This document provides an overview of convertible bonds, including:

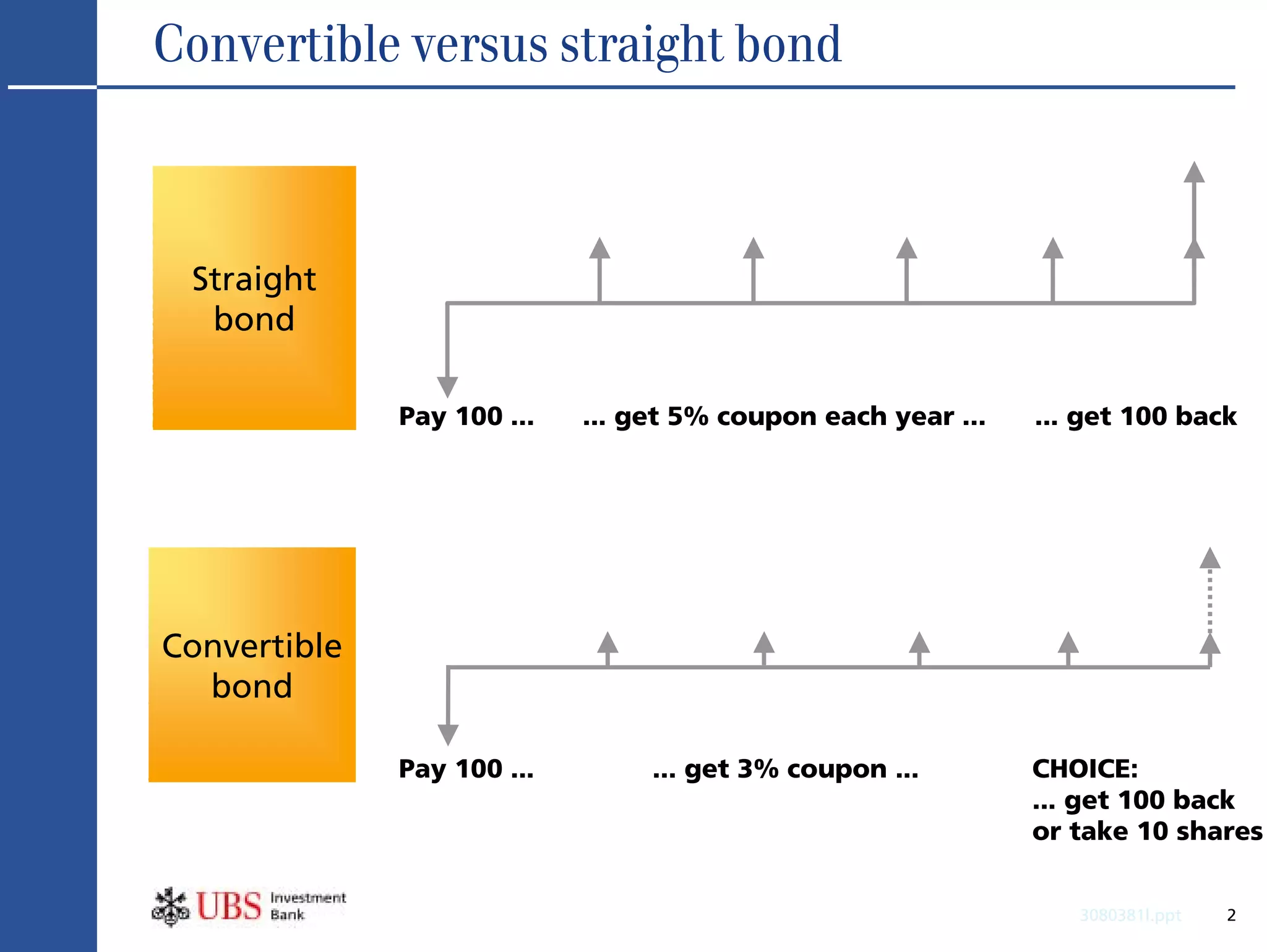

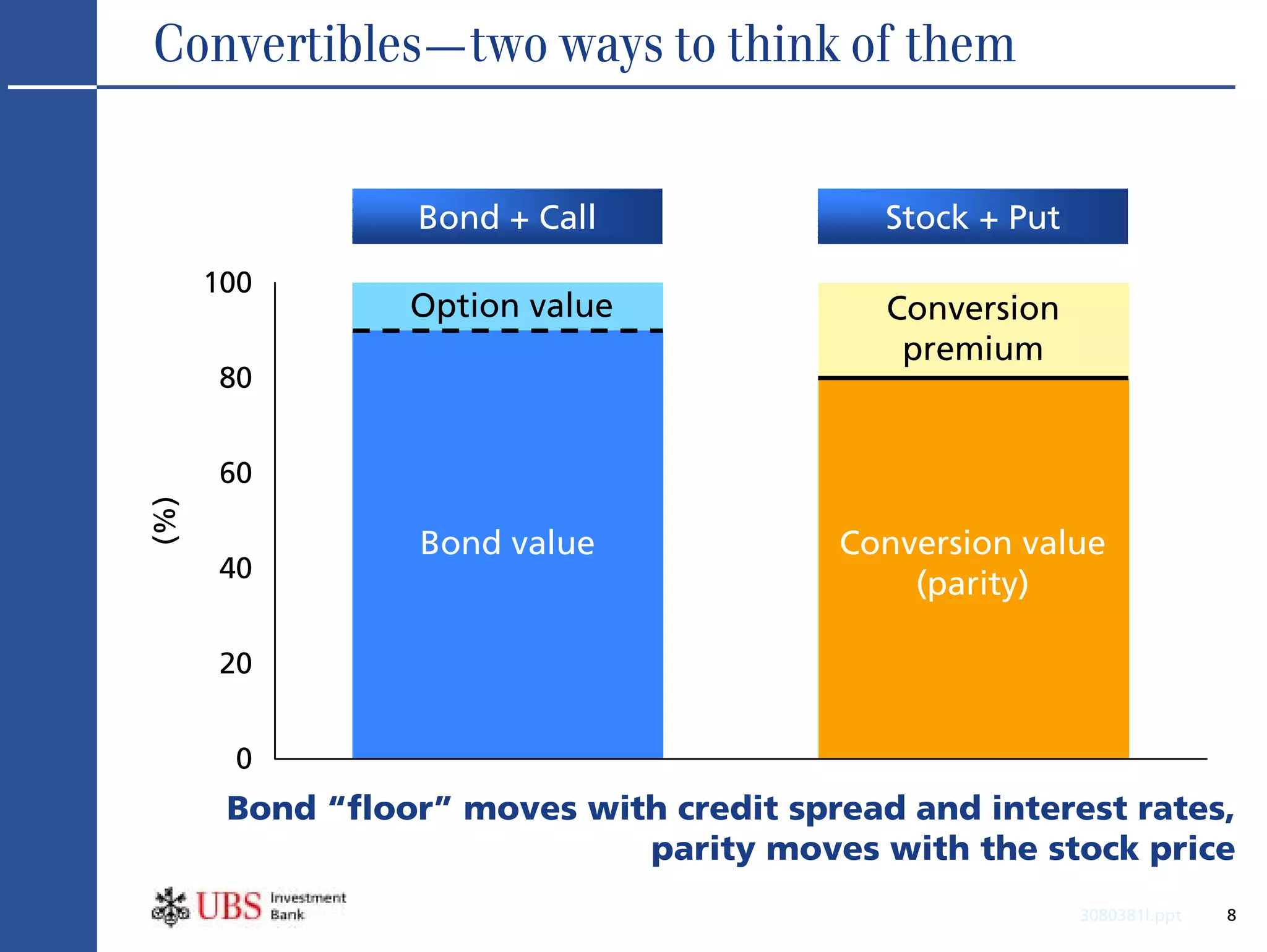

- Convertible bonds offer bond-like coupon payments but also allow conversion to equity, giving bondholders choice.

