🔝+919953056974 🔝young Delhi Escort service Pusa Road

21 April Daily market report

1. Page 1 of 6

QSE Intra-Day Movement

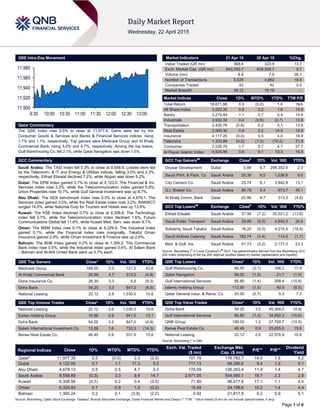

Qatar Commentary

The QSE Index rose 0.5% to close at 11,977.4. Gains were led by the

Consumer Goods & Services and Banks & Financial Services indices, rising

1.7% and 1.1%, respectively. Top gainers were Medicare Group and Al Khalij

Commercial Bank, rising 5.0% and 4.7%, respectively. Among the top losers,

Gulf Warehousing Co. fell 2.1%, while Qatar Navigation was down 1.5%.

GCC Commentary

Saudi Arabia: The TASI Index fell 0.3% to close at 9,558.9. Losses were led

by the Telecomm. & IT and Energy & Utilities indices, falling 3.0% and 2.3%,

respectively. Etihad Etisalat declined 7.2%, while Alujain was down 5.2%.

Dubai: The DFM Index gained 0.7% to close at 4,123.0. The Financial & Inv.

Services index rose 2.2%, while the Telecommunication index gained 0.8%.

Union Properties rose 10.7%, while Gulf General Investment was up 8.7%.

Abu Dhabi: The ADX benchmark index rose 0.5% to close at 4,679.1. The

Services index gained 3.5%, while the Real Estate index rose 3.2%. RAKWCT

surged 14.5%, while National Corp for Tourism and Hotels was up 13.9%.

Kuwait: The KSE Index declined 0.7% to close at 6,308.6. The Technology

index fell 2.7%, while the Telecommunication index declined 1.6%. Future

Communications Global fell 11.6%, while Kuwait Med. Serv. was down 9.1%.

Oman: The MSM Index rose 0.1% to close at 6,329.9. The Industrial index

gained 0.1%, while the Financial index rose marginally. Takaful Oman

Insurance gained 2.9%, while Oman Investment & Finance was up 2.6%.

Bahrain: The BHB Index gained 0.2% to close at 1,395.2. The Commercial

Bank index rose 0.5%, while the Industrial index gained 0.4%. Al Salam Bank

– Bahrain and Al-Ahli United Bank were up 0.7% each.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Medicare Group 168.00 5.0 121.5 43.6

Al Khalij Commercial Bank 20.99 4.7 313.3 (4.8)

Doha Insurance Co. 26.30 3.3 5.9 (9.3)

Doha Bank 54.20 3.0 847.0 (4.9)

National Leasing 22.12 2.6 1,030.0 10.6

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

National Leasing 22.12 2.6 1,030.0 10.6

Ezdan Holding Group 16.88 0.9 941.0 13.1

Doha Bank 54.20 3.0 847.0 (4.9)

Salam International Investment Co. 13.59 1.6 733.3 (14.3)

Barwa Real Estate Co. 48.45 0.9 531.9 15.6

Market Indicators 21 Apr 15 20 Apr 15 %Chg.

Value Traded (QR mn) 368.4 323.9 13.7

Exch. Market Cap. (QR mn) 643,782.7 639,505.7 0.7

Volume (mn) 8.9 7.0 26.1

Number of Transactions 5,525 4,662 18.5

Companies Traded 42 42 0.0

Market Breadth 28:12 19:18 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,611.86 0.5 (0.0) 1.6 N/A

All Share Index 3,202.35 0.6 0.2 1.6 14.6

Banks 3,215.44 1.1 0.7 0.4 14.4

Industrials 3,932.32 0.2 (0.6) (2.7) 13.8

Transportation 2,435.76 (0.8) 0.2 5.1 13.6

Real Estate 2,569.30 0.8 0.2 14.5 14.6

Insurance 4,117.25 (0.0) 0.5 4.0 18.9

Telecoms 1,333.86 (0.2) (1.2) (10.2) 21.8

Consumer 7,228.70 1.7 0.7 4.7 27.7

Al Rayan Islamic Index 4,524.86 0.6 0.1 10.3 16.5

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Deyaar Development Dubai 0.88 6.7 296,352.4 2.9

