Mutual funds [www.writekraft.com]

•Download as DOCX, PDF•

1 like•62 views

We started this Academic Writing Help in the year 2011.Writekraft Research & Publication: www.writekraft.com 1000s of students have graduated across the globe from our in-depth research. We help students with the following services: 1. Thesis Writing (from 50 pages and above) 2. Dissertation writing 3. Research Writing for Publishing 4. Data Analysis 5. Research Proposal Writing 6. Study Plan 7. Plagiarism Report Contact us at shivam.writekraft@gmail OR call us on +917753818181, +919838033084 The charges are fair and we allow negotiations as per the student’s budget. You can also inbox me for more direction.

Recommended

Recommended

More Related Content

What's hot

What's hot (18)

Similar to Mutual funds [www.writekraft.com]

Similar to Mutual funds [www.writekraft.com] (20)

More from WriteKraft Dissertations

More from WriteKraft Dissertations (20)

Recently uploaded

Recently uploaded (20)

Mutual funds [www.writekraft.com]

- 1. Evaluationof mutual fund performance in the present marketcondition

- 2. TABLE OF CONTENTS 1. INTRODUCTION...................................................................................................................3 1.1. BACKGROUND OF THE STUDY...............................................................................3 1.2. SIGNIFICANCE OF THE STUDY...............................................................................7 1.3. OBJECTIVES OF THE STUDY.................................................................................10 2. LITERATURE REVIEW......................................................................................................11 3. RESEARCH METHODOLOGY ........................................................................................44 3.1. SAMPLE SIZE DETERMINATION ...........................................................................45 3.2. DATA COLLECTION INSTRUMENTS.....................................................................45 4. DATA ANALYSIS ................................................................................................................46 4.1. PRESENTATION OF DATA ......................................................................................47 5. RECOMMENDATIONS......................................................................................................63 6. CONCLUSION.....................................................................................................................65 7. BIBLIOGRAPHY..................................................................................................................68 APPENDIX I................................................................................................................................70

- 3. 1. INTRODUCTION 1.1. Background of the Study Even in a relatively developing economy like India the importance of marketing as a profit making activity aimed at facilitating the flow of the required products from the place of production to the consuming public or users is recognized. To achieve effectiveness, such activity requires a lot of planning and marketing strategies. Aware of the fact that, there is a good number of cement producing companies in the country and the fact that profit, which is one of the objectives of every business enterprise, can only be realized by selling products rather than merely producing them. Therefore, business as an act can be seen from a couple of ways. As many as these ways are not withstanding, business can be summarized as the act of marketing goods and services geared towards satisfying customers’ or users’ need and wants with the primary aim of making profit. For this aim to succeed, every business therefore has several ways and styles of having enough money to operate or stay out of debt. This can be subsumed to simply mean, business strategy. However, part of any business is to be competitive. That is, competing against other business set-ups or being competed against. Competition can be very interesting, especially when it is healthy and practice within the rules of the game. Because through healthy competition, business bodies can do self- assessment, readjust and seek avenues for innovation and development. Consumer behaviour from the marketing world and financial economics have come together to bring to surface an exciting area for study and research in the form of

- 4. Behavioral Finance and it has been gaining importance over the recent years. With reforms in financial sector and the developments in the Indian financial markets, Mutual Funds (MFs) have emerged to be an important investment avenue for retail (small) investors. The investment habit of the small investors particularly has undergone a sea change. Increasing number of players from public as well as private sectors has entered in to the market with innovative schemes to cater to the requirements of the investors in India and abroad. For all investors, particularly the small investors, mutual funds have provided a better alternative to obtain benefits of expertise- based equity investments to all types of investors. So in this scenario where many schemes are flooded in to market, it is important to analyze needs of consumers and to find out which factors affects consumers' needs the most. Mutual funds are that collect money from several sources - individuals or institutions by issuing 'units', invest them on their behalf with predetermined investment objectives and manage the same all for a fee. They invest the money across a range of financial instruments falling into two broad categories -and debt. Individual people and no doubt can and do invest in equity and debt instruments by themselves but this requires time and skill on both of which there are constraints. Mutual funds emerged as professional financial intermediaries bridging the time and skill constraint. They have a team of skilled people who identify the right stocks and debt instruments and construct a portfolio that promises to deliver the best possible 'constrained' returns at the minimum possible cost. In effect, it involves outsourcing the management of money. More the benefits of investing in and debt instruments are supposedly much better if done through mutual funds. This is because of the following reasons: Firstly, fund

- 5. managers are more skilled. They are trained to identify the best investment options and to assess the portfolio on a continual basis; secondly, they are able to invest in a diversified portfolio consisting of 15-20 different stocks or bonds or a combination of them. For an individual such diversification reduces the risk but can demand a lot of effort and cost. Each purchase or sale a cost in terms of brokerage or transactional charges such a demat account fees in India. The need to possibly sell 'poor' stocks bonds and I buy 'good' stocks and bonds demands constant tracking of news and performance of each company they have invested in. Mutual funds are able to maintain and track a diversified portfolio on a constant basis with lesser costs. This is because of the pecuniary economies that they enjoy when it comes to trading and other transaction costs; thirdly, funds also provide good liquidity. An investor can sell her/his mutual fund investments and receive payment on the same day with minimal transaction costs as compared to dealing with individual securities, this totals to superior portfolio returns with minimal cost and better liquidity. This can be represented with the following flow chart:

- 6. Chart 1: Source: Association of Mutual Funds in India (AMFI)

- 7. 1.2. Significance of the study This thesis makes several meaningful contributions to the literature and the practical perspective. First, it is conducted in a different setting from most previous studies. Thus, it provides an out-of-sample test for the theories and empirical models so far established. Second, this study fills one of the gaps in mutual fund studies by asking whether the findings in Indian market carry over to India. This is important because, even though India displays several characteristics which are not found in developed markets, the literature on mutual funds in India is relatively thin and incomplete. Third, this study uses an extensive dataset. The high data frequency not only helps to validate our results, but also allows us to advance some analysis. Furthermore, this is the first empirical study of an India which includes flexible funds in the sample. In theory, a flexible fund is in some ways similar to equity funds since its main assets are also stocks. However, a proportion of its holdings can be more varied over time, subject to the fund manager’s decision. Thus, this study includes flexible funds in the sample and puts them into a separate category and it is hoped to provide a more comprehensive account of portfolio behaviour. Fourth, this study applies new methodologies which have never been applied to India. For instance, explores the determinants of risk-adjusted mutual fund performance using multidimensional regression in addition to the common approach, which is to use a zero-cost trading strategy. This alternative methodology can explore several factors simultaneously while controlling the effect between one and another. Using the two

- 8. methods allows us to examine determinants of fund performance statistically and economically and it provides more meaningful results. Moreover, in we apply a model in the hedge fund literature in measuring the illiquid assets contained in a portfolio in our mutual fund data. This is the first empirical study to use such a model outside the hedge fund literature. Fifth, this study explores new issues which have not hitherto been observed in previous studies. This is the first study in India which explores the stock selection strategies and style of fund managers. We consider a broader range of characteristics than previous studies in India have done in determining mutual fund performance and also include more new factors, namely fund longevity and family size, in the analysis. We look at the effect of liquidity on the mutual fund performance because liquidity is one of the major concerns in India. Leaving aside India, the liquidity effect is negligible in all mutual fund literature, even though this issue has been widely documented by writers of asset pricing. The study also puts forward an auxiliary model based on the liquidity effect in measuring mutual fund performance. Sixth, this study can claim several new findings. This is the first mutual fund study to expose the evidence of a liquidity premium and emphasize the inclusion of including a liquidity factor in the fund performance measure. This study also provides new findings about India. The study reveals the style of fund managers in these markets and shows that they rely on medium capitalization strategy. This chapter also relates the sensitivity

- 9. of data frequency to the fund performance. In addition, it gives the first evidence from the India of short-term persistence in performance among poorly performing funds. Seventh, the study is the only one which gives important policy implications, reporting them in turn in each empirical chapter. This is the first study on India which discusses the effect of the Indian government’s encouragement of individual savings by adopting special fund styles which give favorable tax treatment. We reveal the policy implications of this action by assessing these specific funds in a separate group from general funds, before comparing and discussing the results from the two groups. Finally, in its practical aspects, this study will, it is hoped, be useful for individuals and institutional investors in selecting mutual funds. It also helps fund managers to identify their positions and gives ideas on the strategies which they should follow in order to maximize returns for their investors.

