Downloaded 1,952 times

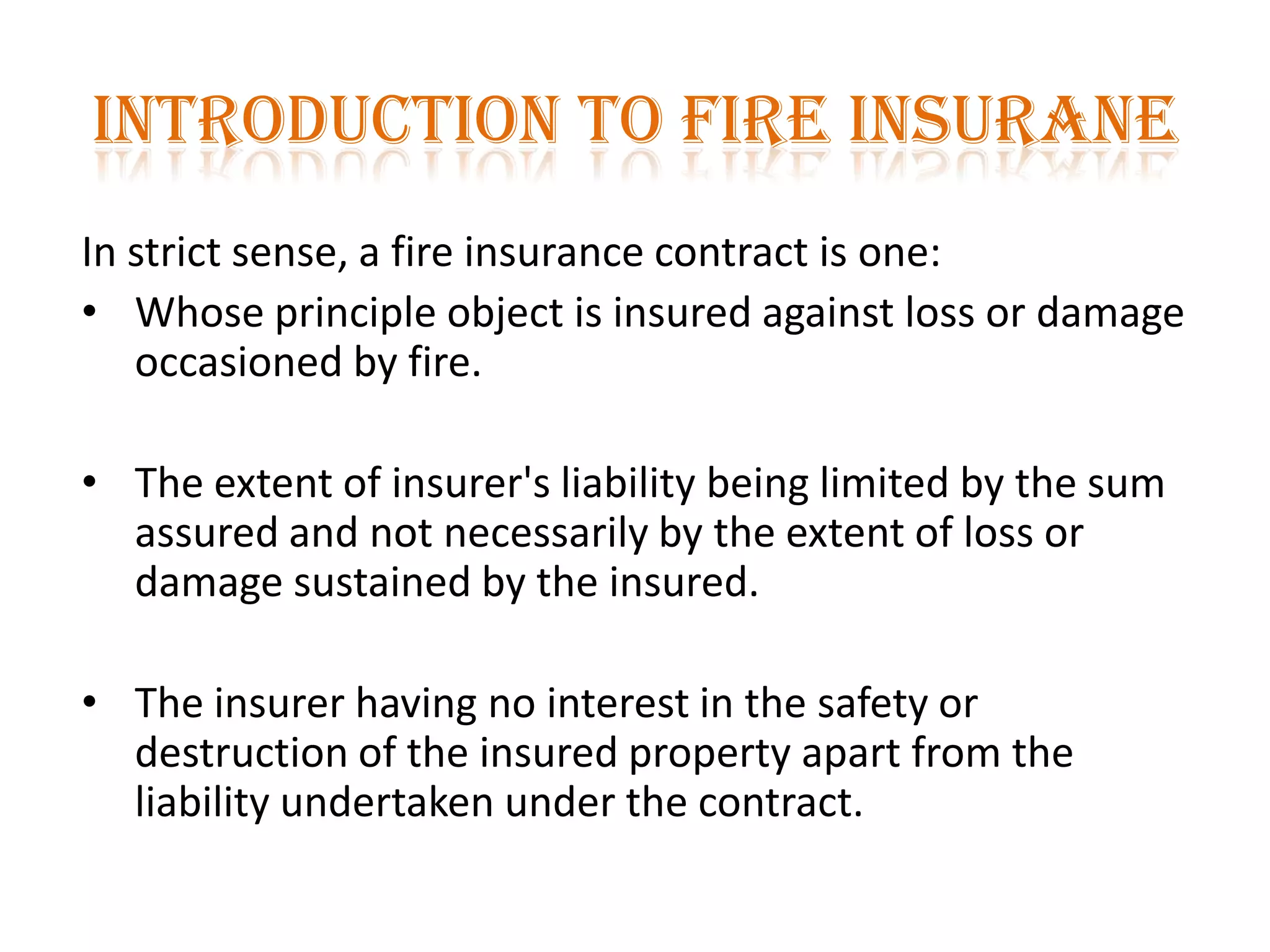

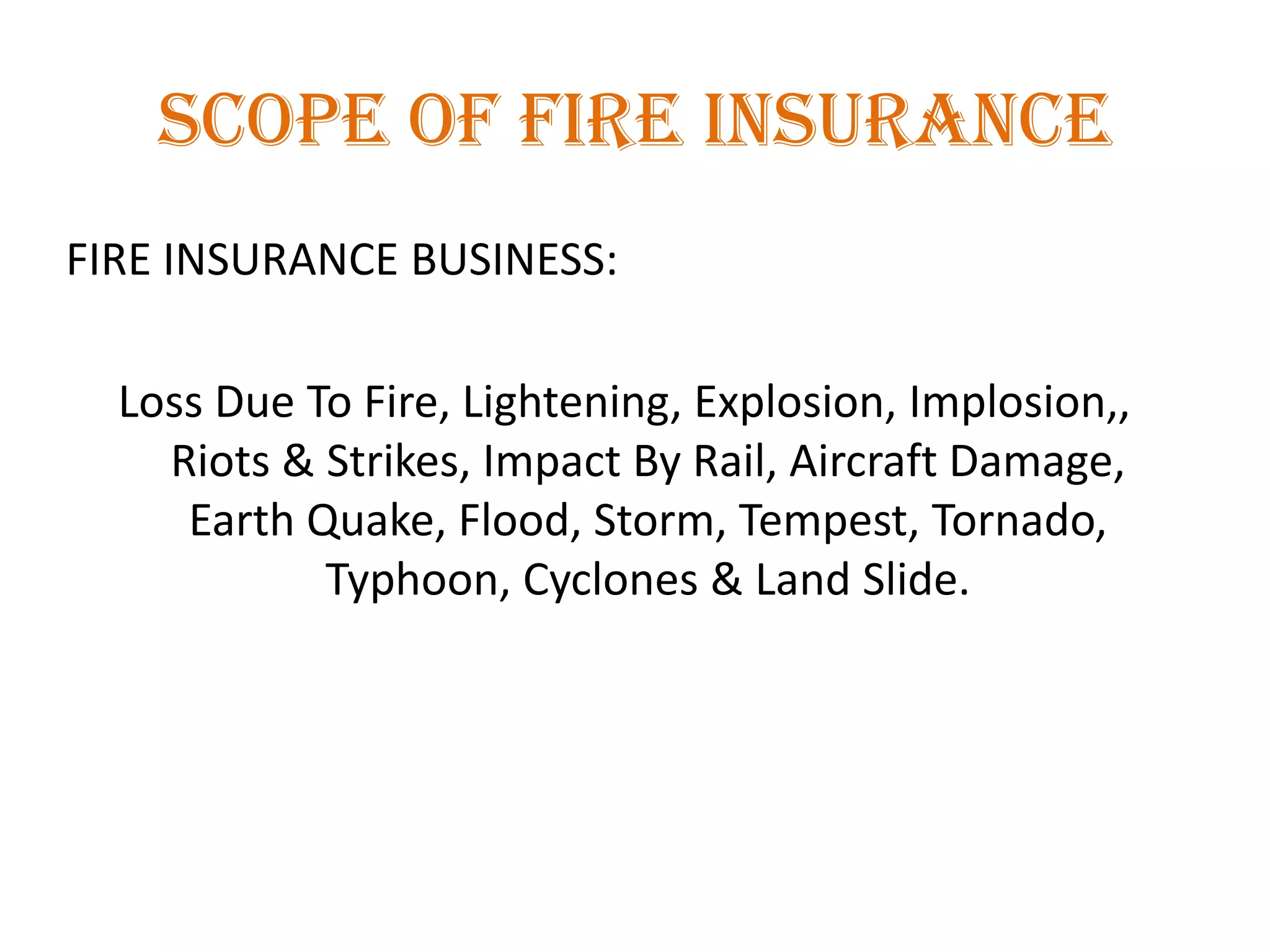

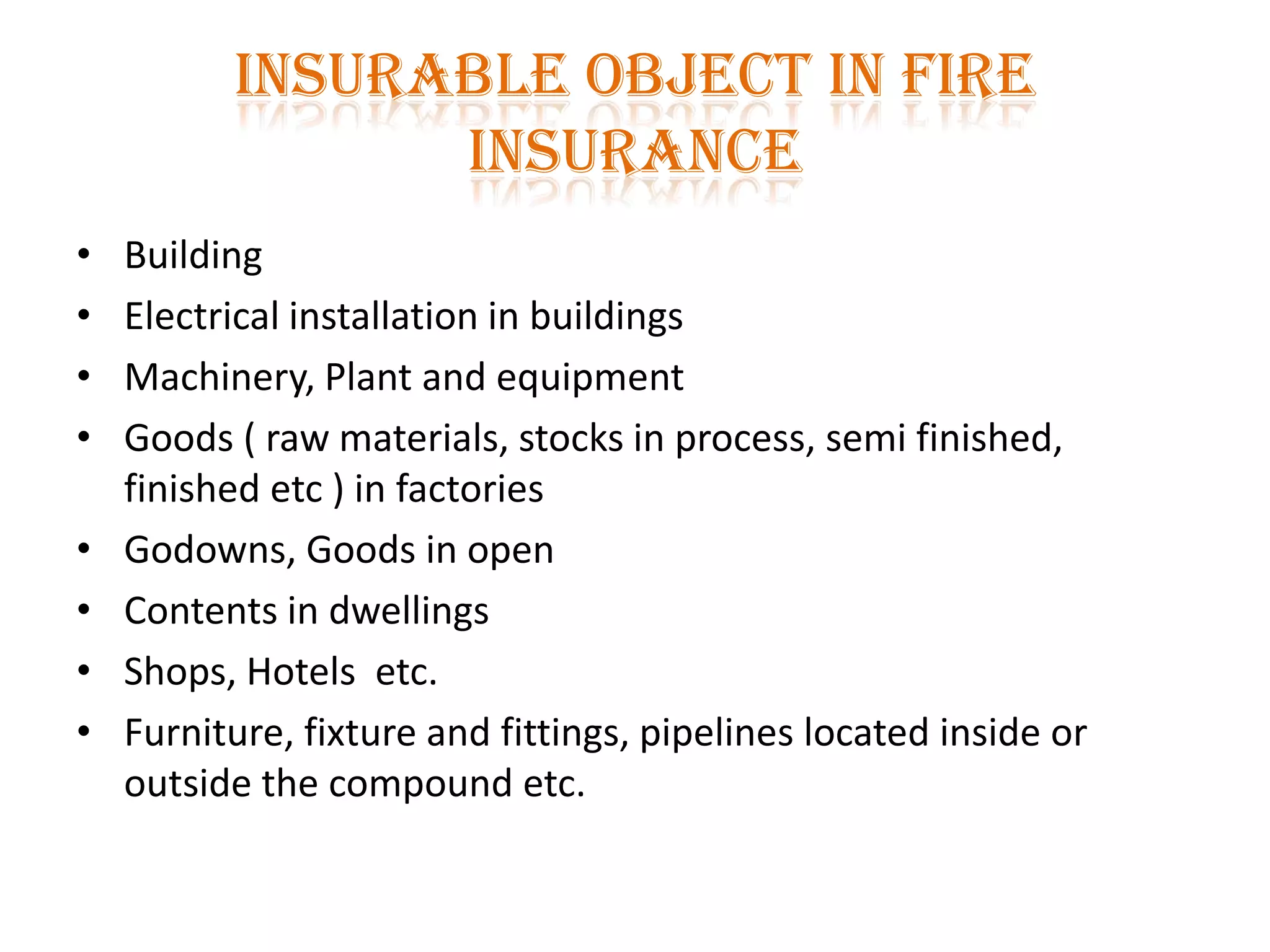

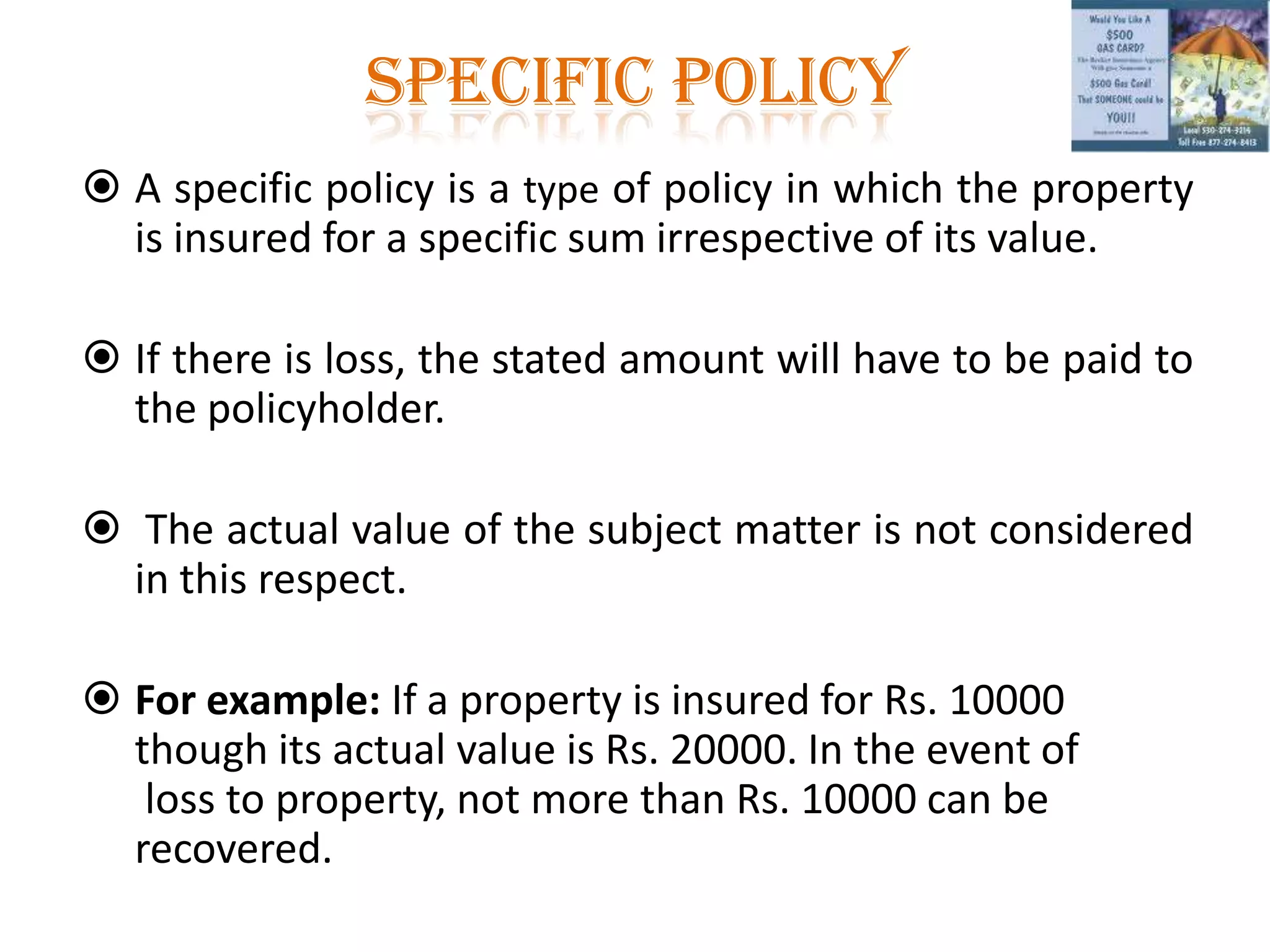

This document provides an overview of fire insurance. It discusses key principles of insurance like utmost good faith, indemnity, and insurable interest. It also describes different types of fire insurance policies like valued policies, floating policies, declaration policies, and adjustable policies. The document outlines the scope of fire insurance and covers losses from fire and other perils. It also discusses the rights of insurers like salvage, subrogation, and contribution. Specific policy and average policy are also summarized.

![Chapter 1[definition and nature of insurance]](https://cdn.slidesharecdn.com/ss_thumbnails/chapter1definitionandnatureofinsurance-150912031826-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![87356964 introduction-to-insurance[1]](https://cdn.slidesharecdn.com/ss_thumbnails/87356964-introduction-to-insurance1-121105111440-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)