Saudi Print. & Pack. Co Saudi Arabia 20.39 6.5 1,036.6 9.0

City Cement Co. Saudi Arabia 25.74 6.1 3,842.8 13.1

G.I. Shaker Co. Saudi Arabia 86.79 5.4 973.7 45.1

Al Khalij Comm. Bank Qatar 20.99 4.7 313.3 (4.8)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Etihad Etisalat Saudi Arabia 37.94 (7.2) 35,031.2 (13.6)

Saudi Public Transport Saudi Arabia 29.89 (5.0) 4,843.3 24.5

Solidarity Saudi Takaful Saudi Arabia 16.20 (5.0) 4,215.4 (18.6)

Saudi Airlines Catering Saudi Arabia 182.74 (3.4) 114.5 (1.7)

Med. & Gulf. Ins. Saudi Arabia 61.73 (3.2) 2,177.0 23.3

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Gulf Warehousing Co. 66.50 (2.1) 166.2 17.9

Qatar Navigation 98.00 (1.5) 21.7 (1.5)

Gulf International Services 86.80 (1.4) 398.4 (10.6)

Islamic Holding Group 113.90 (1.0) 40.0 (8.5)

Qatar General Insur. & Reins. Co. 55.00 (0.7) 5.3 7.2

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Doha Bank 54.20 3.0 45,266.0 (4.9)

Gulf International Services 86.80 (1.4) 34,992.3 (10.6)

QNB Group 190.50 1.2 27,759.7 (10.5)

Barwa Real Estate Co. 48.45 0.9 25,655.0 15.6

National Leasing 22.12 2.6 22,576.9 10.6

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,977.35 0.5 (0.0) 2.3 (2.5) 101.19 176,782.7 14.0 1.9 4.2

Dubai 4,122.95 0.7 1.1 17.3 9.2 717.13 99,286.6 9.4 1.6 5.1

Abu Dhabi 4,679.13 0.5 0.5 4.7 3.3 178.09 126,363.4 11.9 1.4 4.7

Saudi Arabia 9,558.89 (0.3) 3.3 8.9 14.7 2,671.05 554,080.1 19.7 2.3 2.8

Kuwait 6,308.56 (0.7) 0.2 0.4 (3.5) 71.80 96,017.8 17.1 1.1 4.0

Oman 6,329.93 0.1 0.9 1.5 (0.2) 15.49 24,198.6 10.2 1.4 4.4

Bahrain 1,395.24 0.2 0.1 (3.8) (2.2) 0.92 21,817.5 9.2 0.9 5.1

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,900

11,920

11,940

11,960

11,980

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index rose 0.5% to close at 11,977.4. The Consumer

Goods & Services and Banks & Financial Services indices led

the gains. The index rose on the back of buying support from

non-Qatari shareholders despite selling pressure from Qatari and

GCC shareholders.

Medicare Group and Al Khalij Commercial Bank were the top

gainers, rising 5.0% and 4.7%, respectively. Among the top

losers, Gulf Warehousing Co. fell 2.1%, while Qatar Navigation

was down 1.5%.

Volume of shares traded on Tuesday rose by 26.1% to 8.9mn

from 7.0mn on Monday. Further, as compared to the 30-day

moving average of 8.1mn, volume for the day was 9.6% higher.

National Leasing and Ezdan Holding Group were the most active

stocks, contributing 11.6% and 10.6% to the total volume,

respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn) 1Q2015

% Change

YoY

Operating Profit

(mn) 1Q2015

% Change

YoY

Net Profit (mn)

1Q2015

% Change

YoY

Kingdom Holding Co.