- 10. 1.3. Objectives of the Study • To know the preference of investors and their needs regarding mutual funds investment. • To analyze factors that influences most while buying mutual funds. • To evaluate performance of mutual fund schemes preferred by investors on the basis of return parameters.

- 11. 2. LITERATURE REVIEW This chapter has two main purposes. The first is to review the theories associated with the research questions in order to provide readers with an understanding of the theoretical domain. The second purpose is to relate the theories to the research questions and develop a theoretical framework for analysis. The reason for discussing the theories is not to produce a comprehensive survey of their richness but rather to provide a framework within which to facilitate the collection of empirical evidence, conduct the analysis and, finally, achieve solutions to the research questions. The growth of investments in mutual funds around the world has widely increased during the past few decades, leading to fierce competition in the industry. Investors now have a wide range of products to choose from, which makes their investment decision more complicated than before. Although there are many factors in their decisions, performance still seems to be a determining factor (see Ippolito, 1992; Capon et al., 1996; Sirri and Tufano, 1998). As a result, from the investors’ point of view, it is important not only to know how the portfolio managers perform, but also to understand their investment policies. Similarly, at the macro level, it is worth examining the performance of fund managers as a whole to see whether they provide value added to portfolios or they are just sweeping benefits from investors. However, superior performance in the past does not necessarily mean that it will continue into the future. This is because superior performance may be due to either a manager’s skill or good luck. Therefore, it is interesting to understand the characteristics of funds and to know what caused the performance; this helps investors to understand how to select their fund manager.

- 12. This literature survey chapter is organized as follows. Section 2.2 surveys the writings related to performance measures and empirical evidence to do with them in the developed markets. Section 2.3 surveys the literature on persistence in mutual fund performance. Section 2.4 surveys the literature on flows and their relation to performance. Section 2.5 surveys the literature on style analysis. Section 2.6 gives empirical evidence on India and, finally, section 2.6 draws some conclusions and makes suggestions for further research. At the end of this chapter, Tables 2.1 and 2.2 summaries the main theoretical and empirical studies related to mutual fund performance in developed and India, in turn. Performance measures It is typical that when one has made a decision, one wonders what its consequences will be. Therefore, once an investor has given money to a fund manager to invest on his/her behalf, he/she should have the right to know what sort of performance they have obtained. Does the fund manager offer superior or inferior performance? How does the fund manager perform compared to peers? And what sort of strategy is used? Performance evaluation measures the skill of an asset manager and its principal idea is to compare the returns with an alternative appropriate portfolio to that which was obtained in a particular case. The emergence of modern portfolio theory (MPT) by Markowitz (1952), who quantifies how rational investors make decisions based on expected return and risk, has brought much development to portfolio performance measurement. It moves performance measurement from crude measures toward more

- 13. precise, risk-adjusted measures. Up to now, many researchers have proposed various methods for evaluating portfolio performance in order to find a model which could give a precise and reliable measure (e.g. Jensen, 1968; Grinblatt and Titman, 1993; Ferson and Schadt, 1996; Cahart, 1997; Daniel et al., 1997). Although these researchers use different methods to evaluate portfolio performance, they all aim to provide an appropriate method by which to distinguish superior managers from others. However, it is difficult for a user to decide which model is the best suited for the performance evaluation is a given case. Therefore, while many researchers have proposed different methods for performance evaluation, some researchers also enquire which model gives the best evaluation technique. (e.g. Grinblatt and Titmann, 1994; Kothari and Warner, 2001; Fletcher and Forbes, 2002; Otten and Bams, 2004). An appropriate model depends not only on the method used for measurement, but also depends on the appropriateness of the measure to the data and the market being evaluated. This section will first introduce various methods of portfolio performance measurement which have been discussed in the literature, partially following Grinblatt and Titman (Jarrow etal., 1995). We divide performance measures into three classes: first, performance measures in the early stage (Section 2.2.1), second, measures which require benchmark returns (Section 2.2.2 - 2.2.4) and, third, measures which evaluate portfolios based on their composition and do not necessarily require a benchmark portfolio (Section 2.2.5). Following this, we highlight empirical evidence of fund performance in developed markets in Section 2.2.6.

- 14. The early stage of performance measurement In the early stage, the past few decades, performance evaluation was made by focusing fund performance on the returns of the portfolio. The two methods which can measure the return on a portfolio are the ‘money-weighted return method’ and the ‘time-weighted return method’. The money-weighted return (otherwise called the internal rate of return) is the discount rate which makes the final value of portfolio equal the sum of initial value and cash flows occurring during the period. Alternatively, the time-weighted return method is the geometric mean return of the portfolio’s sub periods. This measure assumes that all distributed cash flows, such as dividend, are reinvested. As return is the key aspect of performance measurement, some criticisms can be made of the choice of method when measuring return. For example, Sharpe and Alexander(1990) suggest that the time-weighted return method is preferable because this method is not strongly influenced by the size and timing of cash flows, which managers are unable to control. Spaulding (2003) reveals that when a portfolio is measured in a short period and has few cash flows, the choice of return method is not different. Campisi (2004) argues that the money-weighted return method is more appropriate for measuring active investments. Nevertheless, the time-weighted return method is still widely used in practice in the investment fund industry and it is believed that increasing the measurement interval improves the precision of the calculation. In term of risk measurement, there are two possible choices for measuring risk, namely, ‘total risk’ and ‘systematic risk’. Total risk is the overall risk of a portfolio including both systematic and unsystematic risk and is measured by the portfolio’s standard deviation of portfolio. In contrast, systematic risk (or market risk) is measured by the portfolio’s

- 15. beta coefficient, which is the sensitivity of the portfolio’s return to changes in the return on the market portfolio. The choice of risk measures depends on the way in which the portfolio is diversified. If the portfolio is well diversified, then using systematic risk is preferable. Thus, it is advisable in the early stages of mutual fund performance evaluation to use the basic approach, directly comparing the return on portfolios to other portfolios with the same risk (benchmark portfolio). This evaluation technique is straightforward and still widely used among investors and practitioners. However, it could potentially be misleading and biased, because to be truly comparable it requires the benchmark portfolio to have same risks and constraints. In India one can gain additional benefit by investing through mutual funds tax savings. Investment in certain types of funds such as Equity Linked Tax Savings Schemes (ELSS) allows for certain amount of income tax benefits. Mutual Funds are one form of Collective Investment Vehicles (CIV's) in India. The other forms being Collective Investment Schemes (CIS's) and Venture Capital Funds (VCF's).The organization of mutual funds in India (excepting for Unit Trust of India)2 is dictated by the Securities and Exchange Board of India - SEBI (Mutual Funds) Regulations, 1996, (henceforth termed as 'regulations'). Bank-owned mutual funds are also supervised by the Reserve Bank of India (RBI). This does not overlap with SEBl's supervision. Besides, the Indian Companies Act of 1956 and Indian Trust Act of 1882 also govern funds.

