30 December Daily market report

•

1 like•435 views

The QSE Index declined 1.9% led by declines in the Real Estate and Consumer Goods & Services indices. Top losers were Dlala Brokerage & Invest. Holding Co. and Islamic Holding Group, falling 8.2% and 6.4% respectively. Regional indices also declined, with Saudi Arabia down 4.2% and Dubai down 5.4%. Qatar's real GDP is estimated to have grown 6% in 3Q2014 powered by non-hydrocarbon sectors like construction and trade, while the hydrocarbon sector declined around 3%.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to 30 December Daily market report

Similar to 30 December Daily market report (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

30 December Daily market report

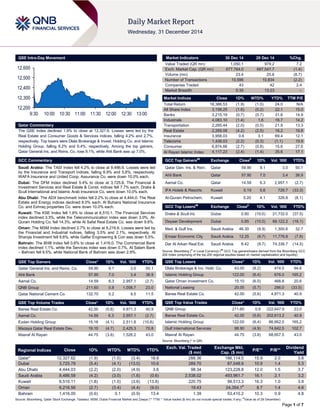

- 1. Page 1 of 7 QSE Intra-Day Movement Qatar Commentary The QSE Index declined 1.9% to close at 12,327.6. Losses were led by the Real Estate and Consumer Goods & Services indices, falling 4.2% and 2.7%, respectively. Top losers were Dlala Brokerage & Invest. Holding Co. and Islamic Holding Group, falling 8.2% and 6.4%, respectively. Among the top gainers, Qatar General Ins. and Reins. Co. rose 9.1%, while Ahli Bank was up 7.0%. GCC Commentary Saudi Arabia: The TASI Index fell 4.2% to close at 8,486.6. Losses were led by the Insurance and Transport indices, falling 6.9% and 5.8%, respectively. WAFA Insurance and United Coop. Assurance Co. were down 10.0% each. Dubai: The DFM Index declined 5.4% to close at 3,725.8. The Financial & Investment Services and Real Estate & Const. indices fell 7.7% each. Drake & Scull International and Islamic Arab Insurance Co. were down 10.0% each. Abu Dhabi: The ADX benchmark index fell 2.2% to close at 4,444.0. The Real Estate and Energy indices declined 8.0% each. Al Buhaira National Insurance Co. and Eshraq properties Co. were down 10.0% each. Kuwait: The KSE Index fell 1.8% to close at 6,510.1. The Financial Services index declined 3.3%, while the Telecommunication index was down 3.0%. Al- Qurain Holding Co. fell 14.3%, while Al Safat Real Estate Co. was down 9.8%. Oman: The MSM Index declined 2.7% to close at 6,216.6. Losses were led by the Financial and Industrial indices, falling 3.5% and 2.1%, respectively. Al Sharqia Investment fell 9.8%, while Galfar Engineering & Con was down 5.5%. Bahrain: The BHB Index fell 0.6% to close at 1,416.0. The Commercial Bank index declined 1.1%, while the Services index was down 0.7%. Al Salam Bank – Bahrain fell 9.5%, while National Bank of Bahrain was down 2.9%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar General Ins. and Reins. Co. 59.90 9.1 3.0 50.1 Ahli Bank 57.90 7.0 3.4 36.9 Aamal Co. 14.59 6.3 2,957.1 (2.7) QNB Group 211.60 0.8 1,058.7 23.0 Qatar National Cement Co. 132.70 0.2 9.5 11.5 QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Barwa Real Estate Co. 42.00 (5.6) 4,871.3 40.9 Aamal Co. 14.59 6.3 2,957.1 (2.7) Ezdan Holding Group 15.16 (4.1) 2,511.8 (10.8) Mazaya Qatar Real Estate Dev. 19.10 (4.7) 2,425.3 70.8 Masraf Al Rayan 44.75 (3.8) 1,526.2 43.0 Market Indicators 30 Dec 14 29 Dec 14 %Chg. Value Traded (QR mn) 1,050.1 979.2 7.2 Exch. Market Cap. (QR mn) 677,764.0 687,547.7 (1.4) Volume (mn) 23.4 25.6 (8.7) Number of Transactions 10,596 10,834 (2.2) Companies Traded 43 42 2.4 Market Breadth 5:35 13:23 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,386.53 (1.9) (1.0) 24.0 N/A All Share Index 3,158.25 (1.6) (0.2) 22.1 15.0 Banks 3,215.19 (0.7) (0.7) 31.6 14.9 Industrials 4,083.10 (1.4) 1.6 16.7 14.2 Transportation 2,265.44 (2.0) (0.5) 21.9 13.3 Real Estate 2,269.08 (4.2) (2.5) 16.2 19.8 Insurance 3,958.03 0.6 3.1 69.4 12.1 Telecoms 1,438.03 (2.2) (0.3) (1.1) 19.9 Consumer 6,874.66 (2.7) (0.8) 15.6 27.6 Al Rayan Islamic Index 4,117.23 (2.4) (1.4) 35.6 17.1 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Qatar Gen. Ins. & Rein. Qatar 59.90 9.1 3.0 50.1 Ahli Bank Qatar 57.90 7.0 3.4 36.9 Aamal Co. Qatar 14.59 6.3 2,957.1 (2.7) IFA Hotels & Resorts Kuwait 0.19 5.6 726.7 (33.3) Al-Qurain Petrochem. Kuwait 0.20 4.1 326.8 (8.1) GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Drake & Scull Int. Dubai 0.90 (10.0) 21,732.0 (37.5) Deyaar Development Dubai 0.85 (10.0) 89,122.2 (16.1) Med. & Gulf Ins. Saudi Arabia 46.30 (9.9) 1,300.6 32.7 Emaar Economic City Saudi Arabia 12.25 (9.7) 11,776.8 (7.9) Dar Al Arkan Real Est. Saudi Arabia 8.42 (9.7) 74,336.7 (14.5) Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Dlala Brokerage & Inv. Hold. Co. 43.00 (8.2) 474.5 94.6 Islamic Holding Group 122.00 (6.4) 676.0 165.2 Qatar Oman Investment Co. 15.10 (6.0) 466.8 20.6 National