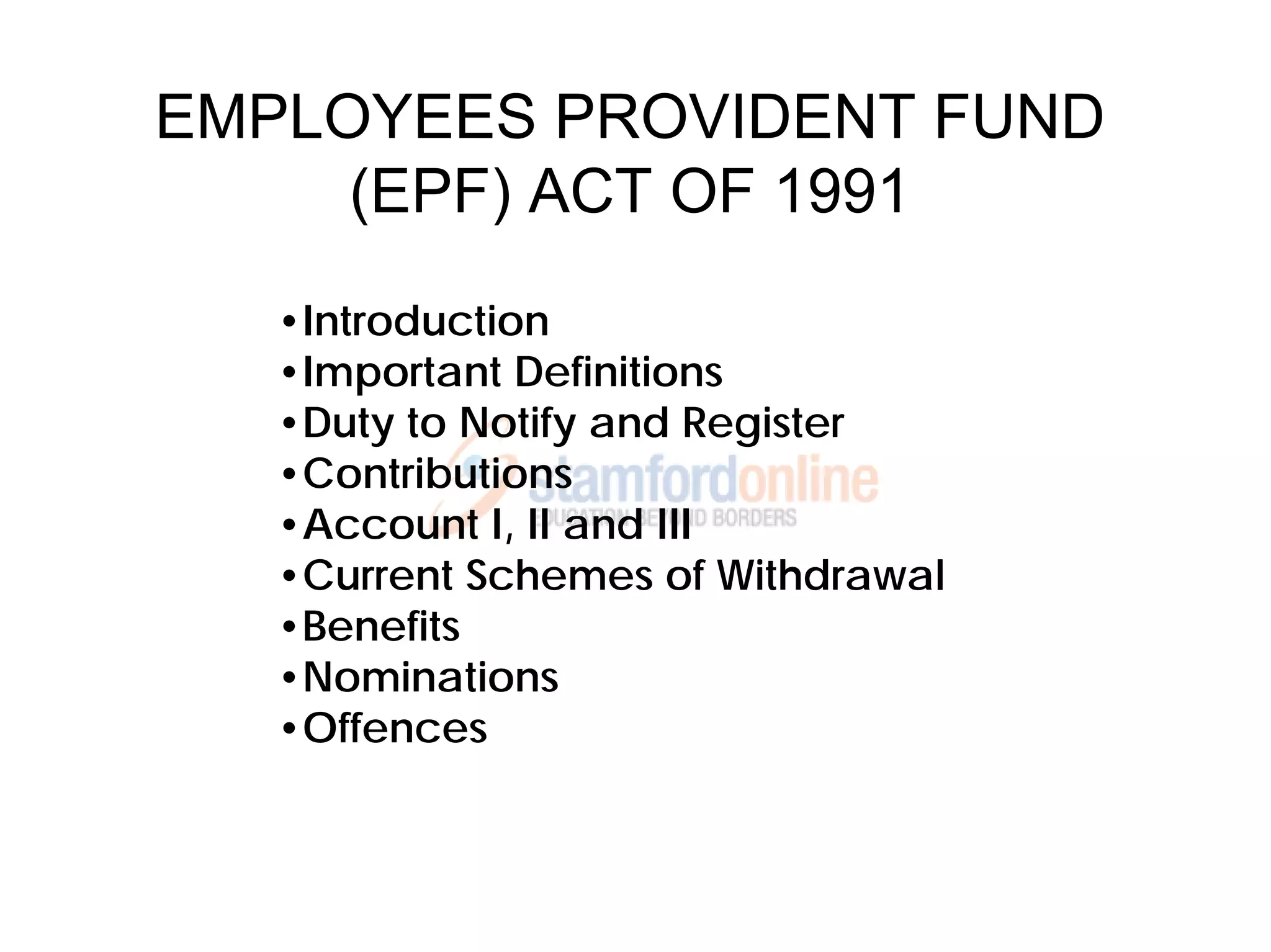

The document summarizes the key aspects of the Employees Provident Fund Act of 1991 in Malaysia, including its objectives to provide financial security for retirement, important definitions, employer and employee contribution requirements at a rate of 12% and 11% of wages respectively, and circumstances for withdrawal of contributions such as upon reaching age 55, death, or permanent incapacity. Employers have a duty to register with the EPF and pay contributions on time, with penalties for non-compliance. Unclaimed contributions refer to savings of members aged 65+ who have not contributed or withdrawn for over 10 years.