- 16. The SEBI regulations stipulate a three tier structure. The constituents of a mutual fund include the Sponsors, the Mutual Fund, the Trustees and the Asset Management Company (AMC). The Sponsor as an individual or along with another corporate body initiates the process by approaching the SEBI for registration of a mutual fund. There are certain eligibility criteria which the sponsor has to fulfill [as laid out in Chapter II, clause 7 of the regulations). Broadly speaking it requires a sound financial track record over the past five years, a sound reputation with respect to integrity and a minimum of 40 percent stake in the AMC by the sponsor. For instance, Tata Mutual 1. Section 80 C of the Indian Income Tax Act allows for Income Tax exemptions upto a maximum of Rs. 100000 2. Unit Trust of India (UTI) is governed by the Government of India UTI Act of 1963 Fund set up in 1995 is sponsored by Tata Sons Limited and Tata Investment Corporation Limited The Mutual fund is itself set up in the form of a trust under the Indian Trust Act of 1882. The instrument of the trust is executed by the sponsor in favour of trustees and is registered under the Indian Registration Act, 1908. The investor subscribes to the 'units' of the fund and, the collected funds/assets are held by the trustee for the benefit of the investor. The Sponsor then appoints the Trustees, AMC and Custodian [Chapter II, clause 7 (e), (I), (g) of the regulations]. A Trustee holds the fiduciary responsibility of protecting the interest of the investor. The trustees themselves are to be of impeccable personal

- 17. credentials [Chapter II, clause 16 (2)]. Two thirds of them have to be independent persons and should not be associated with the sponsors in any manner'. No employee of the AMC is to be a part of the Trustee. The Trustee has the duty of ensuring that the AMC carries out its activities in accordance with the regulations and prevent conflict of interest between the investors and the AMC. The trustee could be either a group of individuals or a Trust Company. Most funds prefer a board of trustees. The Trustee for Tata Mutual Fund is Tata Trustee Company Pvt. Ltd. The AMC consists of the fund managers who manage the investments Regulations are laid down [Chapter IV] with regard to their eligibility and obligations. The AMC takes decisions with respect to investment/sales, computing asset values, declaring dividend and providing investor information, regularity. An AMC cannot www.tatamutualfund.comlrisk-factors.asp Earlier only 50 percent were required to be independent members. This was amended in 2006 by the SEBI (mutual funds) (Fifth Amendment) regulations. Act for any other fund. The AMC for Tata mutual fund is Tata Asset Management Ltd. In addition to the above three principal constituents there is the custodian (Chapter IV, clause 26) predominant duties includes stock keeping of securities and settlement between funds. A custodian can service more than one fund but not a fund promoted by a sponsor who has 50 percent stake or more in the custodian. For Tata Mutual Fund, ABN AMRO Bank N.U and Deutche Bank are the custodians. Apart from these there are the depositories, transfer agents and distributors who complete the organizational chain for mutual funds in India. The study firstly reviews the

- 18. Ories of regulation. The works of Stigler (1971) and Posner (1969) discuss the general theoretical approaches to regulation. The justification of mutual fund regulations stems from asymmetric information leading to possible investor - manager conflict of interest. To control for such behaviour in 'public interest' the regulator might seek to use different approaches including direct price control and or disclosure norms. The study reviews literature relating to measure of risk in the case of equity returns. It looks at both the Mean-Variance (M-V) approach and the lower partial movement (LPM), while the M-V approach assumes that preferences are based only on the mean returns and the variance of the fund portfolio. It is appropriate only if the returns are normally distributed. During the 70s a semi variance measure of risk known as LPM was developed. It gave a better approach towards measuring the risk-return combination. Writings on the single factor capital asset pricing model (CAPM) which uses the M-V approach to risk and a Hemative multi-factor models used to measure portfolio performance are also reviewed. In the process it looks at the efficient market hypothesis and the theoretical impossibility of earning more returns than an informational efficient market. The study then moves on to theories of regulations and the necessity for the same to tackle Principal-Agent problems that arise due to information asymmetries. Regulation ought to be dynamic changing according to market conditions as the fund industry gets competitive the necessity of regulations might wane. In fact it might be a bane as regulations have an impact on performance and increase costs.

- 19. Posner speaks of the costs of regulations generally. To sum up, the basis of regulating mutual funds appears to be from a public interest perspective to control hazards to investors arising from market imperfections. Further the need to have appropriate risk- reward measures emerges clearly. Empirical studies pertaining to mutual fund performance can be grouped into single factor CAPM which uses a single benchmar1< and multiple factor CAPM. Some of the predominant single factor CAPM studies were those of Sharpe (1966), Treynor and Mazuy (1966), Jensen.M (1968). But, Ross (1976) argued that systematic risk need not be explained by a single factor and that there could be 'K' factors. Hence the basis for multi factor models for assessing performance. Several factors such as return of small cap stocks, large cap stocks, midcap stocks, growth stocks, value stocks and momentum are included in various studies. For instance, Fama and French (1993) used multifactor model with the market return, the return of small less big stocks (SMB) and the return of high market, less low market stocks (HML) as three important factors. Using multiple factors eliminates the error that arises out of the assumption of homogeneity of assets held by different portfolios or funds. The multiple factor models recalculate the Jansen alpha which measured superior performance. Apart from these two broad approaches to performance, empirical work on other special factors influencing performance analysis is reviewed. Studies on the influence of size on performance such as Grinblatt and Titman (1989), Indro et al (1999) and Chen et al (2003) are some who examine the role of size and diseconomies of scale/all in the U.S context). The results are however mixed with no clear consensus on diseconomies of scale. With respect to India there has been no

- 20. attempt to study the possibilities of size affecting returns. Another factor which has been found important is the style of a fund. Sharpe (1992), Grinblatt et al (1995), and Bogle. J (1998) discusses the role of style. Style describes the asset class of the portfolio of a fund. This explains a large part of the funds return variability. Studies evolved from the holdings based style analysis (HBSA) method (categorization of funds on the basis of average market capitalization and average price-to-earnings of the fund portfolio) to the returns based style analysis (BSA) classification (compares fund returns to returns of a number of selected indexes) While taking samples of funds for assessing their performance the survivor bias has to be considered. Funds tend to close or merge with others, at times this covers up for poor performance. So choosing funds which survive might tend to bias performance analysis. Several funds in India had been terminated or merged and hence this factor has to be considered while assessing performance. Since the overwhelming emphasis of regulations in India is on direct controls on fees and expenses that are charged to fund, investors' empirical studies relating to this issue have been reviewed. In the relationship between fund expenses and performance Sharpe (1966) and Ippolito (1989) throw up different conclusions. On the relationship between fund size and expenses or economies of scale and scope Baumol et al (1989), Rea (1999), Latke (1998) establish economics of scale and Baumol also finds economics of scope. The Indian context regulatory caps on fund manager fees and expenses and impact on constraining fund expenses has not been dealt with so far.

- 21. Studies on Indian mutual fund performance by Sahadevan and Thiropol Raju (1997) and Sadhak (1997) focus on general trends in the mutual fund performance, regulation and expenses from 1990-91 to 1996. Their focus was not on the evolved risk return analysis. Madhu S Panigrahi (1996) and Bijan Roy et al (2003) have attempted risk- return analysis and using traditional CAPM and conditional performance evaluation techniques respectively. The review of empirical literature points out to the role of benchmarks and style of funds in deciding fund performance. Studies also cover fund behaviour in terms of management fee and expenses. These help point to the general issues of focus concerning mutual funds. The Indian studies, it is found, tend to focus on using evolving techniques to study of fund performance. But there is no attempt to study the impact of regulations on fund behaviour in terms of expenses, fees and performance. This gap in Indian studies needs to be seriously considered. It gives us the motivation for our study. We need to study the past implications of fund regulations before we go ahead with further changes in the same. Have the costs of regulations exceeded the benefits? Can we improve regulations to ensure better governance? Do we notice tendencies of price competition between funds? Do they deliver more than what regulations demand in terms of cost charged to investors?

