in the Bakken oil

play of North Dakota and Montana, as well as a leading

presence in the Anadarko Woodford play in Oklahoma,

and the Red River Units play in North Dakota, South

Dakota and Montana. They have also acquired leasehold’s

in the SCOOP play recently8

.

Current Proved Reserve Holdings. Source: Contres

The above chart shows Continental’s proved reserves as of

December 31, 2011 by location. The makeup of these

reserves consists of 64% oil and 36% natural gas8

. Having

these reserves is a positive for the company because they

have the ability to produce from these reserves with

guaranteed sales after producing the crude oil. Year-end

proved reserves totaled roughly 508 million barrels of oil

equivalent and are projected to triple by 2017 at current

growth estimates.

Growth in Proved Reserves. Source: Contres

The above chart illustrates the growth in proved reserves in

CLR’s possession since 2006. We can expect the growth to

continue as new oil patch discoveries are made and as CLR

acquires more acreage on current oil fields. The growth in

9. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

9

proved reserves can be credited to the continued

acquisition of leasehold’s on current and new oil field

plays.

Growth in Oil and Natural Gas Production. Source: Contres

The above graph illustrates the growth in production of oil

and natural gas from 2006. We can expect production to

continue to grow as they continue to produce from their

growing proved reserves. Production growth in the Bakken

leaseholds has increased from 0.8 MMBoe in the first

quarter of 2008 to 4.9 MMBoe in the second quarter of

2012. This growth resulted in a 51% CAGR for the region

with production expected to continue to grow12

.

Investment Negatives

A substantial decrease in the price of oil over an extended

period of time would negatively impact margins and the

bottom line. The profitability of the E&P business is

heavily weighted on current market prices for crude oil and

natural gas. If we were to see an extended decline in

commodity prices, Continental would not be able to

finance further E&P activity and would fail to meet its

current financial commitments.

76% of total production was completed in the north region

of their properties. This makes them vulnerable to risks

associated with this region like pipeline constraints,

pricing, available rigs/equipment, labor, capacity, and

severe seasonal weather9

. However, the company continues

to diversify their leasehold locations as new oil discoveries

are made in the United States.

The act of extracting oil is a dangerous, high-risk activity.

Many uncertainties are associated with drilling and

extraction: irregularities in geological formations,

equipment failure/shortages, environmental hazards,

spillage or mishandling of oil, and shortages of qualified

personnel9

. As competition continues to increase,

competition for rig equipment and operators will continue

to grow. This increased demand for equipment and skilled

labor will drive up production costs in the long term and

could have a negative impact on margins.

Overview

When valuing Continental Resources we employed four

different valuation models: Discounted Cash Flow (DCF),

Economic Profit (EP), Dividend Discount Model (DDM),

and Relative Valuation. Based on the results from these

models, we projected a price target range of $90-$96.

Continental Energy currently trades for $69.48.

Recommendation

We concluded our research and analysis by placing a buy

rating on CLR common stock. Although crude oil and

natural gas prices have been volatile in recent years, we

expect oil prices to steadily rise in the future. Continental

will continue to increase production, and with oil prices

rising, will remain a highly profitable company.

Revenue Decomposition

We forecasted revenue based on a variety of different

factors. First, we applied a growth rate of 4.5% to crude oil

prices. This growth rate was obtained through industry

estimates and macro-economic outlook. When estimating

production volume, we took a more conservative approach

than management’s guidance. We estimated that CLR will

reach 95,983 MBoe in production by 2020. When

calculating sales volumes, we estimated that they would

sell 99% of total production for 2012 and 2013. As

production continues to increase in 2014 and 2015, we

expect them to sell 95% of total production. From 2016

and forward, we expect them to sell 90% of total

production.

Expenses

For production expenses and production taxes, we used a

base of $6.00 and $6.70 in 2012, respectively. We then

grew them by an average of 10% to reflect increased

expenses in future years. For depreciation, depletion,

amortization, and accretion, we looked historically and

found an average of 8% of beginning book value of

property, plant, and equipment. For forecasting purposes,

most other expenses were held at a constant percentage of

sales revenue.

Valuation Analysis

10. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

10

WACC Estimation

To calculate our WACC, we used the CAPM model to

reach our cost of equity. With the growth rate of the

economy staying low, we used the 30-year Treasury Bond

yield of 2.92% as our risk-free rate. For our equity risk

premium, we used Damodaran’s implied risk premium of

5.92%. We then found the raw beta using an average from

the Bloomberg terminal, which came out as 1.65. Using the

CAPM formula, we found our cost of equity to be 12.69%.

