Do you want to understand the basic economic questions that every nation faces?

This presentation explains why scarcity and choice are the basics of economics.

FUNDAMENTALS

OF ECONOMICS

At theend of this unit, we should:

Understand the basic economic questions that

every nation faces.

Explain why scarcity and choice are the basics of

economics.

2.

The Basic

Problem in

Economics

•What is the basic difference between a ‘need’ and a

‘want’?

• Make a list of common needs for human survival and

wants for human comfort.

• Need: Something essential for human survival (food,

shelter, clothing)

• Want: Something that is desired but not necessary for

survival (video games, wigs).

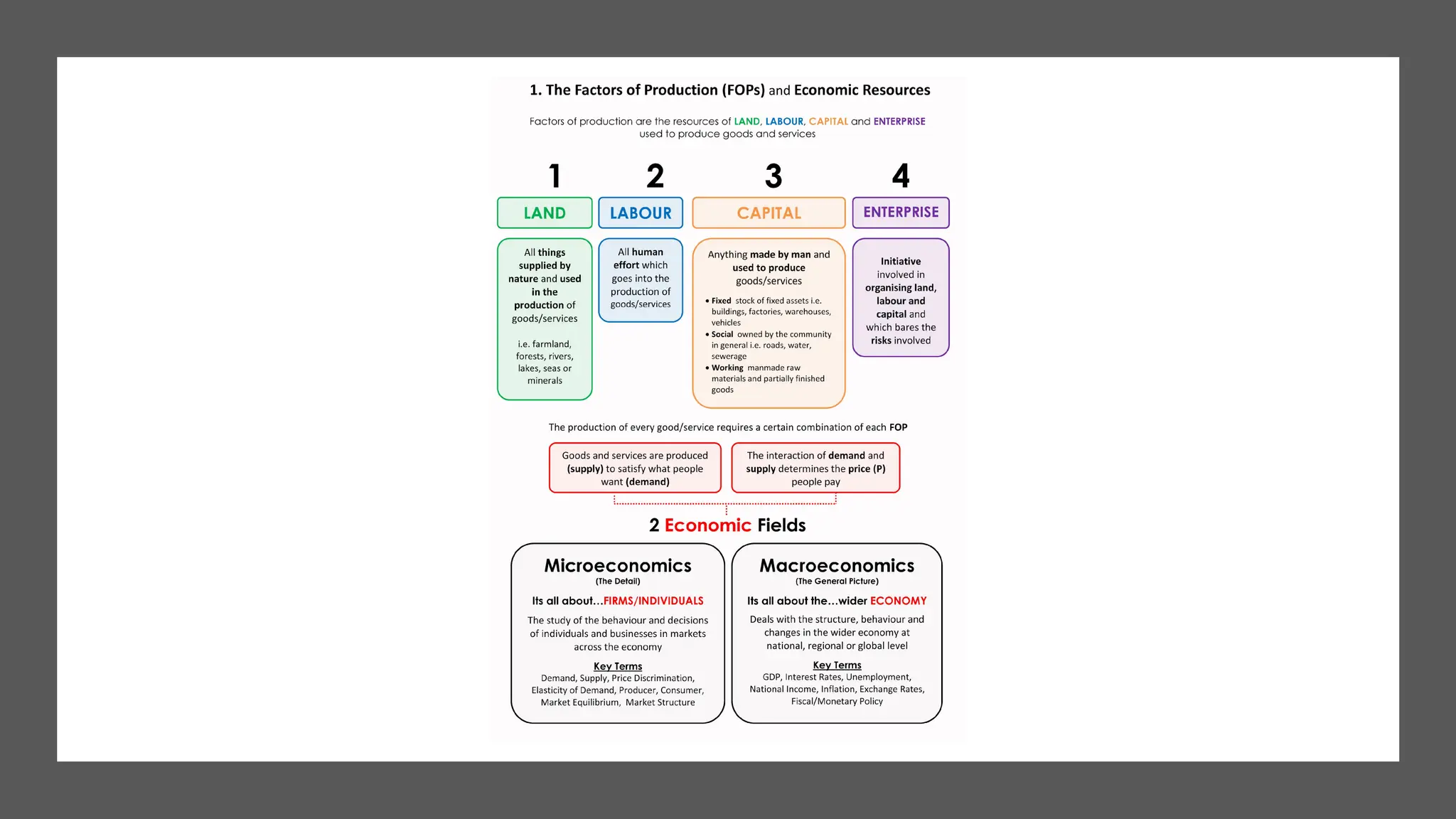

• Economics: The study of how individuals, families,

businesses, societies use limited resources to satisfy

unlimited wants.

• Microeconomics: Behavior and decisions made by small

economic units.

• Macroeconomics: Behaviors and decisions made by

regional/national economy.

