1. 1

68% 68%

64% 64%

69%

72% 72%

04-05 05-06 06-07 07-08 08-09 09-10 10-11

TML National MS

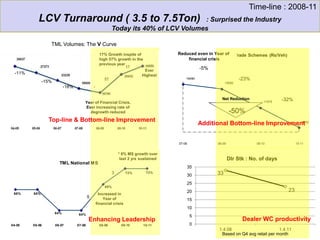

Year of Financial Crisis.

Ever increasing rate of

degrowth reduced

17% Growth inspite of

high 57% growth in the

previous year

Ever

Highest

TML Volumes: The V Curve

5

3

Increased in

Year of

financial crisis

* 8% MS growth over

last 2 yrs sustained

-11%

-15%

-18%

Top-line & Bottom-line Improvement

Enhancing Leadership

16490

15590

11975

8200

07-08 08-09 09-10 10-11

Reduction in Trade Schemes (Rs/Veh)Reduced even in Year of

financial crisis

-32%

-23%

-5%

-50%

Net Reduction

Additional Bottom-line Improvement

0

5

10

15

20

25

30

35

1.4.08 1.4.11

Dlr Stk : No. of days

33

23

Based on Q4 avg retail per month

Dealer WC productivity

Time-line : 2008-11

LCV Turnaround ( 3.5 to 7.5Ton) : Surprised the Industry

Today its 40% of LCV Volumes