Using FINRA and the 30 year treasury yield, we found cost

of debt to be 8.25%. We then found the after-tax cost of

debt to be 5.12% using a 38% marginal tax rate. Finally,

we calculated WACC to be 10.97% after calculating the

market weights of debt and equity.

DCF and EP Valuation

We used the DCF and EP models to reach a target price of

$93.44 as of November 13, 2012. In the DCF model, we

used our WACC estimation to discount future cash flows.

For the EP model, we calculated economic profit by

subtracting the WACC multiplied by the beginning

invested capital from NOPLAT. When calculating the

continuing value for these models, we applied a CV growth

rate of 3.50% to account for inflation. After obtaining the

value of operating assets from these models, we added

back non-operating assets and subtracted the value of debt

and other claims to arrive at the value of equity.

Dividend Discount Model

Using the dividend discount model, we calculated an

intrinsic value of $42.80. However, we do not believe this

model accurately predicts the value of CLR stock. This low

intrinsic value is mainly due to our expectations that CLR

will not pay any dividends within the model’s forecast

period. Therefore, we chose to disregard this model when

making our final investment recommendation.

Relative Valuation

To compute the value of CLR stock using relative

valuation, we found peer competitors in the same industry

based on market capitalization. We then removed any

outliers from the group after calculating P/E. When

compared to these peers, the model yielded a valuation of

$83.01 for 2012 and $103.23 for 2013.

We used a variety of variables that we felt were important

to the target price when constructing our sensitivity

analysis. These tests allowed us to see how small changes

in key variables affect the target price of CLR stock. We

concluded that our target price has a valid range after

running the sensitivity analysis.

CV Growth vs. WACC

Our first test was the CV growth rate against the WACC.

The CV growth rate is an important factor in our model

because it causes our value of equity to change, which

affects the DCF target price. Since WACC is also

incorporated into the DCF target price, we were interested

in seeing how changes in both of the variables would affect

the outcome of CLR stock price.

MRP vs. Risk-Free Rate

We then tested our risk premium against our risk-free rate.

Since both of these variables are incorporated into

calculating the cost of equity, which is used to calculate

DDM price, we felt it was an important test to run.

CV Growth vs. Beta

We also tested CV growth against beta, since both of these

variables are included in calculating the DCF target price.

This analysis had a much smaller effect on the target price

than testing CV growth against WACC.

MRP vs. Beta

We tested market risk premium against beta to see how

changes in cost of equity would affect the target price. As

expected, small changes in either variable caused drastic

changes to the target price of CLR.

Important Disclaimer

This report was created by students enrolled in the Security

Analysis (6F:112) class at the University of Iowa. The

report was originally created to offer an internal investment

recommendation for the University of Iowa Krause Fund

and its advisory board. The report also provides potential

employers and other interested parties an example of the

students’ skills, knowledge and abilities. Members of the

Krause Fund are not registered investment advisors,

brokers or officially licensed financial professionals. The

investment advice contained in this report does not

Sensitivity Analysis

11. The University of Iowa

Krause Fund Research Henry B. Tippie College of Business

Important disclosures appear on the last page of this report.

11

represent an offer or solicitation to buy or sell any of the

securities mentioned. Unless otherwise noted, facts and

figures included in this report are from publicly available

sources. This report is not a complete compilation of data,

and its accuracy is not guaranteed. From time to time, the

University of Iowa, its faculty, staff, students, or the

Krause Fund may hold a financial interest in the companies

mentioned in this report.

References:

1

Bloomberg Economic Calendar

http://www.bloomberg.com/markets/economic-calendar/

2

Deloitte Oil & Gas Pricing Outlook

http://www.deloitte.com/assets/Dcom-

UnitedStates/Local%20Assets/Documents/Energy_us_er/u

s_er_MAReport_Midyear2012_0812.PDF

3

Europe Turn Corner

http://www.oregonlive.com/newsflash/index.ssf/story/after

-3-bumpy-years-europe-turns-

corner/4a468ac330664326a44f36de609236b4

4

U.S. Unemployment Rate Rises

http://articles.nydailynews.com/2012-11-

02/news/34881947_1_unemployment-rate-jobs-report-

jobless-rate

5

Fiscal Cliff Effect on Unemployment

http://www.examiner.com/article/cbo-warns-

unemployment-will-rise-to-9-1-if-deal-on-fiscal-cliff-is-

not-reached-1

6

Oil Rises as Consumer Sentiment Gains

http://www.businessweek.com/news/2012-11-09/oil-is-

steady-as-politicians-squabble-while-gasoline

7

Oil & Gas Exploration and Production Report

http://clients1.ibisworld.com/reports/us/industry/default.as

px?entid=103

8

Continental Resources Investor Information

http://www.clr.com/operations

9

Continental Resources 10-K

http://sec.gov/Archives/edgar/data/732834/0001193125120

77054/d267719d10k.htm#toc267719_10

10

World Energy Outlook, International Energy Agency

http://www.iea.org/newsroomandevents/pressreleases/2012

/november/name,33015,en.html

11

NetAdvantage Natural Gas Report

http://www.netadvantage.standardandpoors.com/NASApp/

NetAdvantage/showIndustrySurvey.do?code=ngd

12

CLR Energy Conference Presentation

http://phx.corporateir.net/phoenix.zhtml?c=197380&p=irol

-calendar

13

Industry Analysis, Yahoo Finance

http://biz.yahoo.com/p/121conameu.html

14

SCOOP Oil Discovery

http://www.tulsaworld.com/business/article.aspx?subjectid

=49&articleid=20121010_49_E1_CUTLIN621608

12. Continental Resources Inc.

Key Assumptions of Valuation Model

Ticker Symbol CLR

Current Share Price 69.48

Fiscal Year End Dec. 31

Pre‐Tax Cost of Debt 8.25%

Cost of Equity 12.69%

Beta 1.65

Risk‐Free Rate 2.92%

Equity Risk‐Premium 5.92%

CV Growth 3.50%

CV ROIC 22.51%

WACC 10.97%

Normal Cash(% of Revenue) 4.00%

Marginal Tax Rate 38.00%

For Fiscal Years Ending Dec. 31 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E(CV)

Production:

Oil (MBbl) 24,500.4 35,438.1 42,525.7 51,030.8 58,685.4 63,086.8 66,241.2 69,553.2 71,987.6

Natural Gas (MMcf) 62,371.0 70,167.4 80,798.8 96,958.5 105,633.8 113,556.3 119,234.1 125,195.8 129,577.7

Total Production (Mboe) 34,650.5 46,778.2 53,865.8 64,639.0 70,422.5 75,704.2 79,489.4 83,463.9 86,385.1

Production Growth 55% 35% 20% 20% 15% 8% 5% 5% 4%

Production Costs:

Production Expenses ($/Mboe) 6.00$ 6.60$ 7.13$ 7.70$ 8.31$ 8.98$ 9.70$ 10.47$ 11.31$

Production Taxes and Other Expenses ($/Mboe) 6.70 7.37 9.00 9.90 10.89 11.98 13.18 14.49 15.94

Depreciation, depletion, amortization & accretion 8.0% 8.0% 8.0% 8.0% 8.0% 8.0% 8.0% 8.0% 8.0%

(as % of Beginning Book Value)

SG&A (as % of Sales) 5.5% 5.5% 5.5% 5.5% 5.5% 5.5% 5.5% 5.5% 5.5%

Exploration Expenses (% of Sales) 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0% 2.0%

Production Expenses to Affiliates (% of Sales) 0.20% 0.14% 0.12% 0.09% 0.08% 0.07% 0.07% 0.06% 0.06%

Crude oil & natural gas service operations 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8%

Commodity Price Growth:

Crude Oil Price Growth 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% 4.5%

Natural Gas Price Growth 4.63% 4.63% 4.63% 4.63% 4.63% 4.63% 4.63% 4.63% 4.63%

13. Continental Resources Inc

Income Statement

$ Amounts in Millions

Fiscal Years Ending Dec. 31 2009 2010 2011 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E(CV)

Revenue

Crude oil & natural gas sales 584.09 917.50 1553.63 2,194.17 3,238.83 3,897.80 4,888.36 5,565.98 6,253.34 6,862.21 7,530.35 8,145.50

Crude oil & natural gas sales to affiliates 26.61 31.02 93.79 65.83 97.16 116.93 146.65 166.98 187.60 205.87 225.91 244.36

Gain (loss) on mark-to-market derivative instruments, net (1.52) (130.76) (30.05) ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐

Crude oil & natural gas service operations 17.03 21.30 32.42 50.47 74.49 89.65 112.43 128.02 143.83 157.83 173.20 187.35