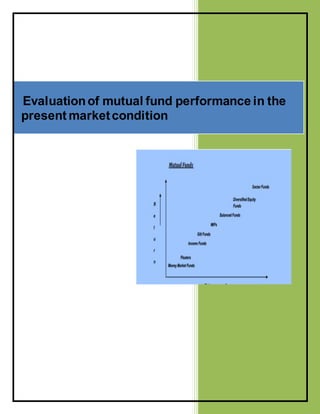

- 22. The organization conceived as above has is emphasis on eliminating moral hazards that could arise out of post contractual opportunistic behaviour on the part of fund managers. It aims at ensuring arms length transactions between the sponsor and the AMC. Types of Mutual Funds A mutual fund, say, Tata Mutual Fund, can have several 'funds' [called 'schemes' in India) under its management. These different funds can be categorized by structure, investment objective and others. It would be well illustrated by the following flow chart:

- 23. Chart 3: Source: Association of Mutual Funds in India (AMFI) Is match of stocks in the equity and derivative (Mures and options) segments of the stock market (Value Research Inc). They invest predominantly in equities 'Money Marker. Funds invest only in short term debt such as call money, treasury bills and commercial paper. In the case of these funds the Net Asset Value is simply the interest accrued on these investments on a daily basis. Their NAV does not fall below the initial investment value, unlike bond funds which are marked to market.

- 24. Tax saving funds give an investor tax benefits under section 80 C of the Income Tax Act. Such funds also termed as Equity Linked Saving Schemes (ELSS), have a lock in period of three years. By investing in such funds a person can avail of a maximum of rupees one hundred thousand in tax deductions. ELSSs are normally diversified equity funds. Index funds invest in securities of a particular index such as the Bombay Stock Exchange (BSE) sensex in the same proposition. They provide returns which are close to that of the benchmark index with similar risks as well. It is a passive investment approach with lower costs. Sector specific funds focus their investments on specific sectors which the fund manager feels would do well. For instance, Franklin FMCG fund invests only in shares of companies that produce fast moving consumer goods. Exchange Traded Fund's (ETF) are relatively a new concept in India. Such funds are essentially index funds that are listed and traded on the stock markets. There are also commodities ETFs such as Reliance hold ETF. The Mutual Funds Industry in India The beginning of mutual funds in India was laid by the enactment of the Unit Trust of India (UTI) Act in 1963. The objective was to provide investors from the middle and lower income groups with a route to invest in the equity market. It was also meant to encourage savings. UTI brought out its first fund, Unit Scheme (US) 64 in 1964. It called an amount of Rs.246.7 millions. UTI remained a monopoly in the mutual fund industry till 1987. By then US 64 had grown to Rs.32.69 billion and the overall asset base of UTI was RS.67.38 billion with 25 different schemes·. In 1987 other public sector banks were

- 25. allowed to offer mutual funds. The State Bank of India (SBI) set up the SBI Mutual Fund and Canara Bank Mutual Fund. Other public sector banks such as Bank of India, Punjab National Bank, Indian Bank entered the fray by 1990. Two public sector insurance companies -Life Insurance Corporation of India (LlC) and General Insurance Corporation of India (GIC) also started their own mutual fund companies. But during this period only public sector companies were permitted to enter the mutual fund market. The collective assets under management continued to grow and by the end of 1993 it was Rs.470 billion with UTI alone accounting for RS.390 billion>' There were 44.7 million investors in mutual funds". 1992-93 saw the beginning of economic reforms in India. The reforms aimed at reducing government control over the economy and allowing for greater play for the private sector besides others. In keeping with this direction the private sector was allowed to enter the mutual fund industry in 1993. In keeping with this direction the private sector was allowed to enter the mutual fund industry in 1993. In the same year the first mutual fund regulations 1993 SEBI (mutual fund) Regulations came into being. This was later substituted by a more comprehensive set of regulations - SEBI (mutual fund) Regulations 1996. However, UTI did not come under these regulations and continued to be governed under the UTI Act of 1963. By 2003 the total assets under management (AUM) had increased to Rs.1, 218 billion mutual fund families and 401 funds. UTI alone accounted for Rs.445 billion of the total AUM In 2003 the public sector UTI, which had faced serious problems in the late 90's and again during 2002, was into two entities. One was the specified undertaking of UTI which managed US 64, assured return schemes and others which totaled to Rs.298.4

- 26. billion and the other was UTI Mutual Fund Ltd. The latter came under the regulations of SEBI. Since 2003 the mutual fund industry has also seen a spate of mergers. Hence this period was marked by consolidation. By March 2007 the total AUM excluding UTI touched Rs.3, 591 billion showing a phenomenal growth of 47 percent year-on-year since 2003". During this period only Russia and China did better than India AUM growth rates of 97 percent and 67 percent, respectively. The financial savings of the households in India and the savings of the private corporate sector form the main source of funds for the mutual fund industry. The gross financial assets of Indian households increased from Rs.l09.6 billion (10.4 percent of the GOP at CMP) in 1993-94 to Rs.4, 176.8 billion (14.85 percent of GOP at CMP) in 2003-0413. The gross financial assets include currency held, bank and non-bank deposits, life insurance, provident and pension funds, claims on the government, shares and debentures, investments in Unit Trust of India and the net trade debt. Bank deposits comprised of 42.83 percent of the total financial assets and shares and debentures (which include mutual fund investments) forming a small 1.81 percent (EPW). The total AUM at the end of March 2004, Rs.1, 396.16 billion was 4.96 percent of the GOP (CMP). A comparison of India with other countries is given below:

- 27. Data from Investment Company Institute 2004, fact book •• GDP data from IMF world economic outlook databases The above table shows the vast potential for growth in the mutual funds industry. A minuscule 5 percent of the GOP (CMP) was invested in mutual funds as "Economic and political weekly, Oct. 09, 2004, pp 4487 compared to 67.5 percent in the U.S. The comparison is to show what the growth potentials are. In many ways the mutual fund industry can be termed to be still in its infancy. A SEBI survey of Indian Investors 14 for the period April 01, 1999 to March 31, 2001 revealed the low household penetration rate for mutual funds. The survey found that 7.4 percent of Indian households (13.7 percent of urban and 3.8 percent of rural households) had invested in mutual funds. Even among the urban households most investors were from the largest cities with a population of 5 million or more. The facts point to a low household penetration rate by mutual funds and also a very narrow urban bias. For

- 28. individual investors direct investment in equity was a risky proposition and an important deterring factor as per the survey. Mutual funds have potential to offer a safer route to the vast untapped households that still seem to prefer bank savings. But to use the mutual fund route there are other concerns which need to be addressed. Firstly funds have to deliver in terms of performance. Comparisons are bound to arise particularly between fund return and benchmark indices are to be expected. Outperforming benchmarks with lower costs is an important factor to attract more savings into mutual funds. Apart from performance there is the issue of moral hazards. Once a contract has been entered into with the fund house there are risks of conflicting interests. These risks could be broadly classified into portfolio selection risks and management process risks. The former involves 'adverse portfolio selection' which contradicts the objective of the fund as mentioned in the prospectus. This could mean higher risk of the fund portfolio on Risk Containment. Opinion, Business Line, 2~ October 2000 or lower risk-weighted returns. There could also be excessive churning of the portfolio leading to more expenses that would be deducted from the AUM. Management process risks involve risks arising due to errors in execution of transactions losses due to counter-party default. It is to protect investors against such risks that SEBl's (mutual fund) Regulations of 1993 were framed. The same was substantially amended in 1996. Given the growth of the mutual fund industry, it's present and potential importance as a vehicle of financial saving for Indian households, and the development of regulations to govern fund behaviour we feel it is important to assess the role of regulation in adding

