RSA Conference Exhibitor List 2024 - Exhibitors Data

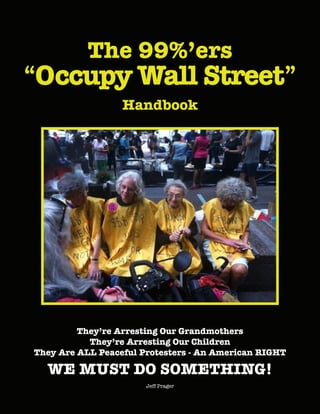

Occupy handbook

1. The 99%’ers

“Occupy Wall Street”

Handbook

They’re Arresting Our Grandmothers

They’re Arresting Our Children

They Are ALL Peaceful Protesters - An American RIGHT

WE MUST DO SOMETHING!

Jeff Prager

3. One Of These Two Girls Who Were

PROVEN To Have Been Pepper

Sprayed By A Psychopathic Thug With

A Badge And A Gun Was Born Deaf.

This Book Is For Her,

Wherever She May Be.

Speaking For ALL of Us, We Love Her.

SHE IS US.

The 99%.

4. If Not Now, WHEN?

When YOU are Homeless?

When YOU have NOTHING.

THEN, it will be too late!

If Not Now, WHEN?

7. These Are Just Some

Of The Men Responsible

For EVERYTHING Wrong

With This Country.

This IS A WAR On US.

Make No Mistake.

It’s called Class Warfare.

Of course we can add Obama, Geithner, Bernanke, Summers, Bush 1, Bush 2, Ru-

bin, Clinton and 100s of additional names from the Koch Brothers to Petraeus and

Panetta. We all know the names. There are many 100s. Add our worthless, self

serving criminal Congressional representatives and there are over a 1,000 key

people in positions of vast power that are controlling our lives and assuring that

the hired thugs with badges are arresting our sons and daughters, our parents

and grandparents, our mothers and fathers and you and me if we DARE to pro-

test. And it’s our Constitutional RIGHT to protest. This is ALL unacceptable. Fur-

ther, it’s criminal and I intend to relentlessly pursue justice by exposing the lies,

the fraud, the collusion, the crimes of vast proportions and I just won’t be silenced.

These men DO NOT give a shit about any of us. They laugh at us drinking Martinis

on their yachts, they muse over our stupidity while being served leg of lamb by their

servants on the porches of their mansions. Heck man, they don’t even pump gas, do

laundry, dust, vacuum, clean, shop for food or ANY of the mundane crap WE all have

to do. We have no choice and they have ALL of the choices. WE are the 99% and they

are the “less then 1%” of the global elite that screw us every day.

8. We Should Occupy

EVERY MAJOR CITY IN THE USA

But I Know Many Of Us Can’t.

So, What Can We Do?

This Book Will Tell You.

And The Strategy In This Book

WILL WORK!

9. Who Owns and Controls America? The Corporations, the Banks, the Pentagon

NOT YOU AND ME

10. Judges of the Ontario Court of Justice

Regional Judge for Toronto

Order Per: G20 Arrests

August 12, 2011

TORONTO — An Ontario Court judge has concluded that “zealous” police officers criminalized a

peaceful political protest that led to dozens of arrests during last year’s G20 summit.

In his 29-page judgment released Thursday, Justice Melvyn Green criticized police for their

“kettling” tactics used to corral protesters on June 26, 2010.

“The only organized or collective physical aggression at that location that evening was perpe-

trated by police each time they advanced on demonstrators,” he wrote.

Police tactics like those used during the G20 summit risks the “criminalization of dissent,” the

judge ruled.

“The zealous exercise of police arrest powers in the context of political demonstrations risks

distorting the necessary if delicate balance between law enforcement concerns for public safety

and order, on the one hand, and individual rights and freedoms, on the other.”

Link: http://www.canada.com/news/Judge+slams+police+tactics+arrest/5249418/story.

html#ixzz1ZKc63OR2

Wall Street’s Den of Thieves

If you follow the trail of deceit from Enron to its natural lair, it only leads to one destination:

Wall Street. Here’s why.

The first thing you learn on Wall Street: Earnings don’t mean anything. Everyone assumes that

earnings are financially engineered (sometimes downward!) to meet a variety of stakeholder

expectations. The key expectation -- the one that stakeholders want companies to meet -- is

steady growth. Earnings that spike and swoon set off alarm bells at places like Fidelity. Steady

growth makes fund managers feel calm and content.

That’s exactly what big companies -- such as General Electric, IBM, Wal-Mart, and, for a time,

Enron -- deliver. Go back and read the quarterly reports of those companies over the past few

years, and you’ll feel as if you’ve taken Valium, so steady and predictable is the metronome of

their results.

The Arrests

While this is a Canadian ruling it has just as much to do with what’s happening in America to-

day and in New York City specifically as Mom and Apple Pie, as you’ll soon see.

The second thing you learn on Wall Street has to do with the length of the auditor’s letter and

the number of footnotes included. Simply put, shorter and fewer is better than longer and more.

If the auditor’s letter is a paragraph long, go directly to the footnotes. If the auditor’s letter is

two paragraphs long, read the footnotes carefully. If the auditor’s letter is four paragraphs long,

all hands on deck and hedge your position. For the record, Enron’s auditors wrote long letters

that had a lot of footnotes.

The third thing you learn on Wall Street is that cash flow and sales are really what matter

(since earnings can be engineered). If a company is booking revenue and its cash flow is strong,

then it has flexibility. And if the company is well managed -- if the people in charge know what

they’re doing -- then it’s probably worth more tomorrow than it is today. That makes it a buy if

it’s a stock or a bond. During the run-up years from 1996 to 2000, Enron appeared to be all that

and more.

The fourth thing you learn

on Wall Street -- and this

one is what they call a “job

ender” or a “job keeper” -

- is that one hand washes

the other. If the firm that

you work for happens to do

a lot of other business with

a firm that you’ve been as-

signed to cover, you do not

ever forget that there is no

“I” in “team.” You are on the

team, and you will do what’s

right for the team. If you

don’t, well, don’t kid your-

self: No one is irreplaceable.

That’s why Enron was always a strong buy with all of those firms that did business with the

company. Even as the stock sank like a stone during the spring, summer, and fall of 2001, ENE

was always a buy or a strong buy. There’s no one on Wall Street who doesn’t understand that

one hand washes the other.

After the music stopped and the stock tanked and Enron collapsed into bankruptcy, everyone

on Wall Street pretended to be absolutely shocked that such a thing could happen. Happily

enough, the more excitable members of the press and their allies in the Democratic Party saw

Enron’s collapse as a huge opportunity to rebrand President George W. Bush and his Republi-

can friends as the running dogs of dastardly corporate interests. Enron CEO Kenneth Lay, ex-

CEO Jeffrey Skilling, and ex-CFO Andrew Fastow were all quickly sketched as Dr. Evils, and the

games (known in Washington as congressional hearings) began.

The hearings, of course, have been a joke. Andersen’s hapless David Duncan, former lead auditor

for Enron, was the first sacrificial offering. Next up was Skilling, who declined to take the Fifth

Amendment. Skilling’s lack of contrition discombobulated hearing members, causing them to

embark on great flights of rhetoric in which they denounced the perfidy and the heinousness of

the whole affair. Next came Lay, who did take the Fifth, thus enabling various senators to slap

him around at will. On and on it went, each hearing dumber and more irrelevant than the next.

The net result was disgust -- shared equally between Enron and the members.

11. Sensing that the Enron scandal was not playing out as they had hoped, the members directed

their attention toward Wall Street, and a shower of subpoenas rained. Wall Street’s response

(figuratively speaking) was, “Go ahead. Make my day.” After all, Wall Street is the mother lode

of political fund-raising, and 2002 is an election year. The congressional subpoenas were fishing

lines with no bait and no hook. The exercise had everything to do with headlines and nothing

to do with substance.

