1. Page 1 of 5

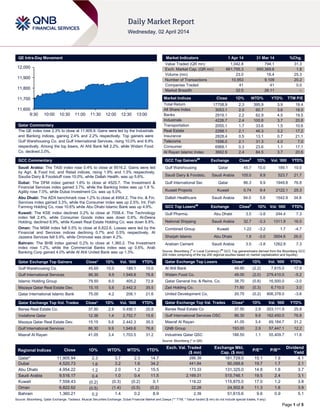

QE Intra-Day Movement

Qatar Commentary

The QE index rose 2.3% to close at 11,905.9. Gains were led by the Industrials

and Banking indices, gaining 2.4% and 2.2% respectively. Top gainers were

Gulf Warehousing Co. and Gulf International Services, rising 10.0% and 9.9%

respectively. Among the top losers, Al Ahli Bank fell 2.2%, while Widam Food

Co. declined 2.0%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.4% to close at 9516.2. Gains were led

by Agri. & Food Ind. and Retail indices, rising 1.9% and 1.5% respectively.

Saudia Dairy & Foodstuff rose 10.0%, while Dallah Health. was up 5.6%.

Dubai: The DFM index gained 1.6% to close at 4520.7. The Investment &

Financial Services index gained 3.7%, while the Banking Index was up 1.8 %.

Agility rose 7.0%, while Dubai Investment Co. was up 5.0%.

Abu Dhabi: The ADX benchmark rose 1.2% to close at 4954.2. The Inv. & Fin.

Services index gained 3.3%, while the Consumer index was up 2.5%. Int. Fish

Farming Holding Co. rose 10.6% while Abu Dhabi Islamic Bank was up 4.9%.

Kuwait: The KSE index declined 0.2% to close at 7558.4. The Technology

index fell 2.4%, while Consumer Goods index was down 0.9%. Al-Deera

Holding. declined 8.9%, while Kuwait Real Estate Holding Co. was down 8.8%.

Oman: The MSM index fell 0.5% to close at 6,822.6. Losses were led by the

Financial and Services indices declining 0.7% and 0.5% respectively. Al

Jazeera Services fell 5.9%, while Ominvest was down 4.2%.

Bahrain: The BHB index gained 0.2% to close at 1,360.2. The Investment

index rose 1.2%, while the Commercial Banks index was up 0.6%. Arab

Banking Corp gained 4.0% while Al Ahli United Bank was up 1.3%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Gulf Warehousing Co. 45.65 10.0 189.1 10.0

Gulf International Services 86.30 9.9 1,949.8 76.8

Islamic Holding Group 79.50 6.0 405.2 72.8

Mazaya Qatar Real Estate Dev. 15.15 5.6 2,442.3 35.5

Qatar International Islamic Bank 75.00 4.2 206.1 21.6

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 37.50 2.9 5,456.1 25.8

Vodafone Qatar 12.38 1.4 2,752.7 15.6

Mazaya Qatar Real Estate Dev. 15.15 5.6 2,442.3 35.5

Gulf International Services 86.30 9.9 1,949.8 76.8

Masraf Al Rayan 41.05 3.4 1,703.5 31.2

Market Indicators 1 Apr 14 31 Mar 14 %Chg.

Value Traded (QR mn) 1,042.8 794.1 31.3

Exch. Market Cap. (QR mn) 661,795.3 650,369.6 1.8

Volume (mn) 23.0 18.4 25.3

Number of Transactions 10,953 9,109 20.2

Companies Traded 41 41 0.0

Market Breadth 32:5 26:11 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 17708.9 2.3 395.9 3.9 19.4

All Share Index 3053.1 2.0 60.7 3.6 18.0

Banks 2919.1 2.2 62.9 4.5 19.5

Industrials 4226.7 2.4 100.8 3.7 20.8

Transportation 2055.1 1.7 33.6 1.5 10.6

Real Estate 2288.1 2.1 46.3 3.2 17.2

Insurance 2828.4 0.5 13.1 0.7 21.1

Telecoms 1556.0 2.1 31.3 4.0 7.0

Consumer 6968.1 0.3 23.6 1.1 17.1

Al Rayan Islamic Index 3662.9 2.4 84.5 3.7 20.6

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Gulf Warehousing Qatar 45.7 10.0 189.1 10.0