(Kingdom)

Saudi Arabia SR – – 250.2 -0.1% 139.4 10.3%

Mobile Telecommunications

Company Saudi Arabia

(ZAIN KSA)

Saudi Arabia SR – – -59.0 NA -257.0 NA

Tihama Advertising & Public

Relations Co. (TAPRCO)

Saudi Arabia SR – – 2.5 NA 1.6 NA

Abdullah Al Othaim Markets

Co. (A.Othaim Market)

Saudi Arabia SR – – 42.3 -1.0% 48.9 5.2%

Saudi Fisheries Co. (SFICO) Saudi Arabia SR – – -9.0 NA -11.0 NA

Al-Ahlia Insurance Co. (Al-

Ahlia)

Saudi Arabia SR 60.2 -29.1% – – 0.5 6.4%

Saudi Paper Manufacturing

Co. (SPM)

Saudi Arabia SR – – 15.3 -5.6% 4.9 -40.2%

Saudia Dairy and Foodstuff.

Co. (SADAFCO)

Saudi Arabia SR – – 33.9 -37.0% 29.4 -44.9%

Arabian Pipes Co. (APC) Saudi Arabia SR – – 0.4 NA -6.3 NA

Qassim Agriculture Co.

(GACO)

Saudi Arabia SR – – -2.8 NA -3.0 NA

Saudi Industrial Services Co.

(SISCO)

Saudi Arabia SR – – 35.9 32.8% 18.5 49.3%

Etihad Etisalat Co. (Mobily) Saudi Arabia SR – – -104.0 NA -199.0 NA

Arabian Aramco Total

Services Co. (SATROP)

Saudi Arabia SR – – 662.7 NA 472.4 NA

Saudi Electricity Co. (Saudi

Electric.)

Saudi Arabia SR – – -1,402.0 NA -1,940.0 NA

Amana Cooperative

Insurance Co. (Amana

Insurance)

Saudi Arabia SR 35.6 -62.7% – – -25.9 NA

Al Jouf Cement Co. (Jouf

Cement)

Saudi Arabia SR – – 28.3 55.8% 25.8 71.6%

The Mediterranean and Gulf

Insurance and Reinsurance

Co. (MEDGULF)

Saudi Arabia SR 1,299.6 44.1% – – -52.4 NA

Solidarity Saudi Takaful Co.

(Solidarity)

Saudi Arabia SR 69.2 77.5% – – -64.0 NA

Al-Baha Investment and

Development Co. (Al-baha)

Saudi Arabia SR – – – – 0.0 NA

Saudi Cable Co. (SCC) Saudi Arabia SR – – -15.8 NA -7.9 NA

Al-Babtain Power

&Telecommunication Co.

(Al-Babtain)

Saudi Arabia SR – – 31.5 25.0% 26.3 18.5%

Middle East Specialized

Cables Co. (MESC)

Saudi Arabia SR – – 3.0 NA -3.0 NA

Takween Advanced

Industries

Saudi Arabia SR – – -21.4 NA -15.5 NA

Mohammad Al Mojil Group

Co. (MMG)

Saudi Arabia SR – – -105.1 NA -110.5 NA

Orient Insurance Dubai AED 147.9 19.5% 61.1 30.9% 117.8 8.6%

Aramex Dubai AED 930.0 9.2% – – 86.6 10.0%

Overall Activity Buy %* Sell %* Net (QR)

Qatari 56.87% 57.57% (2,594,026.04)

GCC 8.32% 11.51% (11,744,261.29)

Non-Qatari 34.81% 30.92% 14,338,287.33

3. Page 3 of 6

Abu Dhabi National Energy

Co. (TAQA)

Abu Dhbai AED 27,325.0 6.1% – – -2,289.0 NA

Hotels Management

Company International

Oman OMR – – – – 1.3 -5.0%

Oman Fiber Optic Co. (OFO) Oman OMR 4.3 -23.7% – – 0.2 -29.9%

Salalah Mills Co. (SMC) Oman OMR 16.3 -1.1% – – 1.3 -29.8%

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

04/21 EU Eurostat Govt Debt/GDP Ratio 6-July 91.90% – 90.90%

04/21 EU ZEW ZEW Survey Expectations April 64.8 – 62.4

04/21 Germany ZEW ZEW Survey Current Situation April 70.2 56.5 55.1

04/21 Germany ZEW ZEW Survey Expectations April 53.3 55.3 54.8

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QATI reports 33.6% QoQ surge in 1Q2015 net profit – Qatar