Leasing 20.05 (5.7) 286.0 (33.5) Barwa Real Estate Co. 42.00 (5.6) 4,871.3 40.9 QSE Top Value Trades Close* 1D% Val. ‘000 YTD% QNB Group 211.60 0.8 222,647.9 23.0 Barwa Real Estate Co. 42.00 (5.6) 202,613.2 40.9 Islamic Holding Group 122.00 (6.4) 86,662.0 165.2 Gulf International Services 98.90 (4.9) 74,642.5 102.7 Masraf Al Rayan 44.75 (3.8) 68,657.5 43.0 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 12,327.62 (1.9) (1.0) (3.4) 18.8 288.36 186,114.0 15.9 2.0 3.8 Dubai 3,725.79 (5.4) (4.1) (13.0) 10.6 289.70 87,048.9 10.9 1.4 5.3 Abu Dhabi 4,444.03 (2.2) (2.0) (4.9) 3.6 98.34 123,228.8 12.0 1.5 3.7 Saudi Arabia 8,486.58 (4.2) (3.0) (1.6) (0.6) 2,538.02 493,961.7 16.1 2.1 3.2 Kuwait 6,510.11 (1.8) (1.0) (3.6) (13.8) 220.75 99,513.3 16.3 1.0 3.9 Oman 6,216.56 (2.7) (3.4) (4.4) (9.0) 19.43 24,354.1# 8.7 1.4 4.6 Bahrain 1,416.00 (0.6) 0.1 (0.9) 13.4 1.39 53,410.2 10.3 0.9 4.8 Source: Bloomberg, Qatar Stock Exchange, Tadawul, MSM, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any; # Value as of 29 December) 12,200 12,300 12,400 12,500 12,600 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QSE Index declined 1.9% to close at 12,327.6. The Real Estate and Consumer Goods & Services indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari shareholders. Dlala Brokerage & Investments Holding Co. and Islamic Holding Group were the top losers, falling 8.2% and 6.4%, respectively. Among the top gainers, Qatar General Insurance and Reinsurance Co. rose 9.1%, while Ahli Bank was up 7.0%. Volume of shares traded on Tuesday fell by 8.7% to 23.4mn from 25.6mn on Monday. However, as compared to the 30-day moving average of 15.8mn, volume for the day was 47.5% higher. Barwa Real Estate Co. and Aamal Co. were the most active stocks, contributing 20.9% and 12.7% to the total volume respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings and Global Economic Data Earnings Releases Company Market Currency Revenue (mn) 3Q2014 % Change YoY Operating Profit (mn) 3Q2014 % Change YoY Net Profit (mn) 3Q2014 % Change YoY Sahara Hospitality Co. (SHC) * Oman OMR 12.0 4.9% – – 2.0 7.8% Source: Company data, DFM, ADX, MSM (*FY2013-14 results) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 12/30 US S&P/Case-Shiller S&P/CS 20 City MoM SA October 0.76% 0.40% 0.24% 12/30 US S&P/Case-Shiller S&P/CS Composite-20 YoY October 4.50% 4.40% 4.82% 12/30 US S&P/Case-Shiller S&P/CaseShiller 20-City Index NSA October 173.4 173.7 173.6 12/30 US S&P/Case-Shiller S&P/Case-Shiller US HPI YoY October 4.64% – 4.82% 12/30 US S&P/Case-Shiller S&P/Case-Shiller US HPI NSA October 167.1 – 167.5 12/30 US Conference Board Consumer Confidence Index December 92.6 93.9 91.0 12/30 EU European Central Bank M3 Money Supply YoY November 3.10% 2.60% 2.50% 12/30 EU European Central Bank M3 3-month average November 2.70% 2.50% 2.30% 12/30 UK Nationwide Building Soc. Nationwide House PX MoM December 0.20% 0.20% 0.30% 12/30 UK Nationwide Building Soc. Nationwide House Px NSA YoY December 7.20% 7.20% 8.50% 12/30 Spain INE Retail Sales YoY November 0.50% – 1.90% 12/30 Spain INE Retail Sales SA YoY November 1.90% 0.80% 1.00% 12/30 Spain INE CPI EU Harmonised YoY December -1.10% -0.70% -0.50% 12/30 Spain INE CPI YoY December -1.10% -0.70% -0.40% 12/30 Spain Bank of Spain Current Account Balance October 0.3B – 0.3B 12/30 Italy ISTAT Business Confidence December 97.5 96.7 96.5 12/30 Italy ISTAT Economic Sentiment December 87.6 – 87.6 12/30 Italy Banca D'Italia 5 Year Bond Allotment 30-December 2.846B – 3.500B 12/30 Italy Banca D'Italia 5 Year Bond Average Yield 30-December 1.0 – 0.9 12/30 Italy Banca D'Italia 5 Year Bond Bid/Cover Ratio 30-December 1.4 – 1.5 12/30 Italy Banca D'Italia 10 Year Bond Allotment 30-December 2.996B – 2.000B 12/30 Italy Banca D'Italia 10 Year Bond Average Yield 30-December 1.89% – 2.08% 12/30 Italy Banca D'Italia 10 Year Bond Bid/Cover Ratio 30-December 1.3 – 1.6 12/30 Italy ISTAT PPI MoM November -0.20% – -0.50% 12/30 Italy ISTAT PPI YoY November -1.60% – -1.50% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari 58.33% 55.61% 28,675,571.38 Non-Qatari 41.66% 44.40% (28,675,571.38)