Saudi Dairy & Foodstu. Saudi Arabia 105.0 9.9 523.7 21.7

Gulf International Ser. Qatar 86.3 9.9 1949.8 76.8

Kuwait Projects Kuwait 0.74 9.4 2122.1 25.3

Dallah Healthcare Saudi Arabia 94.0 5.6 1542.9 34.8

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Gulf Pharma. Abu Dhabi 3.5 -3.8 244.4 7.3

National Shipping Saudi Arabia 32.7 -3.3 1311.9 16.0

Combined Group Kuwait 1.22 -3.2 1.7 -4.7

Sharjah Islamic Abu Dhabi 1.9 -3.0 3954.6 26.0

Arabian Cement Saudi Arabia 3.5 -3.8 1262.9 7.3

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Al Ahli Bank 49.90 (2.2) 7,615.0 17.9

Widam Food Co. 49.00 (2.0) 279,410.0 -5.2

Qatar General Ins. & Reins. Co. 38.70 (0.8) 16,500.0 -3.0

Zad Holding Co. 71.60 (0.3) 6,710.0 3.0

United Development Co. 20.75 (0.2) 906,378.0 -3.6

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Barwa Real Estate Co 37.50 2.9 203,111.9 25.8

Gulf International Services OSC 86.30 9.9 162,450.0 76.8

Masraf Al Rayan 41.05 3.4 69,184.7 31.2

QNB Group 193.00 2.9 57,447.1 12.2

Industries Qatar QSC 188.50 1.1 55,409.7 11.6

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,905.94 2.3 3.7 2.3 14.7 286.39 181,729.0 15.1 1.9 4.1

Dubai 4,520.73 1.6 3.2 1.6 34.2 441.84 90,088.6 19.7 1.7 2.1

Abu Dhabi 4,954.22 1.2 2.0 1.2 15.5 173.33 131,325.0 14.8 1.8 3.7

Saudi Arabia 9,516.17 0.4 1.0 0.4 11.5 2,169.31 515,746.1 19.5 2.4 3.1

Kuwait 7,558.43 (0.2) (0.3) (0.2) 0.1 118.22 115,875.0 17.0 1.2 3.8

Oman 6,822.62 (0.5) (1.4) (0.5) (0.2) 22.28 24,502.8 11.3 1.6 3.9

Bahrain 1,360.21 0.2 1.4 0.2 8.9 2.39 51,615.6 9.6 0.9 5.1

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,600

11,700

11,800

11,900

12,000

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QE index rose 2.3% to close at 11,905.9. The Industrials

and Banking indices led the gains. The index rose on the back of

buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Gulf Warehousing Co. and Gulf International Services were the

top gainers, rising 10.0% and 9.9% respectively. Among the top

losers, Al Ahli Bank fell 2.2%, while Widam Food Co. declined

2.0%.

Volume of shares traded on Tuesday rose by 25.3% to 23mn

from 18.4mn on Monday. Further, as compared to the 30-day

moving average of 16.2mn, volume for the day was 42.9%

higher. Barwa Real Estate Co. and Vodafone Qatar were the

most active stocks, contributing 23.7% and 12.0% to the total

volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn)FY2013

% Change

YoY

Operating Profit

(mn) FY2013

% Change

YoY

Net Profit (mn)

FY2013

% Change

YoY

Majid Al Futtaim Dubai AED 23,000.0 10.0% – – 1,600.0 -0.6%

International Financial

Advisors

Kuwait KD 51.0 494.6% – – 2.9 N/A

Islamic Arab Insurance Co. Dubai AED 900.5 -46.4% – – -70.2 -82.2%

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

04/01 US Markit Markit US Manufacturing PMI March 55.5 56 55.5

04/01 US

Institute for Supply

Managemen

ISM Manufacturing March 53.7 54 53.2

04/01 US Bloomberg Total Vehicle Sales March 16.33M 15.80M 15.27M

04/01 EU Markit Markit Eurozone Manufacturing PMI March 53 53 53

04/01 EU Markit Markit EU Manufacturing PMI March 53.4 – 53.8

04/01 EU Eurostat Unemployment Rate February 11.90% 12.00% 11.90%

04/01 France Markit Markit France Manufacturing PMI March 52.1 51.9 51.9

04/01 Germany Deutsche Bundesbank Unemployment Change (000's) March -12K -10K -15K

