Learning

objectives

To understand thenature of economics as a

social science

To distinguish between microeconomics

and macroeconomics

To explain why scarcity exists and how it

forces choices to be made

To understand what is meant by

opportunity cost

To explain the connection between scarcity

and sustainability

Economics as asocial science

•Social sciences are

academic disciplines that

study human society and

social relationships.

16.

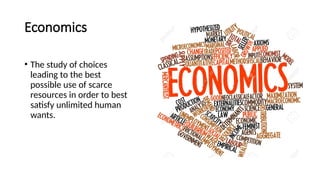

Economics

• The studyof choices

leading to the best

possible use of scarce

resources in order to best

satisfy unlimited human

wants.

17.

Do you thinklike an economist?

1. Because it is desirable, sunshine is scarce.

2. Because it is limited, asthma is scarce.

3. Because water covers three-fourths of the earth’s surface and is renewable,

it cannot be considered scarce.

4. The main costs of going to college are tuition and living expenses.

5. If public transportation fares are raised, almost everyone will take

the subway anyway.

6. You get what you pay for.

7. If someone makes an economic gain, someone else loses.

8. A business owner’s decision to show more care for consumers is a

decision to accept lower levels of profits.

18.

Micro vs macro

•Microeconomics is the study of

how households and firms make

decisions.

• Macroeconomics is the study of

the economy as a whole.

19.

Micro or macro?

•The price of Air Jordan 11s has risen by 20% since the end of last month.

• The government reduces individual income tax to boost consumer

spending.

• Haidilao is closing many dine-in locations due to poor performance.

• Petroleum producers see record profits.

• The total revenue of BYD car production has increased as consumers

purchase more electric vehicles.

• Consumers discover their purchasing power has fallen as the general

price level has risen.

23.

Scarcity: the fundamentalproblem of

economics

• Scarcity exists because

wants are unlimited and

resources are finite.

• As a result of scarcity,

choices have to be made.

24.

Scarcity, choice andopportunity cost

•The opportunity cost of

a choice/decision is the

next best alternative

foregone.

25.

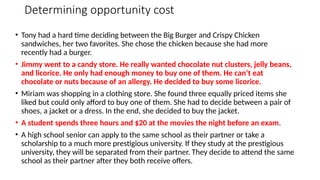

Determining opportunity cost

•Tony had a hard time deciding between the Big Burger and Crispy Chicken

sandwiches, her two favorites. She chose the chicken because she had more

recently had a burger.

• Jimmy went to a candy store. He really wanted chocolate nut clusters, jelly beans,

and licorice. He only had enough money to buy one of them. He can’t eat

chocolate or nuts because of an allergy. He decided to buy some licorice.

• Miriam was shopping in a clothing store. She found three equally priced items she

liked but could only afford to buy one of them. She had to decide between a pair of

shoes, a jacket or a dress. In the end, she decided to buy the jacket.

• A student spends three hours and $20 at the movies the night before an exam.

• A high school senior can apply to the same school as their partner or take a

scholarship to a much more prestigious university. If they study at the prestigious

university, they will be separated from their partner. They decide to attend the same

school as their partner after they both receive offers.

26.

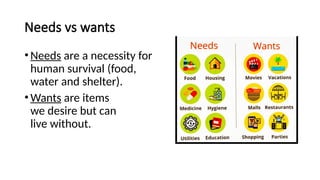

Needs vs wants

•Needsare a necessity for

human survival (food,

water and shelter).

•Wants are items

we desire but can

live without.

27.

Free goods

• Freegoods do not require

resources to produce them

and therefore have no

opportunity cost.

28.

Economic goods

• Economicgoods require

resources to produce them

and therefore have an

opportunity cost.

29.

Scarcity and sustainability

•Sustainability means using

scarce resources in a way that

does not leave behind fewer or

lower-quality resources for

future generations.

Learning

objectives

To understand thenine key concepts that underpin our study of

economics

To identify and explain the four factors of production

To identify and explain the three basic economic questions

To distinguish between the role of markets and government

intervention in designing and proposing solutions to the basic

economic questions

To distinguish between economic systems: the free market economy,

the planned economy and the mixed economy

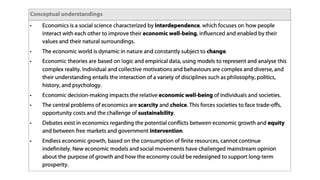

What is Economics?(again)

• A social science that studies the interdependence (1) of

people who interact with each other to improve their

economic well-being (2).