3.

Fundamentals

of Economics:

Content

Vocabulary

• EconomicsMicroeconomics Macroeconomics

• Scarcity Factors of Production Land

• Labor Capital Goods

• Services Productivity Entrepreneur

• Technology Trade-off Opportunity Cost

• Production Possibility Curve Hypothesis

• Economic Model

4.

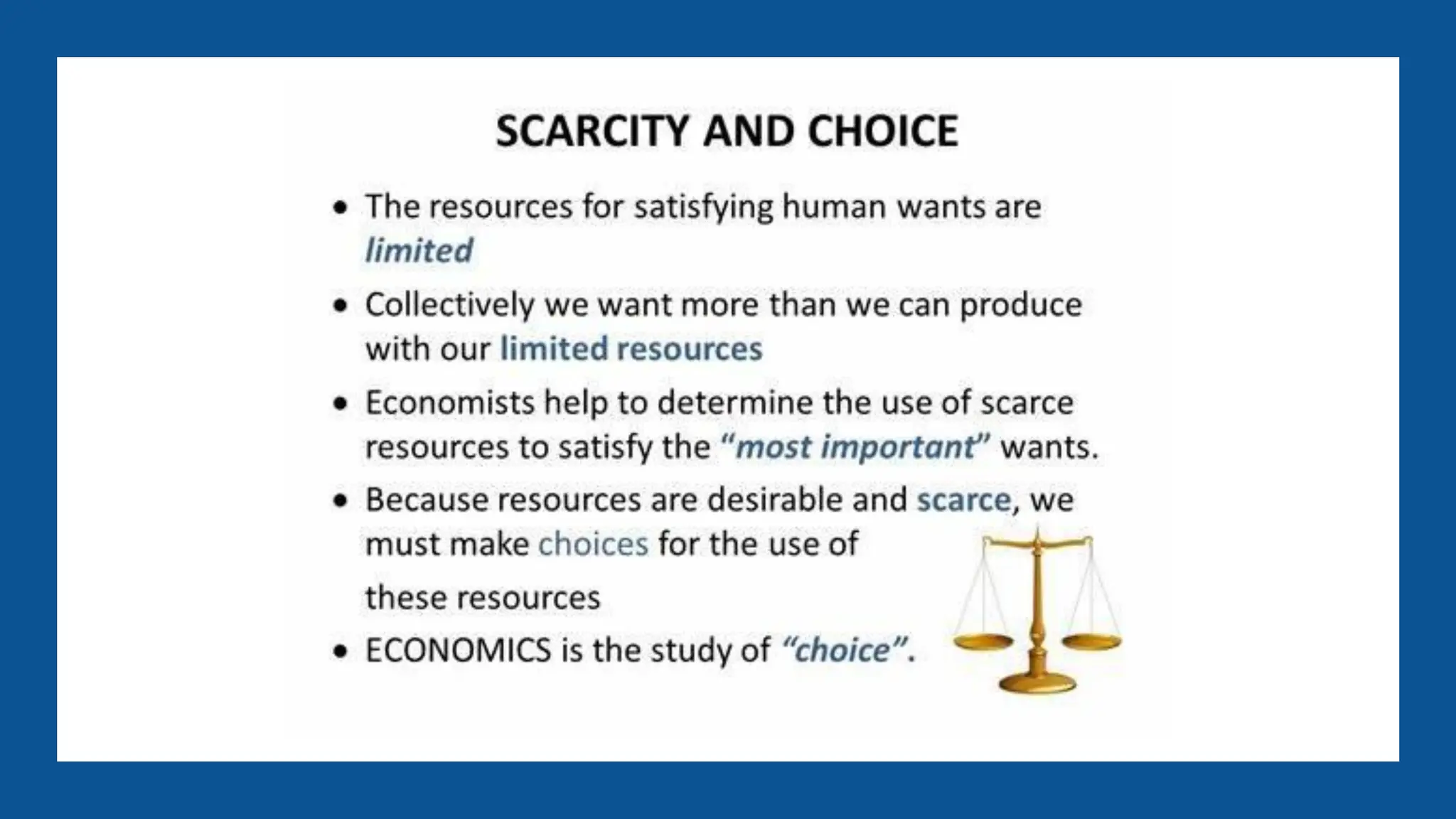

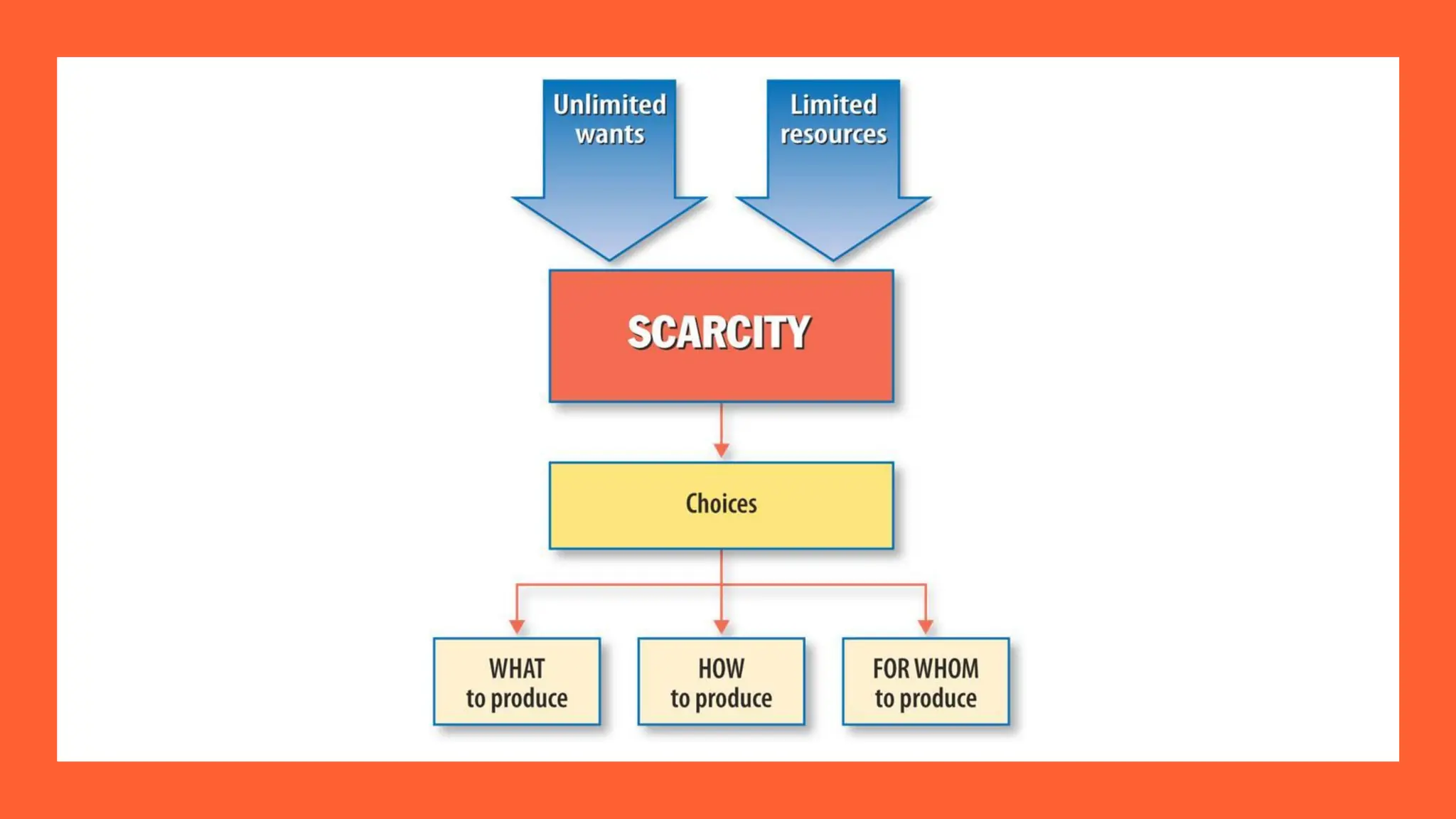

Scarcity

• Economics isthe study of how individuals, businesses and governments make choices

when faced with limited resources.

• Scarcity: Limited amounts of goods and services are available to meet unlimited wants.

Scarcity forces us to make choices by deciding which options are the most important

ones.

• Goods: Physical (tangible) objects that can be manufactured or produced. (clothing,

furniture, computers).

• Services: Activities (intangible) that one person performs on the behalf of another for a

fee (medical care, legal aid, education, ).

• Shortages: The temporary unavailability of goods and services due to some natural or

man-made occurrence (disaster). Shortage is not the same as scarcity. Scarcity always

exists, while shortage is temporary.