04/01 Germany Deutsche Bundesbank Unemployment Rate March 6.70% 6.80% 6.70%

04/01 Germany Markit Markit/BME Germany Manu. PMI March 53.7 53.8 53.8

04/01 UK Markit Markit UK PMI Manufacturing SA March 55.3 56.7 56.2

04/01 Spain Markit Markit Spain Manufacturing PMI March 52.8 52.3 52.5

04/01 Italy Markit Markit/ADACI Italy Manufacturing PMI Mar 52.4 52 52.3

04/01 Italy ISTAT Unemployment Rate February 13.00% 12.90% 12.90%

04/01 China CFLP Manufacturing PMI March 50.3 50.1 50.2

04/01 China Markit HSBC China Manufacturing PMI March 48.0 48.1 48.1

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Qatar’s real GDP growth accelerated to 6.5% in 2013 on

strong investment and higher population – Qatar’s economy

continued to maintain its strong growth momentum in the fourth

quarter of 2013. Qatar’s real GDP expanded at a buoyant 5.6%

(year-on-year) in the last three months of 2013, spurred by

double-digit growth in construction, wholesale trade and

hospitality, and financial, real estate, and business services,

according to figures released by the Ministry of Development

Planning and Statistics (MDPS). For 2013 as a whole, real GDP

grew 6.5%, in line with QNB Group’s forecast (see Qatar

Economic Insight report). QNB Group expects real GDP growth

to accelerate to 6.8% in 2014 as the implementation of large

infrastructure projects and higher population continue to drive

double-digit growth in the non-hydrocarbon sector. The growth

figures for the fourth quarter of 2013 confirm the continued

process of economic diversification of Qatar’s economy away

from its traditional role as a hydrocarbon exporter toward a

manufacturing and services hub. The oil and gas sector

contracted by 1.1% year-on-year in 4Q2013, reflecting a fall in

oil production, the temporary halt of a number of LNG trains for

maintenance, as well as the moratorium on further exploration of

the North Field. At the same time, wholesale trade, hotels and

restaurants was the fastest growing sector (19.3% year-on-

year), predominantly on the back of the double-digit increase in

population. Financial, real estate, and business services was the

Overall Activity Buy %* Sell %* Net (QR)

Qatari 63.53% 72.58% (94,454,552.18)

Non-Qatari 36.48% 27.42% 94,454,552.18

3. Page 3 of 5

second fastest growing sector (18.1% year-on-year) as banking

intermediation accelerated and real estate services were

boosted by the growing population. Construction activity

expanded by 15.0% year-on-year as Qatar’s infrastructure

investment program is gathering momentum. (QNB Group,

Ministry of Development Planning and Statistics, Gulf-

Times.com)

QCB auctions t-bills worth QR4bn – Qatar Central Bank

(QCB) auctioned t-bills worth QR4bn, for which it received bids

totaling QR12.6bn. T-bills worth QR2bn, with a maturity period

of 3 months were auctioned at a yield of 0.68%. T-bills worth

QR1bn, with a maturity period of 6 months were sold at a yield

of 0.92%, while t-bills with a maturity period of 9 months were

auctioned at a yield of 0.97%. All the t-bills were issued on April

1, 2014. (QCB)

LR2 to enhance condensate refining capacity in 2016 – HH

the Emir Sheikh Tamim bin Hamad Al Thani laid the foundation

stone for the new Laffan Refinery (LR2) expansion project at

Ras Laffan, which will effectively double Qatar’s condensate

refining capacity. Being built at an estimated cost of QR5.5bn,

the LR2 project will raise capacity to 300,000 bpd after its

completion in 2016. LR2 is a JV among Qatar Petroleum (QP),

Total, Idemitsu, Cosmo, Marubeni and Mitsui, with QP holding

an 84% stake and Total holding 10%. As in the case of LR1,

LR2 will also be operated by Qatargas and will process 146,000

barrels per stream day (bpsd) of condensate feedstock. Both

LR1 and LR2 combined will make the Ras Laffan facility the

largest condensate refinery in the world. Upon completion of

LR2, Qatar will have the capacity to process nearly 40% of the

condensate from the North Field into high quality products.