- 29. value for the investor. Have the regulations ensured due diligence, transparency and sound portfolio selection? Have the dynamics of the fund industry led to the necessity for change in regulations? Is the present form of fund performance information dissemination adequate? These are some of the questions that the present study attempts to answer. This is sought to be done by examining the ability of regulations to: ensure proper performance disclosure; better returns from funds; control costs of operation; prevent excessive management fees and be proactive in tackling new issues. The term ‘India’ was first introduced by the World Bank in the 1980s and defined as countries which are in the transition from developing to developed economies. More recently, the study of India has become more controversial and a number of studies reveal several differences between them and developed markets. Harvey (1995) claims that India exhibit high volatility and low correlation with developed markets. However, the standard asset pricing model fails to explain cross-section returns in this market, since India are not integrated with the world economy and there is a time variation in risk exposure. Bekaert and Harvey(2002, 2003) also argue that India are inefficient. India usually suffers from infrequent trading; high transaction cost; and abnormal distribution of returns. In addition, some researchers investigate the stock selection strategies in India and reveal that stock returns in India are predictable owing to certain fundamental characteristics. Claessens et al. (1995) investigate cross-section returns in 19 developing markets over the period 1986-1993 using several variables including, market returns, earning-to-price, price-to-book value, size, dividend, turnover, and exchange

- 30. rate. They reveal that, in addition to market risk, firm size and turnover have explanatory power in stock returns in many countries, although the signs are reversed in the evidence from the US. Conversely, Fama and French (1998) argue that the results in Claessens et al. are due to the sensitivity to outliers. They examine the value and growth premium in 16 India for 1987-1995. They reveal that the evidence from developed markets is inconsistent with the value and size premium in India. Nonetheless, they point to the unreliability of their results, since the sample period is short and the returns are highly volatile. Using a longer sample period, Rouwenhorst (1999) examines the return factors in 20 India over the period 1982-1997. In comparison to Fama and French, he concludes that return factors in India are similar to those in the US and in developed markets in that they exhibit momentum and small and value premium. Similarly, van der Hart et al. (2003) survey 32 India. They argue that stock returns can be Explained by value, momentum and earning revisions but not for size, liquidity and mean reversion. Nonetheless, Griffin et al. (2003), examining momentum strategy in 39 markets, show evidence of momentum strategy among Asian markets. In addition, some studies investigate the return factors in some specific India. For instance, Drew and Veeraraghanvan (2002) find a size and value premium in Malaysia; and Brown et al. (2008) reveal a momentum and a value premium in Hong Kong and Singapore, respectively.

- 31. In the mutual fund literature, in contrast to the extensive evidence from developed markets, studies in India are scarce. Details of the empirical evidence in India are chronologically presented in Table 2.2 and its main details are described below. For his PhD thesis Elsiefy (2001) investigates the risk and return characteristics of 7 equity funds in Egyptian markets over the period 1996-1999. He employs several performance measures, including the CAPM-based models; market timing models; and Fama’s decomposition of returns (Fama, 1972). He reveals that over the period of his study Egyptian funds do not outperform the market. However, the number of underperforming funds is different for different measures used in the evaluation. Funds do not diversify and therefore he suggests that using total risk is more appropriate in the Egyptian context. In addition, he shows that performance does not change with the market conditions. Roy and Deb (2003) take 89 Indian mutual funds over4 years, 1999- 2003 and examine the importance of using a conditional performance model which allows time varying according to the economic conditions. They evaluate mutual fund performance and market timing models, using both unconditional and conditional single- factor models. Their conditional model includes 5 lagged information variables, namely, t-bill, dividend yield, the term structure of interest rates, a dummy variable for the month of April and a dummy variable for the tech rally. Inconsistently with the evidence from the US, their results suggest that, as a whole, Indian mutual funds are unable to beat the market. The conditional version makes funds look better and evidence of negative market timing is not present. Soo-Wah (2007) explores 40 Malaysian funds over the period 1996-2000 using single-factor and market timing models. He also tests for benchmark sensitivity by employing two choices of benchmark: KLCI and the EMAS

- 32. index. He finds inferior performance and poor market timing in these Malaysian funds. However, the choice of benchmark does not impact on performance evaluation, which contradicts the findings in developed markets (e.g. Grinblatt and Titman, 1994). Similarly, Fauziah and Mansor (2007) study mutual fund performance in Malaysia, using a longer sample period (1991-2001) than Soo-Wah used in his study; they employ the measures of Sharpe, Jensen and Treynor. Unlike Soo-Wah, they reveal that funds perform below the market and find no evidence of persistence in performance. Another study in Malaysia was conducted by Fikriyahet al. (2007). These writers observe the difference in performance between conventional and Islamic funds over the period 1992-2001. Their sample is 65 funds, including 14 Islamic funds. Like the studies above, they employ standard measures, including the Sharpe, Jensen and Market timing models. Subsequently, they reveal that Islamic funds are less risky than conventional funds and perform better in bearish market conditions. Conversely, in bullish market conditions, conventional funds seem to perform better. In the Indian market, as far as is known, only a few studies in fund performance have been published, some being in the form of scholars’ dissertations. Results from these studies are, for example, those of Plabplatern (1997), who uses the portfolio holdings method to investigate the performance of Indian mutual funds from 1993 to 1997. He uses the quarterly data of 63 closed end funds. All funds have superior performance and half of them bear evidence of market timing. In contrast, Sakranan (1998), who uses a similar approach and time period, 1995-1997, to examine mutual fund performance, draws a different conclusion: that only 2 out of 98 funds show selectivity skills. Pornchaiya (2000) uses Jensen’s single-factor measure to explore 77 funds over

- 33. the period 1996-1999. He reveals that only two funds have superior performance, which is inconsistent with the two Indian studies listed above. Vongniphon (2002) studies return and risk in 18 equity funds, using a longer and more up-to-date sample, from 1994 to 2000. He employs Sharpe and Treynor measures and also confirms the inferior performance of these funds. Likewise, Jenwikai (2005) uses Sharpe and Treynor measures to compare the performance of 62 equity funds to his self-constructed buy-and-hold portfolios. He reveals that equity funds perform worse than portfolios with buy-and-hold strategy. The most recent and extensive research in mutual fund performance in India is Nitibhon’s (2004) dissertation. He considers 114 equity funds in India from 2000 to 2004 and investigates performance using various methods including: Jensen’s alpha (1968), Cahart’s 4-factor model (1996), Ferson and Schadt’s conditional model (1996) and Daniel’s characteristic-based performance measures (1997). He reveals that Indian mutual funds perform better than the market but not enough to generate statistically abnormal returns. However, he reveals that using a conditional approach creates fairly similar results to those obtained from using unconditional models, which is inconsistent with the conclusions of Roy and Deb (2003), who examine funds in India, Furthermore, there are some researchers who concentrate their studies solely on market timing performance, for example Srisuchart (2001) and Chunhachinda and Tangprasert (2004), who explore timing ability in the Indian mutual funds. Srisuchart explores equity and bond funds in the 1990s and Chunhachinda and Tangprasert examine 65 equity funds over 2001-2003. Both of these studies yield the same