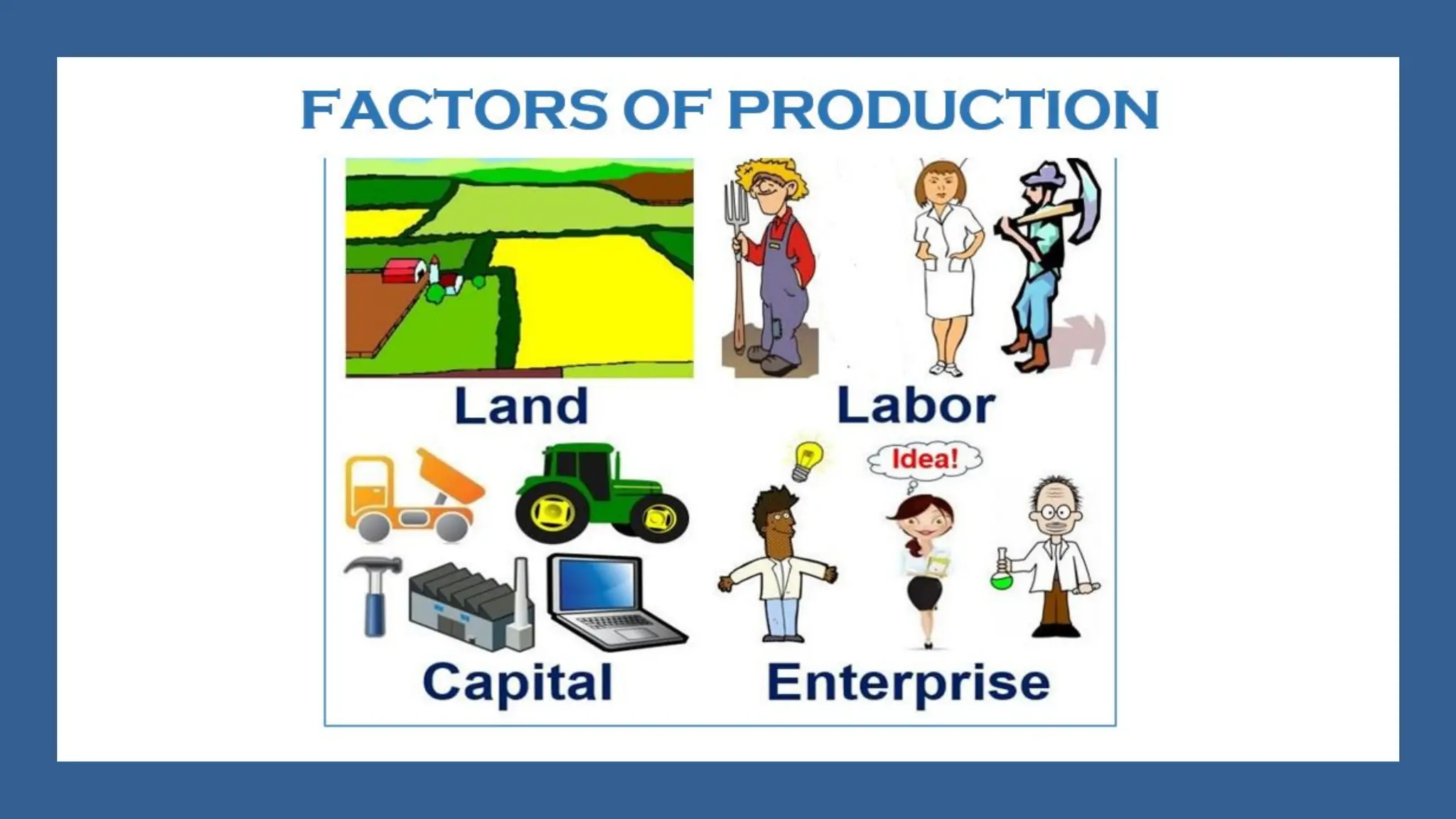

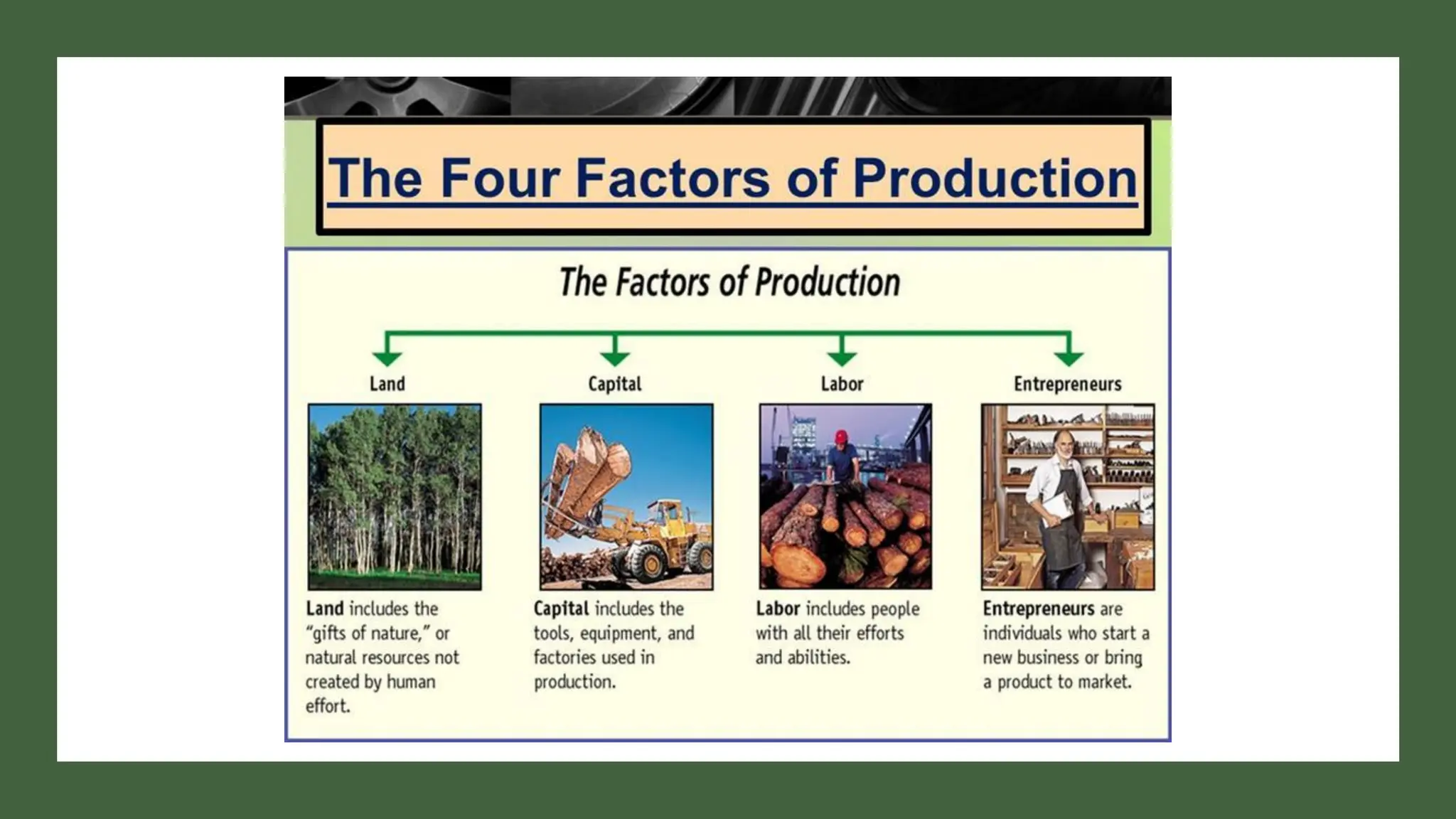

7.

The Factors of

Production1

• Scarce resources require choices about the uses of the

factors of production. The FOP are the resources needed to

produce goods and services. These include: Land, Labor,

Capital, Entrepreneurship and Technology.

• Entrepreneurs: Persons who decide how to combine

resources to create new goods and services.

• Land: Natural resources that exist without human

intervention (farming land, oil, iron, coal, water, forests, air,

animals, mineral deposits and other gifts of nature).

• Labor: Human resources- any work done by humans to

produce goods and services. This includes medical care

provided, tightening of a bolt by an assembly-line worker or

the creation of an artist or musician.

8.

Factors of

Production 2

•Capital: The manufactured goods used to make other goods

and produce other. Capital can be divided into 2 types:

Human capital and physical capital.

• Physical Capital: Human made objects used to produce

other goods and services (Computers, machines, buildings,

and tools used in making automobiles).

• Human Capital: The knowledge and skills a worker gains

through education and experience.

• An economy requires both physical and human capital to

produce goods and services. When capital is combined with

land and labor, the value of all 3 FOP increases. Capital also

increases productivity.

• Productivity: Greater quantities of goods and services in

better and faster ways.

9.

Factors of

Production 3

•Entrepreneurship: The ability of individuals to start new

businesses, introduce new products and processes, and improved

management techniques.

• Entrepreneurship involves the initiative and willingness to take

risks in order to gain profits. ( About 30% of businesses fail; of the

70% that survive, only a few become wildly successful).

• Technology: Some economists add technology to the FOP.

Technology includes any use of land, labor and capital that

produces goods and services more efficiently. Today, technology

is used to describe new products and new methods of producing

goods and services.

• How much of each of the FOP an individual, or a nation has, will

determine his/her/its wealth. Nations/Individuals with many

natural resources tend to be wealthier than nations with few

natural resources.

13.

Trade-Offs

• Economic decisionsalways involve trade-offs that have costs.

The economic choices people make involve the exchanging of

one good/service for another. If you buy an iPhone, you are

exchanging your money for the right to own the iPhone.

• Trade-off: The sacrificing one good or service to purchase or

produce another. It can also be defined as the act of giving up

one benefit in order to gain another, greater benefit.

• Trade-offs often involve things that can be easily measured

(money, property, time). Trade-offs also include values that are

not easily measured (enjoyment, job satisfaction, altruistic

feelings of well being).