(Gulf-Times.com)

ERES’ QR4.5bn Wakrah project will be ready by 2017 –

Ezdan Holding Group (ERES) said its QR4.5bn residential

project comprising 11,000 residential units in Al Wakrah will be

completed by 2017. The Group CEO Ali al-Obaidly said that the

housing project, which is being built in partnership with SAK

Holding Group, will be offered for the mass market and will be

completed in stages. He said the project assumes significance

against the backdrop of increasing expatriate population in view

of the mammoth projects being rolled out to upgrade the

country’s infrastructure ahead of the 2022 FIFA World Cup.

Moreover, ERES plans to acquire two more domestic

companies as part of its strategy to diversify its investment

portfolio. Meanwhile, ERES’ shareholders approved the

distribution of 3.1% cash dividend. (Gulf-Times.com)

Barwa Bank was IMLA for ERES’ 1st tranche of $500mn

syndication – Barwa Bank was the initial mandated lead

arranger (IMLA) for Ezdan Holding Group’s (ERES) first tranche

of its $500mn debut syndication, which was closed recently. In

late 2013, ERES took on a new direction by looking to

strategically diversify its business. ERES’ CEO Ali Al-Obaidly

said, aside from being the first 100% Islamic finance transaction

internationally syndicated for a Qatari corporate and led by a

Qatari bank, the response to the syndication shows a wide

acceptance of the company’s new business direction. (Gulf-

Times.com)

QTA: Qatar tourism grows further in 2013 – According to the

Qatar Tourism Authority (QTA), the tourism sector in Qatar

surged in 2013 as the country welcomed more than 1.3mn

visitors in 2013 as compared to 1.2mn in 2012. The full-year

figures showed that the country’s tourism industry has continued

its upward trajectory, benefiting from new investments and

promotion. QTA stated that the sector is on track to reach

growth targets set out in the Qatar National Tourism Sector

Strategy. (Gulf-Times.com)

QIBK to disclose 1Q2014 financials on April 16 – Qatar

Islamic Bank (QIBK) will disclose its 1Q2014 financial results on

April 16, 2014. (QE)

QOIS to disclose 1Q2014 results on April 20 – Qatar Oman

Investment Company (QOIS) will disclose its 1Q2014 financial

results on April 20, 2014. (QE)

SIIS to disclose 1Q2014 results on April 21 – Salam

International Investment (SIIS) will disclose its first quarter

financial results for the year 2014 on April 21, 2014. (QE)

International

Reuters: Solid US job growth expected for March as winter

fades – Job growth in the US is likely to have accelerated in

March 2014 as the winter's gloom started to lift, providing the

strongest signal yet that economic growth was shifting into

higher gear. According to a Reuters poll of economists, non-

farm payrolls probably increased by 200,000, which is the

largest gain in four months. Hiring advanced by 175,000 jobs in

February and the unemployment rate is expected to have

dropped to 6.6%. The anticipated gain in employment would

take job growth back near the 204,000 monthly average that

prevailed during the first 11 months of 2013. (Reuters)

Japan firms see inflation taking root in boost to BoJ –

Japanese companies forecasted that price gains will be

sustained over the next five years, indicating confidence in

Prime Minister Shinzo Abe’s bid to end deflation. The Bank of

Japan (BoJ) said inflation will grow up to 1.7% in 3 years time

after rising 1.5% over the next 12 months. Rising inflation

expectations were the strongest among small companies that

employ more than two-thirds of Japan’s workers and are feeling

a crunch from a tightening labor market. The progress in

shaking off deflationary malaise could reduce the chances of

additional monetary stimulus and fuel debate on how to manage

an economy with sustained price gains. (Bloomberg)

ECB finds no deflation as recovery gains – The European

Central Bank’s (ECB) Vice President Vitor Constancio said the

Eurozone is likely to avoid outright deflation as a soft economic

recovery gradually reduces spare capacity in the economy.