- 3. Page 3 of 7 News Qatar MDPS: Qatar real economic growth estimated at 6% in 3Q2014 – According to the latest data released by the Ministry of Development Planning & Statistics (MDPS), Qatar’s inflation- adjusted (real) economy is estimated to have grown 6% YoY in 3Q2014, mainly powered by the non-hydrocarbon segment, particularly construction and trade. However, the hydrocarbon sector, witnessed almost a 3% YoY decline in 3Q2014. The sector saw a 4.3% YoY decline in nominal growth on receding crude oil production and some maintenance shutdowns in gas plants. The decline in international price levels of crude oil and gases in this quarter also led to a sharper decline in nominal gross value addition of this sector. MDPS, in its recent Qatar Economic Outlook 2014-16 Update, had forecasted the real economic growth to be 6.3% for the whole of 2014. While flat gas production and receding oil output are seen checking the overall expansion in 2014, the commissioning of production from the Barzan project in 2015 is set to support higher economic growth in 2015–2016. The non-hydrocarbon segment witnessed a robust 12% YoY expansion in 3Q2014, driven by electricity, construction, trading, and transport & communication sectors. The report said the 7% jump in the country’s population in 3Q2014 is another factor in contributing such a growth, adding the sector had grown by 13.9% in nominal terms. The manufacturing sector reported a 7.3% growth YoY on the back of higher volumes of production of petrochemicals, fertilizers, basic iron & steel products and other non-metallic mineral products. The sector had witnessed a 9% rise in nominal terms. Major public investments, especially in the infrastructure-related projects continue to impact the growth in the construction sector, which registered a robust 18.5% growth in 3Q2014. The trade, hotel and restaurant sector witnessed a 13.7% growth in 3Q2014, spurred by high trading and hospitality activities seen during Ramadan, a seasonal phenomenon. The transport & communications segment grew 10.5% and 12.6% in real and nominal terms, respectively, in 3Q2014. The finance, insurance, real estate and business services sector showed a 13.7% and 19.9% growth in real and nominal terms in the review period, while the government services witnessed 8.7% and 9% expansion in real and nominal terms. (Gulf-Times.com) Al-Sharq: ORDS carries out restructuring to improve services and performance – Al-Sharq has reported that Ooredoo (ORDS) is working on restructuring jobs in different administrative verticals. The restructuring drive aims to improve the company’s performance and services. Some positions in some departments have been eliminated as part of the restructuring process. The restructuring process had started many years ago and was subject to continuous assessment and evaluation of employees. Accordingly, some employees were awarded higher positions while some were moved to other departments. (Peninsula Qatar) C-Ring Road third phase expansion to start on January 1 – The Public Works Authority (Ashghal) will start working on the third phase of the C-Ring Road project from January 1, 2015, which is expected to be completed in two and a half months. The third phase extends from the middle point between Rawdat Al Khail and New Slata intersections to the middle point between Rawdat Al Khail and Al Mansoura intersections. All four phases of the C-Ring Road project are expected to be completed in 2Q2015. (Peninsula Qatar) Qatar Chamber CEO sees ‘positive 2015’ for SMEs – Qatar Chamber CEO Remy Rowhani has provided an optimistic forecast for the country’s small and medium-sized enterprises (SMEs), saying 2015 would be a “positive year” for the private sector. (Gulf-Times.com) International US consumer confidence rises in December – According to a private sector report, the consumer confidence in the US increased in December, bolstered by a brightening jobs situation that left perceptions about economic conditions at a high last seen in February 2008. The Conference Board, an industry group, said its index of consumer attitudes rose to 92.6 from an upwardly revised 91.0 the month before. According to a Reuters poll, economists expected a reading of 93.0 for December. November was originally reported as 88.7. The expectations index in December was 88.5 versus November's revised 89.3, and the present situation index rose to 98.6 from a revised 93.7 in November. The present situation index is now at its highest level since February 2008. The "jobs hard to get" index was 27.7 in December, versus a revised 28.7 in November. (Reuters) S&P/Case-Shiller: US home price growth slows further in October – According to a recent survey, the single-family home price appreciation in the US slowed less than forecast in October, as there were hints of some reacceleration in home prices in some cities by year-end. The S&P/Case Shiller composite index of 20 metropolitan areas gained 4.5% YoY in October, as compared to a revised 4.8% YoY increase in September. On a seasonally adjusted monthly basis, prices in the 20 