Insurance Company (QATI) posted a net profit of QR296.62mn

in 1Q2015, in-line with our estimate of QR302mn (variation of

1.7%). Conversely, the profit was down 11.7% on YoY basis,

despite net earned premiums and net underwriting results

registering a growth of 25.4% and 10.9% YoY to QR1,017.8mn

and QR247.6mn, respectively. However, the 21.7% YoY drop

recorded in investment income to QR178.7mn primarily resulted

in YoY profit decline. The EPS amounted to QR1.61 in 1Q2015

as compared to QR1.82 in 1Q2014. (QSE)

QIIK reports net profit of QR212mn in 1Q2015 – Qatar

International Islamic Bank (QIIK) reported a net profit of

QR212.3mn (+5.7% and +4.0 QoQ and YoY, respectively) in

1Q2015, in-line with our estimate of QR212.3mn. The primary

driver of growth was the reversal of provisions. The bank’s total

loans grew by 6.1% YTD to QR23.2bn, while deposits dropped

by 5.5% YTD to QR25.2bn. Thus, the LDR was lifted to 92% vs.

82% at the end of 2014. QIIK’s NPL ratio decreased to 0.96%

vs. 0.98% at the end of 2014. The bank’s cost to income ratio

remained unchanged YoY at 23.1% (4Q2014: 31.9%). QIIK’s

capital adequacy under Basel III reached 18.49%. (QNBFS

Research, Company Financials)

QEWS posts QR346mn net income in 1Q2015 – Qatar

Electricity & Water Company (QEWS) revealed a net profit of

QR346mn in 1Q2015 as compared to QR299mn in 1Q2014.

The EPS stood at QR3.15 in 1Q2015 versus QR2.69 in 1Q2014.

(QSE)

MPHC’s net profit plunges 74.9% YoY to QR116.2mn in

1Q2015 – Mesaieed Petrochemical Holding Company’s (MPHC)

net profit plunged 74.9% YoY to QR116.2mn in 1Q2015, driven

by planned major maintenance shutdowns and due to weak

product prices. The EPS stood at QR0.09 in 1Q2015 versus

QR0.37 in 1Q2014. (QSE)

MCGS discloses QR49.4mn net profit in 1Q2015 – Medicare

Group (MCGS) reported a net profit of QR49.4mn in 1Q2015 as

compared to QR34.1mn in 1Q2014. The EPS amounted to

QR1.75 in 1Q2015 versus QR1.21 in 1Q2014. (QSE)

SIIS profitability soars 166.8% QoQ in 1Q2015 – Salam

International Investment Limited’s (SIIS) operating Income

increased by 6.6% QoQ (up 10.9% YoY) in 1Q2015 while the

bottom-line soared 166.8% QoQ to QR29.6mn (up 11.2% YoY)

in 1Q2015. Consequently, the EPS rose to QR0.26 in 1Q2015

from QR0.23 in 1Q2014. (QSE)

KCBK sells first-ever privately placed MTNs – Al Khalij

Commercial Bank (KCBK) has sold its first ever privately placed

medium term notes (MTNs) on April 21, 2015. The issuer placed

a pair of short dated floating rate MTNs through Commerzbank.

KCBK raised $15mn with an April 2016 note, which pays a

coupon of quarterly dollar Libor plus 49 basis points (bps), and a

€10mn three year, paying three month Euribor plus 36bps. The

deals were priced at par. (Bloomberg)

QCSD raises QGRI’s foreign ownership to 49% – The Qatar

Central Securities Depository (QCSD) has amended the foreign

ownership in the Qatar General Insurance & Reinsurance

Company’s (QGRI) shares, taking it to 49% of the total capital

effective from April 22, 2015. This amendment is pursuant to

Law no. 9 that allows non-Qatari investors to own shares in

listed companies by no more than 49% of a company’s

capital. This move comes after QGRI received an approval in

this regard from its general assembly to amend the Articles of

Association in line with the regulatory provisions, as well as an

approval from the Ministry of Economy & Commerce on the

amendment. (QSE)

Real estate deals peak at QR3.2bn – According to statistics

released by the Land Registry office of the Ministry of Justice,

the aggregate value of property transactions in Qatar soar to a

record high of QR3.2bn in less than a fortnight from April 5 to

16, led by the three major deals struck earlier in April 2015. Data

showed that the total value of just three deals, including a tower

in Al Dafna, was over QR1.43bn, or nearly half of the fortnight’s

total. The Dafna tower measuring 2,472 square meters was sold

out for QR936mn. A residential complex in Al Wakra fetched its

owners QR400mn, while another residential complex in

Ummghuwalina in Doha got its owners QR100mn. (Peninsula

Qatar)

