More Related Content Similar to Chasing unicorns feb 2020 (20) 1. Chasing Unicorns

XenBytes, February 2020: Chasing Unicorns

By Kenneth Yeo, CIO

A unicorn is a privately held startup company

with a current valuation of US$1 billion or

more

In the connected world we live in, we are often shown investment opportunities

by our friends or receive unsolicited opportunities in our Inbox. Here, we discuss

two important considerations (amongst others) when chasing unicorns - investment

stage and share type.

Early Stage

I see a lot of early stage companies looking for seed/A round investments.

These could range from founders with a business plan to companies having some

early revenue.

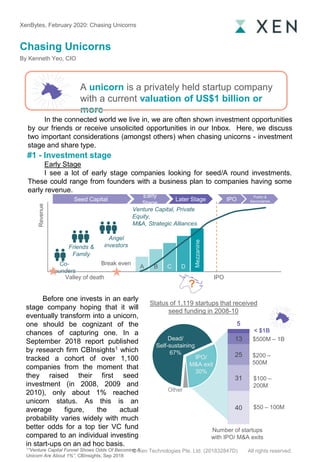

Before one invests in an early

stage company hoping that it will

eventually transform into a unicorn,

one should be cognizant of the

chances of capturing one. In a

September 2018 report published

by research firm CBInsights1 which

tracked a cohort of over 1,100

companies from the moment that

they raised their first seed

investment (in 2008, 2009 and

2010), only about 1% reached

unicorn status. As this is an

average figure, the actual

probability varies widely with much

better odds for a top tier VC fund

compared to an individual investing

in start-ups on an ad hoc basis.

#1 - Investment stage

1“Venture Capital Funnel Shows Odds Of Becoming A

Unicorn Are About 1%”, CBInsights, Sep 2018

40

31

25

13

5

< $1B

$500M – 1B

$200 –

500M

$100 –

200M

$50 – 100M

Number of startups

with IPO/ M&A exits

Dead/

Self-sustaining

67%

IPO/

M&A exit

30%

Other

Status of 1,119 startups that received

seed funding in 2008-10

Co-

founders

Revenue

Seed Capital

Early

Stage

Later Stage IPO

Public &

Secondaries

Valley of death

Break even

A B C D

Mezzanine

Friends &

Family

Venture Capital, Private

Equity,

M&A, Strategic Alliances

Angel

investors

IPO

?

© Xen Technologies Pte. Ltd. (201832847D) All rights reserved.

2. Late Stage

Investing in unicorns after they have become unicorns have been popular in

recent years. While the risk of the company not reaching the finishing line of a

successful IPO is lower than an early stage investment, it may not result in a

profitable investment.

Below is a simulation of the funding rounds a start-up goes through before

reaching a successful IPO.

Pre-Money, $M

Dilution

Post-money,

$M

20

20%

24

50

20%

60

100

20%

120

300

20%

360

1,000

20%

1,200

2,000

20%

2,400

3,000

20%

3,600

1.00 2.10 3.50

8.70

24.10

40.20

50.20

0

10

20

30

40

50

60

A B C D E Pre-IPO IPO

Price/share,$

Stage of

financing

Series A

InvestorCost/share = $1 50x IPO

price

Pre-IPO Investor

Cost/share =

$40.20

1.25x IPO

price

The investor in the A round of this

simulation makes 50x his

investment (his cost/share is $1

while the IPO price per share is

$50).

The pre-IPO investor makes 1.25x.

For the pre-IPO investor, most of

the upside or downside will take

place post-IPO. The risk of making

a loss is high if the stock price

declines after IPO.

Pre-Money valuation is the company

valuation prior to the investment round

Dilution is the decrease in ownership

for existing shareholders that occurs

when a company issues new shares

Post-Money valuation is the value

after the investment has been made

Definitions

© Xen Technologies Pte. Ltd. (201832847D) All rights reserved.

XenBytes, February 2020: Chasing Unicorns

3. Case study: Uber

According to Crunchbase, Uber raised a total of US$16.6b in 22 funding

rounds prior to its IPO in May 2019 at a pre-money valuation of US$74b (US$45

per share), which is just above the pre-IPO round led by Toyota raised about 6

months before its IPO. After IPO, the share price fell to a low of just below

US$30/share, which is below the valuation of the early 2018 funding round led by

Softbank at US$33/share. The share price has since recovered some ground and is

trading at US$36/share (as of end Jan 2020). Thus, pre-investors who bought

shares at pre-IPO valuation and have held on to these shares are still making

losses.

This is not unique to Uber. Of the top 50 VC backed IPOs in 2019, 14 were

trading below their respective IPO valuations on Jan 31, 2020. The top 4

companies have valuations of above US$10b each at IPO, namely, Uber (US$82b),

Lyft (US$24b), Slack Technologies (US$23b) and Pinterest (US$13b). With the

exception of Pinterest, all the other 3 companies were trading below their IPO price

as of end Jan 2020 with discounts of between 16% to 56%. The largest unicorns are

usually the ones that are most well-known and commonly available to investors pre-

IPO and are also the most likely to underperform after the IPO.