cities rose 0.8% MoM. However, non-seasonally adjusted prices fell 0.1% MoM in the 20 cities; analysts had expected them to be unchanged. A broader measure of national housing market activity rose at a 4.6% YoY, compared with a 4.8% rate in September. The seasonally adjusted 10-city gauge rose 0.7% in October versus a revised 0.2% gain in September, while the non-adjusted 10-city index dipped 0.1% for the second straight month in October. (Reuters) US opens door to oil exports after year of pressure – The Obama administration bowed to months of growing pressure over a 40-year-old ban on exports of most domestic crude, taking two steps expected to unleash a wave of ultra-light shale oil onto global markets. The Bureau of Industry and Security (BIS), which regulates export controls, said it had granted permission to "some" companies to sell lightly treated condensate abroad. Condensate is a form of ultra-light crude. Some two dozen energy companies had asked the agency for clarification on permissible exports earlier in 2014, but until December 30, those requests had been put on indefinite hold. The BIS also released guidance in the form of FAQs, to explain what kind of oil was generally allowed under the ban, the first effort by the administration to clarify an issue that has caused confusion and consternation in energy markets for more than a year. The two measures are clearest signs yet that the administration is ready to allow more of the booming US shale oil production to be sold overseas, where drillers have said it can fetch a premium of $10 a barrel or more. (Reuters) Nationwide: UK house price inflation slows to 13-month low – According to a survey from mortgage lender Nationwide, British house prices rose at their slowest annual rate in more than a year in December but the market looks set to recover in 2015 if the economy improves as expected. Nationwide said house prices rose 7.2% YTD, the smallest annual increase since November 2013 and slowing for the fourth consecutive month. British housing market activity and price rises have been slowing since the middle of the year, in part because of steps taken by regulators to require lenders to make tougher checks on borrowers' ability to repay mortgages. House price growth in

- 4. Page 4 of 7 4Q2014 – which many analysts view as the best guide to the short-term trend in house prices – nevertheless ticked up to 1.0%, from 0.9% in 3Q2014. And although annual house price inflation fell in 12 out of 13 British regions – with only the north of England seeing faster growth – Nationwide expects the market to recover in 2015. (Reuters) Japan's ruling coalition approves corporate tax cuts to spur growth – Japan's ruling coalition has approved a tax reform plan that will cut corporate taxes from April 2015 and pledges further reductions in coming years in a bid by Prime Minister Shinzo Abe to boost profitability and bolster economic growth. The plan approved by Abe's Liberal Democratic Party (LDP) and its coalition partner Komeito would cut the overall effective corporate tax rate by 2.51 percentage points to 32.1% from April and then to 31.3% in 2016. Abe had pledged in June to lower the corporate tax rate to below 30% over the coming years to help pull Japan out of nearly two decades of deflation. Earlier in 2014, Abe eliminated a levy on companies imposed in 2012 to help fund disaster relief. Takeshi Noda, chairman of the LDP's tax panel, estimated that the corporate tax cut would amount to about $3.32bn over the next two fiscal years. Abe hopes the tax cuts will encourage companies to raise wages, which would spur consumer spending, and to invest some of the $1.9tn in cash held by companies outside the financial sector. (Reuters) China to relax restrictions on banks' yuan trading, adding transparency; December factory gauge falls – China will relax restrictions on banks' yuan trading starting in 2015, in a small but significant move toward relaxing its capital controls. The changes will replace daily caps on banks' foreign exchange positions with weekly limits, and for the first time establish unified standards for total foreign exchange positions that banks can hold. The State Administration of Foreign Exchange (SAFE) published a set of new rules to simplify 14 sets of related regulations and add new provisions liberalizing banks' forex trading practices. The yuan has lost 1.3% so far in December and looks set to close the year down 2.8% in the face of bearish pressure which is expected to last well into 2015. Meanwhile, a Chinese factory gauge sank to a seven-month low in December, holding