• The cost of a trade-off is what you give up in order to get or do

something else ( when you decide to study Econ for an hour,

you give up other activities you could have been engaged in

during the same time).

• Guns v. Butter: Government trade-off decisions based on the

choice to spending money on military priorities (guns) or

spending money on domestic needs (butter).

15.

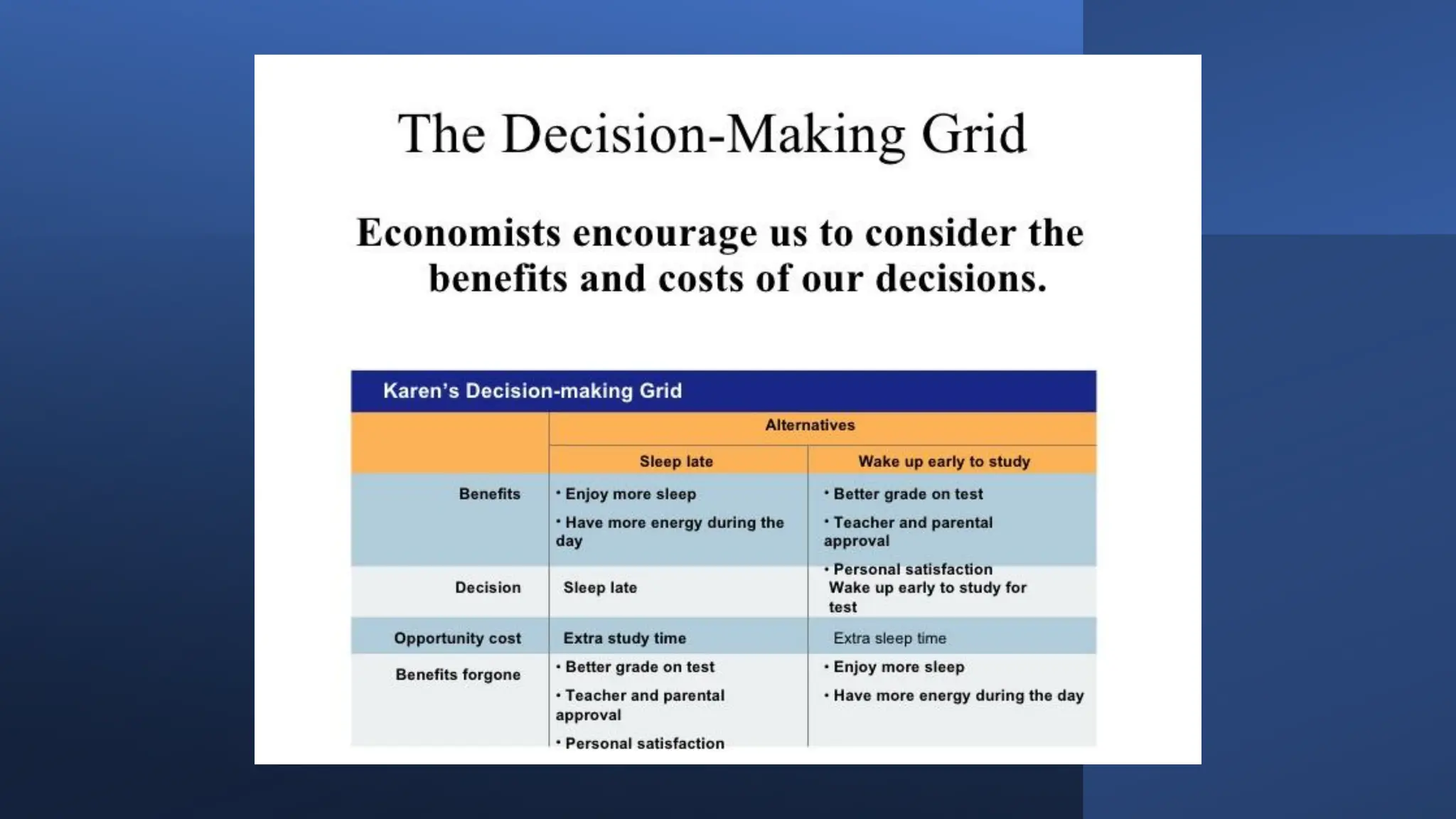

Opportunity Cost

•In mosttrade-off situations, one of the rejected alternatives is more

desirable than the rest.

•Opportunity Cost: The most desired alternative that was sacrificed as

a result of the decision. It is the value of the next best alternative that

had to be given up. When one makes a trade-off, they automatically

lose something. That something is the opportunity cost.

•Being aware of trade-offs and opportunity costs is vital to the making

of economic decisions at all levels. Businesses must consider

trade-offs and opportunity costs when they choose to invest funds or

hire workers to produce one good rather than another.