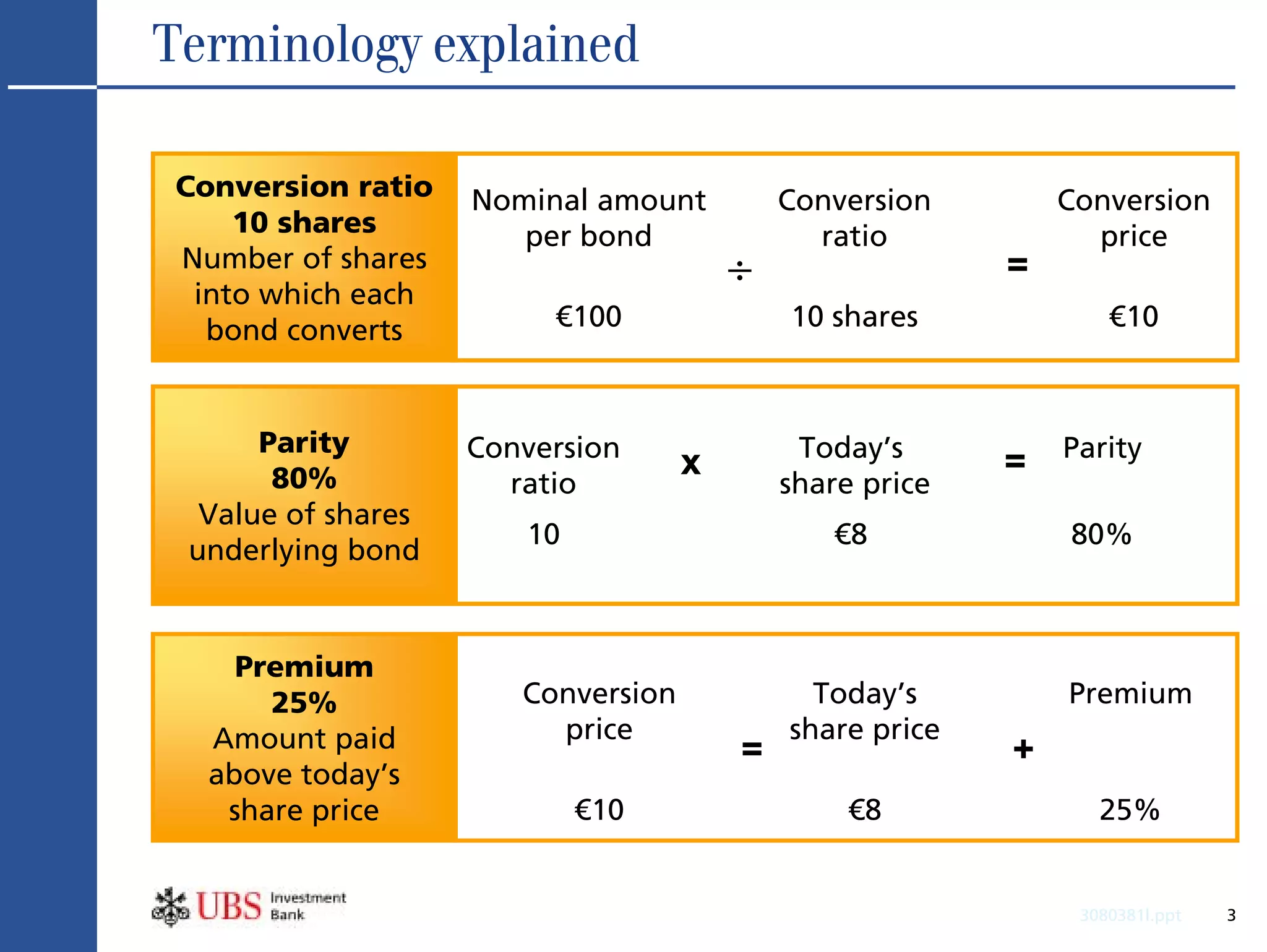

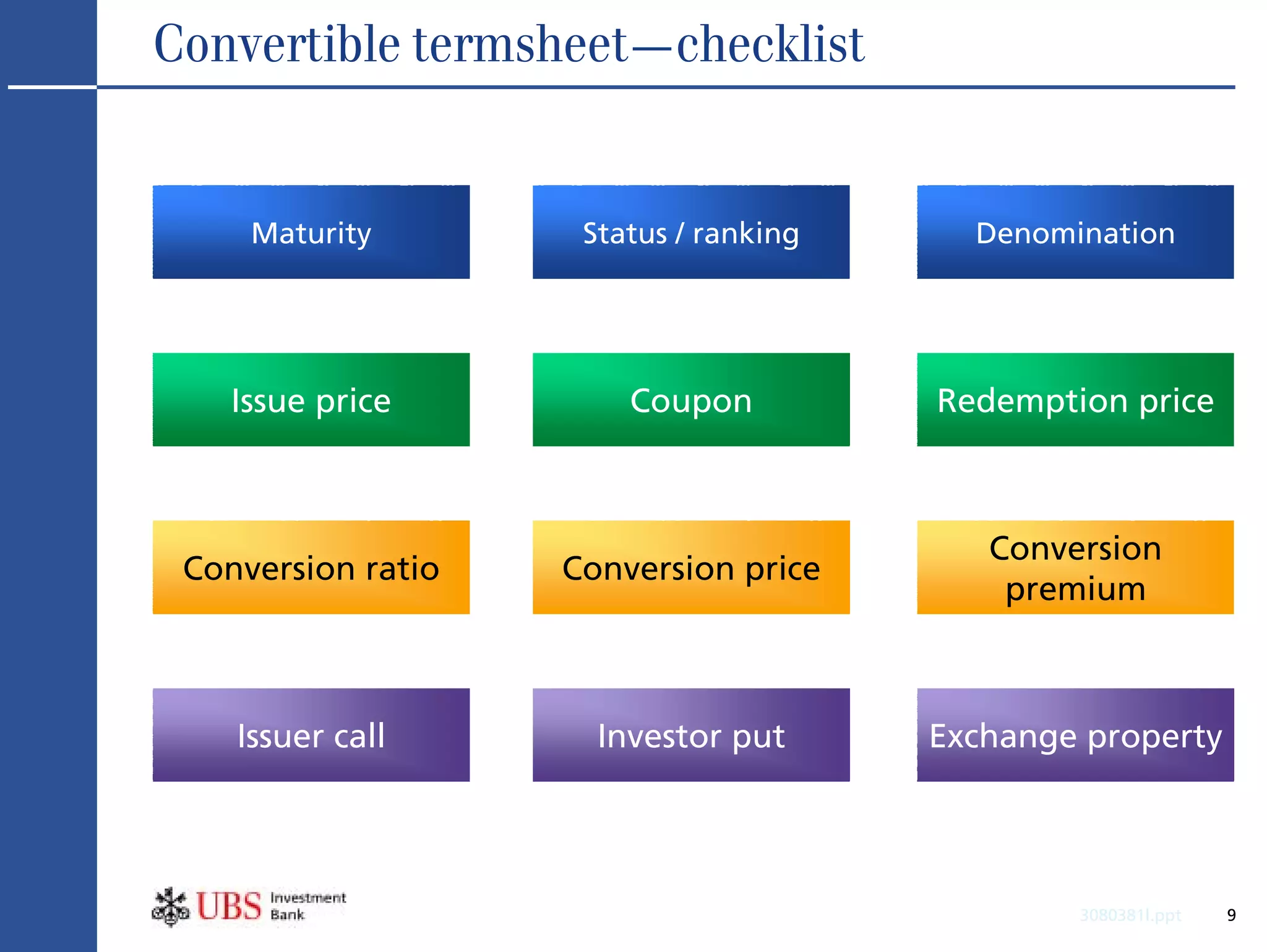

- Terminology around