• Our world is complex and dynamic, so the economic plans of

individuals and nations are subject to change (3).

• The central problem Economics seeks to solve is scarcity (4).

34.

What is Economics?

•Scarcity, forces choices (5), and when people and nations make choices,

they give up one thing in favor of the other (tradeoffs, opportunity cost).

• Their choices also must consider the sustainability (6) of their plan. Can

it last?

• It also must consider if their choices about distributing scarce resources

leads to equity (7) in society (is it fair? Or do the rich just get

everything?). And if not, should there be government intervention (8) in

the economy to correct it?

• Or will that intervention destroy the very efficiency (9) in an economy

that creates the economic prosperity everyone is after?

36.

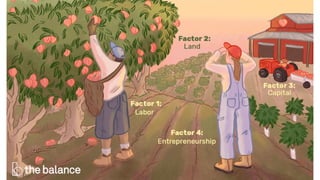

The factors ofproduction

•All resources that

are used to

produce goods

and services.

38.

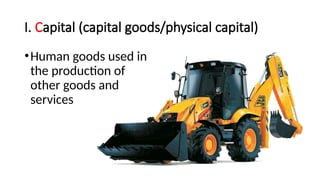

I. Capital (capitalgoods/physical capital)

•Human goods used in

the production of

other goods and

services

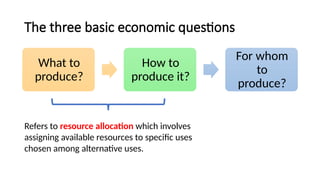

The three basiceconomic questions

What to

produce?

How to

produce it?

For whom

to

produce?

Refers to resource allocation which involves

assigning available resources to specific uses

chosen among alternative uses.

50.

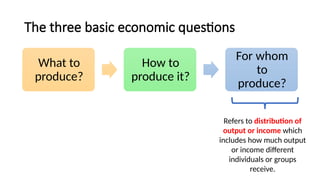

The three basiceconomic questions

What to

produce?

How to

produce it?

For whom

to

produce?

Refers to distribution of

output or income which

includes how much output

or income different

individuals or groups

receive.

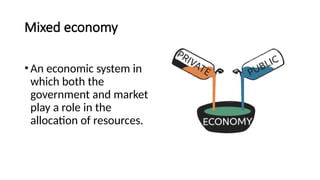

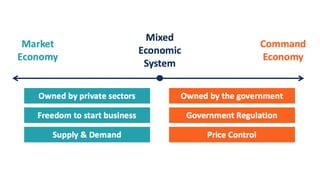

Mixed economy

•An economicsystem in

which both the

government and market

play a role in the

allocation of resources.

59.

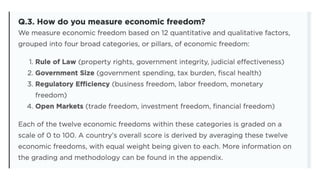

Rank the followingcountries from least

economically free to most economically free

•United States

•Ireland

•Luxembourg

•Malaysia

•Brazil

•Cuba

•North Korea

60.

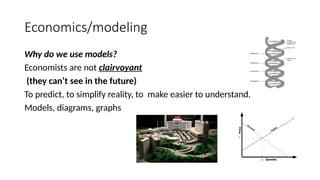

Economics/modeling

Why do weuse models?

Economists are not clairvoyant

(they can’t see in the future)

To predict, to simplify reality, to make easier to understand.

Models, diagrams, graphs

Learning objectives

•Identify andexplain relationships in the production

possibilities curve (PPC) model

•Use the PPC model to explain opportunity cost,

choice, scarcity, unemployment, efficiency, actual

growth and growth in production possibilities

•Draw a diagram to explain all of the above concepts in

a diagram

63.

The Production

Possibilities Curve

(PPC)

UsingEconomic Models…

Step 1: Explain concept in words

Step 2: Use numbers as examples

Step 3: Generate graphs from numbers

Step 4: Make generalizations using graph

63

64.

