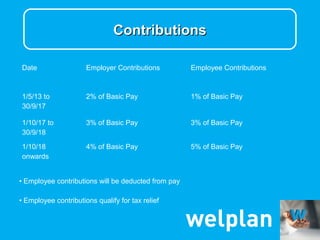

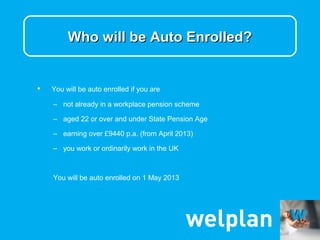

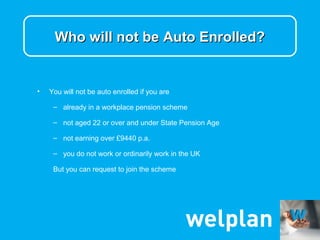

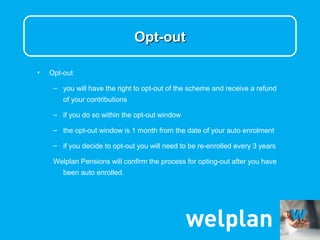

The document summarizes an employer's auto-enrollment of employees into a pension scheme called Welplan Pensions, as required by law. It outlines that eligible employees will be automatically enrolled beginning May 1, 2013, with the option to opt out within one month. It details the contribution levels from both employers and employees over time. It also provides information about who will and will not be automatically enrolled, the enrollment process, investment options within the pension, and benefits at retirement.