And for good reason. Because at the core of Enron’s collapse is the fact that virtually everything

the company did was legal. Accounting and financial engineering obey rules -- not laws, morals,

or notions of right and wrong. If Andersen, Ernst

& Young, and PricewaterhouseCoopers operate

within the rules of accounting as outlined by the

FASB and the SEC, then it doesn’t matter if the

company that they’re auditing covers up debt,

misstates earnings, or misleads investors. Tough

luck. The rules were obeyed. If accounting regu-

lations don’t specifically say, “Do not create an

offshore SPE collateralized by company stock to

keep debt off the company’s balance sheet,” then

all the $600-per-hour brainpower that money can

buy will find a way to do it. And it will be legal.

G20 rioters to hang

banker effigies

from lampposts as

city staff are

told to wear disguises

City workers are being urged to stay at home or

to dress down during next week’s G20 summit

to avoid being targeted by anti-capitalist protest-

ers.

Unprecedented measures are being put in place to

prepare for thousands of demonstrators targeting

the City and Canary Wharf.

About 3,000 anti-capitalist protesters are expected,

with groups next Wednesday marching to the Bank of England, holding ‘flashcamps’ outside

the European Climate Exchange in Bishopsgate, and marching on the US Embassy.

Demonstrators have vowed to hang effigies of bankers from lampposts along the protest route.

City workers have been warned not to wear suits, but to ‘dress down’ in chinos and loafers be-

cause they would be obvious targets.

Banks have been warned to take extra security precautions to protect their staff after vandals

attacked former RBS chief Sir Fred Goodwin’s Edinburgh home.

Security specialists at Kroll, the risk consultancy, said high profile bankers were ‘easy tar-

gets’. Companies linked to the financial crisis are taking extra security measures for prominent

staff.

An extra 2,500 police, including riot units and intelligence officers, are being deployed at a cost

of £10million to tackle any violence, while security consultants are giving firms constant up-

dates on threat levels.

The demonstrations, as 20 world leaders meet

at the ExCeL Centre in Docklands to discuss

how to end the world recession, are expected to

be the biggest in London this decade.

Demonstrators will target the ExCeL centre the

next day. Banks, insurers, accountancy firms

and brokerages have all circulated emails to

staff with security instructions.

One warns: ‘The front door is to be permanently

locked during these two days.’

Royal Bank of Scotland Chief Executive Sir

Fred Goodwin

Face of the financial crisis: Sir Fred

TheLondonChamberofCommercehavewarned

businesses to take security precautions, includ-

ing making sure staff carry ID, keep movement

in and out of the offices to a minimum and can-

celling all but essential meetings.

Colin Stanbridge, chief executive of the LCCI,

said: ‘There will be concern among businesses

at the protests but the vast majority of firms will

have robust security arrangements in place.’

The financial advisory group Bluefin, which

employs 500 staff in London-has told employ-

ees not to go to its office in Mark Lane in the City unless absolutely necessary.

A spokesman for the bank UBS said: ‘We are telling people to be cautious. If you have client

meetings do you need to have them here?”

Chris Knight, professor of anthropology at the University of East London, is organising protests

under the banner G20 Meltdown.

Fred Goodwins Home • As you can see, Americans have no such designs. We’e peaceful

protesters exercising not necessarily our Constitutional rights but our inalienable rights

handed down by a higher power. But we don’t want to create havoc and destruction.

We want Justice and liberty from a corrupt and fraudulentg system.

12. He said: ‘We are going to be hanging a lot of people like Fred the Shred from lamp-

posts and I can only say let’s hope they are just effigies. If he winds us up any more

I’m afraid there will be real bankers hanging from lampposts.’ Meanwhile, the

group claiming responsibility for vandalising the former Royal Bank of Scotland

chairman’s home has threatened further action against ‘criminal’ bank bosses.

A statement claiming to be from the group responsible for damage at his £3million

mansion warned of further attacks, saying: ‘This is just the beginning.’

The threat sparked fears of a terror campaign against those blamed for the collapse

in the financial system.

Security adviser Dai Davies, a former head of Scotland Yard’s Royalty Protection

squad, said: ‘Risk assessments will have to be carried out by the police on individu-

als who are concerned about their safety. If there is cause for concern then appro-

priate advice will be given and pre put in place.

‘The developments at Sir Fred Goodwin’s home will almost certainly make some

other high-profile bankers want to review their own private security arrange-

ments.’

http://www.dailymail.co.uk/news/article-1164999/City-staff-told-wear-dress-dis-

guises-avoid-G20-demonstrator-threat.html#ixzz1ZLk62HHs

Wall

Street

Scene of

a multitude

of real crimes

13. The Modern Day Robber Barons

There are 1000s and we can’t cover them all ...

14. The Robber Barons of Wall Street

It was recently revealed that John Paulson , manager of the hedge fund Paulson & Co., had a personal income of

$5 billion in 2010. While millions of Americans were struggling to survive, this man was raking in $155.55 per

second, 24 hours a day, every day of the year.

Although his hedge fund colleagues haven’t yet revealed their 2010 income, we know that the top 25 hedge fund

managers made an average of $1 billion in 2009. The poor performer at the bottom of this group took home only a

paltry $325 million. Through their special relationships with our elected representatives (i.e., campaign contribu-

tions), these hard-working executives also get a special tax break, paying only a 15 percent tax on their income,

well below that of a typical clerical worker.

I have no problem with individuals making a lot of money

if they provide products and services that people want be-

cause that stimulates our economy and creates jobs. Even

the original reviled Robber Barons of the 19th century cre-

ated infrastructure (railroads), products (steel) and employ-

ment on the road to accumulating their enormous wealth.

On the other hand, our 21st century Robber Barons are mak-

ing their fortunes by skimming and leeching off our loosely

regulated financial system to the detriment of individual in-

vestors and pension funds. Their methods, although assur-

edly legal, push the envelope in ways that are not available

to individuals or smaller banks and investment firms.

They use highly leveraged speculation (a euphemism for

gambling) on commodities, currencies and markets to ma-

nipulate and distort the original intent of the hedging pro-

cess. They have at their disposal expensive banks of high-

speed computers that employ sophisticated mathematical

algorithms to prey on small differences in market prices in

order to realize massive profits in the blink of an eye. An-

other ploy is to take successful public companies private in

order to strip their assets, after which they sell off the strug-

gling and heavily indebted remnants.

All of these activities are designed to extract short-term

profits at the expense of individuals and companies who are

staying the course hoping for long-term investment growth.

They will proclaim that their role is to “make the market more efficient,” but it’s hard to understand why this ef-

ficiency involves siphoning off billions of dollars out of our many pockets into a few of theirs.

Since hedge fund managers take 20 percent of the profits that their funds generate, the top 25 funds produced

profits of at least $125 billion in 2009, and you can bet the booty will be much higher in 2010 and 2011.

We are a collective bunch of saps if we allow this pillage to continue. As a people, we should be outraged at the

unconscionable level of compensation delivered to financial executives across the board. Just what are they con-

tributing to our society and economy that justifies these outsized rewards? In fact, as demonstrated in the recent fi-

nancial meltdown, one can make the case that they are undermining our economic system rather than enabling it.

Overall, I’m in favor of reducing taxes and regulations, especially on small businesses. However, I’d like us to

move in the opposite direction with respect to Wall Street firms. At the very least we should be asking our sena-

tors and congressmen why hedge fund mangers deserve a 15 percent tax bracket when anyone else making over

$373,000 in taxable income is taxed at 35 percent. If they had paid income tax at the top rate in 2009, they would

have contributed an additional $5 billion toward deficit reduction. I suspect that they could have come up with the

additional money without having to sacrifice too many jets, yachts or mansions.

But we need to go much further than that. We should be heavily regulating the financial sector to curb high-lever-

age risk taking and high-speed algorithmic trading. We also need to introduce additional tax brackets directed

at these ludicrously high incomes so that we can recoup

some of their ill-gotten gains for the public good. Unfor-

tunately, our elected officials are already in the pocket of

the financial industry’s well-funded lobbyists; they have

watered down proposed financial regulations and backed

off on eliminating the hedge fund managers’tax loophole.

Incredible as it may seem, our representatives are now

proposing to deregulate Wall Street once more. And we

know where that will lead.

Reining in the financial sector should be something that

appeals to people across a wide political spectrum, and

yet there seems to be a collective passive response to these

excesses. We need to stand up and express our outrage to

our government officials in no uncertain terms and hold

their feet to the fire until corrective actions are taken.