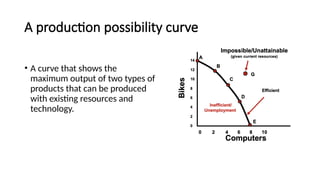

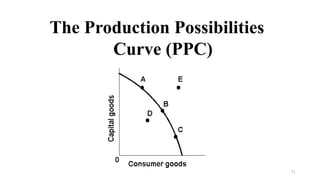

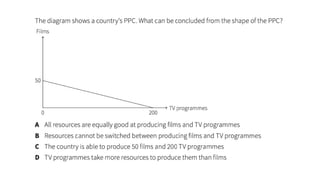

A production possibilitycurve

• A curve that shows the

maximum output of two types of

products that can be produced

with existing resources and

technology.

65.

Assumptions

•Only two goodscan be produced

•Full employment of resources

•Fixed Resources (Ceteris Paribus)

•Fixed Technology

66.

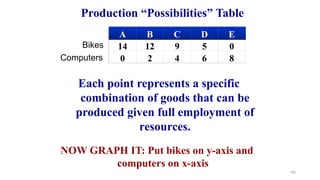

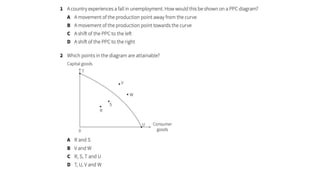

A B CD E f

14 12 9 5 0 0

0 2 4 6 8 10

Bikes

Computers

NOW GRAPH IT: Put bikes on y-axis and

computers on x-axis

Production “Possibilities” Table

Each point represents a specific

combination of goods that can be

produced given full employment of

resources.

66

67.

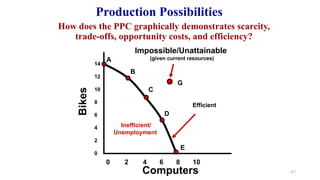

Bikes

Computers

14

12

10

8

6

4

2

0

0 2 46 8 10

A

B

C

D

E

G

Inefficient/

Unemployment

Impossible/Unattainable

(given current resources)

Efficient

Production Possibilities

How does the PPC graphically demonstrates scarcity,

trade-offs, opportunity costs, and efficiency?

67

68.

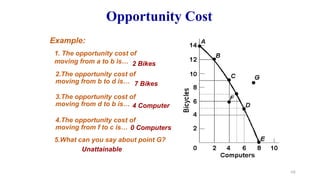

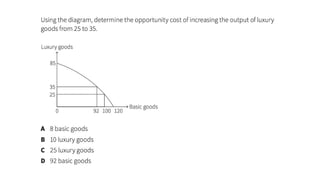

2 Bikes

2.The opportunitycost of

moving from b to d is…

4.The opportunity cost of

moving from f to c is…

3.The opportunity cost of

moving from d to b is…

7 Bikes

4 Computer

0 Computers

5.What can you say about point G?

Unattainable

1. The opportunity cost of

moving from a to b is…

Example:

Opportunity Cost

68

Learning objectives

•Distinguish betweenconstant and increasing

opportunity costs in the PPC model

•Draw a diagram to illustrate the difference between

constant and increasing opportunity costs in the PPC

model

73.

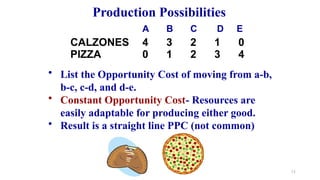

PIZZA 0 12 3 4

CALZONES 4 3 2 1 0

• List the Opportunity Cost of moving from a-b,

b-c, c-d, and d-e.

• Constant Opportunity Cost- Resources are

easily adaptable for producing either good.

• Result is a straight line PPC (not common)

Production Possibilities

A B C D E

73

74.

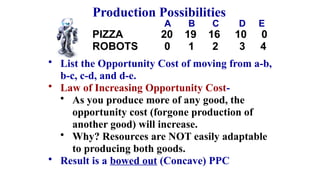

PIZZA 20 1916 10 0

ROBOTS 0 1 2 3 4

• List the Opportunity Cost of moving from a-b,

b-c, c-d, and d-e.

• Law of Increasing Opportunity Cost-

• As you produce more of any good, the

opportunity cost (forgone production of

another good) will increase.

• Why? Resources are NOT easily adaptable

to producing both goods.

• Result is a bowed out (Concave) PPC

A B C D E

Production Possibilities

75.