near a preliminary reading and putting pressure on policy makers to provide more support to the world’s second- largest economy. The final reading of the Purchasing Managers’ Index (PMI) from HSBC Holdings Plc and Markit Economics was 49.6 In December from 50 in November, compared with the December 16 reading of 49.5. The Bloomberg median estimate was for 49.5. (Reuters, Bloomberg) Regional China to step up FTA talks with GCC members – China and members of the GCC will speed up free trade agreement (FTA) talks as Beijing accelerates efforts to sign such agreements. China and GCC members started free trade talks in 2004, and a deal will help China cut costs on energy imports from the region. (GulfBase.com) APICORP: Investments in Arab Energy to total $685bn over next five years – According to a report released by the Arab Petroleum Investments Corporation (APICORP), energy capital investments in the Arab world will total $685bn over the next five years. Set against the backdrop of continuing regional turmoil, uncertainty in many global and regional economies, and a declining oil price, APICORP’s latest Arab Energy Investment Outlook predicted lower investment levels as compared to the previous year’s report. It stated that the energy sector investments would have dipped even further had it not been for an apparent catch-up effect, particularly evident in the power sector, as well as ever-increasing project costs. APICORP’s report highlighted the growing divide between the GCC and rest of the Arab region in terms of their credit ratings, and it pinpointed three primary constraints on energy investments. These were: the unrelenting cost of project inflation, the paradoxical scarcity of fuel and feedstock such as natural gas and ethane, and the accessibility of funding, which will be exacerbated if oil prices remain low and below the national breakeven levels over the long-term. (GulfBase.com) SEC signs deal for integrated gas/solar plant – State-owned utility Saudi Electricity Company (SEC) signed a contract worth SR1bn to buy generators for the kingdom's first fossil fuel-fired power plant that will also produce solar energy. The 550- megawatt integrated solar combined cycle (ISCC) plant will primarily burn natural gas, but will generate 50 MW of solar energy to increase fuel efficiency at the planned facility near Tabuk on the Red Sea coast. As per the source, General Electric will supply generating units to the plant. ISCC plants reduce emissions of climate-warming carbon by increasing the amount of steam available for driving power generation turbines, without having to burn more gas or oil. SEC said the project, expected to cost a total of SR2.5bn, would be fully operational before the end of 2017. (Reuters) Reuters: OPEC oil output hits six-month low in December on Libya – According to a Reuters survey, OPEC's oil supply fell by 270,000 barrels per day (bpd) in December to a six-month low as fighting cut Libyan output, offsetting record Iraqi southern exports and stable Saudi Arabian production. The survey indicates Libyan turmoil is effectively lowering output by the OPEC, even after oil ministers decided at a meeting in Vienna last month against a formal reduction to defend market share. As per the survey based on shipping data and information from sources at oil companies, OPEC and consultants, Supply from OPEC averaged 29.98mn bpd in December, down from a revised 30.25mn bpd in November. The drop in OPEC output since September reduces the size of the projected market surplus in 2015, but if supply remains at December's rate the group will be pumping close to 2mn bpd more than the demand for its crude in the first half. OPEC forecasts demand for its crude will average 28.22 million bpd in the first six months of 2015. (Reuters) Saudi coffee market rises sharply to SR15bn – A local Saudi brand Bonnon Coffee, part-owned by the Sedco Holding Group, CEO Khalid Bin Hamad, said that coffee sales in Saudi Arabia will rise by 77% in 2016 thereby overtaking tea sales, pointing out that the growth in coffee processing has helped boost the Saudi coffee market to SR15bn. Meanwhile, tea sales are projected to rise by only 49% amid the stiff competition among global and local companies. According to the International Coffee Organization (ICO), 1.4bn cups of coffee are consumed a day worldwide. Coffee consumption has risen sharply in Saudi Arabia whereby 18,000 tons worth SR203mn are imported. (GulfBase.com) NCB: KSA financial sector remains expansionary despite oil shock – According to a report released by the National Commercial Bank (NCB), Saudi Arabian economy has the benefit of substantial reserve assets to overcome shocks to the oil sector. The financial sector in the Kingdom remains expansionary despite the turbulent oil and equity markets. Aggregate money demand continues to push growth in supply, which had annually peaked in October 2014 at 14.7%. Broad money supply (M3) growth retained its double-digit growth at 13.4% in September 2014. Therefore, the annualized growth rate of money supply in 3Q2014 concluded levels on par with. The monetary base expansion peaked in July 2014 at the rate of 16.7%, and moderated in the following consecutive months to