0

10

20

30

40

50

60

70

80

90

0

1

2

3

4

5

6

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Equity

Debt

Funds raised

(US$B)

Implied

valuation

(US$B)

IPO Valuation:

$82.4B

Current market cap:

$62.5B

2013

TPG & Google lead

$258m investment

2015

Goldman raises $1.6b in convertible

debt from private wealth clients

2016

Saudi wealth fund makes $3.5b

backing

2017

SoftBank-led consortium invests

$1.3b

2018

Toyota invests

$500m

© Xen Technologies Pte. Ltd. (201832847D) All rights reserved.

XenBytes, February 2020: Chasing Unicorns

4. #2 - Share type

The other important consideration is the share type which can be broadly

classified into primary and secondary shares.

Primary shares

Shares you buy directly from the

company when the company raises a

new round

Secondary shares

Shares bought from existing

shareholders or management

Who are the investors investing in

the round?

Having a top tier VC fund leading

the round will give more assurance than

a round led by a strategic investor who

might have other considerations beyond

financial gains.

What to consider

Who is the seller and why is he

selling?

As an “outsider” we must avoid being

“dumped” shares by “insiders” who have

better visibility of the company’s

performance.

What to consider

Share class and valuation

Shares sold by founders or early

investors are usually of a lower

preference than later round shares sold

by the company. In the event of a

liquidation, the holders of lower class of

shares will only be paid back after the

holders of higher classes of shares have

been paid back.

Direct vs. indirect shares

Earlier investors typically hold their

shares in an SPV. When selling their

shares to you they are transferring

shares in the SPV instead of shares of

the underlying company. This means

you have no direct access to the

company and are dependent on the

seller to provide you with ongoing

updates on the company.

When purchasing indirect

shares, you should also

look at the terms of sale

to see if the seller

charges you any fees and

carry for managing the

SPV.

© Xen Technologies Pte. Ltd. (201832847D) All rights reserved.

XenBytes, February 2020: Chasing Unicorns

5. Chasing unicorns is a potentially rewarding but highly risky hobby that is best

left to the professionals (top tier VC funds) who have the experience of spotting the

next unicorn and also the expertise to give assistance and guidance to groom the

start-ups into unicorns.

At Xen, we seek out the best VC managers and present opportunities for

investors to invest in them via our a fintech solution, which allows fractionalized

access and tradability in alternative investments, through a user-friendly, compliant

onboarding platform. We also bring curated quality unicorn opportunities backed by

top tier VC funds to our investors.The author

About Xen

Kenneth has over 20 years of experience in the private equity industry.

He started his investment career with the Government of Singapore

Investment Corp (GIC) where he spent 12 years, half of which was

based in GIC's overseas offices in Bangkok, London and the Silicon

Valley. Kenneth joined Allianz Capital Partners in 2007 as an

Investment Director, responsible for its private equity fund investments

in Asia. Most recently, he was a Senior Director at Azalea, a wholly

owned subsidiary of Temasek Holdings.

Transforming Alternative Asset Management.

We live in an age where access to the right investments can be a door to wealth and financial security.

In Asia, where there has been an unprecedented growth in wealth, the current force of economic

influence and power is among the young and affluent, the millennials and XENnials.

Most accredited investors in Asia are locked out of alternative opportunities due to high barriers to entry

– high minimum investment levels, zero liquidity and lack of transparency. Only a small fraction of

investors has access to the above market returns and performance of alternative investments, including

private equity, venture capital, real estate, infrastructure, private debt and hedge funds. Xen creates a

fintech solution which allows fractionalized access and tradability in alternative investments, through a

user-friendly, compliant onboarding platform.

Xen is opening up an industry, traditionally dominated by and designed for UHNWIs and institutional

investors, to accredited investors seeking access and liquidity in alternatives.

Founded in 2018 by a strong management team of former investment bankers, traders and fintech

veterans, Xen envisions a future of alternative asset management powered by technology for the

utmost transparency, liquidity and cost efficiency.

© Xen Technologies Pte. Ltd. (201832847D) All rights reserved.

This Publication and any information contained herein is made available by Xen Technologies Pte. Ltd. (hereafter “Xen”) for general

information only and not for any other purpose. The Viewer agrees that this website shall be used solely as reference, or for

informational use and not for any other purposes, commercial or otherwise. The information contained in this publication is not

intended and should not be used or construed as an offer to sell, or a solicitation of any offer to buy, securities of any fund or other

investment product in any jurisdiction. Neither Xen nor any of its officers, directors, agents and employees makes any warranty,

express or implied, of any kind related to the adequacy, accuracy or completeness of any information on this site or the use of

information in this publication. The information in this publication is not intended and should not be construed as investment, tax,

legal, financial or other advice. Xen holds exclusive and rightful ownership of the intellectual and proprietary rights to all opinions,

concepts, ideas, work products, and the like, related to or as a result of the General Information and contents in this publication.

Contact us info@xen.net Oxley Tower #23-02, 138 Robinson

Road

Singapore 068906

Conclusion

XenBytes, February 2020: Chasing Unicorns