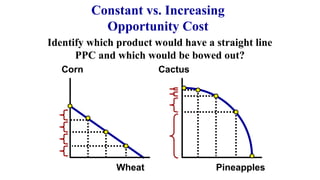

Constant vs. Increasing

OpportunityCost

Corn

Wheat

Cactus

Pineapples

Identify which product would have a straight line

PPC and which would be bowed out?

76.

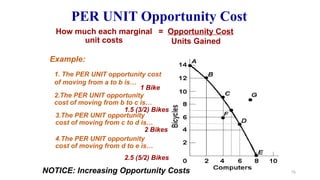

1 Bike

2.The PERUNIT opportunity

cost of moving from b to c is…

4.The PER UNIT opportunity

cost of moving from d to e is…

3.The PER UNIT opportunity

cost of moving from c to d is…

1.5 (3/2) Bikes

2 Bikes

2.5 (5/2) Bikes

= Opportunity Cost

Units Gained

1. The PER UNIT opportunity cost

of moving from a to b is…

Example:

PER UNIT Opportunity Cost

How much each marginal

unit costs

NOTICE: Increasing Opportunity Costs 76

4 Key AssumptionsRevisited

• Only two goods can be produced

• Full employment of resources

• Fixed Resources (4 Factors)

• Fixed Technology

What if there is a change?

Shifting the PPC

Change in resource quantity or quality 78

Production Possibilities

Panama – Favors

ConsumerGoods

Mexico – Favors

Capital Goods

Consumer goods

Capital

Goods

Current

PPC

Future

PPC

Consumer goods

Capital

Goods

Future

PPC

Current

PPC

Capital Goods and Future Growth

Mexico

Panama

83

Countries that produce more capital goods will have

more growth in the future.

84.

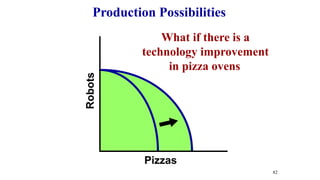

PPC Practice

Draw aPPC showing changes for each of the

following:

Pizza and Robots (3)

1. New robot making technology

2. Decrease in the demand for pizza

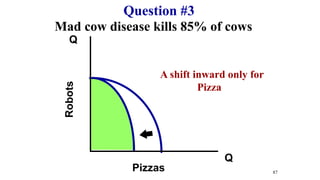

3. A disease kills 85% of cows

Consumer goods and Capital Goods (4)

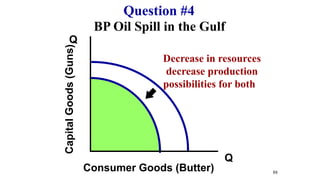

4. Destruction of power plants leads to severe

electricity shortage

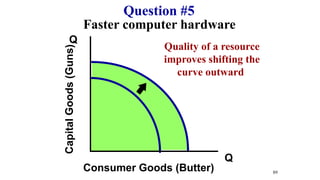

5. Faster computer hardware

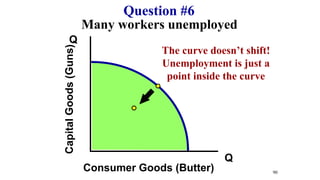

6. Many workers unemployed

7. Significant increases in education

84

85.

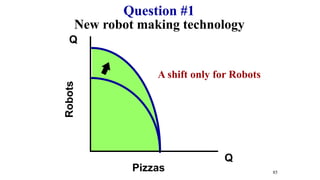

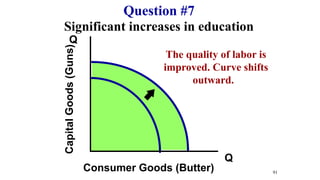

New robot makingtechnology

Q

Q

Robots

Pizzas

Question #1

85

A shift only for Robots

86.

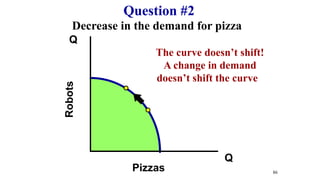

Decrease in thedemand for pizza

Q

Q

Robots

Pizzas

Question #2

86

The curve doesn’t shift!

A change in demand

doesn’t shift the curve

87.

Mad cow diseasekills 85% of cows

Q

Q

Robots

Pizzas

Question #3

87

A shift inward only for

Pizza

88.