- 5. Page 5 of 7 11.3%, and 8.5%, in 3Q2014. Demand deposits, which account for around 56% of the money supply reached SR940.8bn at the end of September 2014, surging by 13.9% YoY. Referring to inflation, the report said that consumer prices continued to edge higher in September 2014 following a demand pull in August 2014. Annualized CPI recorded a 2.8% upturn in August 2014 and September 2014 from 2.6% in July 2014, putting the average inflation rate for the quarter at around 2.75%. The shifting cyclicality of Ramadan amplified annualized price changes for the most important category, food and beverages, which rose by 2.9% YoY. (GulfBase.com) Saudi Ceramic BoD recommends Ceramics Pipe acquisition, opening of investment portfolio – Saudi Ceramic Company’s board of directors has recommended the cash acquisition of the other shareholders’ shares of Ceramics Pipe Company (closed joint stock company). The company will prepare a MoU to be presented at the upcoming ordinary general meeting. Saudi Ceramic currently owns 50% of Ceramics Pipe. Ceramic Pipe capital amounts to SR193mn, divided into 19.3mn shares. The finical effect will be determined after preparation of the MoU. The purpose of this acquisition is to merge the activities of both these companies as well as to increase operational efficiency. Meanwhile, Saudi Ceramic will open an investment portfolio (internally funded) for participating in initial public offerings in the Saudi Arabian stock market to generate additional sources of income in line with CMA’s regulations. The party to manage this portfolio will be selected later. (Tadawul) Saudi Ceramic BoD recommends SR100mn dividend for FY2014, SR125mn capital increase – Saudi Ceramic’s board of directors has also recommended the distribution of 20% cash dividend (SR2 per share) amounting to SR100mn for FY2014. The cash dividends will include the issued bonus shares as well. Shareholders registered at of the end of trading on the general assembly meeting day, which will be announced in due course after obtaining the necessary approvals from the official bodies, will be eligible for dividends. Meanwhile, the company’s board of directors has recommended the increase of capital from SR375mn to SR500mn being 33% increase by issuing 12.5mn shares with value of SR125mn and number of shares will increase from 37.5mn shares to 50mn shares. The increase will be funded from retained earnings after the approval of the extraordinary general assembly and the official bodies. This will be done through issuing one bonus share for every three existing shares owned by the shareholders and registered at the end of trading day on the date of the extraordinary general assembly. Each shareholder will receive whole number of shares the fractions will be combined and sold according to market price and the return will be distributed to all shareholders pro rata, the sale will be performed within 30 days of the date of distribution. This capital increase is in line with the growth of Saudi Ceramic as well as to complement its expansion and to ensure the strength of the company’s financial position. (Tadawul) Sipchem announces initial start-up of EVA film plant – Saudi International Petrochemical Company (Sipchem) has commenced the initial start-up of the ethylene-vinyl acetate (EVA) film plant of the Saudi Specialized Products Company (SSPC). Sipchem Chemicals Company, an affiliate of Sipchem owns 75% of SSPC, while Hanwha Chemical Corporation Korea owns 25%. The initial start-up will continue until the completion of testing and will ensure the efficiency of the plant equipment. The total estimated cost of the project is SR150mn, with an annual production capacity of 4,000 metric tons. The EVA film plant for manufacture of solar panels is located in the industrial zone of Hail. (Tadawul) Riyad Bank recommends SR0.35 per share dividend for 2H2014 – Riyad Bank has recommended a dividend of SR0.35 per share for 2H2014. (Reuters) Ajman approves AED1.61bn