17.

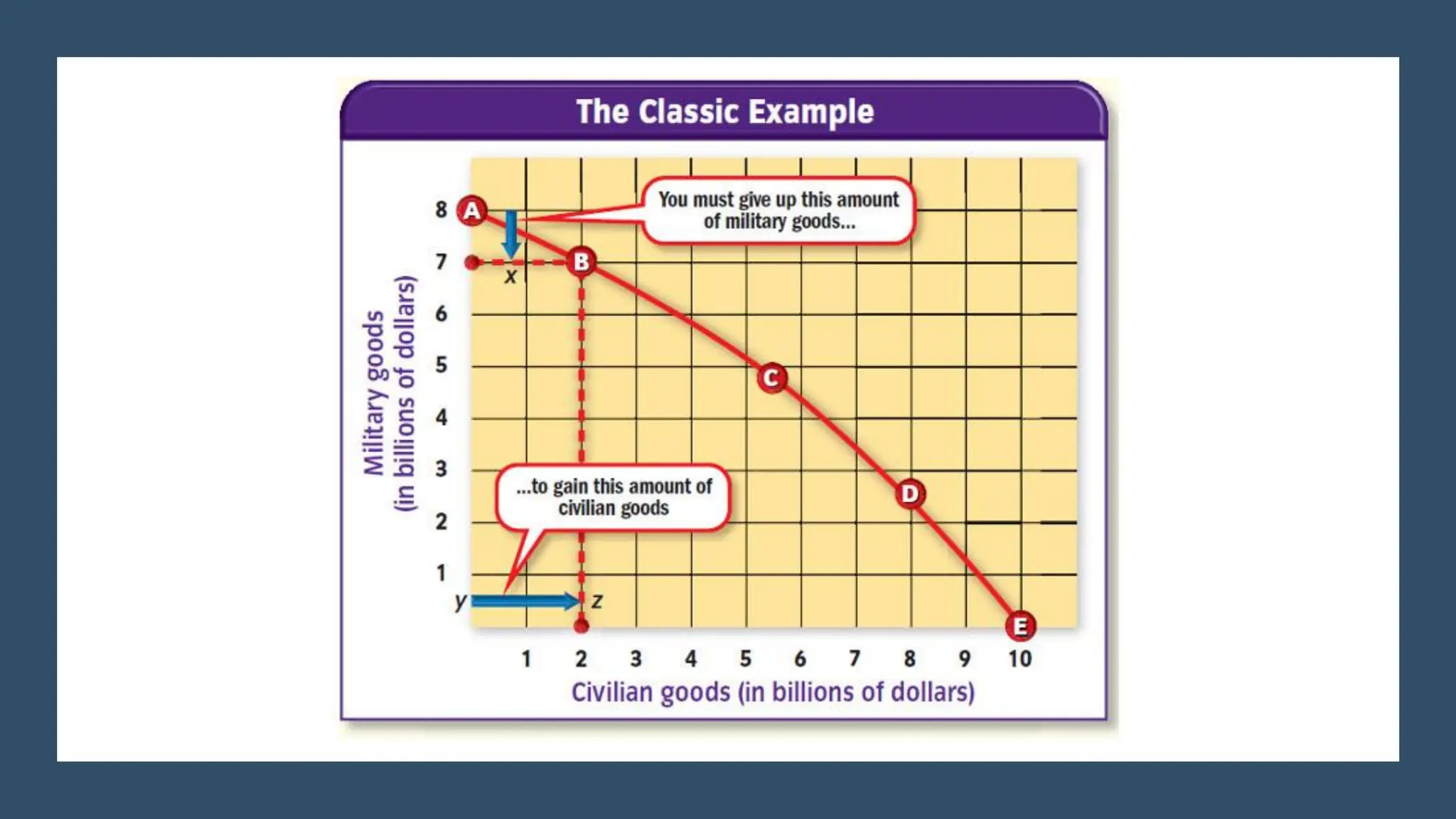

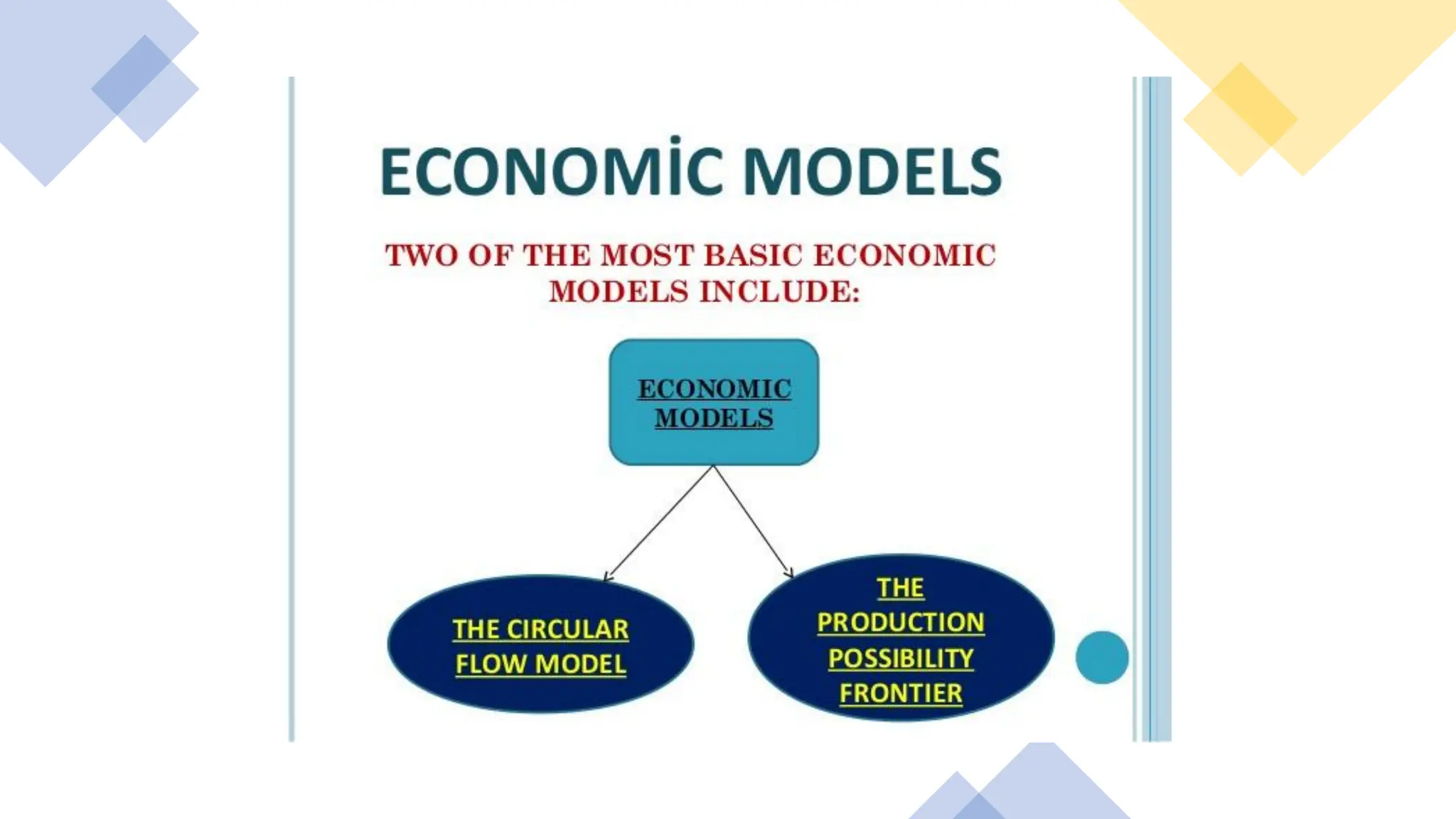

Production Possibility Curve

•Aproduction possibilities curve shows the maximum combinations of

goods and services that can be produced with a given amount of

resources.

•Many businesses produce more than one type of product (an

automobile manufacturer may produce several makes of cars per

plant in a given year. The company produces combinations of goods,

which results in an opportunity cost.

•The classic example of explaining production possibilities in

economics is the trade-off between military defense and civilian

goods (guns v butter).

19.

Economic

Models 1

• Economistsconstruct models to investigate the way that

economic systems work.

• To economists, the word economy means all of the activity

in a nation that together affects the production,

distribution, and use of goods and services.

• When economists study specific parts of the economy, they

often formulate theories and gather data from the real

world. These theories are called economic models. The

study of these models can help explain and predict

economic behavior.

• Economic models are simplified representations of the real

world. Economists test these models and use the solutions

to form the basis for actual decisions by businesses or

governments. No economic model records every detail and

relationships that exists about the problem being studied.

20.

Economic

Models 2

• Economicmodels show a visual representation of

consumer, business and other economic behavior. These

models all relate the way consumers and businesses

react to real-world changes.

• Economic models assume some factors remain constant

(material inputs, weather conditions, etc). A model will

show only the basic factors needed to analyze the

problem at hand.

• An economist begins with some idea about the way

things work, then collects facts and discards those

deemed irrelevant.

• Hypothesis: An educated guess or prediction,

• Testing a model/hypothesis allow economists to see if

the model is credible. Much of the work of economists

involves attempts at predicting how people will react in a

given situation (cutting taxes to stimulate the economy).