- 34. conclusion: that Indian equity fund managers have market timing ability. These results are also comparable to those of Khanthavit (2001), who employs an alternative technique in examining market timing ability in Indian closed end funds in the 1990s. He uses a Markov-switching technique and reveals that fund managers exhibit both selectivity and market timing abilities, although overall performance is not significant. However, these find managers tend to use their market timing ability when the market is up and their selectivity ability when the market is down. Nonetheless, issues outside mutual fund performance evaluation have received less attention. Fauziah Md and Mansor (2007) look at the issue of persistence in performance in the Malaysian context as part of their study of mutual fund performance. They estimate performance annually over the period 1991-2001 and examine the correlation between past and current performance. They do not find persistence in performance for mutual funds in Malaysia. However, this contrasts with the evidence in India. Watcharanaka (2003) reveals persistence in performance in Indian mutual funds over the period 1992-2002, using a cross-section regression approach in examining 62 funds. Nitibhon (2004) also examines persistence in performance for the Indian mutual funds. In his study, he constructs portfolios on the basis of past year returns and estimates performance using unconditional and conditional single-factor models. He reveals that only the top docile portfolios (high past returns) show significant positive performance. Some studies explore mutual fund style in relation to performance. These include: Ferruz and Ortiz (2005), who investigate whether Indian mutual funds correspond to their classification. They employ factor analysis and cluster analysis and conclude that funds are very close to one another. Similarly, Acharya and Sidana (2007)

- 35. employ cluster analysis to mutual funds in India over the period 2002-2006 and reveal the inconsistency between investment style and the returns obtained by mutual funds. In Malaysia, Lau (2007) applies Sharpe factor analysis to 43 funds over the period 1996-2000. He reveals that funds which contain large and high liquidity stocks perform better than others. Regarding the factors related to fund performance in India, Prasomsak (2001) investigates 77 mutual funds over the period 1998-2000, using fixed-effect regression of fund raw returns on market returns size, turnover and fund style. He claims that fund returns are positively correlated with market returns but negatively related to fund size and turnover. This finding is in contrast to the findings of Nitibhon (2004), who employs cross-section analysis and regress fund performance on size, value and growth factors. He reveals that fund returns are positively related to size and growth stocks. In addition, the evidence from Taiwan suggests that large funds perform better than small funds (Shu et al., 2002). Tng Cheong (2007) explores the effect of fund size and expenses on mutual fund performance in Singapore over the period 1999-2004. He reveals that large funds perform insignificantly better than small funds and there is no difference in fund returns between high and low expenses funds. A study in the flows of mutual funds was conducted by Shu et al. (2002). They investigate the investment flows of mutual funds in Taiwan over the period 1996-1990 and reveal the difference of behaviour between small- and large-amount investors. Both

- 36. small- and large-amount investors tend to buy funds on the basis of short-term performance. However, large-amount investors are more rational and redeem funds on the basis of performance. In India, Nitibhon (2004) estimates mutual fund flows of docile portfolios rank on the basis of the past year’s returns. He claims that flows are not induced by the prior year return and suggests no evidence of a smart money effect in Indian mutual funds. Reviewing the evidence from the India makes it clear that: first, mutual fund literature in this region concentrates mainly on performance evaluation. With various techniques and different samples, most of these studies claim no abnormal returns in mutual fund performance. Nevertheless, because these studies tend to use a small number of funds and survey a short sample period, their results are still questionable. This is also because, as mentioned above, India is highly volatile and there is a certain amount of evidence of structural breaks. Second, the evidence suggests that India is inefficient and display several characteristics which distinguish them from to developed markets. In addition, there are other factors outside the market risk which have explanatory in stock returns, for example, size, and value and momentum premium. Nevertheless, mutual fund studies in India mostly employ standard CAPM-based measures, such as the Sharpe ratio and Jensen’s alpha and none of these studies take these effects into consideration. Third, we know very little about other issues related to mutual fund performance.

- 37. Evidence on persistence and flows, as well as other factors related to performance, is relatively small and still mixed. Consumer perception and satisfaction towards Mutual Funds Mutual funds have already attracted the attention of global practitioners and academicians but most of the existing research available is on either accelerating the return on funds or comparing it with benchmark fund schemes. In marketing literature, Service Quality and Customer Satisfaction have been conceptualized as a distinct, but closely related constructs. There is a positive relationship between the two constructs (Beerli et al., 2004). The relationship between customer satisfaction and service quality is debatable. Some researchers argued that service quality is the antecedent of customer satisfaction, while others argued the opposite relationship. Parasuraman et al (1988) defined service quality and customer satisfaction as “service quality is a global judgment, or attitude, relating to the superiority of the service, whereas satisfaction is related to a specific transaction”. Jamal and Naser (2003) stated that service quality is the antecedent of customer satisfaction. However, they found that there is no important relationship between customer satisfaction and tangible aspects of service environment. This finding is contrasted with previous research by Blodgett and Wakefield (1999), but supported by Parasuraman et al (1991). Most of the researchers found that service quality is the antecedent of customer satisfaction (Bedi, 2010; Kassim and Abdullah, 2010; Kumar et al., 2010; Naeem and Saif 2009; Balaji, 2009; Lee and Hwan, 2005; Athanassopoulos and Iliakopoulos, 2003; Parasuraman et al 1988). Yee et al (2010)

- 38. found that service quality has a positive influence on customer satisfaction. On the other hand, Bitner (1990) and Bolton and Drew (1991) pointed out that customer satisfaction is the antecedent of service quality. In 2004, Beerli et al supported this finding. Beerli et al mentioned a possible explanation is that the satisfaction construct supposes an evaluative judgement of the value received by the customer. This finding is contrasted with most of the researchers. Investor’s satisfaction in case of mutual funds depends upon amount of trust and dependence that an investor places with AMC and in turn the benefits that are actually delivered to them. Although fund managers uses their expertise skills and diligence while investment but still dissatisfaction prevail among the investors and their experiences show that majority of mutual funds have shown underperformance in comparison to risk free return and reported that mutual funds were not able to compensate them for additional risk they have taken by investing in mutual funds (Anand, S. And Murugaiah, V.2004). Concept of investor satisfaction is gaining importance for every MF organization because in addition to its contribution in a dominating way to the overall success of these organizations, it also shows them roadmap to retain and grow their business. Zeithaml, V (1993) expressed satisfaction of individual investor comprise of a range of varied parameters and is not easy to define but in general it means positive assessment. Where the growing demand of investor’s expectation is following the way most of researcher admit the fact that working of customer’s mind is a mystery which is difficult to solve (Dash, 2006). Customer satisfaction is subjective and even difficult to

- 39. measure. To draft an accurate picture of customer satisfaction organizations should diligently use information – collecting tools and market research that will finally enable an organization to identify critical elements of customer satisfaction and further fine- tune their operations to achieve incremental improvements. Significant gaps that exist between service expectations and perceptions is right from the first step where AMCs are not found capable enough to translate investor’s expectation, reason being financial intermediaries having inadequate knowledge and training are not able to communicate the message to each player effectively. Consumer behavior The consumer behavior literature has a long history of study of individual purchase decisions. Anchored by Howard and Sheth's (1969) comprehensive model, consumer behavior researchers have developed and tested many constructs believed to comprise the purchase decision process. In this study, we focus on three of the more ubiquitous: information sources, selection criteria, and purchase. We explore how these constructs relate to one another in the mutual fund purchase decision. Consumer behavior researchers have often modeled the purchase decision process in the following manner. Initially, consumers gather information on the product class of interest (i.e., mutual funds in this study) from both internal (e.g., memory of previous experience) and external (e.g., advertising, brochures, newspaper articles) sources (the two sources may be referred to as information sources). Armed with this information, they develop a set of product and service attributes (e.g., price, performance, level of service) that are important to them in assessing the various alternative product