budget – His Highness Shaikh Humaid bin Rashid Al Nuaimi, Member of Supreme Council and Ruler of Ajman, has approved the general budget of the Ajman government for the fiscal year 2015, with a total expenditure of about AED1.61bn and estimated revenues reaching AED1.61bn. Shaikh Humaid issued Emiri Decree No. 14 of 2014 which takes effect on January 1, 2015. The 2015 budget is 23.44% larger than the 2014 budget, explaining that the growth in expenses was a result of the government’s interest in the emirate’s developmental projects. He said that the increase in revenues is a result of opening new channels for investments in the emirate. The budget includes 33% for the economic affairs sector, 32% for housing and community facilities, 22% for the public services sector, and 13% for the system and public safety affairs sector. (GulfBase.com) IIF: UAE $700bn spending on track – The Institute of International Finance (IIF) said that the relatively low fiscal and external current account breakeven price of oil and ample foreign assets will enable the UAE to press ahead with an estimated $700bn worth of infrastructure projects, which are expected to come on stream over the next 15 years, spurring credit growth in the banking sector. The UAE’s nominal GDP is poised to touch $435bn in 2016, up from $417bn in 2014 and $405bn in 2015 under a predicted baseline oil price scenario of $78 and $85 per barrel respectively in 2015 and 2016. With the economic growth set to hover between 4.8% and 5.1% in the next two years, the UAE will post a current account balance of $29.9bn and $30.2bn respectively in 2015 and 2016, accounting for 7.4% and 6.9% of the GDP. IIF Deputy Director, Dr Garbis Iradian said that the Emirates will record a fiscal balance of 1.8% and 2.8% of the GDP respectively in 2015 and 2016. The coming years will also see the country’s public foreign assets swell from $573bn in 2014 to $615bn in 2015 and $652bn in 2016. The government debt will increase to 22.1% and 23.3% of the GDP respectively in 2015 and 2016. (GulfBase.com) DEWA signs MoU with TECOM Investments – Dubai Electricity and Water Authority (DEWA) has signed a MoU with TECOM Investments to enhance cooperation and invest in their partnership to support developmental initiatives and projects, particularly DEWA’s Smart initiatives. These include electric vehicle charging infrastructure and smart applications through smart meters and grids. Under the terms of the MoU, the two sides will promote joint work and exchange of knowledge, expertise, experiences, and best practices in various disciplines related to common areas of work, in addition to conducting joint research and consultations on projects that support the sustainable development of Dubai. (GulfBase.com) ENOC reduces domestic diesel prices – Emirates National Oil Company (ENOC) has further reduced domestic diesel prices in line with the international decrease in crude oil prices, passing on benefits to customers in the shortest time possible. ENOC reduced diesel prices by an additional 20 fils to AED3.10 per liter, effective as of December 30, 2014. The revised price is applicable across the entire service station network of ENOC and EPPCO. (GulfBase.com) DIA: Russia turmoil slows passenger traffic growth – Dubai International Airport (DIA) has witnessed slower movement in passenger traffic in November 2014 because of the geopolitical and economic instability hitting Russia. Passenger traffic related

- 6. Page 6 of 7 to Russia and other countries in the Commonwealth of Independent States plunged 18.2% YoY in November 2014. This cut growth in total passenger traffic through DIA, which rose 4.3% to 5.57mn people in November 2014, slowing from 5.7% growth in October 2014. In the first 11 months of this year, passenger traffic climbed 5.9% to 63.98mn people. The growth was interrupted earlier this year by an 80-day runway refurbishment project that temporarily cut the airport's capacity. Cargo volume through DIA dropped 8% from a year earlier in November 2014 to 205,375 tons, while cargo handled in the first 11 months shrank 2.7% to 2.16mn tons because of the shift of dedicated freighter services to Dubai's other main airport, Al Maktoum International, in May 2014. (Bloomberg) NBK: Kuwait inflation down 3% in October 2014 – According to a report released by the National Bank of Kuwait (NBK), Kuwait’s inflation in the consumer price index (CPI) eased slightly to 3% YoY in October 2014, as inflation in most components slowed. Core inflation eased slightly from 3.3% YoY in September 2014 to 3.1% YoY in October 2014, as housing