It’s time to pick up our

pitchforks and torches

It is always good to take a look at history because it gives

us insight into the present. It is important not to forget,

especially since today, we are faced with a similar strug-

gle. Essence Restored says, “Since the 1980’s with the

election of Ronald Reagan the country has gone further

and further in favor of business leaders and the wealthy

and taken away more and more rights, opportunities, and

wealth from the middle and lower classes. In fact, the in-

come disparity now is the greatest it has been since the 1920’s.

Perhaps, it is time for another age of progressive and labor movements. Those in power will listen if enough

people rise up against the greed that has come to define our system. It is time to quit buying into the lies, fears, and

false promises of those seeking to enrich their own wealth. Let us follow the path of history and limit the power

and strength of the modern day robber barons.”

But will we? What is so disturbing to me is that we have the information, yet we are allowing history to repeat

itself. We will complain to each other, but we won’t do anything. I’m going to show some modern day robber

barons and give the links to read more about each. My intent is to inform, educate, and hopefully open eyes in the

hope that ‘we the people’ finally rise up and say “enough “!

The Koch Brothers

15. The Kochs And Their Weapons Of Mass Distraction

Capitol Hill - “When it comes to assault on American freedoms, few terrorists — if any — are more dangerous

than Charles and David Koch — the energy magnates who use their checkbooks as weapons of mass distraction

to finance threats against Democracy.” http://www.capitolhillblue.com/node/40038

Countrywide’s Many ‘Friends’

Two U.S. senators, two former Cabinet members, and a former ambassador to the United Nations received loans

from Countrywide Financial through a little-known program that waived points, lender fees, and company bor-

rowing rules for prominent people.

Senators Christopher Dodd, Democrat from Connecticut and chairman of the Banking Committee, and Kent

Conrad, Democrat from North Dakota, chairman of the Budget Committee and a member of the Finance Com-

mittee, refinanced properties through Countrywide’s “V.I.P.” program in 2003 and 2004, according to company

documents and emails and a former employee familiar with the loans.

http://www.portfolio.com/news-markets/top-5/2008/06/12/Countrywide-Loan-Scandal/index.html

Hedgie John Paulson, 21st Century Robber Baron?

International Political Economy Zone - “Like the robber barons of yore, John Paulson has made an outrageous

fortune – in his case by taking out credit default swaps against issuers of subprime mortgages. The $15 billion he

netted has been called The Greatest Trade Ever .” http://ipezone.

blogspot.com/2011/02/hedgie-john-paulson-21st-century-rob-

ber.html

Robber Baron Redux

http://www.portfolio.com/interactive-features/2007/05/moguls

The Big Oil Company Execs

Oil executives – aka robber barons – at right, BPAmerica Chair-

man Robert Malone; Shell Oil President John Hofmeister (not

pictured); Chevron Vice Chairman Peter Robertson (not pic-

tured); ConocoPhillips Executive Vice President John Lowe (not

pictured); and ExxonMobile Senior Vice President J. Stephen

Simon (second from left at top right), are sworn in on Capitol

Hill.

http://www.msnbc.msn.com/id/24757944/ns/business-oil_and_

energy/t/oil-execs-defend-huge-profits-senate/

In Conclusion

These are just a few of the modern day robber barons. They are

not doing anything that hasn’t been done before. The question

is, are ‘we the people’ ever going to do anything to change the

plight of the average American, or just continue to whine and

be victims. When do we stop taking what any politician says

at face value? When do we start researching how they actually

vote on important issues, rather than believe what they say in

a campaign speech? When do we start asking some hard ques-

tions, and demand truthful answers? When do we stop putting

them in office? When do we hold them accountable? Robber

barons are essentially bullies, and I was taught there is only one

way to handle a bully.

16. Twice a year, the billionaire industrialist brothers Charles and David Koch host

secretive retreats for an exclusive list of corporate America’s rich and powerful to

strategize and raise money for their right-wing political agenda.

At Center Right Is One Of

Charles Koch’s 7 Homes

Mother Jones obtained exclusive audio recordings that shed some light on the

brothers’ latest retreat, held at a resort near Vail, Colorado, in late June.

In a speech that is part of these recordings, Charles Koch thanks donors who gave

more than $1 million to the cause. We checked the audio against a list of partici-

pants at the Kochs’2010 seminar in Aspen that was obtained by ThinkProgress.org

and did additional research on these individuals. Below are the names Koch read

that appeared on the previous guest list.

John Childs

Childs is the founder and CEO of private equity firm JW Childs Associates. In

2006, Boston Magazine placed the “notoriously media-shy” magnate—a.k.a. “the

Republican ATM”—among the city’s wealthiest residents, reportedly worth $1.2

billion. Childs donated $750,000 to outside political expenditure groups in 2010.

He’s also been involved in Floridawetlands conservation efforts.

The Cortopassis

Dean “Dino” Cortopassi and his wife, Joan, hail from Stockton, California.This ar-

ticle, which identifies the pair as philanthroposts, calls Dino a “wealthy self-made

agribusinessman who is Stocktonian of the Year for 2005.” He is suing the state of

California for its failure to dredge streams in the Sacramento-San Joaquin Delta.

Joe Craft

Joseph Craft is president, CEO, and chairman of Alliance Resource Partners, a coal company based in Tulsa,

Oklahoma, that gave $2.4 million to outside political expenditure groups in 2010. His family is reportedly worth

$1.9 billion.

The DeVoses

Rich and Helen DeVos hail from Michigan. The cofounder of Amway and owner of the NBA’s Orlando Magic,

Rich DeVos is reportedly worth in the ballpark of $4.2 billion. The Richard and Helen DeVos Foundation funds

conservative Christian groups such as Focus on the Family. The DeVoses are big enough political donors to have

their own profile at OpenSecrets.org.

The Farmers

Dick Farmer is from Ohio. The founder and former CEO of the Cintas Corporation, his story is literally rags-to-

riches: He turned his father’s Depression-era rag-cleaning business into a $3.5 billion enterprise. Farmer and his

wife, Joyce, are longtime Republican boosters; during the 2002 election cycle the couple gave about $1 million

to the party.

The Friesses

Foster Friess founded the investment firm Friess Associates in 1974 with his wife, Lynn; in 2001, he sold a major-

ity share for $247 million. Friess is a champion of conservative Christian causes and one of Wyoming’s richest

men. His son, Steve Friess, helps him run the family’s philanthropic foundation. (Steve’s wife, Polly, was also on

the list of Aspen Koch participants.)

17. The Fullinwiders

Jerry and Leah Fullinwider hail from Dallas. Jerry has pursued oil exploration and development in the United

States, Canada, and Russia. He now serves under Ross Perot’s son as vice chairman of Hillwood International En-

ergy, which has operations in Iraq and Jordan as well as the United States and Russia. He also has ties to Hilarion

Alfeyev, an anti-abortion Russian Orthodox bishop.

The Gilliams

Richard Gilliam and wife, Leslie, are natives of southwest Virgin-

ia. Richardfounded the Cumberland Resources Corporation, which

was one of the nation’s largest private coal mining companies when

Massey Energy bought it for nearly $1 billion in March 2010. He’s

now a director with the Vancouver-based mining corporation En-

durance Gold.

The Griffins

Ken and Anne Dias Griffin are a hedge fund power couple from

Chicago whowed in 2003. Ken is the founder and CEO of Cita-

del and is reportedly worth $2.3 billion. Anne founded one of the

nation’s largest woman-run hedge funds, Aragon Global Manage-

ment. Ken bundled money for both President Barack Obama and

Sen. John McCain during the 2008 election.

The Haworths

Richard “Dick” Haworth is the former CEO and chairman emeritus

of Haworth, an international office-interiors manufacturer based

in Holland, Michigan, that he took over from his father in 1975.

The company reported sales of $1.4 billion in 2005, the year he

retired. He is married to Ethie Haworth and has donated more than

$100,000 to Republican causes, according to OpenSecrets.org.

