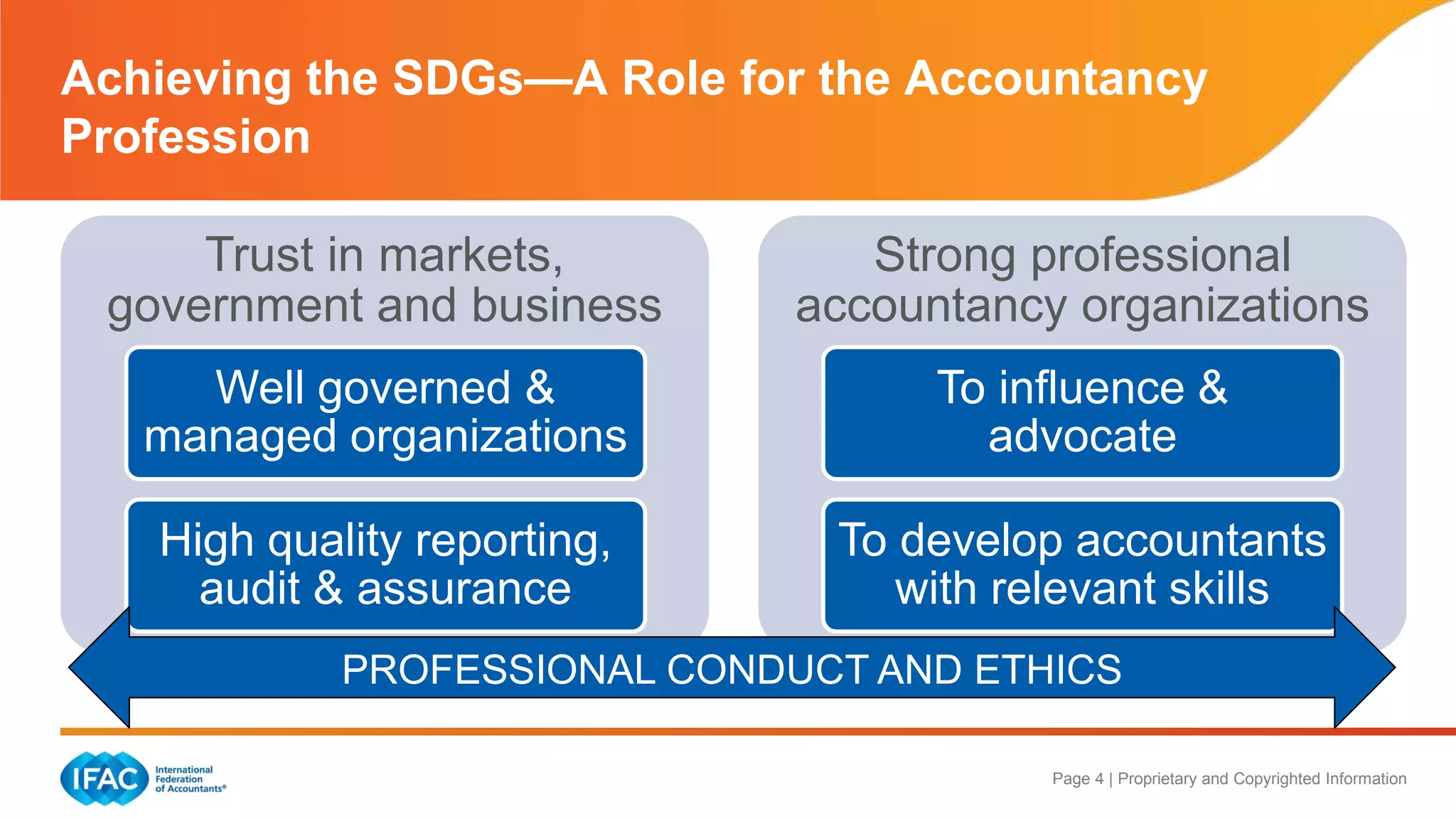

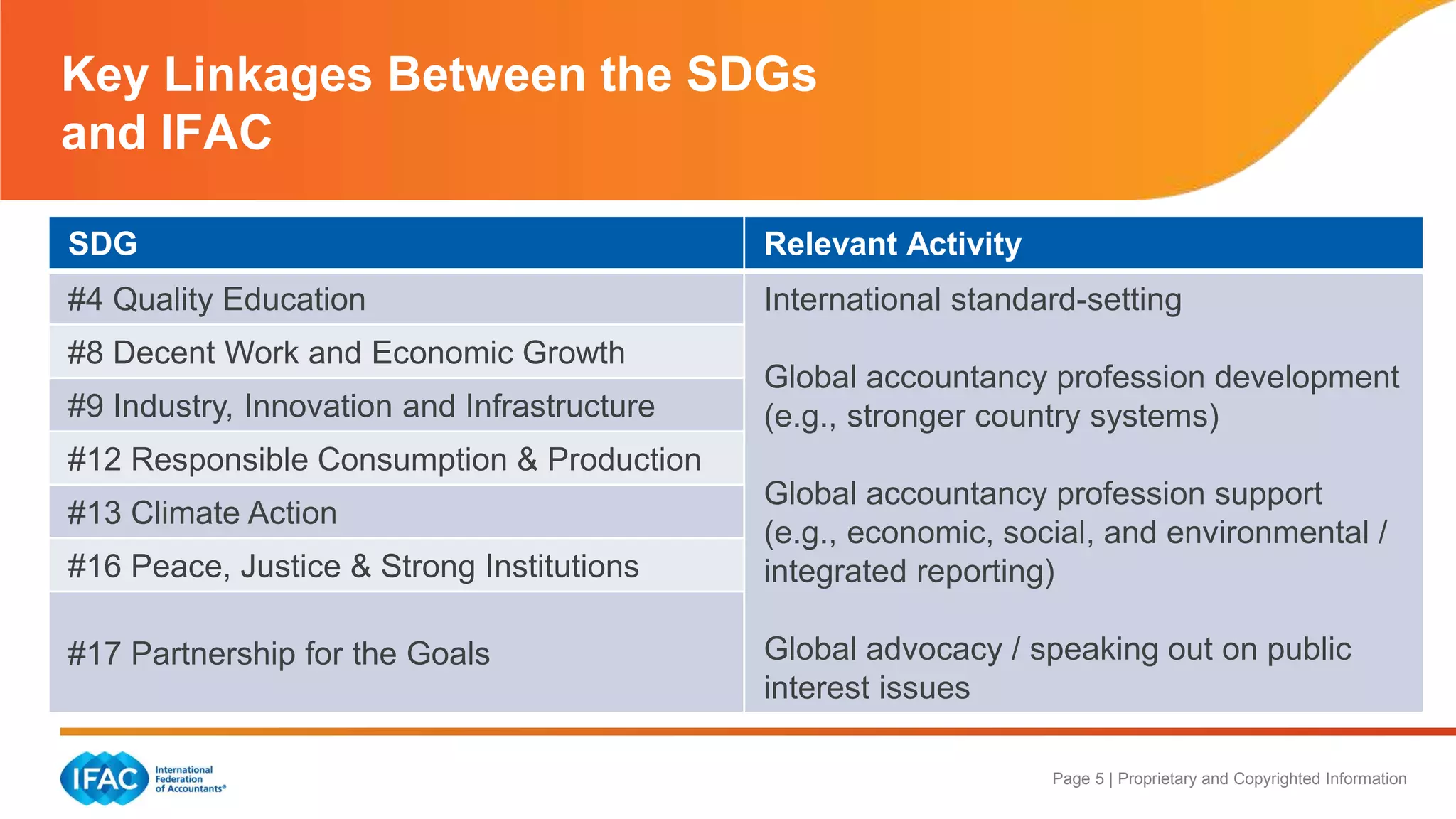

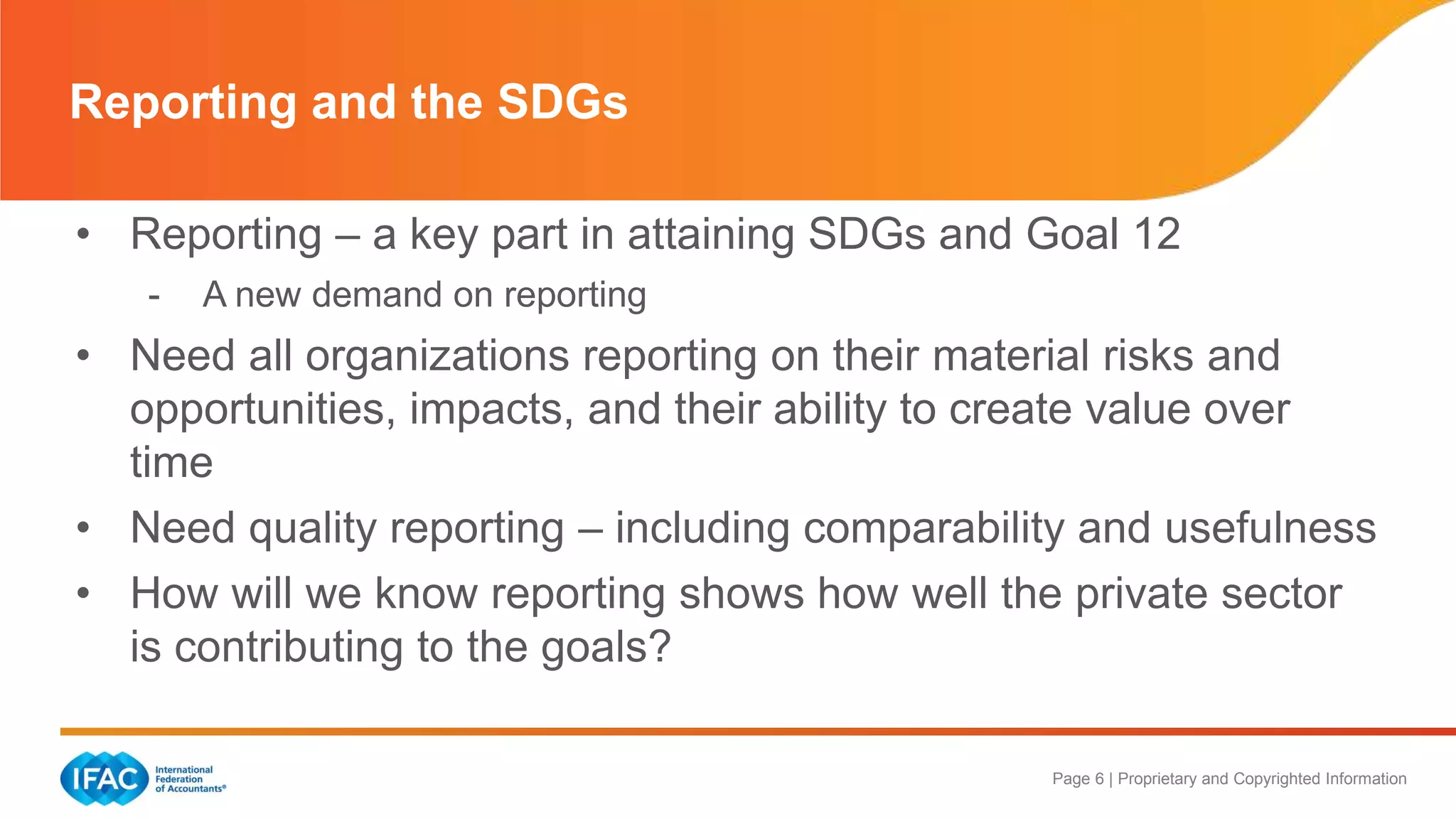

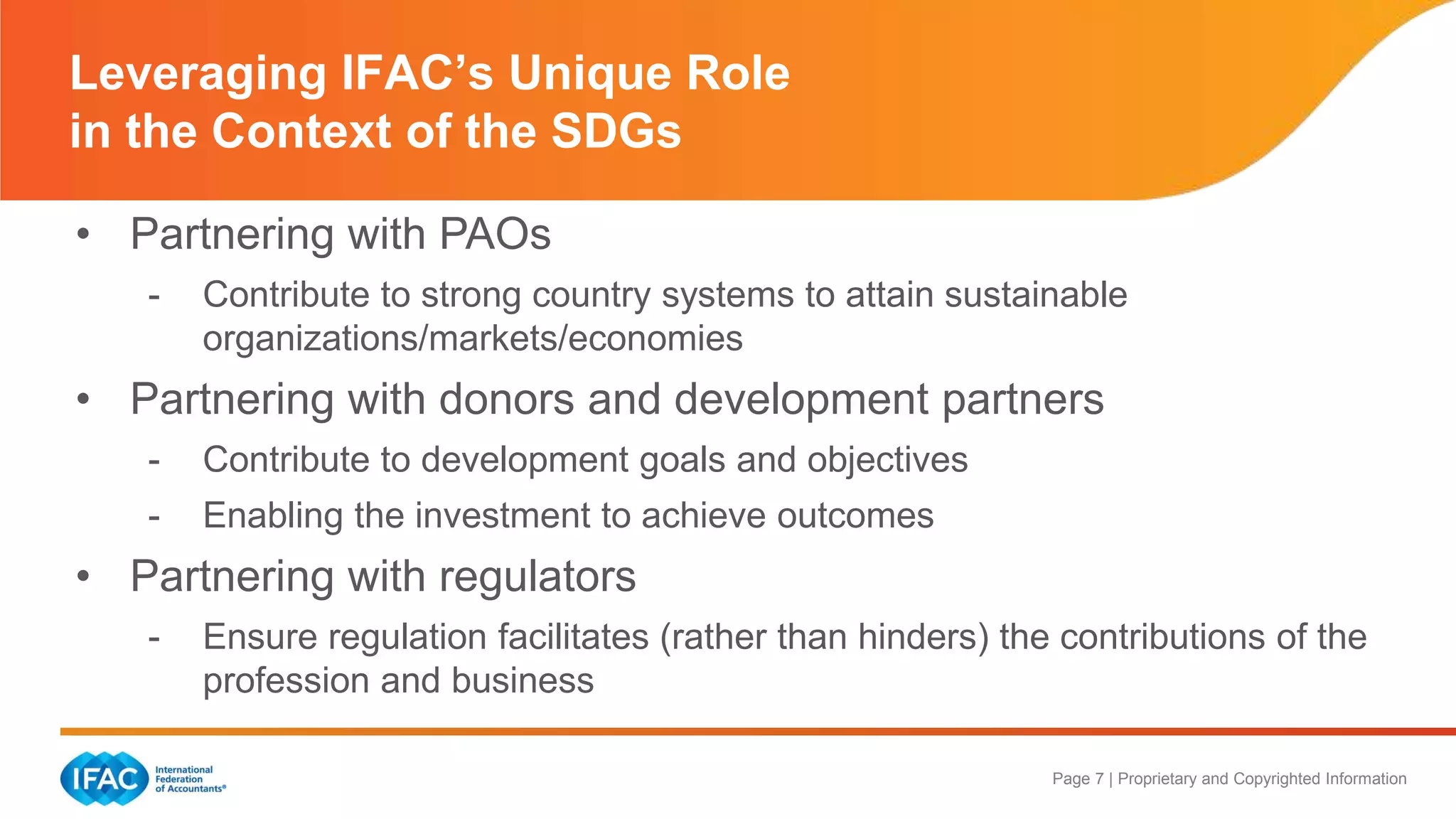

The document outlines the role of the accountancy profession in achieving the Sustainable Development Goals (SDGs), emphasizing the importance of quality reporting and governance. It highlights the need for accounting professionals to contribute to sustainable economic development through trusted organizations and markets. Additionally, it discusses partnerships with various stakeholders to advance development goals and support strong reporting standards.