inflation remained unchanged and inflation in other major components decelerated. As per the report, food inflation witnessed a marginal slowdown in October 2014 and is projected to continue easing in the coming months in line with lower international food inflation. A stronger Kuwaiti dinar is also expected to help keep domestic inflation under control. Inflationary pressures appear modest and headline inflation is seen ending 2014 at an annual average of 3.0%. Inflation in the food price index eased slightly in October 2014, from 2.7% YoY in September 2014 to 2.6% YoY. The data also showed that the inflation in housing services remained unchanged at 4.4% YoY in October 2014. (GulfBase.com) GCC–Stat: Oman’s inflation lowest in GCC states – According to a report released by the Statistical Centre for the Cooperation Council for the Arab Countries of the Gulf (GCC– Stat), Oman registered the lowest inflation rate of 1.02% among GCC countries in October 2014. Inflation rates across the GCC region ranged between 1.02% and 3.11% in October 2014, as compared to the same period in 2013. As per the report, the UAE recorded the highest inflation rate among GCC states, registering an increase of 3.11%, followed by 3% in both Kuwait and Qatar, 2.6% in Saudi Arabia and 2.5% in Bahrain. The October 2014 inflation rates showed a slight increase of 0.2% in Saudi Arabia, 0.11 % in the UAE, 0.1% on a MoM basis in both Oman and Qatar, while prices in Bahrain and Kuwait remained stable. Meanwhile, Qatar was the only GCC country where prices for food and beverages decreased in October 2014 by 0.6% YoY. (GulfBase.com) GBCM acquires Oman-based brokerage business of Bank Muscat – Gulf Baader Capital Markets (GBCM), a subsidiary of Gulf Investment Services Holding Company, has acquired the Oman-based brokerage business of Bank Muscat, which provides brokerage services for securities traded on the Muscat Securities Market (MSM) and other GCC markets on mutually agreeable terms. This acquisition is line with GBCM’s strategy to further reinforce its dominant position in the institutional and corporate brokerage business and strengthen its position in the retail brokerage business. The company has received the necessary approval from the Capital Market Authority (CMA) for this acquisition and the process of opening of brokerage accounts of erstwhile customers of Bank Muscat is expected to be completed in 1Q2015. Meanwhile, for Bank Muscat the divestment is line with its ongoing review of strategic alternatives and operational priorities, and has no material impact on the bank’s other existing operations. Bank Muscat brokerage will cease to operate from February 10, 2015. (MSM) Port Services BoD approves disposal of some assets – Port Services Corporation’s board of directors has approved the disposal of some of its assets, which include cargo handling equipments and marine tug boats that were rendered surplus to operation’s requirements consequent to the shifting of major vessel and cargo operations out of Port Sultan Qaboos. The disposed equipments and tug boats will be sold through a public auction on December 31, 2014. (MSM)

- 7. Contacts Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509 saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 80.0 100.0 120.0 140.0 160.0 180.0 200.0 220.0 Nov-10 Nov-11 Nov-12 Nov-13 Nov-14 QSE Index S&P Pan Arab S&P GCC (4.2%) (1.9%) (1.8%) (0.6%) (2.7%) (2.2%) (5.4%) (7.0%) (5.6%) (4.2%) (2.8%) (1.4%) 0.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,200.55 1.5 0.4 (0.4) MSCI World Index 1,721.01 (0.6) (0.5) 3.6 Silver/Ounce 16.31 3.1 1.5 (16.2) DJ Industrial 17,983.07 (0.3) (0.4) 8.5 Crude Oil (Brent)/Barrel (FM Future) 57.90 0.0 (2.6) (47.7) S&P 500 2,080.35 (0.5) (0.4) 12.6 Crude Oil (WTI)/Barrel (FM Future) 54.12 1.0 (1.1) (45.0) NASDAQ 100 4,777.44 (0.6) (0.6) 14.4 Natural Gas (Henry Hub)/MMBtu 3.12 3.6 13.2 (28.2) STOXX 600 341.02 (1.1) (1.1) (8.4) LPG Propane (Arab Gulf)/Ton 50.25 (2.4) (5.2) (60.3) DAX 9,805.55 (1.3) (1.3) (9.6) LPG Butane (Arab Gulf)/Ton 64.50 (1.5) (4.8) (52.5) FTSE 100 6,547.00 (1.1) (0.9) (8.9) Euro 1.22 0.0 (0.2) (11.5) CAC 40 4,245.54 (1.8) (1.4) (12.9) Yen 119.48 (1.0) (0.7) 13.5 Nikkei 17,450.77 (0.6) (1.3) (5.8) GBP 1.56 0.3 0.0 (6.0) MSCI EM 954.58 (0.4) 0.2 (4.8) CHF 1.01 0.1 (0.1) (9.7) SHANGHAI SE Composite 3,165.81 0.3 0.7 46.0 AUD 0.82 0.6 0.8 (8.2) HANG SENG 23,501.10 (1.1) 0.7 0.8 USD Index 89.99 (0.2) (0.0) 12.4 BSE SENSEX 27,403.54 0.7 1.2 26.5 RUB 56.38 (3.6) 5.4 71.5 Bovespa 50,007.41 0.9 0.9 (13.4) BRL 0.38 2.1 0.8 (10.7) RTS 790.71 (0.6) (4.6) (45.2) 177.1 133.3 `` 121.9