Diane Hendricks

Hendricks is the billionaire former head of the ABC Supply roofing company, which she took over from her hus-

band Kenneth after he died in a construction site accident in 2007. Reportedly worth $2.2 billion, she is therichest

businesswoman in Wisconsin and a big Republican Party donor. She recently gave her state’s embattled Republi-

can governor, Scott Walker,$10,000 in advance of a potential recall vote next year.

The Humphreys family

Ethelmae Humphreys is the chair of the board of Tamko Building Products, one of the country’s largest indepen-

dent roofing manufacturers. She also serves on the board of directors of the Cato Institute, a Koch-funded think

tank. Her son David is Tamko’s CEO. The two have doled out hundreds of thousands of dollars to Republican

candidates. That includes David’s $25,000 donation to the successful recount effort this year of conservative Wis-

consin Supreme Court Justice David Prosser, who came under fire recently for allegations that he choked a fellow

justice. (He wasn’t charged.)

The Levys

Kenneth Levy of Mountain Lakes, New Jersey, cofounded the Jacobs Levy equity management firm and has

donated about $85,000 to conservative causes, according to FEC records. His wife, Frayda Levin, is a nation-

al director at the Koch brothers’ advocacy group Americans for

Prosperity and sits on the board of the Club for Growth. She also

cofounded the Motion Picture Institute, which “promotes liberty

through film,” according to her AFP bio. FEC records show that

she has given well over $100,000 to conservative causes.

The Marshall family

Elaine Marshall of Dallas is the widow of E. Pierce Marshall, a

son of oil tycoon J. Howard Marshall who served on the board of

Koch Industries before his death. Elaine was involved in a suc-

cessful effort to prevent the late Playboy Playmate Anna Nicole

Smith, who married Howard when he was 89, from inheriting the

family’s wealth. Before Smith’s death, she was investigated by the

FBI but never prosecuted in a murder-for-hire plot against Pierce.

In the end, Pierce inherited the bulk of his father’s wealth because

he and his father had previously helped Charles and David Koch

thwart a takeover of Koch Industries; Howard’s eldest son—also

named Howard—sided against his father and was disinherited as

a result. Meanwhile, Elaine’s son, E. Pierce Marshall Jr., is se-

nior vice president and general counsel at oil exploration company

MarOpCo.Another son, Preston Marshall of Houston, is the presi-

dent of MarOpCo.

The Popes

Art Pope is a millionaire Republican booster from Raleigh, North

Carolina, who inherited his retail fortune from a family business.

According to this article, he’s “one of the most trusted members of the

Koch’s elite circle” and a regular at the Kochs’ secret seminars, as well as a “valuable junior partner in many key

Koch operations.” He’s another national director at Americans for Prosperity and is married to Kathy Pope.

The Robertsons

Corbin Robertson is CEO and chairman of the board of Natural Resource Partners, a Houston-based fossil fuels

company. He’s also been involved with a number of other energy organizations and was listed as the richest US

small-business owner in 2007 byCNNMoney. He and wife Barbara have donated to the Baylor College of Medi-

cine and both Democratic and Republican politicians.

Ethelmae Humphreys and Vernon Smith at the IFREE Gala Evening

18. Karen Wright

Wright is the founder and CEO of the Ariel Foundation, a private philanthropy group based in Mount Vernon,

Ohio. She’s also CEO of the Ariel Corporation, a natural-gas compression company, and on the American Pe-

troleum Institute’s board of directors. She has donated more than $100,000 to Republican causes, according to

OpenSecrets.org.

Tom Rastin

Rastin shares a Mount Vernon, Ohio, address with Karen

Wright. He serves onthe board of directors at the Ariel Foun-

dation and is vice president of marketing and engineering at

the Ariel Corporation. Last year, he gave $2,400 to the failed

congressional campaign of former Democratic Louisiana

House Speaker Hunt Downer, who switched to the Republi-

can Party after endorsing the Bush-Cheney ticket in 2000.

Peter Smith

The principals with the Services Group of America: SGA is a

billion-dollar food services wholesaler; its CEO, Peter Smith

of Scottsdale, Arizona, appears on the list of 2010 Koch at-

tendees. Smith took over as CEO last year after its former

head, GOP heavyweightThomas J. Stewart, died in a heli-

copter crash. According to FEC records, Smith has donated

$12,500 to Republican congressional candidates. SGA’s po-

litical action committee donates heavily to Republicans.

The Camerons

Ron Cameron of Little Rock, Arkansas, runs agribusiness gi-

ant Mountaire Corporation, which generated $1.22 billion in

revenue in 2009. He has donated at least $175,000 to Repub-

licans in recent years, including $5,000 to Sarah Palin’s PAC,

according to FEC records. The company itself has given at

least $125,000 to outside spending groups over the past de-

cade, according to OpenSecrets.org.

The Hamms

Self-made magnate Harold Hamm of Oklahoma City is reportedly worth $8.2 billion. The son of sharecroppers,

Hamm soared up the corporate ladder from gas station attendant to CEO of “America’s Oil Champion,” Okla-

homa-based Continental Resources.According to OpenSecrets.org, he’s doled out more than $100,000 to political

causes and candidates, mostly Republican. Stricken with diabetes, he and wife Sue Ann founded a centerat the

Oklahoma University Health Sciences Center to help combat the disease.

The Haydens

Jerry and Marilyn Hayden of Barrington, Illinois, doled out $400,000 to conservative-leaning outside spending

groups in 2010 and about $250,000 to Republicans in 2008. Before retirement, Jerry ran Peacock Engineering, a

packaging company. As of September 2008, he served on the board of directors at the United Republican Fund

of Illinois. The Haydens recently donated $2.5 million toward an alumni center at their alma matter, Bradley

University.

Virginia James

James is an investor from New Jersey. She has donated hand-

somely to right-wing causes, including a $750,000 gift to

the Club for Growth in 2008 and another $350,000 last year.

This year, she donated $25,000 to the successful recount of

Wisconsin’s Justice Prosser.

The Menards

John Menard of Eau Claire, Wisconsin, is the founder of Me-

nards, the country’s third-largest hardware company. He’s

worth a reported $5.2 billion and has donated about $80,000

to his state’s Republican Party and federal candidates, mostly

Republicans, according to FEC records. His company backed

a recent anti-union program that was linked to the Kochs’

Americans for Prosperity and supported by Gov. Scott Walk-

er.

John Moran

Hailing from Palm Springs, Florida, Moran is the former

chairman of the Dyson-Kissner-Moran Corporation, an inter-

national holding company based in New York City. He also

chaired the Republican National Finance Committee from

1993 to 1995. Moran has given more than $900,000 to Re-

publican causes since 1991, according to OpenSecrets.org,

and he bundled between $250,000 and $500,000 more for

McCain’s 2008 presidential bid. In 1997, he warned that the

religious right was putting his party’s future “in jeopardy.”

The Schwabs

Charles Schwab of San Francisco is founder and chairman of the Charles Schwab Corporation, the country’s

largest independent brokerage firm. He is reportedly worth $4.7 billion. Since 1989, Schwab has donated more

than $1.6 million to political causes, mostly Republican, according toOpenSecrets.org. Part of that went to his

company’s lobbying arm, which has given away millions more.

They’re

Laughing

At Us Because

We’re Sheep

NOT ANY MORE!

Washington Weeps

19. Paul Singer

While Singer is not on the list of Aspen participants, the New York Times notedthat “Annie Dickerson, who also

runs a foundation for Paul Singer, a hedge fund executive who like the Kochs is active in promoting libertarian

causes,” showed up at that seminar. Singer founded the $17 billion hedge fund Elliott Management and recently

issued an economic manifesto slamming the Federal Reserve as a “group of inbred academics.”

The Templetons

John “Jack” Templeton Jr. and his wife, Josephine, of Pennsyl-

vania, gave $50,000 apiece to Wisconsin Justice Prosser’s re-

count effort this year. Jack has donated more than $1 million to

Republicans, according to state and federal records. He heads

the conservative John Templeton Foundation, which aims to

merge evangelical Christianity with “science” and “health.”

The foundation was started by Jack’s father, Sir John the mu-

tual fund billionaire, and in 2009 reportedly had $1.7 billion in

assets.

