Download to read offline

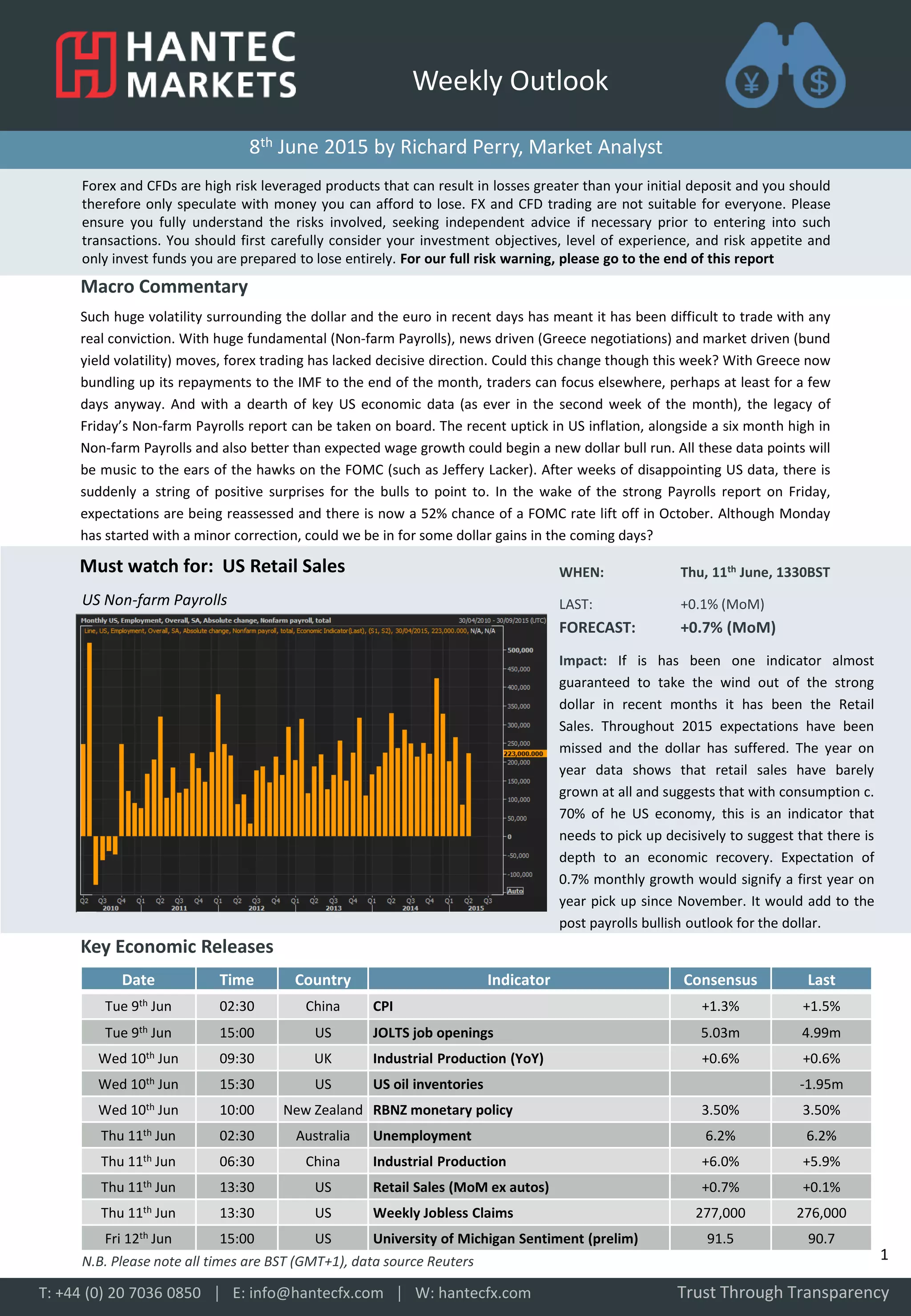

The document outlines the high-risk nature of forex and CFD trading, highlighting the need for cautious investment and full understanding of associated risks. It discusses recent volatility in currency markets, particularly concerning the US dollar and euro, and anticipates potential movements based on economic data releases, including US retail sales. Additionally, it notes the impact of strong non-farm payroll figures on market sentiment, suggesting a favorable outlook for the dollar amidst mixed equity market reactions.