BP Oil Spillin the Gulf

Q

Q

Capital

Goods

(Guns)

Consumer Goods (Butter)

Question #4

88

Decrease in resources

decrease production

possibilities for both

Learning objectives

• Todistinguish between positive and normative economics

• To explain the role of positive economics:

• The use of logic, hypotheses and theories

• The role of the ceteris paribus assumption

• The role of empirical evidence and refutation in positive economics

• To explain the role of normative economics:

• The role of value judgments in policy-making in normative economics

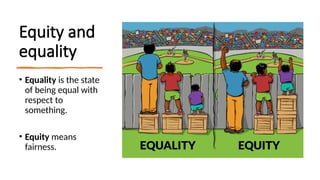

• To distinguish between equity and equality

98.

Positive statements areobjective statements

dealing with matters of fact that can be proven to

be truthful or false.

They may suggest an economic relationship that

can be tested by recourse to the available

evidence.

Positive statements

99.

Normative statements aresubjective -

based on opinion only - often without a basis

in fact or theory.

They are value-judgments, or emotional

statements that focus on "what ought to be".

Normative statements

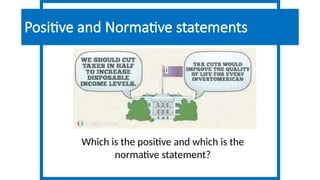

100.

Which is thepositive and which is the

normative statement?

Positive and Normative statements

101.

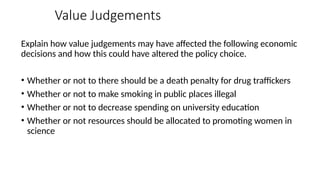

Value Judgements

Explain howvalue judgements may have affected the following economic

decisions and how this could have altered the policy choice.

• Whether or not to there should be a death penalty for drug traffickers

• Whether or not to make smoking in public places illegal

• Whether or not to decrease spending on university education

• Whether or not resources should be allocated to promoting women in

science

102.

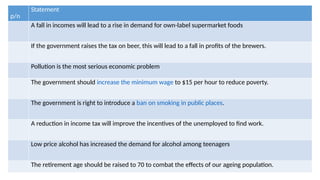

p/n

Statement

A fall inincomes will lead to a rise in demand for own-label supermarket foods

If the government raises the tax on beer, this will lead to a fall in profits of the brewers.

Pollution is the most serious economic problem

The government should increase the minimum wage to $15 per hour to reduce poverty.

The government is right to introduce a ban on smoking in public places.

A reduction in income tax will improve the incentives of the unemployed to find work.

Low price alcohol has increased the demand for alcohol among teenagers

The retirement age should be raised to 70 to combat the effects of our ageing population.

Logic, hypotheses andtheories

• Logic is a method of reasoning that involves making a series of

statements each of which is true if the preceding statement is true.

• A hypothesis is an educated guess.

• In economics a hypothesis will typically be formulated about a cause and

effect relationship.

• Economic theories are particular ideas or principles that aim to best

describe how an economy works.

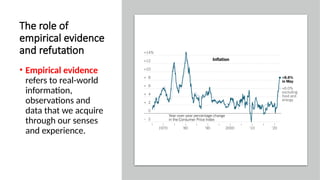

The role of

empiricalevidence

and refutation

• Empirical evidence

refers to real-world

information,

observations and

data that we acquire

through our senses

and experience.

107.

Refutation

• Refutation isthe act of

disproving something.

• Empirical data would be

necessary to support the

refutation.

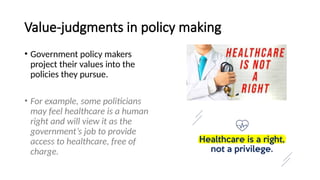

Value-judgments in policymaking

• Government policy makers

project their values into the

policies they pursue.

• For example, some politicians

may feel healthcare is a human

right and will view it as the

government’s job to provide

access to healthcare, free of

charge.

Learning objectives

• Tounderstand the origins of economic ideas in a historical context

• 18th century: Adam Smith and laissez faire

• 19th century: classical microeconomics (utility); the concept of the margin;

Classical macroeconomics; Marxist critique

• 20th century: Keynesian revolution, rise of macroeconomic policy,

monetarist/new classical counter revolution

• 21st century: Increased dialogue with other disciplines such as psychology

and the growing role of behavioral economics, increasing awareness of the

interdependencies that exist between the economy, society and environment

and the need to appreciate the compelling reasons for moving toward a

circular economy

115.