Exclusive: Inside the Koch

Brothers’ Secret Seminar

“We have Saddam Hussein,” declared billionaire industrialist

Charles Koch, apparently referring to President Barack Obama

as he welcomed hundreds of wealthy guests to the latest of

the secret fundraising and strategy seminars he and his brother

host twice a year. The 2012 elections, he warned, will be “the

mother of all wars.”

Charles Koch would probably not publicly compare the president

of the United States to a murderous dictator. (As a general rule, he and his brother don’t do much politicking or

speechifying in public at all.) But Mother Jones has obtained exclusive audio recordings from the Koch seminar,

a private event that took place in June at a resort near Vail, Colorado.

These unprecedented recordings provide a behind-the-scenes look at how the Koch brothers and their comrades

talk when they gather. They include a pair of keynote speeches and remarks by brothers Charles and David Koch,

who spell out their political aims and name some of the “great partners” who have contributed millions of dollars

to their causes. (The audio was provided by a source who approached the author after the event was over and was

not seeking compensation.)

Security was tight at the Ritz-Carlton Bachelor Gulch on opening night of the weekend conference, which drew

an estimated 300 guests. (Past attendees have included prominent politicians, right-wing media luminaries, corpo-

rate titans, and wealthy political donors.) Audio technicians even set up outward-pointing speakers around the pe-

rimeter of the outdoor dining pavilion, according to sources, emitting static to frustrate would-be eavesdroppers.

“There is anonymity that we can protect,” noted emcee “Kevin”—likely Kevin Gentry, a VP for the Charles G.

Koch Charitable Foundation—as he gently urged guests to open their wallets in support of the brothers’ causes.

Indeed, Charles Koch named 32 individuals and families who had donated more than $1 million over the previous

12 months, yet because of loopholes in federal campaign law, their donations do not exist in the public record.

Charles and David Koch are co-owners of Koch Industries, an energy and chemical conglomerate inherited from

their father that is currently America’s second-largest privately held company. To date, the brothers have spent

more than $100 million supporting hard-right political campaigns and institutions. They are key funders of the

movement to discredit climate science and sow doubt on the scientific consensus that human activities contribute

to global warming.

The Kochs have tried to keep everything about the seminars

secret: the content, identities of attendees and speakers—even

meeting locations and dates.

The Kochs also bankrolled the fledgling tea party by making

massive investments in right-wing political advocacy groups

such as Americans for Prosperity, as detailed by Jane Mayer in

The New Yorker last year. More generally, the brothers have

dedicated a portion of their vast wealth—and that of their bene-

factors—to influencing elections across the nation and swaying

public opinion on everything from health care and fracking to

labor policy and government spending.

The brothers have held their twice-yearly seminars since at

least 2003, endeavoring to keep almost everything about them

a secret—not just the content but also the identities of attend-

ees and speakers, and even the locations and dates. They’ve

succeeded until recently. Last October, a leaked invite for the

Kochs’ January 2011 seminar was first obtained and published

by the New York Times.* In response, groups including Com-

mon Cause and Greenpeace organized a massive protest out-

side the gates of the resort near Palm Springs where the gather-

ing was held.

According to an agenda (PDF) for an earlier Koch seminar

(Aspen, 2010) that accompanied the leaked invitation, previous Koch seminars have featured “such notable lead-

ers” as Rush Limbaugh and Glenn Beck, Sens. Jim DeMint (R-S.C.) and Tom Coburn (R-Okla.), and Reps. Paul

Ryan (R-Wis.) and Mike Pence (R-Ind.). Supreme Court Justices Antonin Scalia and Clarence Thomas also have

attended.

Several GOP governors made it to the Vail seminar in June, among them Florida’s Rick Scott, Virginia’s Robert

McDonnell, and White House hopeful Rick Perry of Texas. News of the event slipped out after McDonnell put

the trip on his weekend schedule; neither Perry nor Scott initially disclosed the trip to their constituents. A Perry

spokesman acknowledged his attendance only after the Austin American-Statesman tracked the tail number of a

plane belonging to one of the governor’s top donors from Texas to Colorado. He described the summit as a “pri-

vate gathering of business leaders.” Koch read off the million-dollar honor roll, a list of 32 donors who have made

seven-figure contributions to the brothers’ efforts.

During his welcoming remarks, Charles Koch warned his guests that the 2012 elections are nothing short of a

battle “for the life or death of this country.” He then acknowledged the individuals and families who had given

more than $1 million to the brothers’ efforts—though he misspoke, saying “more than a billion,” earning a huge

20. laugh from the crowd. “Well, I was thinking of Obama and

his billion-dollar campaign,” Koch said, to more laugh-

ter and cheers. “So I thought, ‘We gotta do better than

that.’” (Forbes pegs the brothers’ personal net worth at

around $22 billion apiece.)

Koch then proceeded to read off the million-dollar honor

roll, a list of 32 names that we have cross-checked against

the published list of 2010 attendees, as well as additional

sources. The list features many well-known GOP donors

including John Childs (JW Childs Associates), Rick and

Helen DeVos (Amway), Dick and Joyce Farmer (Cin-

tas), and Diane Hendricks (ABC Supply). MoJo’s Gavin

Aronsen breaks it all down in his post, “Exclusive: The

Koch Brothers’ Million-Dollar Donor Club.”

Concluding his reading of the list, Charles quipped that

there were “10 more [million-dollar donors] who will re-

main anonymous, including David and me... We’re very

humble... The plan is the next seminar I’m only reading

the names of the $10 million,” he added, to laughs from

the crowd.

Charles spoke again the next evening, following a key-

note speech by Fox News host and retired New Jersey

Superior Court Judge Andrew P. Napolitano. The judge

didn’t stray far from his usual libertarian fare; he was

met with hardy approval when he declared that the Sec-

ondAmendment was created to ensure “the right to shoot

at the government if it is taken over by tyrants.”

Among Napolitano’s other revelations: that he some-

times gets in “a little bit of trouble” from his employers

at Fox for being tough on Republicans; that Fox hired

him on the strength of his televised advice, during the

contentious 2000 Florida election contest, that the Bush-

Cheney campaign should take its case straight to the US

Supreme Court; that he views the PATRIOT Act as the

“the single most abominable, hateful, unconstitutional

piece of legislation [ever] enacted”; and that he believes

former Attorney General Alberto Gonzales undermined

the Constitution when he threatened to prosecute the

New York Times for exposing spying by the National

Security Agency.

Napolitano closed his address with a quote he misattrib-

uted to Thomas Jefferson**: “When the people fear the

government, there is tyranny. When the government fears

the people, there is liberty.”

At this point, Charles Koch returned to the podium. “We’ve

talked about our competitive disadvantage, how

we’re overwhelmed in a number of areas,” he said.

“One of those areas, of course, is the media—and

we’re overwhelmed. The media is 90-plus percent

against us. But we have a few bright stars, and Judge

here is one of ‘em.

“We are absolutely going to do our utmost to invest

this money wisely and get the best possible payoff

for you in the future of our country.”

“Now, we’ve opined on what you should do, and you

have to go execute. And I’m sure you’ll do a great

job,” Koch said. “We’ve had great discussions, great

arguers, I think great programs, great initiatives. And

lastbutnotleast,Iwanttothankallofyouwhostepped

forward so generously to support this as you’ve done

in the past. And I want to give all of you a big hand

for stepping forward to save our country.”

The crowd applauded it-

self

“We’ve had a lot of tough battles,” he continued.

“We’ve lost a lot over the years, and we’ve won some

recently. And I pledge to all of you who’ve stepped

forward and are partnering with us that we are abso-

lutely going to do our utmost to invest this money

wisely and get the best possible payoff for you in the

future of our country.”

But “it isn’t just your money we need,” Koch added.

“We need your energy. We need you bringing in new

partners, new people. We can’t do it alone. This group

can’t do it alone. We have to multiply ourselves. Just

as to change the media we just can’t have the judge.

We need to clone him thousands and thousands-fold.

“And so, thank you so much,” Koch said. “God bless

you, and God bless America.”

*Clarification: The original version of this article implied that

Lee Fang of ThinkProgress.org broke the news about the Koch’s

January 2011 seminar. Actually, the Times had it first, and de-

scribed the leaked Aspen agenda; Fang was the first to provide

a link to the document.