MRDS AGM endorses agenda, EGM postponed to April 27 –

Mazaya Qatar Real Estate Development Company’s (MRDS)

ordinary general assembly meeting (AGM) has approved its

agenda, including the proposal to distribute 3% cash dividend

i.e. QR0.3 per share, and 5% bonus shares (5 shares for each

100 shares). Meanwhile, MRDS’ extraordinary general assembly

meeting (EGM) has been postponed due to a lack of quorum.

The next meeting will be held on April 27, 2015. (QSE)

Qatar Rail completes 20% tunnel work for Doha metro –

Qatar Railways Company (Qatar Rail) has completed digging

nearly 20% of tunnels i.e. 18.6 kilometers (km) for the Doha

Metro project. Qatar Rail had already received the 21 tunnel

boring machines (TBMs) assigned for the project, after being

imported from German company Herrenknecht. Most of Qatar

Rail TBMs are currently operational, with tunneling phase

expected to be completed by 2Q2017. Meanwhile, Qatar Rail

has assured that the operation of tunnel boring machines

4. Page 4 of 6

(TMBs) deployed for the Doha Metro project will not pose any

safety hazard to people and establishments above ground.

Furthermore, Qatar Rail has placed orders for about 70 ‘train

sets’ (coaches and at least one engine make a train set) from a

Japanese consortium. (Bloomberg, Gulf-Times.com, Peninsula

Qatar)

International

ZEW: German economic sentiment drops unexpectedly in

April – The ZEW indicator of German economic sentiment fell to

53.3 points in April 2015 from 54.8 in March, recording its first

fall since October 2014. ZEW said the world economy was

dampening Germany's export prospects and reducing the

potential for further improvement, and some economists also

cited concerns about Greece's debt crisis as a factor in

investors' weaker expectations. However, ZEW economists said

the investors surveyed expected the good situation to continue

for at least the next half year and noted that German private

consumption, seen as the mainstay of growth in 2015, would

strengthen further. (Reuters)

Greece hopes to reach deal on Russian gas pipeline soon –

Greece hopes that it would soon reach a deal with Russian gas

giant Gazprom on a pipeline that will bring Russian gas to

Europa via its territory. Greek Energy Minister Panagiotis

Lafazanis said Greece is continuing talks with the Russian side

and hopes to reach an agreement very soon. Gazprom's Chief

Executive Officer, Alexei Miller said Gazprom would pump up to

47 billion cubic meters (bcm) of gas via Greece through the

pipeline, which would be implemented strictly according to the

EU law. However, Russia denied a German media report on

April 18 that suggested the gas pipeline deal could add up to

€5bn to Athens' depleted state coffers. (Reuters)

Japan reports first trade surplus in three years – Japan

posted its first trade surplus in nearly three years in March 2015

as exports of cars and electronics picked up, an encouraging

sign that the economic growth may be back on track after a

sluggish start to the year. Exports rose at an annual rate of 8.5%

in March while imports by value tumbled 14.5% weighed down

by lower oil prices, leaving Japan with a trade surplus of

¥229.3bn for the first time since June 2012. Exports to China,

Japan's largest trading partner, rose 3.9% YoY in March

whereas exports to Asia rose an annual 6.7%. Shipments to the

US rose 21.3% in the year to March, faster than a 14.3% gain in

the previous month as Japan sent more cars to the world's

largest economy. (Reuters)

China pledges proactive employment policy as economy

slows – China's cabinet pledged to implement more proactive

employment policies to cope with the rising pressures on job

creation. The State Council said the government would take

steps, including giving tax breaks for firms set up by college

graduates and unemployed people, to help create more jobs.

The government will also support companies if they refrain from

laying off workers via the unemployment insurance scheme and

also help rural migrant workers to start new businesses. The

government's pledge to boost employment came after data

showed China's annual economic growth slowed to a six-year

low of 7% in 1Q2015. (Reuters)

Australia’s core inflation matches forecast; leaves rate-cut

scope – Australia’s core consumer prices advanced 0.6% QoQ

in 1Q2015, matching economists’ forecasts and providing scope

for the central bank to reduce interest rates. The consumer price

index rose 0.2% QoQ and 1.3% YoY. The Reserve Bank of

Australia (RBA) aims for inflation between 2 and 3% on an

average. The RBA has left the key rate unchanged over the past

two months after cutting to a record 2.25% in February.

