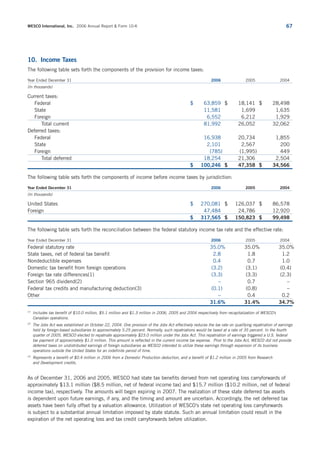

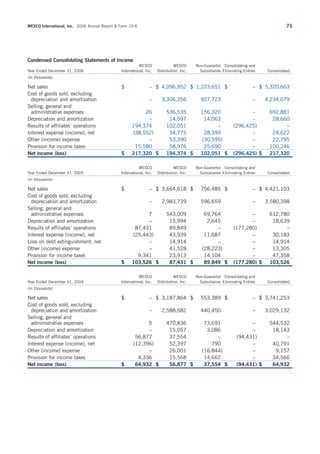

Download to read offline

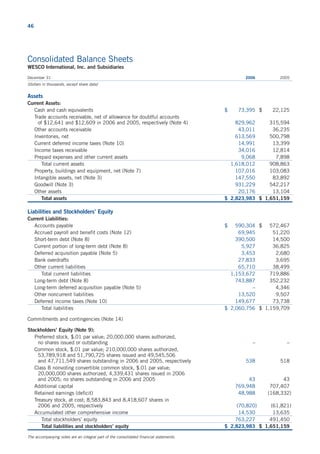

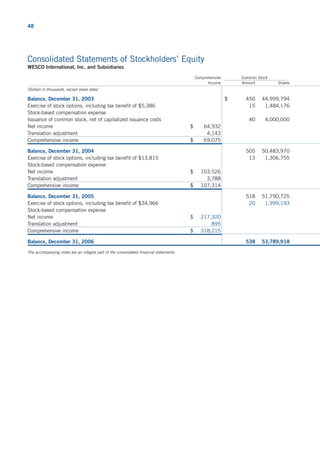

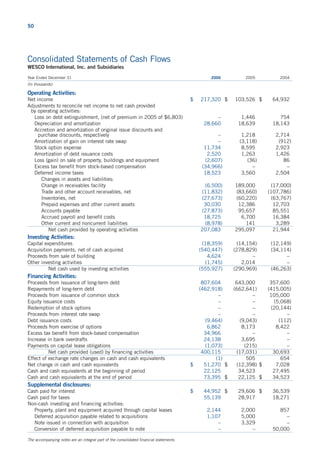

WESCO International, Inc. reported record financial results for 2006, with net sales increasing 20% to $5.32 billion and net income more than doubling to $217 million. The company's core electrical products distribution business drove excellent performance, as continued process improvements led to increased productivity and profitability. WESCO also integrated recent acquisitions, including Communications Supply Corporation, and expects additional acquisitions will be completed to further expansion. Looking ahead, the company is well positioned for continued growth with favorable market conditions and numerous opportunities identified for further performance gains.