Downloaded 60 times

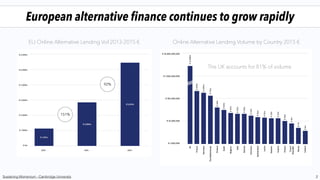

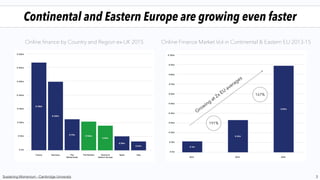

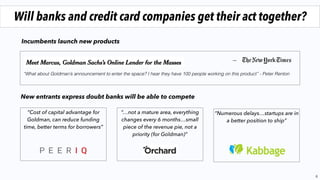

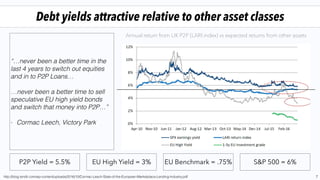

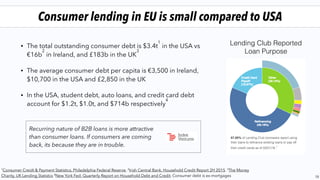

European alternative lending continues to grow rapidly, led by the UK which accounts for 81% of the market. Growth in continental and eastern Europe is even faster. Yields remain attractive compared to traditional assets like bonds. While a few large players like Funding Circle have emerged, penetration of alternative lending remains low in Europe. As the market matures, players are focusing on withstanding potential downturns and exploring international expansion. Bordersless online lenders are also emerging to serve new regions. Overall, the market is expected to continue growing from its current penetration rate of less than 1% of the total lending market in Europe.