Brief history ofeconomic thought

• Economics is a relatively new science

• Adam Smith, “Wealth of Nations,” 1776 - Self interest, free trade, limited government

intervention, “Invisible Hand” – Economic man is rational – so we need a “Free Market”

• David Ricardo – Comparative advantage – nations trade based on abilities to produce with less

opportunity cost

• Jean-Baptiste “Say’s Law” – Supply creates its own demand. Spending will never fall enough to

prevent what is being produced from being sold. (Say what?)

• Karl Marx, “Communist Manifesto,” 1848 – reaction to free markets – Labor theory of value (value

of a product determined by labor put into it – difference between price and labor value is surplus

value (profit) = exploitation of workers – so we need a “Command Economy”

• Utility theory (1850s +)– Pleasure/satisfaction/benefit derived from consumption determines

value or price (Karl off the mark)

• Marginal Utility (1850s+) – What matters is not total utility but marginal utility, the pleasure

gained from consumption of an additional unit

116.

• Marginal Utility(1800s+) – What matters is not total utility but marginal utility, the

pleasure gained from consumption of an additional unit.

• Alfred Marshall (early 1900s) – marginal utility leads to “Law of demand” and demand

curve

• John Maynard Keynes, 1920s-1940s – Capitalist’s free-market reaction to communism

is the “Mixed Economy” (pretty much in use everywhere in world today)

• Milton Friedman – Friedrich Hayek, “Chicago School,” 1940s-1990s (1980s) reaction to

Keynesian economics – Supply side should drive economy not demand side (more of a

return to Free Markets)

• Behavioral Economics – Economic man is not rational (2008 “Nudge”) Richard Thaler

- humans are in fact predictably irrational when it comes to economic decision making;

Daniel Kahneman (2015) “Thinking fast and slow.” Quick judgements and biases

misguide our economic choices

• Circular economy (contemporary)– Sustainable economic growth means we need a

circular economy where products are built to be repaired not thrown away and that

are made from biological materials that if discarded, do not pollute the planet.

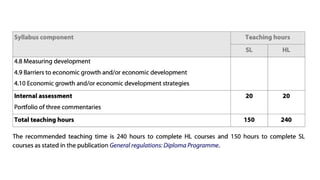

#6 Group 3 - The Group 3: Individuals and societies subjects of the IB Diploma Programme consist of ten courses offered at both the Standard level (SL) and Higher level (HL): Business Management, Economics, Geography, Global Politics, History, Information technology in a global society (ITGS), Philosophy, Psychology, Social and cultural anthropology, and World religions (SL only).[1] There is also a transdisciplinary course, Environmental systems and societies (SL only), that satisfies Diploma requirements for Groups 3 and 4.[

#20 5-7 minutes reading

10-15 minutes to choose

5-7 minutes discuss how choices were made, opportunity cost and the concept of scarcity

#26 Ask students to distinguish between needs and wants based on the image provided. Can they clarify if any needs may actually be wants?

#27 Students to name other free goods such as wind and water. Contrast against economic goods which require resources to produce and therefore have an opportunity cost such as consumer goods and services.

#30 Students generate ideas about how to preserve fresh water. Where does the problem lie and what is the solution?

#32 Students are given a specific term to lookup in the IB economics guide and explain its meaning with an example.

5 minutes

#38 Alternative meaning of capital – human capital, natural capital and financial capital ---- not applicable in our context.

#39 Goods and services purchased by households for their own satisfaction.

#47 The products could be given to the tallest people, smartest people, most important people, best friends, richest, neediest, and so on.) Encourage as many diverse suggestions as possible even if they are impractical. List suggestions on the board

Allow time for each group to decide which method of allocation it will use and tell the class. Discuss: • Who will benefit from your allocation method and who will suffer? • Do you think one allocation method is fairer than another? • Besides producing more, is there any way for everyone to be satisfied? (no) • What three questions did each group have to answer during this lesson? (What to produce? How to produce? F or whom to produce?)

#48 Students have just come up with an economic system that addresses the basic economic problem.