**Correction: The original version of this story missed this fact. A sharp-eyed commenter notes that Napolitano did not close his

address with a well-worn Thomas Jefferson quote, “he closed it with a well-worn John Basil Barnhill quote often misattributed to

Jefferson.”

22. The US Federal Reserve injected $500 billion into the US economic system between January and March 2011

The Goals Is Simple

The Strategy Even Easier

• STOP PARTICIPATING •

I’ll Explain

23. $14,639,239,567,874.38

The Fraud and Criminality

Of Fractional Reserve Banking

The US National Debt has increased an average of $2.27 billion per day since 2005 until 2008!

Now, due to the bailout of the rich bankers and world elite, the US National Debt is increasing

substantially faster!

The US trade deficit is on track to set a record for an eighth consecutive year, running at an an-

nual rate of $780 billion.

During fiscal year 2010/2011 the U.S. Treasury is on-track to pay upwards of $500 billion just

in interest payments to finance the already-existing debt.

Annual interest payments for individuals, households, businesses, and all levels of US govern-

ment are likely to reach $3 trillion — out of a $14 trillion annual GDP, an annual GDP that this

year will likely decline.

The debt limit was raised for the third time in less than a year with the passage of American

Recovery and Reinvestment Act of 2009 on February 13, 2009 (ARRA; H.R. 1).

Signed into law on February 17, 2009

(P.L. 111-5)

the debt limit was increased to $12.104 trillion

An end-of-session vote in December 2009 increased the debt ceiling by $290 billion set at

$12.394 trillion.

12 February 2010 Obama signed a law increasing the debt limit from $12.394 trillion to $14.294

trillion.

April 15, 2011 US stated debt exceeded present US law until August 1, 2011 when a stop-gap

measure of four hundred billion was passed by Congress biding new ‘Super-Congress’ legisla-

tion.

The Debt Subject to Limit is the maximum amount of money the Government is allowed to

borrow without receiving additional authority from Congress. The current statutory limit is

$14.694 trillion.

The estimated population of the United States 2006 is around 300,000,000 people. David M.

Walker, Comptroller General of the US and head of the Government Accountability Office, in his

December 17, 2007, report to the US Congress on the financial statements of the US government

noted that “the federal government did not maintain effective internal control over financial

reporting (including safeguarding assets) and compliance with significant laws and regulations

as of September 30, 2007.”

The US government cannot pass an audit.

The GAO report states accrued liabilities of the federal government “totaled approximately $53

trillion as of September 30, 2007”, likely to increase to $70 trillion by the end of 2009.

USA TODAY May 28, 2009, used federal data to compute all government liabilities, from Trea-

sury bonds to Medicare to military pensions.

Bottom line: The government took on $6.8 trillion in new obligations in 2008, pushing the total

owed to a record $63.8 trillion.

No funds have been set aside against the liability.

The estimated net worth of all Americans including all business is about $47 trillion, reducing

rapidly as property and company value reduces.

The Debt Can Not

And Will Not Ever Be Paid.

EVER.

THIS IS FRAUD

By CONGRESS

AND

The Central Bankers of the

US Federal Reserve

US debt as of August 19th 2011

24. M2 has never grown this fast in a seven week period for at least the past 50 years.

No matter how you look at it, this is a major event.

During recessions the US Bureau of Labor Statistics model doesn’t work.

The model is based on good times when new jobs always exceed lost jobs.

On the ‘death’ side, if a company goes out of business due to recession and does not

report its payroll, the US Bureau of Labor Statistics assumes the employees are still in place.

On the ‘birth’ side, 30,000 jobs are added to the monthly numbers as an estimate of new start-ups.

25. China

China’s leading credit rating agency Dagong Global Credit Rating Company last summer stripped

America, Britain, Germany and France of their AAA ratings, accusing Anglo-Saxon competi-

tors of ideological bias in favour of the West.

And last week:

Analysis shows that the crisis confronting the U.S. cannot be ultimately resolved through cur-

rency depreciation.

On the contrary, it is likely that an overall crisis might be triggered by the U.S. government’s

policy to continuously depreciate the U.S. dollar against the will of creditors.

Creation of Electronic Nonsense

Is Fraud

And China Knows This

If we exclude the factor of virtual [a more polite term for false] economy, the U.S. actual GDP is

about 5 trillion U.S. dollars.

Total domestic consumption is 10.0 trillion U.S. dollars and government expenditure was 4.5

trillion U.S. dollars in 2009, now in 2011 it is anticipated with debt load to be somewhere above

the moon, between U.S. 10 and 30 trillion dollars of creation of electronic nonsense.

26. Financial collapse and the Illuminati Gods

But when the banks use their putrid mortgage-backed sludge in the repo markets — concealing their true condition

from investors — they get high-fives from bondholders and regulators alike!

...The whole thing a scam from the get go! ‘Creative accounting’ — think Enron — is the insolvency of the system!

HFT — complex derivatives — securitization — repo transactions — all preserved in their previous state!

27. Financial collapse and the Illuminati Gods

Stabilization and recovery is not part of the plan.

Only extension of the economy — until the right spot is reached to pull the plug on the entire system.

The key to that is the bond market, which is ten times larger than the stock market.

28. Obama and the Illuminati Gods

And think of all the volatility that all these events will bring to world financial markets, and the fabulous wealth

accumulated by anyone having insider information on when these events will be orchestrated to occur!

However, as for the those of you who have not been anointed by the New World Order, only those who own gold

and silver [that means part buried in your garden, part under the floorboards] will survive!

UNLESS WE OCCUPY WALL STREET

AND EVERY MAJOR CITY IN THE USA

New World Order Statistics

The gifts of billions of dollars of taxpayers’ money provided the banks with an abundance of low cost capital that has

boosted the banks’ profits, while the taxpayers who provided the capital are increasingly unemployed and homeless.

JPMorgan Chase announced that it has earned $3.6 billion in the third quarter of this year.

Meanwhile, New York City’s homeless shelters have reached the all time high of 39,000 - 16,000 of whom are children.

OUR CHILDREN!

29. The US is bankrupt!

This period — up to a future where the veil can no longer cloak

— is going to see heightening dissembling within our present structures!

Dissemble — to hide under a false semblance or seeming; to feign (something) not to be what it really is;

to put an untrue appearance upon; to disguise; to mask.

And from now — and for the next few years — we are going to see major dismembering of everything we

have viewed and expected as a progression of our Earth lives!

Whatever they are telling you, the time to prepare is fast coming to an end!

Prepare means of food procurement and private storage and other survival mechanisms!

This applies to people in all Western countries, and all other nation-states also!

And Occupy Wall Street and Every Major US City

Or You Will Not Survive

30. JP Morgan and the US Gold Bullion Fed dollar Empire

This period — up to a future where the veil can no longer cloak —

is going to see heightening dissembling within our present structures!

Dissemble — to hide under a false semblance or seeming; to feign (something) not to be what it really is;

to put an untrue appearance upon; to disguise; to mask.

And from now — and for the next few years — we are going to see major dismembering of everything we

have viewed and expected as a progression of our Earth lives!

Whatever they are telling you, the time to prepare is fast coming to an end!

Prepare means of food procurement and private storage and other survival mechanisms!

This applies to people in all Western countries, and all other nation-states also!

And Occupy Wall Street and Every Major US City

Or You Will Not Survive

31. SuperCon • Obama Steps In As Crime Boss

Fraud is initiated in boardrooms and CEO offices by making “really bad loans, because they pay better”.

Grow them like a Ponzi scheme multiplied through leverage

— it’s hugely profitable early on, then inevitably creates

“disaster down the road”.

One scheme was subprime Alt-A and even prime “liars’

loans” — meaning no checks are made on income, jobs,

ability to repay, and the more they’re inflated the more

profitable they are.

The amount was enormous — for one company alone

they generated as many losses as the entire Savings &

Loan scandal.

Toxic products willfully created to scam borrowers for

big profits and rating agencies went along by apprais-

ing junk as AAA instead of doing it honestly.

Don’t Be Fooled!

