1. Queen Mary Trading & Investment Society

Energy Market Round-up (February 2nd, 2015)

1

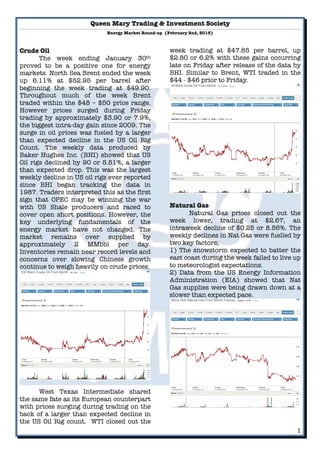

Crude Oil

The week ending January 30th

proved to be a positive one for energy

markets. North Sea Brent ended the week

up 6.11% at $52.95 per barrel after

beginning the week trading at $49.90.

Throughout much of the week Brent

traded within the $48 – $50 price range.

However prices surged during Friday

trading by approximately $3.90 or 7.9%,

the biggest intra-day gain since 2009. The

surge in oil prices was fueled by a larger

than expected decline in the US Oil Rig

Count. The weekly data produced by

Baker Hughes Inc. (BHI) showed that US

Oil rigs declined by 90 or 5.51%, a larger

than expected drop. This was the largest

weekly decline in US oil rigs ever reported

since BHI began tracking the data in

1987. Traders interpreted this as the first

sign that OPEC may be winning the war

with US Shale producers and raced to

cover open short positions. However, the

key underlying fundamentals of the

energy market have not changed. The

market remains over supplied by

approximately 2 MMbbl per day.

Inventories remain near record levels and

concerns over slowing Chinese growth

continue to weigh heavily on crude prices.

West Texas Intermediate shared

the same fate as its European counterpart

with prices surging during trading on the

back of a larger than expected decline in

the US Oil Rig count. WTI closed out the

week trading at $47.85 per barrel, up

$2.80 or 6.2% with these gains occurring

late on Friday after release of the data by

BHI. Similar to Brent, WTI traded in the

$44 - $46 prior to Friday.

Natural Gas

Natural Gas prices closed out the

week lower, trading at $2.67, an

intraweek decline of $0.25 or 8.56%. The

weekly declines in Nat Gas were fuelled by

two key factors;

1) The snowstorm expected to batter the

east coast during the week failed to live up

to meteorologist expectations.

2) Data from the US Energy Information

Administration (EIA) showed that Nat

Gas supplies were being drawn down at a

slower than expected pace.

2. Queen Mary Trading & Investment Society

Energy Market Round-up (February 2nd, 2015)

2

Revenge of the Oil Workers? - On Sunday

February 1st the United Steelworkers

Union (USW), a large union

representative for workers in the US Oil &

Gas Industry began strike action at 9 US

refinery and chemical plant sites. The

strike action resulted after negotiations

between the union and the

energy/petrochemicals industry led by

Royal Dutch Shell broke down. The

refineries involved in the strike at present

can produce approximately 1.82 MMbbl

of fuel per day, approximately 10% of

total US capacity. It has also been

reported that more refineries are

standing by to join the strike action.

Notably, USW has not called a national

strike since 1980, when that stoppage

lasted for 3 months.

This could have major implications

for prices on distillates such as gasoline in

the near future, dependent upon how long

the negotiations take and whether the

Union decides to take a more aggressive

stance.

One step closer to Keystone

The US senate, currently controlled by

republican passed a bill to approve the

Keystone XL pipeline. The proposed

Keystone XL pipeline is expected to

transport oil from the Alberta Oil Sands in

Canada to Nebraska and increase supply

into US refineries by 830K barrels per

day. The action by the US senate is in an

effort to bypass the administration

review, which has been on going for the

past 6 years. While this will not have any

impact on energy prices in the short-term,

approval of the pipeline would eventually

increase overall supplies of crude oil stock

available to refineries in the Gulf and

reduce America’s need for imports crude

from Middle Eastern and South American

countries. Supporting its goal of complete

energy independence.

Sustained low prices continue to hurt US oil

producers. The latest BHI rig count figures shown

above highlight how acutely US shale Oil

producers are feeling the pinch of cheap oil, with

the rapid decline in oil rigs.

The EIA reported total natural gas in storage at

2,543 billion cubic feet (Bcf), a WoW decline of

approximately 3.6%. Presently stocks of nat gas

are 324 Bcf higher than last year same time.

Created by - Brad Kellman, QMTIS Energy

Analyst