Moreover, Australia’s jobless rate fell to 6.1% in March as

employers boosted hiring, spurring optimism the RBA’s effort to

shore up the economy is paying off. (Bloomberg)

Regional

Sipchem announces startup of PBT plant – Saudi

International Petrochemical Company (Sipchem) has

announced the startup of the Polybutylene Terephthalate plant

(PBT) at its complex in Jubail Industrial City. The plant is owned

by Sipchem Chemical Company (SCC), an affiliate of Sipchem,

which will produce 63,000 metric tons of polybutylene

terephthalate, a highly-specialized, thermal engineering polymer

used in the automotive industry and the production of electrical

and electronic materials. The move followed the successful

testing of the plant equipment. The total project cost is around

SR600mn, where Sipchem owns 95% of SCC’s capital, while

the remaining stake is held by Sipchem Marketing Company.

(Tadawul)

RSHS’ AGM approves SR60mn cash dividends for 2014 –

Red Sea Housing Services Company’s (RSHS) ordinary general

assembly meeting (AGM) has approved the distribution SR60mn

as cash dividends (SR1 per share) for 2014, representing 10%

of the nominal share value. Shareholders, who are registered

with the Securities Depository Center (Tadawul) on April 20,

2015, will be eligible to receive the dividend. (Tadawul)

Tasnee to cut costs, revise contracts after 1Q2015 loss –

National Industrialization Company (Tasnee) said that it would

cut costs and revise foreign exchange and derivatives contracts

at a subsidiary after swinging to a loss of SR332.5mn in

1Q2015. (GulfBase.com)

Marafiq selects DEC to enhance training services – Marafiq

Power & Water Utility Company has contracted Doble

Engineering Company (DEC), a subsidiary of ESCO

Technologies to provide consulting & training services for

supporting reliable best practices within its transmission &

distribution division. DEC will maintain a strong presence in the

region, working hand-in-hand with the Marafiq team on

implementation, supported by a team of Doble apparatus

specialists. (GulfBase.com)

AHAB to put revised debt proposal to creditors – Saudi-

based Ahmad Hamad Algosaibi & Brothers (AHAB) will put an

improved offer to its creditors in a fresh attempt to reach a

settlement. AHAB has liabilities to banks and financial

institutions worth around $6bn, which it disclosed in May 2014,

when it made an initial offer to repay creditors a minimum of 20

cents on every dollar owed. AHAB said it had agreed with the

steering committee, the five-member group charged with

negotiating on the behalf of creditors, to present improved

settlement terms to the full claimant group. The five-member

steering committee comprises Arab Banking Corporation, BNP

Paribas, Emirates NBD, Fortress Investment Group and

Standard Chartered. (Reuters)

Etisalat, Al Falak to develop video monitoring solution –

Emirates Telecommunications Corporation (Etisalat) has

selected Al-Falak Electronic Equipment & Supplies Company to

provide a comprehensive video monitoring solution to analyze

the quality of service and user experience. (GulfBase.com)

Dubai Crown Prince approves Islamic economy initiatives –

Dubai Crown Prince and the Chairman of Dubai Executive

Council Shaikh Hamdan Bin Mohammad bin Rashid Al Maktoum

has approved a series of initiatives proposed by the board of

Dubai Islamic Economy Development Centre (DIEDC). The

initiatives include the launch of the second Islamic Economy

Index, the third edition of the Islamic Economy Award, the

5. Page 5 of 6

second Global Islamic Economy Summit and the release of the

third State of Global Islamic Economy Report. As part of the

plans for 2015, DIEDC will seek collaborations with international

museums to position Dubai as the capital of Islamic fashion, art

and design. (Gulfbase.com)

Nakheel invites bids for Dubai mixed-use project – Nakheel

has invited tenders for the development of the retail component

at Warsan Village, a family-oriented neighborhood containing

942 three-bedroom modern townhouses on the southwestern

corner of the International City in Dubai. Nakheel has invited

bids for two zones within Warsan Souk involving the

development of around 1,160 retail units, 52 food & beverage

outlets and 333 town houses. The last date for submitting the

tenders has been set for May 13, 2015. (GulfBase.com)

Noor Bank tightens guidance for $500mn debut Sukuk

issue – Noor Bank has tightened the pricing guidance for its

$500mn, five-year, debut US dollar Sukuk issue. The bank has

revised the guidance to 130-135 basis points (bps) over

midswaps, from the 140 bps area indicated earlier on April 21,

2015. Order books for the transaction are in the vicinity of

$1.9bn and include $900mn interest from the lead managers.