- 40. offerings. Ultimately, consumers use this set of attributes (commonly referred to as selection criteria) to determine which alternative from the set of available products to purchase. The two constructs of information source and selection criteria are quite distinct, yet closely related. For example, three investors (consumers), whose major information sources were, respectively. The Wall Street Journal, an investment advisor, and personal experience with an asset management firm, might form very different selection criteria. A factor complicating the distinction between information sources and selection criteria in the mutual fund investment decision is that not only may some information sources (e.g., published performance rankings) also function as selection criteria, a single information item may serve a different function at each stage of the decision process. For example, in the information gathering stage a consumer may use performance rankings to identify the various possible performance measures (e.g., one- year, five-year, or ten-year return), or to ascertain whether large fund families in general outperform small fund families. In the selection criteria stage, the consumer may decide that one-year return is the most important criterion, then use that criterion to discriminate and choose among alternative mutual funds. Consumer behavior researchers spend much effort to develop models of construct interdependencies in order to predict purchase behavior. In a similar vein, we examine both how information sources and selection criteria relate to each other, and how they relate both to demographic profiles of investors and to mutual fund purchase. Through an investigation of these interrelationships, we hope to develop a richer understanding of the mutual fund investment decision.

- 41. Information sources In the purchase decision process, consumers may receive twotypes of information— namely, interpersonal and impersonal (mass) communication. Interpersonal communication is received from both informal (e.g., family and friends)and formal (e.g., organizations) sources.-^ Research on the relationship between information sources and other purchase decision constructs is limited (Engel, Blackwell, and Miniard, 1986, pp. 259-299). A notable exception is the Vinson and McVandon (1978) study that identified a strong relationship between the subjects' information sources and their product concept recall. In addition, Murray (1991) related information source use to product category (goods versus services) and consumer experience; internal memory was preferred as a source of information by those with greater experience. In related research, the degree of personalization of a service encounter has been shown to impact the level of consumer satisfaction (Surprenant and Solomon, 1987). Inthe financial services arena, Carroll (1990) argues that a bank's retail customer mix maybe enhanced through selective information presentation; and Crosby and Stephens (1987) demonstrate that insurance customers value personal over impersonal information sources. For the mutual fund purchase decision, impersonal sources include advertising, direct mail, and published fund performance statistics; informal interpersonal sources include family and friends; formal interpersonal sources include planners—fee-based advisors (who charge a set fee for their services regardless of transaction volume), and

- 42. commission-based advisors (who implicitly charge on a per transaction basis). Unfortunately, little hard data concerning the relative value that investors place on these various information sources are available, despite their importance for mutual fund managers who must allocate resources for communication and distribution. Selection criteria Selection criteria embrace the set of product or service attributes that consumers consider when making purchase decisions among alternatives. Such attributes may be clearly defined physical attributes, such as the scope of a mutual fund family (i.e. the number of funds), or may be less precise constructs, such as responsiveness or perceived confidentiality of a mutual fund sales agent. Fishbein and Azjen (1975) is perhaps the most widely cited attempt by consumer researchers to model the choice process. In their multi-attribute model, choice is determined by each alternative's sum of perceived values on multiple (importance-weighted) attributes. The alternative with the largest score on independently rated, weighted attributes is selected. Lancaster (1966)presents a multi-attribute model of consumer choice that may be more familiar to researchers in economics and finance. He suggests that consumer utility resides in the characteristics that a good possesses, rather than in the good itself. Thus, preference orderings for goods are rankings of sets of characteristics (i.e., attributes) and are only indirectly rankings of goods. We attempt to identify those attributes or characteristics of mutual funds that are important to investors when making investment decisions.

- 43. For a given purchase, three sets of variables—individual, brand or product characterizes, and purchase context—jointly determine the particular selection criteria employed. Individual factors encompass a variety of demographic and psychographic characteristics of decision makers (Maheswaran and Meyers-Levy, 1990). Brand or product characteristics, including product features or attributes (e.g., price, quality, and performance: return and risk for the mutual fund purchase) are widely believed to impact significantly upon the weighting of selection criteria (Gupta, 1988). Finally, purchase context (e.g., internal and external framing of the purchase decision) has a significant impact on selection criteria (Kahneman and Tversky, 1974). Some researchers have investigated the relationship between consumer selection criteria and demographic variables. For example, Anderson, Cox, and Fulcher (1976) find that consumer selection criteria for a bank (e.g., convenience versus service orientation)is related to several demographic variables (e.g., service-oriented customers were more likely to have a working spouse and higher income). In examining the mutual fund investment decision, as noted above, previous research has focused on the attributes of return and risk. Based on the research reviewed above, we expect to find that investors employ other selection criteria, either in addition to, or instead of, risk and return.

- 44. 3. RESEARCH METHODOLOGY Research methodology is a systematic and objective search for new knowledge of the subject of study and or application to knowledge to the solution of a novel problem. Patel (2004) defines research design as “the structuring of investigation aimed at identifies variables and their relationship to one another”. This is use for the purpose of obtaining data to enable the research questions. It is an outline or a scheme that serves as a useful guide to the research in the efforts to generate data for the study. The design for this research is descriptive in nature. The research entails collection of data which is used in making a systematic description of the existing situation. The present Research will be divided into two different studies: Primary Research

- 45. Primary Research to know the preference of mutual fund investors regarding their investment Secondary Research Secondary Research to evaluate the performance of Mutual funds which are preferred by most of the investors is based upon Descriptive Research Design. Three mutual fund sectors viz. tax Volume 5 Issue 3 (September 2012) funds, diversified funds and sector funds are selected and top 5 companies based on NAV is selected from each sector for further analysis. The secondary Research is based upon Judgmental Sampling. Judgmental sampling is a non-probability sampling technique where the researcher selects units to be sampled based on their knowledge and professional judgment. Sampling Method and Sampling Frame The primary research will be based upon convenience sampling. Convenience sampling (Sometimes known as grab or opportunity sampling) is a type of non- probability sampling which involves the sample being drawn from that part of the population which is close to hand. 3.1. SAMPLE SIZE DETERMINATION Primary research is conducted of 100 educated investors of Mumbai city. 3.2. DATA COLLECTION INSTRUMENTS The data collection instrument used for primary research is questionnaire. The type of questionnaire used is open and close ended structured.

- 46. 4. DATA ANALYSIS The aim of the discussion is providing the needed foundation for offering useful recommendations in the next chapter which are thought to be essential for improving the investors’ returns performance. This chapter will also deals with the presentation and analysis of data collected, and testing of the hypothesis formulated earlier in chapter one. It is important in a research project for data to be analyzed and interpreted in the light of the analysis made. Osuala (1987), states that “the analysis and interpretation of the raw data of an investigation are the means by which the research problem is answered and the stated hypothesis tested”. This means that data collected in its real being willed be meaningless and useless if there are not analyzed and interpreted in a meaningful way. If this is done, the data therefore becomes information on which basis, decisions are made and conclusions are drawn from there.

- 47. 4.1. Presentation of Data Findings of Demographics The above table is self-explanatory. However the following observations can be made Gender Distribution: Total number of respondents is 100 out of which 93% are male and 7% are female respondents. Hence we can say that the majority of our respondents are male and due to this reason No further analysis of the impact of gender as a dependant (demographic) factor on other independent factors is done.

