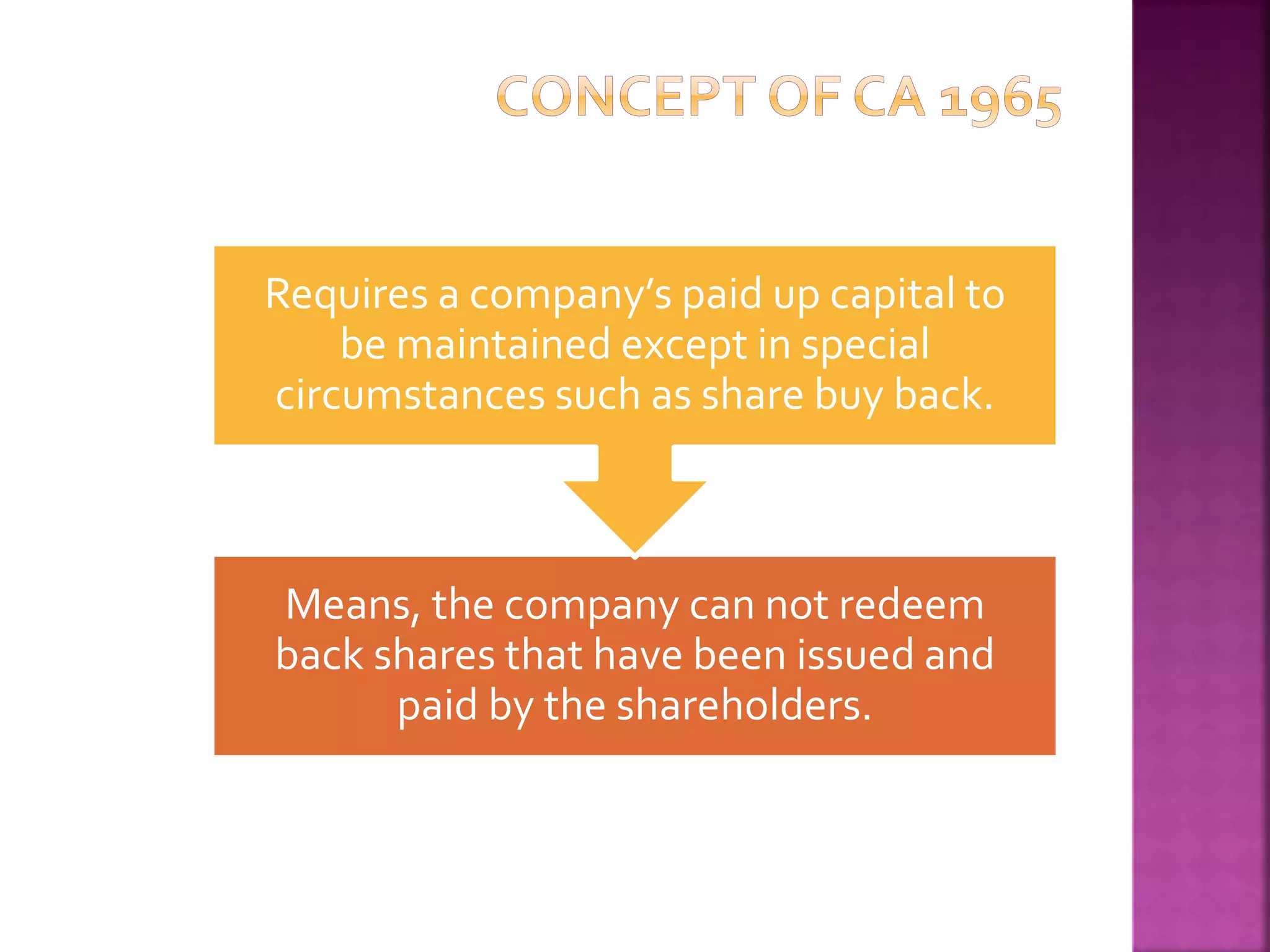

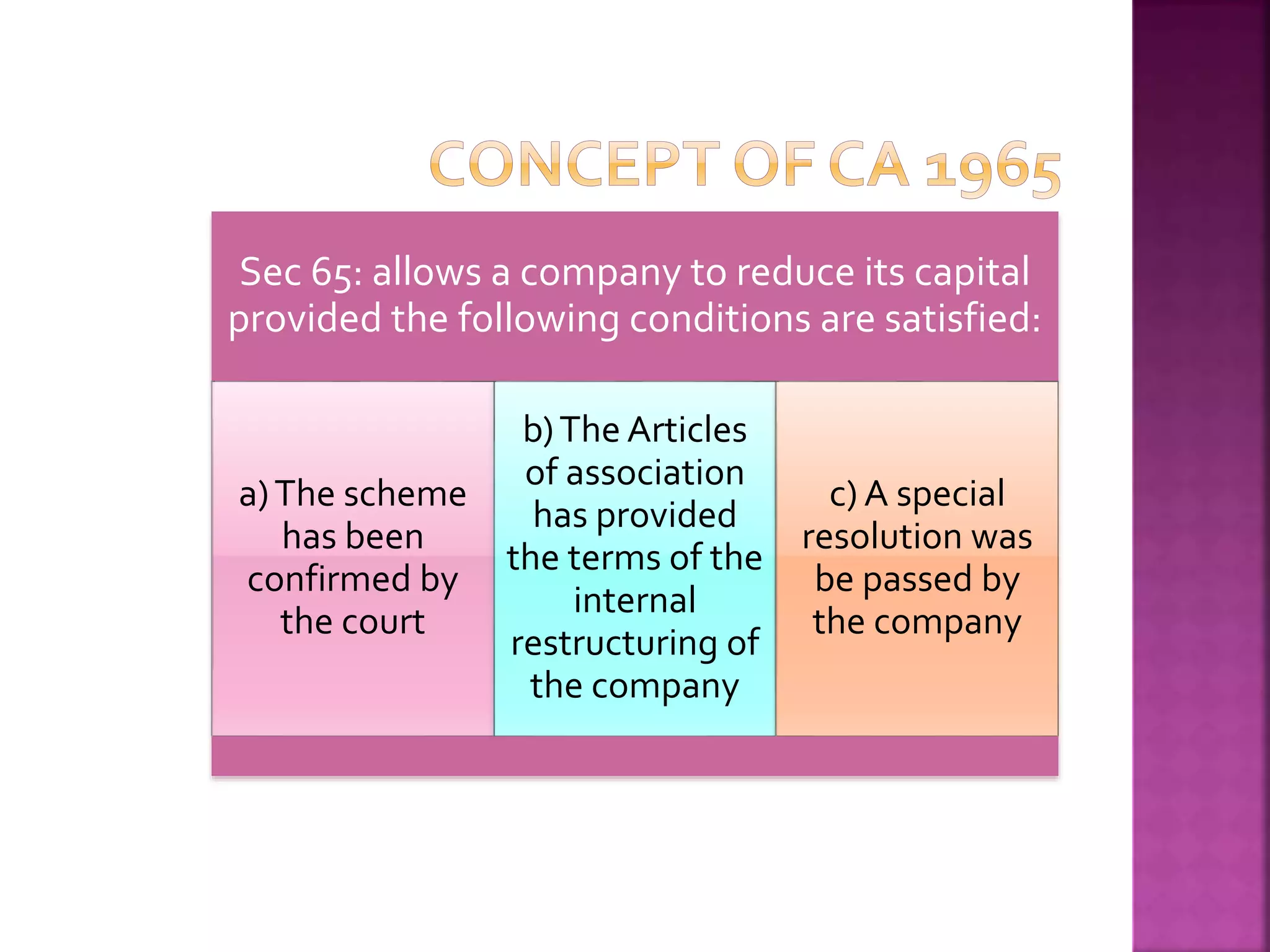

The document outlines procedures related to company reconstruction and capital structure changes, emphasizing accurate accounting practices and financial statement preparations. It details the statutory framework for capital reduction, including conditions under which a company can reduce its capital, manage accumulated losses, and address creditors' rights. Additionally, it discusses the necessary entries for accounting treatment during the internal restructuring process and how to equitably handle the claims of affected parties.