32. The Whole Truth And Nothing But The Truth

Stephen Lendman

April 18, 2009

Obama Capone Since taking office, Obama, wittingly or otherwise, has headed the largest crimi-

nal enterprise in history - the mass looting of national wealth to enrich his Wall Street benefac-

tors. He assembled a rogue economic team of Clinton Robert Rubin retreads - to fix the current

crisis they engineered.

Since taking office, Obama, wittingly or otherwise, has headed the largest criminal enterprise

in history — the mass looting of national wealth to enrich his Wall Street benefactors.

He assembled a rogue economic team of Clinton/Robert Rubin retreads — to fix the current cri-

sis they engineered.

In a March 13 article, (author and former Republican strategist) Kevin Phillips called them:

“recycled senior (Clinton administration) Democrats (responsible for the) tech mania, deregu-

lation binge and (1997 — 2000) stock market bubble and crash.

Obama) extend(ed) the (disastrous) mismanagement and pro-Wall Street bias of the 2008 Bush

regime bailout.”

He called Geithner and Bernanke “hapless,” the result of their ruinous misjudgments (and,

along with Alan Greenspan, complicit) with finance-sector malfeasance.”

He said Summers will be “remembered for helping to block federal regulation of financial deriv-

atives and orchestrat(ing) the 1999” Glass-Steagall repeal, among his other “achievements.”

He went down the list of key economic officials and trashed them all as the very types to be

avoided, not appointed.

He noted that Bernanke was chairman of George Bush’s Council of Economic Advisers and add-

ed:

“Imagine if FDR had retained Herbert Hoover’s chief economic advisor and loyal Republican

Fed Chairman in 1933... To think that the pussycat Fed (would become) a saber-toothed tiger

is a deception.”

Worse still, ruinous economic policies “could prove fatal” if White House policies favor “Wall

Street but not the national economy or American people” — the very direction they’ve now

taken.

In a follow-up April 7 article, Phillips highlighted:

“The Disaster Stage of US Financialization....a much grander-scale disaster than anything that

happened in 1929 — 1933.

Worse, it dwarfs the abuses of debt, finance and financialization that brought down previous

leading world economic powers like Britain and Holland.”

Today’s crisis represents:

“the bursting of the huge 25-year, almost $50 trillion debt bubble that helped underwrite the

hijacking of the US economy by a rabid financial sector....”

It’s realigning global power with America losing its economic leadership won in WW II.

“The ignominy deserved by Wall Street after 1929-1933 is peanuts compared with the opprobri-

um the US financial sector and its political and regulatory allies deserve this time.” Financial-

ized America radically transformed the country, now “doubly staggering because of the crush-

ing burden of its collapse.”

Yet major media pundits and reporters barely noticed and now claim relief is just a few quarters

away — ignoring a metastasizing cancer, a national disaster, while policy makers heap fuel on a

raging blaze now consuming us, yet too little public rage confronts them.

A Former Insider Speaks Out

Economics Professor William Black is a former senior bank regulator and Savings and Loan

prosecutor, currently teaching economics and law at the University of Missouri.

In an April 13 Barrons interview, he referred to “failed bankers (advising) failed regulators on

how to deal with failed assets” they all had a hand in creating and proliferating.

His conclusion: “How can it result in anything but failure.”

He called the scale of financial fraud “immense,” and said “Unless the current administration

changes course pretty drastically, the scandal will destroy Barack Obama’s presidency,” besides

what it’s doing to the country, global economies, and many millions of people here and abroad.

He scathed Summers and Geithner, both “important architects of (today’s) problems,” and the

latter as a failed and dishonest regulator, yet “numbering himself among those who convey

tough medicine when he’s really pandering to the interests of a select group of banks.”

No need to mention which ones.

The law mandates corrective action, the kind FDR took in the 1930s.

He, Bernanke and Summers flout the law, “in naked violation, in order to pursue the kind of

favoritism that the law was designed to prevent.”

They’ve turned taxpayers into “suckers” who’ll pay dearly for decades, maybe generations.

[Not unless they are very, very, very, stupid — Kewe]

His refusal to put insolvent banks into receivership, resorting to deceptive language like “leg-

acy assets,” and pursuing the worst of Chicago School economics “is positively Orwellian... If

cheaters prosper, (they’ll) dominate.

33. It’s like Gresham’s law: Bad money drives out the good.

Well, bad behavior” does the same thing “without good enforcement.”

His bailout plans are disastrous.

They prop up zombie banks by:

“mispricing toxic assets....The last thing we need is a further drain on our resources....by pro-

moting this toxic asset market (and notions of) too-big-to-fail.”

Multi-trillion dollar cover-up

by publicly traded enterprises

With most, perhaps all, the big banks insolvent (a polite term for bankrupt), what’s going on is

“a multi-trillion dollar cover-up by publicly traded (enterprises), which amounts to felony secu-

rities fraud on a massive scale.”

Ultimately, these firms will be forced into receivership, their “managements and boards stripped

of office, title, and compensation.”

What’s needed is a 1930s-style Pecora investigation to get to the bottom of their fraud, deceit,

and cover-up, along with government complicity to hide it.

More on that below.

Black cited billions to AIG as the single worst abuse so far — to bail out their counterparties like

Switzerland’s UBS at the same time we were prosecuting it for tax fraud. As bad was following

Goldman Sachs’ advice to direct a $13 billion counterparty windfall to itself.

The whole process reeks of corruption

It must be stopped, and a new direction instituted under a reformist economic team — one that

will admit the nature and depth of the problem, cut the tie to Wall Street, and take corrective

action the law mandates.

That’s “precisely what isn’t happening.”

Washington is “wedded to the bad idea of bigness” and power of Wall Street.

In today’s America, financialization is predominant.

It’s a cancer eating away at the fabric of the nation and many millions affected, the result of the

grandest of grand thefts.

A good start would be to break up the financial giants into more effectively managed and less

powerful units — maybe the way Standard Oil was dismantled through a simple share spinoff.

In addition, “a new seriousness must be put into regulation,” and a new resolve to enforce it.

Today, the whole system encourages fraud, one based on results at any cost, so “fudging the

numbers” becomes de rigueur and global bigness the holy grail.

It sends the wrong message — play or pay with your job and future on Wall Street.

“The basis for all regulation and white-collar crime is to take the competitive advantage away

from the cheats, so the good guys can prevail. We need to get back to that.”

It’s been decades since we’ve been there and high time we took it seriously.

Job one is a thorough housecleaning and new direction, much like what’s described below.

On April 3, Black appeared on Bill Moyers Journal on PBS and explained what’s briefly enumer-

ated below.

From his experience as a regulator and prosecutor, he said:

• Fraud is initiated in boardrooms and CEO offices by making “really bad loans, because they

pay better;”

• Then grow them like a Ponzi scheme multiplied through leverage; it’s hugely profitable early

on, then inevitably creates “disaster down the road;”

• Dismantling regulation makes it possible;

• One scheme was subprime, Alt-A , and even prime “liars’ loans” — meaning no checks are

made on income, jobs, ability to repay, and the more they’re inflated the more profitable they

are; the amount of them was enormous — for one company alone, they generated as many losses

as the entire S & L scandal;

• Toxic products were willfully created to scam borrowers for big profits;

• Rating agencies went along by appraising junk as AAA instead of doing it honestly;

• In September 2004, the FBI warned about a mortgage fraud epidemic, but nothing was done

to stop it; so now we have a crisis hundreds of times greater than the S & L one and bad policy

in play to address it;

• As in Barrons, he accused top Bush and Obama officials of a cover-up — to conceal the insol-

vency of all major banks and by so doing broke the law established after the S & L crisis, the

Prompt Corrective Action Law that mandates insolvent banks be shut down and/or placed in

receivership; and

• This is the greatest financial scandal in history — swept under the rug by top government of-

ficials of both parties; it’s legally and morally indefensible, and it’s wrecking the country.

In an April 6 article, Black calls ongoing “stress tests a complete sham.... to fool people.... make

us chumps” and essentially say ‘If we lie and they believe us, all will be well’” when, in fact, it’s

not.

34. Greatest ever criminal fraud

by bankers and complicit government officials

It’s part of the giant cover-up and greatest ever criminal fraud — by bankers and complicit gov-

ernment officials.