- 48. Age Distribution: This shows that majority of the respondents are young and they have just started their career. It might be possible that these respondents do not have complete knowledge of mutual fund and they might be investing in various avenues according to the advices given by their brokers and agents. Qualification Distribution: A minor portion of 6% of the respondents are high school pass out while maximum of them i.e. 46% are graduates while 29% and 19% of the respondents hold Postgraduate and Professional qualification respectively. Occupation Distribution: 51% of the respondents are salaried employees which forms a majority. 33% are business persons 12% are practicing professionals (like Chartered Accountants, Architects, Lawyers etc.) while a minor portion of 4% of them are retired employees. Income Distribution: Majority of the respondent’s i.e.59% lie in the slab of annual income between Rs. 3-5lakhs. 34% of the respondents have an income ranging from Rs. 5-15 lakh, while a minor portion of 6% and1% of the respondents have an annual income of Rs.15-25 lakh and above Rs. 25 lakh respectively.

- 49. Preferred Investment Avenue by investors: Ranking the Kind of investments preferred by the respondents Factor preferred most while making investment and Age of investors:

- 50. The investors who are of the age of less than 30 are more attracted by the high returns followed by low risk involved and then liquidity or company reputation. Investors in the age group of 31-40 years of age also give high preference to high return. On the other hand the investors between the age group of 41-50 are evenly distributed for factors like liquidity, high return and low risk. Investors above 50years of age prefer low risk more than any other factor. Out of total sample of 100 investors, 75 investors are investing in to mutual funds. So further Analysis is done with sample of 75 investors. Annual income of the respondent and % investment of mutual fund in total Investments The respondents having an annual income of 3-5 lakhs usually prefer to invest less than Rs. 20000 or between 20000-50000 in mutual fund while investors with anannual income between 5-15 lakhs usually prefer toinvest between 20000-50000. On the other handinvestment of more than 100000 in mutual fund is madeonly by the investors having an annual income rangingbetween 5-15 lakhs. Annual income of the individualinvestor and annual investment in mutual fund are Independent of each other.

- 51. Share of Mutual Funds in your total Investment: The cross tabulation clearly states that no matter in which income slab the investor might lie, he would mostly prefer to invest 0-33% of his total investments in mutual funds. There are around 15 no of investors who would prefer 25-50% of their investments in mutual fund, while only 5 investors prefer 50-75% investments in mutual fund. This is the minimum. Moreover the above table also states that annual income does not have any impact on % investment of mutual fund out of total investment and a high income does not mean that his investment in mutual fund would also be high. Share of mutual funds in the total investment and the income of the investors are independent of each other.

- 52. Qualification of the respondent and knowledge about mutual fund The above cross tabulation shows those investors who are just high school pass out are mostly aware of the specific scheme in which they have invested. The graduates are either mostly partially aware of mutual fund or fully aware of the specific scheme. It can be clearly seen that whatever the qualification maybe the investors are on an average aware of the scheme in which they have invested and their qualification plays a little role to determine their knowledge about mutual funds.

- 53. Qualification and knowledge about mutual funds have moderate correlation with each other. Occupation of the respondent and the feature that allures him the most while investing in mutual fund Thus there is no significant relationship between two variables. Occupation of individual investor and the feature that allures him the most are independent of each other

- 54. Preferred mode to receive the returns and frequency to receive the returns from a mutual fund scheme The table above shows that there is significant relationship between two variables. Mode preferred to receive returns yearly and the type of Return expected by the investors is dependent on each other. Findings related to Schemes most preferred by the investors:

- 55. Investors mostly prefer equity schemes while making investment into mutual funds. Amongst equity schemes also equity tax savings (ELSS), Equity diversified scheme and Equity sectoral schemes are mostly preferred by the investors. Based on this preference top 5 schemes are selected from each of this category and its Performance is measured on the basis of secondary data analysis and schemes are identified which have outperformed the market. The analysis is as follows. Equity Tax Savings Scheme Risk Analysis:

- 56. The Risk analysis of Equity Tax Planning top 5 schemes have a varying attributes such as Standard deviation, Sharpe, Beta, Treynor and Correlation which measures the schemes in terms of risk to the portfolio or the individual schemes. For the return analysis of Equity Tax Planning top 5schemes it can be seen that all the returns of 1 month,3 months, 6 months and 1 year are having negative returns so here investor have to invest minimum for 3years to get returns in positive value. The returns of such schemes since inception have shown a growth but on a fluctuating basis as the scheme Canara Robeco Equity Tax saver - Growth and Franklin India Tax shield- Growth which is ranked fourth and third respectively shows the highest return since inception of 32.82 and25.85 while the schemes such as BNP Paribas Tax Advantage Plan - Growth and Axis Long Term

- 57. Equity Fund - Growth which are ranked second and first respectively have the lowest growth amongst the top 5schemes. So the investors who have invested in the schemes whose growth has been highest have benefited more than the investors who had invested in the first two schemes. Canara Robeco Equity TaxSaver - Growth is considered as a better scheme but with standard deviation, beta and correlation to also be considered then Axis Long Term Equity Fund - Growth is considered as a viable investment option. Amongst the top 5 schemes of Equity Diversified funds, It can be said that UTI Wealth Builder Fund - Series II - Growth is said to be the most advisable one irrespective of the ranking giving on the basis of NAV, so similarly Canara Robeco Large Cap+ Fund -Growth is said to be the least advisable to the investors. Hence these schemes are not having the same ranking as per the preference given on the basis of the risk analysis so it can be said that Standard Deviation, Sharpe, Beta, Treynor and Correlation are not the only measure of fund ranking analysis.

- 58. Equity Diversified Schemes: Risk Analysis:

- 59. Amongst the top 5 schemes of Equity Diversified funds, it can be said that UTI Wealth Builder Fund - Series II - Growth is said to be the most advisable one irrespective of the ranking giving on the basis of NAV, so similarly Canara Robeco Large Cap+ Fund -Growth is said to be the least advisable to the investors. Hence these schemes are not having the same ranking as per the preference given on the basis of the risk analysis so it can be said that Standard Deviation, Sharpe, Beta, Treynor and Correlation are not the only measure of fund ranking analysis. Return Analysis

- 60. The top 5 schemes of Equity Diversified funds are having negative returns for short term investments that include 1month, 3 months, 6 months and 1 year. But for the investors who wants to invest for a long term period they will be benefited with the positive return. The most beneficial scheme is the Edelweiss Absolute Return Fund - Growth but if the return of the schemes are considered then UTI Wealth Builder Fund - Series II - Growth and SBI Magnum Sector Funds Umbrella- Emerging Buss Fund - Growth are more viable from the investment point of view again the investors who have invested in these schemes since last 3 years have benefited more in comparison with the investors who have invested in such schemes since inception. So the most profitable period for investors to invest in the Equity Diversified schemes can be said is of last 3 years. Again as per the ranking Equity Sector Funds Risk Analysis

- 61. In the top 5 schemes of Equity Sector funds for risk analysis all the measure have more or less the same result so there is hardly any difference in the preference. High Sharpe and Treynor. And SBI Magnum Sector Funds Umbrella - Pharma - Growth can be said to be least preferred from amongst others in case of risk analysis of top 5 schemes of equity sector funds. Return Analysis

- 62. The investment in the top 5 schemes of Equity Sector Funds advisable for a long term period as investment in short term period yields negative returns to the investor. So only those investors who are planning to retain the mutual fund investment as their asset for more than a year invest in such schemes. The growth in 3 years investment in higher than the growth in the 5years investment and a balance growth between the two is for the investors who had invested in the Equity Sector Fund since inception. As per the ranking the SBI Magnum Sector Fund Umbrella-Pharma-Growth is the first ranked scheme to invest in but the scheme that has shown the highest growth in terms of return is the Reliance Pharma Fund - Growth scheme. Irrespective of the long term period of investment that is 3 years, 5 years or since inception the Reliance Pharma Fund - Growth have shown the highest growth in terms of return analysis to the investor. But others schemes in the Equity Sector Fund also have a good amount of return to the investor as all the schemes have more or less the similar return to the investors.