Constancio said the prospects for inflation are a cause for

concern, after figures showed Eurozone’s inflation had slowed in

March to 0.5%, the lowest level in more than four years. The

Frankfurt-based central bank will be soon have its monthly

monetary-policy meeting against a backdrop of improving

economic data with gains in prices lagging behind. ECB

President Mario Draghi has predicted that the recovery will

eventually push inflation toward the ECB’s target of around 2%.

(Bloomberg)

Regional

OPEC output falls due to Iraqi exports setback, African

outages – The OPEC’s oil output fell in March 2014 to its lowest

since December, as Iraq’s oil revival suffered a setback and

outages cut the output from African producers. According to the

survey based on shipping data and information from oil

company sources, supply from the OPEC averaged at 29.72mn

bpd, down from a revised 30.06mn bpd in February. A drop in

Iraq’s northern region exports, oilfield maintenance in Angola

and further unrest in Libya outweighed the extra volumes from

Saudi Arabia, Nigeria and a small rise in Iranian supplies. The

survey highlights the impact of unrest and outages on supply

from the group which pumps one-third of the world’s oil. (Gulf-

Times.com)

4. Page 4 of 5

Al Tayyar buys 70% in Hanouf Tourism – Al Tayyar Travel

Group Holding (Al Tayyar) has acquired 70% of Egypt-based

Hanouf Tourism & Services Company and its subsidiary

companies in a deal worth SR40.95mn. The deal was funded

from the company’s own resources. (GulfBase.com)

Dallah Health signs MoU to purchase Erfan Hospital –

Dallah Healthcare Holding Company has signed a MoU with

Bagedo Commercial Holding Company and Mohamed Ahmed

Erfan & Sons Holding Company to fully acquire their shares in

Bagedo & Dr. Erfan General Hospital Co. (GulfBase.com)

SAAC declares SR143.5mn dividend for 4Q2013 – Saudi

Arabian Airlines Catering Company’s (SAAC) AGM has

approved the distribution of 17.5% cash dividends (SR1.75 per

share), amounting to SR143.5mn for 4Q2013. (Tadawul)

ICD signs $6mn financing deal – The Islamic Corporation for

the Development of the Private Sector (ICD) has signed a

financing agreement with the Orienbank of Tajikistan for a $6mn

facility. The facility will be extended by Orienbank to SMEs for

financing projects in the industrial, communication, technology,

health, construction and agricultural sectors. (GulfBase.com)

Sipchem to stop Butaindiol plant for maintenance,

expansion – Saudi International Petrochemical Company

(Sipchem) has announced the stoppage of operations in its

Butaindiol plant from April 1, 2014 for 35 days duration for a

scheduled maintenance of all plant units and facilities. This

stoppage will be utilized to complete the tie-in of the expanded

units to the existing plant facilities. Due to this, the company is

expecting SR5mn financial impact on its 2Q2014 results.

(Tadawul)

EIB declares 8.33% bonus shares – Emirates Investment

Bank’s (EIB) AGM has approved its board’s proposal for

distributing 8.33% bonus shares for the year ended December

31, 2013. (DFM)

Abu Dhabi airport records 15.6% jump in passenger traffic –

According to the Abu Dhabi International Airport’s management,

the airport recorded a 15.6% increase in passenger traffic in

February 2014 as compared to February 2013. A total of 1.4mn

passengers used the airport as compared to 1.2mn in February

2013. The number of aircraft movements rose by 12.2% in

February 2014 to 11,174 as compared to 9,960 movements in

February 2013. Further, the cargo handling activity also rose to

56,902 tons, representing a 13.8% increase YoY.