On April 13, Nouriel Roubini shared Black’s view.

He cited the stress test “spin machine” leaking stories to the press that all 19 banks in question

will pass.

None will fail.

If more “exceptional assistance” is needed, Washington will provide it.

However, Q 1 macro data tells another story as growth, unemployment, and falling home prices

alone “are worse than those in FDIC’s baseline scenario for 2009 AND even worse than those

for the more adverse stressed scenario for 2009.

Make believe

Thus, the stress test results are meaningless” as worsening data are outdistancing “the worst

case scenario.”

In other words, test results “are not worth the paper (they’ll be) written on” as their assump-

tions are fraudulently based.

They’re “fudge tests....blatantly rigged” to put a brave face on a very bleak economic picture.

They’re in addition to other changes, including the recent Financial Accounting Standards

Board (FASB) ruling. It’s responsible for developing “generally accepted accounting princi-

ples” known as GAAP. On April 3, it changed so-called “mark-to-market” standards to “mark-to-

make believe” ones. It also voted to allow banks to book smaller impaired asset losses to paint a

brighter profits picture. It let Wells Fargo, for example, claim a Q 1 profit when it’s drowning in

losses, ones it can hide and not take. Also likely coming is restoration of the “uptick rule” that

prohibited short-selling in a down market.

Established in 1938 to prevent disorderly selling, it allows shorts only when shares trade up.

In June 2007, it was removed. Re-introductory proposals are now being considered to artifi-

cially boost prices. Roubini calls it “a form of legalized manipulation of the stock market by

regulators... to prevent short-sellers (from doing) their job, i.e. make stock prices reflect funda-

mentals and prevent bubbles.”

Overall, alarm bells should be warning about reckless monetary and fiscal policies, but perverse

market reaction was relief. That’s wildly premature according to some like Roubini.

Others see a protracted downturn, a prolonged winter, and if conditions deteriorate enough

perhaps a nuclear one, unlike anything before seen, and why not:

• World economies are plummeting at depression-level speed by all key measures — produc-

tion, consumption, trade, profits, asset values, capital flows, and more;

• Unemployment is soaring; in America close to 20% (it already has) with all excluded and un-

derstated categories included;

• Pensions have been lost along with benefits;

• Homelessness is rising sharply, the result of over six million foreclosures; tent cities are ap-

pearing across the country;

• Recent data shows soaring foreclosures up 24% in Q 1 2009; in March alone, 46% higher than

a year earlier — alone providing clear evidence of serious trouble we now have OVER 11 million

foreclosures, and,

• Desperation is fueling anger and despair as conditions keep deteriorating absent sound poli-

cies to address them.

From Bubble to Depression

On April 6, Professor Vernon Smith (a 2002 economics Nobel laureate) and research associate

Steven Gjerstad headlined a Wall Street Journal op-ed: “From Bubble to Depression?”

They asked:

What creates bubbles?

Why does a large one, like the dot.com bubble, do no damage to the financial system while an-

other (housing) caused collapse?

They believe “events of the past 10 years have an eerie similarity to the period leading up to the

Great Depression,” including rising mortgage debt and speculation, then asked:

“Had banking system difficulties “been caused by losses on brokers loans for margin purchases

in 1929, the results should have been felt in the banks immediately after the stock market

crash.”

But they weren’t apparent until fall 1930, a year later.

Further, if money supply contraction caused bank failures, why haven’t massive infusions to-

day prevented the crisis?

They conclude that conventional wisdom needs reassessing and believe “excessive consumer

debt — especially mortgage debt — was transmitted into the financial sector” causing the Great

Depression.

35. Their Hypothesis:

“Is that a financial crisis (originating) in consumer debt, concentrated at the low end of the

wealth and income distribution (affecting so many households), can be transmitted quickly and

forcefully into the financial system...

We’re witnessing the second great consumer debt crash, the end of a massive consumption

binge,” but want more study to prove it.

However, much more than that is needed — real reform, a complete reversal from current poli-

cy of the kind addressed below.

Also, Smith and Gjerstad omitted a crucial fact — how misdirected today’s massive infusions

have been.

Instead of helping beleaguered households, they’ve gone mostly to bankers for purposes oth-

er than economic recovery; namely, recapitalizations, for acquisitions, and big bonuses at the

same time they fire thousands of lower level staff.

The 1930s Pecora Commission

On March 4, 1932 (one year to the day before FDR took office), a majority-Republican Senate

Banking, Housing, and Urban Affairs Committee established it to investigate the causes of the

1929 crash.

It was little more than a fig leaf until Democrats took over, appointed Ferdinand Pecora as spe-

cial counsel, and made a real effort for banking and regulatory reform.

Straightaway, Pecora looked into Wall Street’s seamy underside by placing powerful bankers in

the dock, holding them accountable for their actions, and doing through hearings what would

have been impossible in open court given their ability to “buy” justice.

He confronted Wall Street’s biggest names:

Richard Whitney, president of the New York Stock Exchange;

Noted investment bankers, including Thomas Lamont, Otto Kahn, Charles E. Mitchell, Albert

Wiggin, and JP Morgan, Jr., scion of the man who dominated the Street for decades as its boss

and de facto Fed chairman before the central bank was established.

Market Speculators Like Arthur Cutten

No income taxes paid. He got Morgan to admit that he and his 20 partners paid no income taxes

in 1931 and 1932. Neither did its Philadelphia operation, Drexel and Co., in the same years and

way underpaid them in previous ones. It made headlines, was stunning, and galvanized critics

to demand reform. Pecora went further. He questioned Morgan and others on various matters,

including sweetheart deals for political figures and insider ones for Wall Street cronies, similar

shenanigans to today but not on the same scale, and under a president then who cared once

Roosevelt took office. He directed “pitiless publicity” on Street corruption, what they easily got

away with under Republicans.

Pecora was a former New York district attorney, an Eliot Spitzer-type with a reputation for

toughness and fearlessness, but one serving at the behest of the President. He established

straightaway that some of Wall Street’s most powerful lied to their shareholders, manipulated

stocks to their advantage, and profited hugely through malfeasance.

Roosevelt encouraged him in his March 4, 1933 inaugural address saying:

“There must be a strict supervision of all banking and credits and investments. There must be

an end to speculation with other people’s money. There must be provision for an adequate but

sound currency... The rulers of the exchange of mankind’s goods have failed through their own

stubbornness and their own incompetence, have admitted their failure and abdicated. Prac-

tices of the unscrupulous money changers stand indicted in the court of public opinion, rejected

by the hearts and minds of men....”

“They know only the rules of a generation of self-seekers. They have no vision, and when there

is no vision the people perish. The money changers have fled their high seats in the temple of

our civilization. We must now restore that temple to the ancient truths. (Doing it requires)

apply(ing) social values more noble than mere monetary profit.”

Imagine Obama Saying This

Imagine Obama saying this, followed by strong policies for enforcement under Roosevelt-style

officials. Men like Pecora who asked tough questions and demanded answers, including on the

House of Morgan’s operations, something unimaginable today under any leadership. Morgan’s

counsel, John W. Davis, called Pecora’s questions outrageous, but Morgan had to answer in de-

tail enough to shake the “secret government’s” foundations.

Pecora’s staff examined company records that revealed financial manipulations among the

Street’s powerful to reap enormous profits — enough for Morgan to gain control of most US in-

dustry, buy politicians and diplomats, and effectively control the most powerful banks in the

country.

A Small Group Of Highly Placed Financiers

Holds The Real Power

Years later in his book, Wall Street Under Fire, Pecora wrote:

“Undoubtedly, this small group of highly placed financiers, controlling the very springs of eco-

nomic activity, holds more real power than any similar group in the United States.”

Morgan called it performing a “service” and exercising no more control than through “argument

and persuasion.” His managing partner, Thomas Lamont, told the committee that the firm only

offered advice that clients could accept or reject. Pecora learned otherwise as he peeled away

the layers of company power and influence.

36. Friends of the bank lists in two tiers

He discovered “preferred clients” and friends of the bank lists in two tiers — special allies, op-

eratives, and cronies and a “fishing list” from which new ones were recruited. In total, it showed

Morgan was more powerful than Washington — that the firm effectively controlled a network