conversion ratios, prices, and premiums is explained.

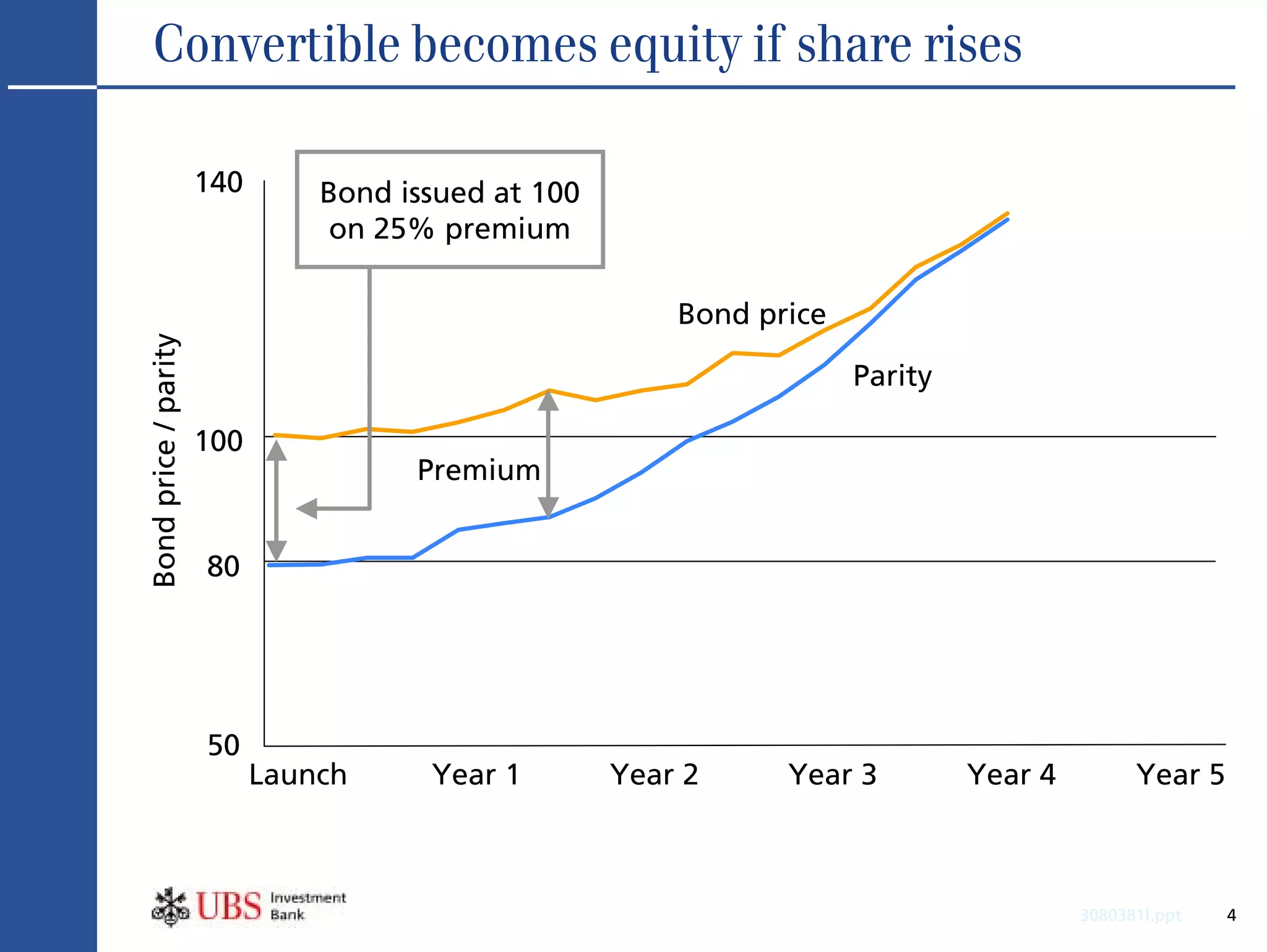

