1. PORTFOLIO PUMPING IS NOT

AS RAMPANT AS COMMONLY PERCEIVED

IN THE BROAD MARKET

POTENTIAL PORTFOLIO PUMPING

REPORT FINDINGS:

• Dispelled misconception that portfolio pumping is rampant in Singapore, contrary to the broader market assumption

• Showed that appropriate regulatory framework and structures in place have played a critical role in deterring market manipulation

• Found at certain segmented market level, some degree of potential portfolio pumping, though they are not statistically significant

• Identified common traits among stocks which are potential subject of portfolio pumping

A study that analyses tick-by-tick data from January 2003

to December 2013 from the Singapore Stock Exchange

to gain insight into the degree of market manipulation

that was prevalent. The study was in response to the

2010 successful prosecution of a fund manager involving

portfolio pumping in Singapore.

Market manipulation

is the deliberate attempt to

interfere with free and fair

market operation and involves

the act of artificially inflating or

deflating the price of a security.

Window dressing occurs

when poorly performing stocks in

the portfolio are sold and replaced

with well-performing stocks,

in order to present a favorable

picture of the portfolio for the fund

manager for its annual report.

Portfolio pumping occurs

with the intent of manipulating

the prices of the chosen stocks to

increase the closing prices around a

reference period (usually at quarter-

ends and year-ends). For such

stocks to be considered “pumped”,

their prices should subsequently fall

when the activity ceases, i.e. these

stocks should return to their market

equilibrium prices once the artificial

inflation of stock prices ends.

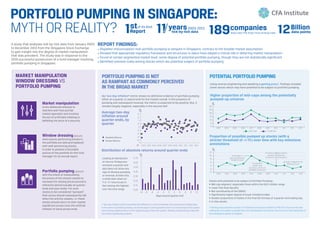

Our two-day inflation* metric shows no definitive evidence of portfolio pumping

either at a quarter or yearly level for the market overall. In the presence of

pumping and subsequent reversal, the metric is expected to be positive. But, it

remains largely negative, especially in the second half.

Using reverse engineering and adopting a gaming proxy*

, findings revealed

some stocks which may have potential to be subject to portfolio pumping.

* Two-day Inflation metric represents the difference in returns between two consecutive trading days.

In the event of portfolio pumping, we would expect a strong positive return on the last day of the quarter

and a strong negative return on the beginning day of the next quarter, thereby making the two-day infla-

tion metric significantly positive.

* Gaming proxy assumes a value of 1 if absolute and excess (relative to FTSE STI) returns on the last

trading day of a quarter is greater than zero and absolute and excess returns on the first trading day of

the subsequent quarter is negative.

Stocks with potential to be subject to Portfolio Pumping:

• Mid-cap segment, especially those within the S$2-5 billion range

• Lower free float liquidity

• Not constituents of the SIMSCI

• Significantly higher degree of buyer-initiated trades

• Greater proportions of trades in the final 30 minutes of a quarter-end trading day

• S-chip stocks

Average two-day

inflation around

quarter-ends, by

quarter

Distribution of absolute returns around quarter ends

Proportion of possible pumped up stocks (with a

stricter threshold of +/-1%) over time with key milestone

annotations

Higher proportion of mid-caps among the potentially

pumped-up universe

Excess Returns

Absolute Returns

MARKET MANIPULATION

WINDOW DRESSING VS

PORTFOLIO PUMPING

Looking at distribution

of returns 10 days pre-

and post a quarter-end

also does not show any

sign of obvious pumping

or reversal, at best only

a small slow-down on

T+3. T+1 returns are in

fact among the highest

over the time range.

%

Days around quarter end

Q1

0

%

-2

-1

1

2

3

-3

-4

-5