Noor Bank has chosen Standard Chartered as the global

coordinator and Al Hilal Bank, Barwa Bank, Citigroup, Dubai

Islamic Bank, Emirates NBD, Qinvest and Sharjah Islamic Bank

as joint lead managers for the issue. (Reuters)

ADCB’s net profit surges 31% YoY to AED1.25bn in 1Q2015

– Abu Dhabi Commercial Bank (ADCB) reported a net profit of

AED1.25bn in 1Q2015, reflecting an increase of 31% YoY and

22% QoQ. The bank’s net fees & commission income reported a

significant growth, up 32% YoY to reach AED375mn in 1Q2015.

This was primarily attributable to higher corporate banking fees,

up 46% YoY at AED157mn, and higher retail banking fees, up

13% YoY at AED220mn. ADCB’s total assets stood at

AED206.89bn in 1Q2015 as compared to AED186.1bn in

1Q2014. EPS amounted to AED0.23 in 1Q2015 versus

AED0.16 in 1Q2014. Net loans & advances reached to

AED141.1bn, while customer deposits stood at AED128.47bn.

As at March 31, 2015, the bank was a net lender of AED18bn in

the interbank market, and the liquidity ratio improved to 25.5%

from 22.9% as at March 31, 2014. The cost-to-income ratio for

the quarter improved to 31.9% as compared to 32.9% in

1Q2014. (ADX)

ADNOC still in talks with companies on oil concessions –

Abu Dhabi National Oil Company’s (ADNOC) Director General,

Abdulla Nasser Al Suwaidi said that the company is still in talks

with international companies about concessions at the Emirate’s

largest fields and has not set a deadline for deciding on the

awards. Meanwhile, ADNOC’s Offshore Division Manager,

Qasem Al-Kayoumi said that Abu Dhabi is planning to invest

over $25bn in the next five years on boosting its oil production

capacity from offshore fields. ADNOC’s current plan is to reach

3.5mn barrels per day (bpd) and to sustain it. He said that the

company is planning to drill around 160 wells per year in the

next couple of years. (GulfBase.com, Reuters)

Gulf Bank posts 12% YoY rise in net profit in 1Q2015 –

Kuwait’s Gulf Bank reported a net profit of KD9.8mn in 1Q2015,

showing an increase of 12% YoY. The bank’s operating profit

before provisions rose by 15% to KD27.2mn in 1Q2015 from

KD23.6mn in 1Q2014, mainly due to an increase in net interest

income by 9%. The bank's key metrics have also witnessed

strong growth, which contributed to the overall improvement in

the bank’s performance. The capital adequacy ratio as per Basel

III norms is at 15.2% against the regulatory requirement of

12.5%. The bank's non-performing loans (NPL) ratio also

continued to improve to 3% at the end 1Q2015, decreasing from

6.5 % at the beginning of 2014. The NPL coverage ratio also

increased to 290% at 1Q2015-end against the 187% coverage

at the beginning of 2014. (Zawya)

NBO signs construction contract with Al Turki Enterprises –

The National Bank of Oman (NBO) has signed a contract with Al

Turki Enterprises, a construction company, to build a new head

office in Athaiba. The project is estimated to be valued at

OMR50mn and expected to open in 2Q2017. The new building

will be of nine storeys and will provide approximately 50,000

square meters of high-quality office space and support facilities

for the bank, as it enters a new growth phase. Spread over two

basements, the building will also have a massive car parking

facility that can accommodate around 560 cars at any point of

time. (GulfBase.com)

Bank Sohar announces closure of trading rights – Bank

Sohar had announced that April 21, 2015 was the last day for

trading of its rights entitlements within the ongoing rights issue

currently open for subscription till April 29, 2015. (MSM)