(GulfBase.com)

HSBC Bank Oman appoints CEO – HSBC Bank Oman has

appointed Andrew Long as its Chief Executive Officer. Andrew

Long joins from HSBC Bank Egypt where he was the Deputy

Chairman and CEO. (MSM)

SMNP declares 20% dividend, appoints chairman – SMN

Power Holding Company’s (SMNP) AGM has approved its

board’s proposal for the distribution of 20% cash dividend (200

baizas per share) for the year ended December 31, 2013.

Meanwhile, the company has appointed Johan Van Kerrebroeck

as the Chairman of the Board of Directors and Abdullah Humaid

Al Yahya’ey as the Vice Chairman. (MSM)

Ominvest declares 15% cash dividend, 10% stock dividend

– Oman International Development & Investment Company’s

(Ominvest) AGM has approved the distribution of 15% cash

dividend (15 baizas per share) for the year ended December 31,

2013. Further, the company’s AGM has approved the

distribution of 10% stock dividend for 2013. This will increase

the paid-up share capital from OMR30.6mn (306.13mn shares)

to OMR33.7mn (336.7mn shares), with a nominal value of 100

baizas per share. (MSM)

GFIH declares 5% interim dividend – Global Financial

Investments Holding’s (GFIH) AGM has approved the board’s

proposal to distribute an interim cash dividend, not exceeding

5% (equivalent to 5 baizas per share) to its shareholders. (MSM)

GIS declares 15% dividend for 2013 – Gulf Investment

Services Holding Company’s (GIS) AGM has approved the

distribution of 15% cash dividend (15 baizas per share) for the

year ended December 31, 2013. (MSM)

ACWA Power Barka declares 50% interim dividend,

appoints chairman, deputy chairman – ACWA Power Barka’s

AGM has authorized the board of directors to distribute 50%

interim dividend (50 baizas per share) for 2014. Meanwhile, the

company has appointed Mohammad Abdullah Abunayyan as

the Chairman and Rohit Gokhale as the Deputy Chairman of the

board of directors. (MSM)

Takaful declares 5% dividend for 2013 – Takaful International

Company’s AGM has approved the board’s proposal for the

distribution of 5% cash dividend (5 fils per share) for the year

ended December 31, 2013. (Bahrain Bourse)

5. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

0.4%

2.3%

(0.2%)

0.2%

(0.5%)

1.2%

1.6%

(2.0%)

0.0%

2.0%

4.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,278.95 (0.4) (1.3) 6.1 DJ Industrial 16,532.61 0.5 1.3 (0.3)

Silver/Ounce 19.76 (0.1) (0.3) 1.5 S&P 500 1,885.52 0.7 1.5 2.0

Crude Oil (Brent)/Barrel (FM

Future)

105.62 (2.0) (2.3) (4.7) NASDAQ 100 4,268.04 1.6 2.7 2.2

Natural Gas (Henry

Hub)/MMBtu

4.35 (2.7) (3.0) 0.1 STOXX 600 336.35 0.6 0.8 2.5

LPG Propane (Arab Gulf)/Ton 105.75 (0.5) (0.5) (16.4) DAX 9,603.71 0.5 0.2 0.5

LPG Butane (Arab Gulf)/Ton 120.75 (0.2) (0.4) (11.0) FTSE 100 6,652.61 0.8 0.6 (1.4)

Euro 1.38 0.2 0.3 0.4 CAC 40 4,426.72 0.8 0.4 3.0

Yen 103.65 0.4 0.8 (1.6) Nikkei 14,791.99 (0.2) 0.7 (9.2)

GBP 1.66 (0.2) (0.0) 0.4 MSCI EM 1,000.79 0.6 1.6 (0.2)

CHF 1.13 0.1 0.4 1.1 SHANGHAI SE Composite 2,047.46 0.7 0.3 (3.2)

AUD 0.92 (0.2) 0.0 3.7 HANG SENG 22,448.54 1.3 1.7 (3.7)

USD Index 80.09 (0.0) (0.1) 0.1 BSE SENSEX 22,446.44 0.3 0.5 6.0

RUB 35.08 (0.3) (1.9) 6.7 Bovespa 50,270.37 (0.3) 1.0 (2.4)

BRL 0.44 0.4 (0.0) 4.4 RTS 1,235.74 0.8 4.2 (14.3)

171.1

149.9

136.2