Total Operating Revenues 626.21 839.07 1649.79 2,310.46 3,410.49 4,104.39 5,147.44 5,860.98 6,584.77 7,225.90 7,929.46 8,577.21

Production expenses 76.72 86.56 135.18 207.90 308.74 383.96 497.61 585.50 679.77 770.85 874.15 977.12

Production expenses to affiliates 16.52 6.65 4.63 4.68 4.73 4.77 4.82 4.87 4.92 4.97 5.02 5.07

Production taxes & other expenses 45.65 76.66 143.24 232.16 344.76 484.79 639.93 766.90 906.86 1,047.42 1,209.77 1,377.33

Exploration expenses 12.62 12.76 27.92 46.21 68.21 82.09 102.95 117.22 131.70 144.52 158.59 171.54

Crude oil & natural gas service operations 10.74 18.07 26.74 41.59 61.39 73.88 92.65 105.50 118.53 130.07 142.73 154.39

Depreciation, depletion, amortization & accretion 207.60 243.60 390.90 493.12 725.12 921.12 1,097.12 1,257.12 1,417.12 1,569.12 1,721.12 1,853.12

Property impairments 83.69 64.95 108.46 113.88 119.57 125.55 131.83 138.42 145.34 152.61 160.24 168.25

General & administrative expenses 41.09 49.09 72.82 127.08 187.58 225.74 283.11 322.35 362.16 397.42 436.12 471.75

(Gain) loss on sale of assets (0.71) (29.59) (20.84) (21.88) (22.97) (24.12) (25.33) (26.60) (27.92) (29.32) (30.79) (32.33)

Total operating costs & expenses 493.92 528.74 889.04 1,244.73 1,797.11 2,277.78 2,824.68 3,271.28 3,738.46 4,187.66 4,676.95 5,146.24

Income (Loss) from operations 132.29 310.32 760.75 1,065.73 1,613.38 1,826.61 2,322.76 2,589.69 2,846.31 3,038.24 3,252.51 3,430.97

Interest expense (23.23) (53.15) (76.72) (227.48) (290.36) (335.25) (374.84) (426.10) (477.36) (528.62) (579.88) (631.14)

Other income (expense) 0.95 1.29 3.42 3.42 3.42 3.42 3.42 3.42 3.42 3.42 3.42 3.42

Total other income (expense) (22.28) (51.85) (73.31) (224.06) (286.94) (331.83) (371.42) (422.68) (473.94) (525.20) (576.46) (627.72)

Income before income taxes 110.01 258.47 687.45 841.67 1,326.44 1,494.78 1,951.34 2,167.01 2,372.37 2,513.04 2,676.05 2,803.25

Total current tax provision 2.55 12.85 13.17 42.08 42.50 42.93 43.36 43.79 44.23 44.67 45.12 45.57

Total deferred income tax provision 36.12 77.36 245.20 264.82 286.00 308.89 333.60 360.28 389.11 420.23 453.85 490.16

Provision (benefit) for income taxes 38.67 90.21 258.37 306.90 328.51 351.81 376.95 404.08 433.34 464.91 498.97 535.73

Net income (loss) 71.34 168.26 429.07 534.77 997.93 1,142.97 1,574.38 1,762.94 1,939.03 2,048.14 2,177.08 2,267.52

Basic Earnings per share 0.42 0.99 2.41 2.96 5.48 6.27 8.64 9.68 10.64 11.24 11.95 12.45

Number of Shares Outstanding 169.97 170.41 180.87 180.96 182.16 182.16 182.16 182.16 182.16 182.16 182.16 182.16

Dividends per Share 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

20. Continental Resources Inc.

Weighted Average Cost of Capital (WACC) Estimation

Risk Free Rate 2.92%

MRP 5.92%

Beta 1.65

Cost of Equity 12.69%

Debt Rating BB+

Pre‐tax Cost of Debt 8.25%

Tax Rate 38.00%

After‐Tax Cost of Debt 5.12%

Shares Outstanding 185.02

Current Stock Price 70.59

Market Value of Equity 13060.28

Value of Debt 3829.086

PV of Operating Leases 5

Market Value of Debt 3834.086

Market Value of firm 16894.37

Weight of Debt 22.69%

Weight of Equity 77.31%

Weighted Average Cost of Capital 10.97%

21. Continental Resources Inc

Discounted Cash Flow (DCF) and Economic Profit (EP) Valuation Models

Key Inputs:

CV Growth 3.50%

CV ROIC 22.51%

WACC 10.97%

Cost of Equity 12.69%

Fiscal Years Ending Dec. 31 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E(CV)

DCF Model

Free Cash Flows (1,773.09) (783.11) 123.46 804.20 1,438.57 1,967.61 2,381.96 2,988.73

Continuing Value 37,999.29

Present Value Factors 1.11 1.23 1.37 1.52 1.68 1.87 2.07 2.30

PV of FCF discounted by WACC (1,597.82) (635.94) 90.35 530.34 854.90 1,053.71 1,149.51 1,299.76 16,525.37

Value of Operating Assets 19,270.17

Add: Non‐Operating Assets

Derivative Assets 10.29

Less: Debt

Long Term 3,829.09

Less: Other Claims

Operating Leases 5.00

ESOP 38.05

Derivative Liabilities 174.58

Enterprise Value 15,233.75

Shares Outstanding 180.87

Price 84.22

Adjusted Price 93.44

Fiscal Years Ending 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E(CV)

EP Model

Economic Profit 457.57 683.72 659.35 979.37 1,106.36 1,257.61 1,377.96 1,544.25

Present Value Factors 1.11 1.23 1.37 1.52 1.68 1.87 2.07 2.30

Continuing Value 23,065.90

PV of Economic Profit 412.34 555.23 482.51 645.86 657.48 673.48 664.99 671.57 10,031.04

PV of EP and Continuing Value 14,794.50

Invested Capital 2011 4,475.67

Value of Operating Assets 19,270.17

Add: Non‐Operating Assets

Derivative Assets 10.29

Less: Debt

Long Term 3,829.09

Less: Other Claims

Operating Leases 5.00

ESOP 38.05

Derivative liabilites 174.58

Enterprise Value 15,233.74

Shares Outstanding 180.87

Price 84.22

Adjusted Price 93.44

26. 2011

Present Value of Operating Lease Obligations

Operating

Fiscal Years Ending Dec. 31 Leases

2012 2.191

2013 1.67

2014 1.67

2015 0.088

2016 0.088

Thereafter 0.194

Total Minimum Payments 5.901

Less: Interest 1

PV of Minimum Payments 5.00

Capitalization of Operating Leases

Pre‐Tax Cost of Debt 8.25%

Number Years Implied by Year 6 Payment 2.2

Lease PV Lease

Year Commitment Payment

1 2.191 2.0

2 1.67 1.4

3 1.67 1.3

4 0.088 0.1

5 0.088 0.1

6 & beyond 0.088 0.1

PV of Minimum Payments 5.0

27. Effects of ESOP Exercise and Share Repurchases on Common Stock Balance Sheet Account and Number of Shares Outstanding

Number of Options Outstanding (shares): 86,500

Average Time to Maturity (years): 1.25

Expected Annual Number of Options Exercised: 69,200

Current Average Strike Price: 45.43$

Cost of Equity: 9.00%

Current Stock Price: 69.48$

2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Increase in Shares Outstanding: 86,500 1,198,344

Average Strike Price: 0.71$ 48.66$

Increase in Common Stock Account: 61,415 58,311,419 - - - - - - - -

Change in Treasury Stock 0 0 0 0 0 0 0 0 0 0

Expected Price of Repurchased Shares: 69.48$ 75.73$ 82.55$ 89.98$ 98.08$ 106.90$ 116.52$ 127.01$ 138.44$ 150.90$

Number of Shares Repurchased: - - - - - - - - - -

Shares Outstanding (beginning of the year) 180,871,688 180,958,188 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532

Plus: Shares Issued Through ESOP 86,500 1,198,344 0 0 0 0 0 0 0 0

Less: Shares Repurchased in Treasury - - - - - - - - - -

Shares Outstanding (end of the year) 180,958,188 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532 182,156,532

28. VALUATION OF OPTIONS GRANTED IN ESOP

Ticker Symbol CLR

Current Stock Price 69.48

Risk Free Rate 4.80%

Current Dividend Yield 0.79%

Annualized St. Dev. of Stock Returns 38.80%

Average Average B‐S Value

Range of Number Exercise Remaining Option of Options

Outstanding Options of Shares Price Life (yrs) Price Granted

ESOP 86,500 0.71 0.25 68.64$ 5,937,479$

Restricted Stock 1,198,344 48.66 1.70 26.79$ 32,107,990$

Total 1,284,844 45.43$ 1.60 29.49$ 38,045,469$