BP eyes 1 bcf gas output from Khazzan field by 2017 –

British Petroleum (BP) could start natural gas production from

Oman's Khazzan field by 2017 at a rate of 1bn cubic feet (bcf) a

day. BP Middle East’s President, Michael Townshend said that

the company is planning to drill 20 wells in 2015, boosting it to

50 wells in the next couple of years, and is already building a

plant to handle the produced gas. He said that the total

investment in the first phase to reach the initial gas production

target will be $16bn. Earlier, BP has said it expects to invest

around $9.6bn, in accordance with its 60% stake in the project,

while the Oman Oil Company Exploration & Production holds

the remaining 40% stake. (GulfBase.com)

Ithraa, MoCI signs pact to attract inward investment in

Oman – Ithraa and the Ministry of Commerce & Industry (MoCI)

have signed a MoU that takes Oman's efforts to attract and

facilitate inward investment to a new height. The MoU has been

designed to improve Oman's business climate by streamlining

inward investment processes and simplifying regulations for

inward investors. The agreement grants Ithraa the authority to

manage inward investment of OMR10mn and above. (Gulf)

AUB sets IPTs for benchmark dollar Tier 1 bond – Ahli

United Bank (AUB) has set the initial price thoughts (IPTs) for a

benchmark US dollar-denominated bond in the low 7% area.

AUB expects the bond boost its Tier 1 (core) capital. The bank

has hired Goldman Sachs, HSBC and Morgan Stanley to

arrange investor meetings for the bonds. The perpetual, non-call

five deal, at present has commitments from lead arrangers worth

$375mn. (Reuters)

6. Contacts

Saugata Sarkar Ahmed Al-Khoudary Sahbi Kasraoui

Head of Research Head of Sales Trading – Institutional Head of HNI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6548 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (

#

Market closed on April 21, 2015) Source: Bloomberg (*$ adjusted returns;

#

Market closed on April 21, 2015)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

QSE Index S&P Pan Arab S&P GCC

(0.3%)

0.5%

(0.7%)

0.2% 0.1%

0.5%

0.7%

(1.2%)

(0.6%)

0.0%

0.6%

1.2%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,202.34 0.5 (0.2) 1.5 MSCI World Index 1,781.95 0.2 0.7 4.2

Silver/Ounce 16.03 0.4 (1.5) 2.1 DJ Industrial 17,949.59 (0.5) 0.7 0.7

Crude Oil (Brent)/Barrel (FM

Future)

62.08 (2.2) (2.2) 8.3 S&P 500 2,097.29 (0.1) 0.8 1.9

Crude Oil (WTI)/Barrel (FM

Future)

55.26 (2.0) (0.9) 3.7 NASDAQ 100 5,014.10 0.4 1.7 5.9

Natural Gas (Henry

Hub)/MMBtu

2.57 0.8 (2.6) (14.3) STOXX 600 409.12 0.6 1.1 6.2

LPG Propane (Arab Gulf)/Ton#

56.50 0.0 (1.3) 15.3 DAX 11,939.58 0.4 1.9 7.7

LPG Butane (Arab Gulf)/Ton#

66.62 0.0 (1.7) 1.7 FTSE 100 7,062.93 0.5 1.1 3.3

Euro 1.07 (0.0) (0.6) (11.3) CAC 40 5,192.64 0.1 0.7 8.0

Yen 119.67 0.4 0.6 (0.1) Nikkei 19,909.09 1.3 0.8 14.0

GBP 1.49 0.1 (0.2) (4.2) MSCI EM 1,042.21 0.8 (0.0) 9.0

CHF 1.05 0.1 (0.3) 4.1 SHANGHAI SE Composite 4,293.62 1.7 0.1 32.9

AUD 0.77 (0.2) (0.9) (5.7) HANG SENG 27,850.49 2.8 0.7 18.0

USD Index 98.00 0.1 0.5 8.6 BSE SENSEX 27,676.04 (0.5) (3.3) 1.1

RUB 53.70 0.6 3.3 (11.6) Bovespa #

53,761.27 0.0 0.5 (6.5)

BRL 0.33 (0.1) 0.2 (12.6) RTS 1,007.69 1.2 0.9 27.4

172.1

141.5

128.0