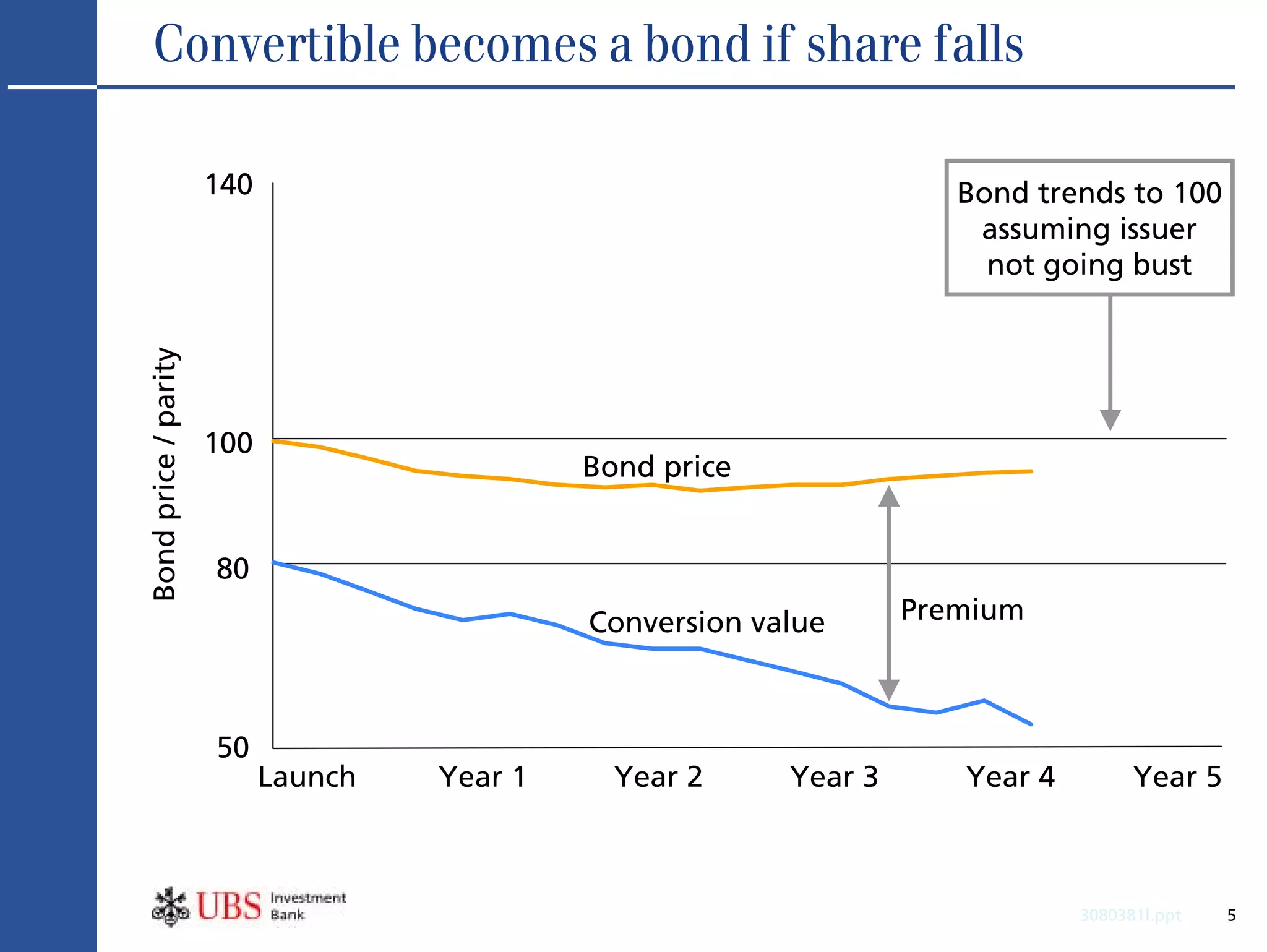

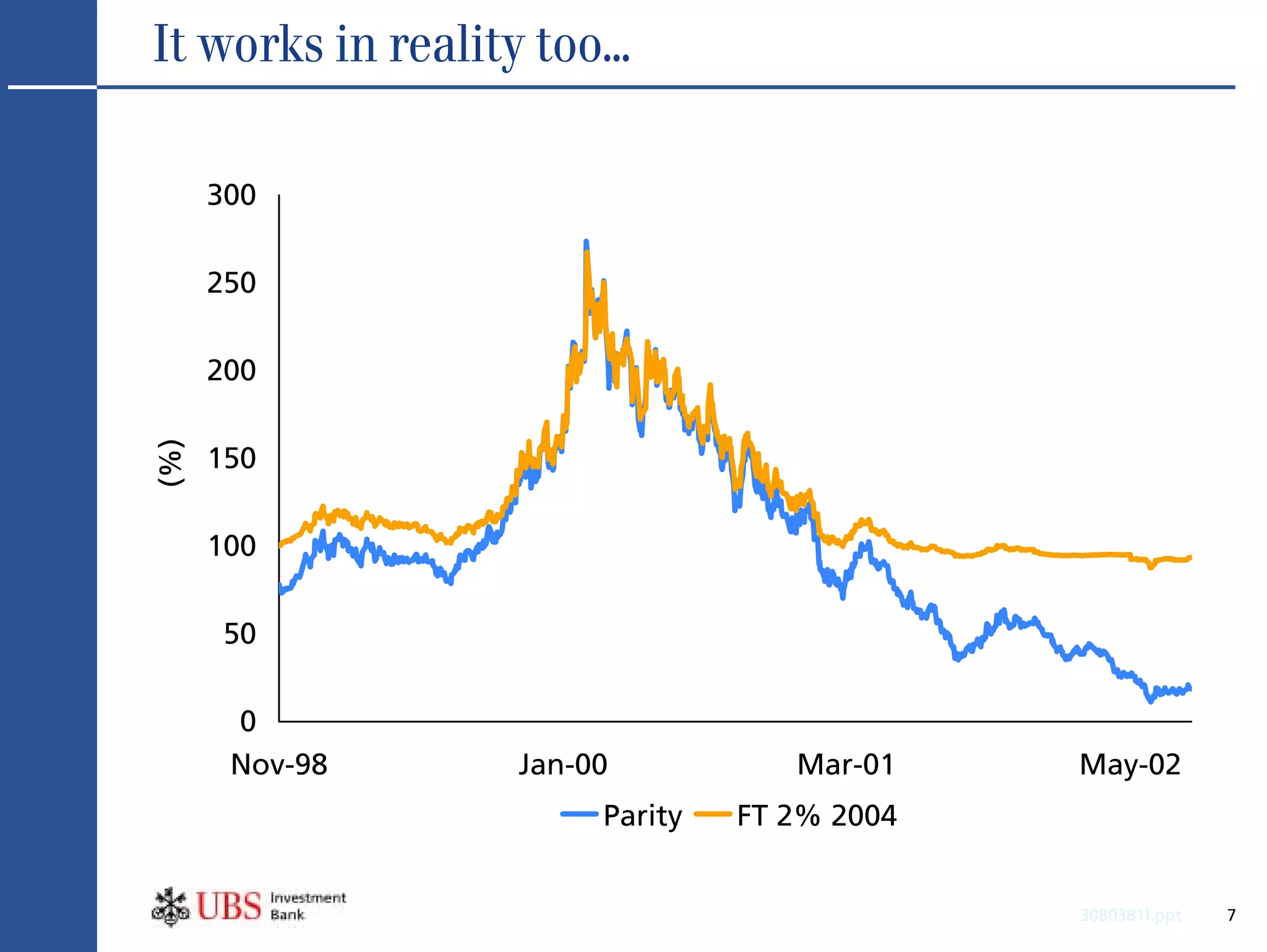

- Convertible bonds take on characteristics of bonds or equities depending on whether the underlying share price rises or falls.

