Recommended

More Related Content

What's hot

What's hot (20)

Similar to Alert 22

Similar to Alert 22 (20)

Recently uploaded

Recently uploaded (20)

Alert 22

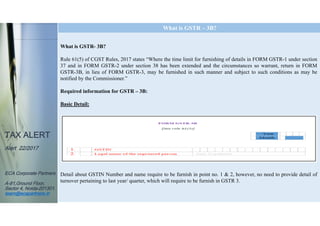

- 1. TAX ALERT Alert 22/2017 ECA Corporate Partners A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in This image cannot currently be displayed. What is GSTR – 3B? What is GSTR- 3B? Rule 61(5) of CGST Rules, 2017 states “Where the time limit for furnishing of details in FORM GSTR-1 under section 37 and in FORM GSTR-2 under section 38 has been extended and the circumstances so warrant, return in FORM GSTR-3B, in lieu of FORM GSTR-3, may be furnished in such manner and subject to such conditions as may be notified by the Commissioner.” Required information for GSTR – 3B: Basic Detail: Detail about GSTIN Number and name require to be furnish in point no. 1 & 2, however, no need to provide detail of turnover pertaining to last year/ quarter, which will require to be furnish in GSTR 3.

- 2. TAX ALERT Alert 22/2017 ECA Corporate Partners A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in Details of Outward Supplies and inward supplies liable to reverse charge As the detail mentioned in return itself describes that what information require to furnish in the cell. We discuss on the point (e) which require clarification from department. As per our opinion, here, taxpayer has to furnish details of sale of alcohol, petrol, diesel, etc. which are out of the purview of GST law. Further, Value of Taxable Supplies = Value of invoices + value of Debit Notes – value of credit notes + value of advances received for which invoices have not been issued in the same month – value of advances adjusted against invoices. (Details of advances as well as adjustment of same against invoices to be adjusted and not shown separately, amendment in any details to be adjusted and not shown separately) Details of inter-State supplies made to unregistered persons, composition dealer and UIN holders In the below table, you need give a break-up of the interstate outward supplies made to Unregistered Persons, Composition Dealers and UIN Holders. These details needs to be captured State-wise/ Union-Territory-wise total with taxable value and total IGST levied on these supplies.

- 3. TAX ALERT Alert 22/2017 ECA Corporate Partners A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in Details of eligible input tax credit

- 4. TAX ALERT Alert 22/2017 ECA Corporate Partners A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in In the above table, you need to capture the details of ITC availability, ITC to be reversed, and arrive at the Net ITC available. The following are the details you need to capture: 1)ITC Available (Whether in Full or Part): You need to give the break-up of inward supplies on which the ITC was availed. The following are the details you need to capture: Import of Goods: Tax credit of IGST paid on import of goods. Import of Service: Tax credit of IGST paid on import of services. Inward supplies liable to reverse charge: You need to capture the ITC of GST paid on inward supplies liable for reverse charge such as, sponsorship services, purchase from URD, and so on, other than import of goods or services. Inward Supplies from ISD: Input tax credit received from Input Service Distributor (ISD). All other ITC: Apart from above, ITC of other inward supplies has to be captured here. 2) Details of Input Tax credit to be reversed: Under this table, you need to capture the ITC reversible on usage of inputs/input services/capital goods used for non-business purpose, or partly used for exempt supplies. Also, if the depreciation is claimed on tax component of capital goods, and plant & machinery, then the ITC will not be allowed. Such reversal needs to be captured in this table. 3) Details of Ineligible ITC: GST paid on inward supplies listed in negative list will not be eligible as input tax credit. The details of GST paid on such supplies needs to be recorded in this table Details of exempt, nil-rated and non-GST inward supplies You need to capture the details of inward supplies made from the composition dealer, inward supplies at nil rate and exempt. Also, you need to separately mention Non-GST inward supplies. The value of above discussed supplies need to be captured separately for interstate and intrastate supplies.

- 5. TAX ALERT Alert 22/2017 ECA Corporate Partners A-81,Ground Floor, Sector 4, Noida-201301. team@ecapartners.in Payment of tax In the above table (6.1), you need to declare the self-ascertained tax payable. This is based on the details of outward supplies and inwards supplies liable to be paid on reverse charge captured in Table No. 3.1. The tax-wise break-up of payment tax by way of utilization of ITC and cash deposit needs to be provided. Our Comments: Though GOI is providing some relaxation to file simplified summary return in GSTR 3B for the initial 2 months, but beware! GSTR 1 of the initial two months still needs to be filed, and that too after two months into GST regime where you may start facing new issues! Also during September you need to prepare the data for filling return which will be due in Oct. So please don’t get relaxed by getting the news of simplified return, rather it is recommended to take extra cautions in the initial period.