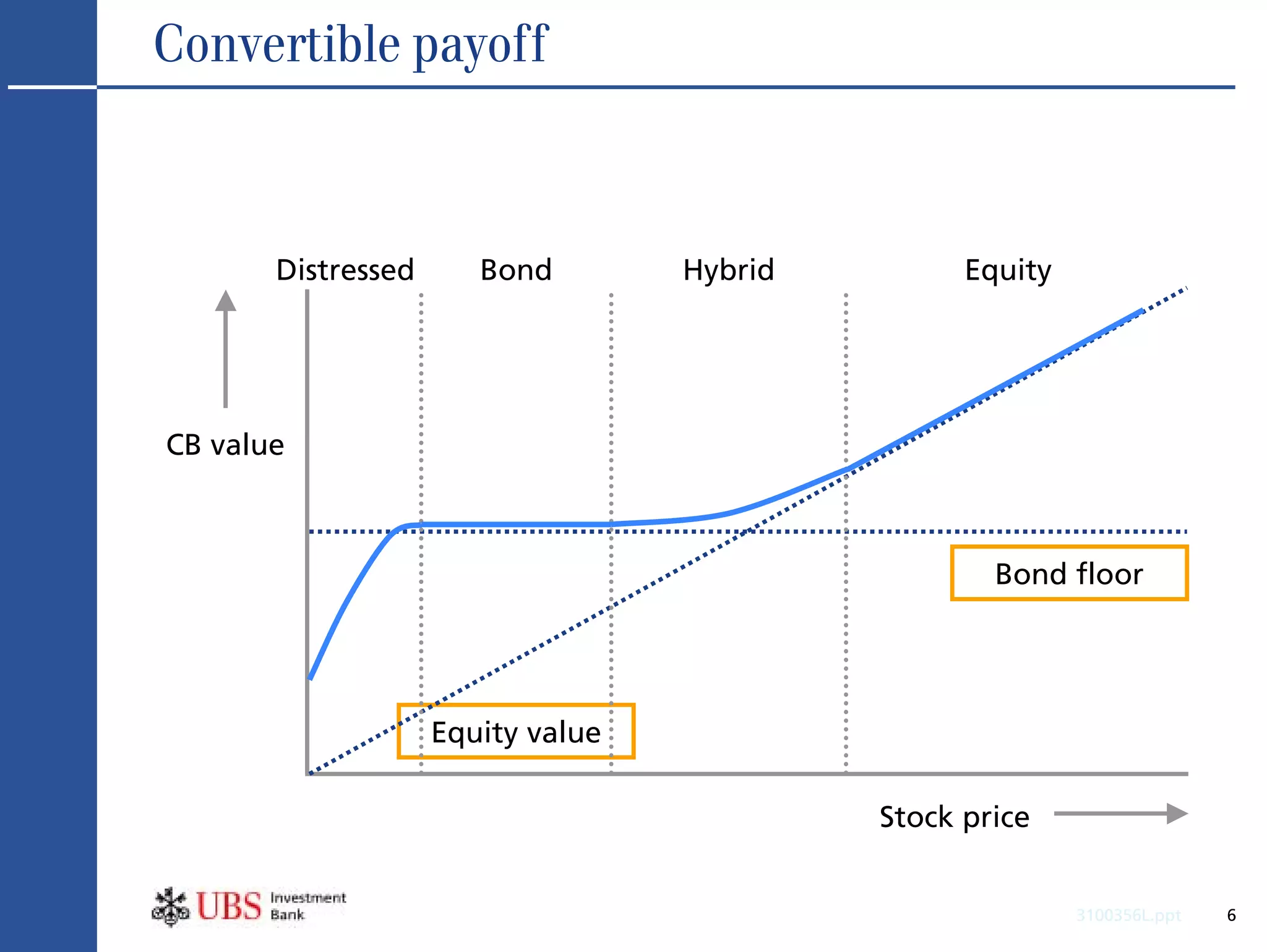

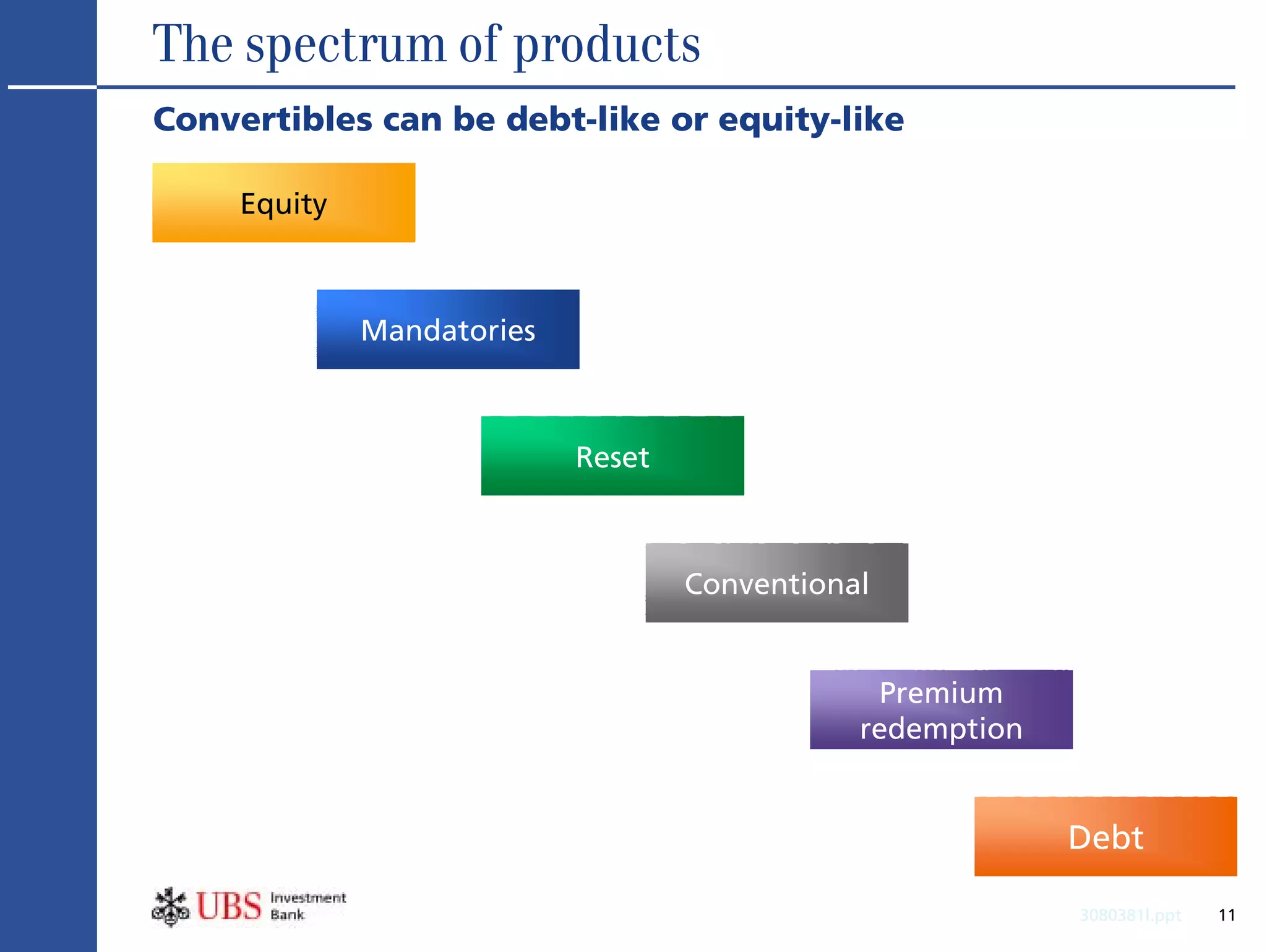

- Various convertible bond structures are discussed, ranging from equity-like to debt-like.

![Correlation[1]](https://cdn.slidesharecdn.com/ss_thumbnails/correlation1-090915084422-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)