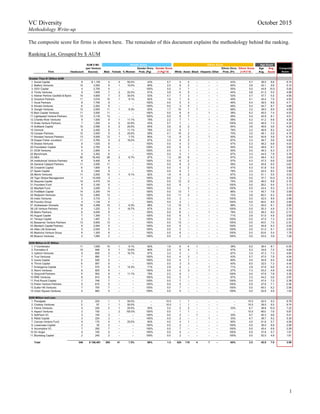

The document provides a methodology write-up for ranking venture capital firms based on a composite score calculated from gender, ethnic, and age diversity scores. It includes a table ranking 46 firms with over $1 billion in assets under management (AUM) based on their composite scores, as well as rankings of firms with between $250 million to $1 billion AUM and those with $250 million or less AUM. The composite score is calculated based on the gender, ethnic, and age diversity of each firm's investment team as explained in the methodology.

4.

4

This methodology walk-through addresses the following areas:

(i) Firm selection

(ii) People selection

(iii) Demographic variable estimation

(iv) Ranking methodology

(v) Appendix: Supplementary schedules are included at the end

I. Firm Selection

To compose a study of VC demographics, we wanted to select a representative number of funds with the following

characteristics:

(i) Firms based in the US: We are focusing on the diversity decisions of US firms, so international firms were

excluded

(ii) Traditional technology VC firms: We are focused on VC firms that invest mainly in technology-related startups;

notably this excludes biomedical / life science-focused VC firms or firms (though we include life sciences team

members if within a broader fund); we oriented around firms that have a Series A / Series B practice but

included any investors in growth stage products if broken out (e.g. DFJ, Sequoia)

(iii) Largest Firms: Using a combination of VentureSource and Mattermark, we force-ranked VC firms by AUM

and only looked at funds above $275M of AUM – we wanted to capture the firms which on a $ capital basis

represented a sizable portion of the market.

(iv) Active Firms: We did not include any firms that are less active which we estimated as either not having raised a

new fund in the last 5 years or that were not building their portfolio with new investments; this was based on

public signals or VentureSource

(v) High Mindshare: We included certain firms that commanded a high mindshare score from Mattermark to the

extent they weren’t already included (e.g. if below $275M AUM)

This resulted in a list of 71 firms representing over $160B in AUM, per VentureSource (see p. 1). We consider this a starting

point and can add additional peer firms as time goes on.

II. People Selection

For each of the firms, we wanted to measure the diversity of the “investment team leadership”. We are defining “investment

team leadership” as anyone holding the title of General Partner, Partner, Managing Director, and any other variation of the

senior investment titles on the investment team. We also include active Venture Partners and Board Partners to the extent

they are actively involved on the investment team. For A16Z, KPCB, Sequoia and Y-Combinator who designate all their

team members as “Partner”, we approximated the leadership team based on tenure, experience, leading deals and taking

board seats.

We do not include any junior investment team members (e.g. Associates, Vice Presidents or Principals) or other teams

(operating or growth teams, finance team, or other non-investment team functions). We also excluded people based in

international offices of US VC firms as we are focusing on team diversity within the US.

This gave us a list of 546 investment team leaders across the 71 firms.

There are a few reasons to focus on “investment team leaders”:

(i) Leaders drive the direction of the firm: These individuals most directly make decisions that affect the direction

of the firm, have investment-decision power and represent the firm on boards

(ii) Total would paint a different picture: People have already caught on that the few women hired in VC tend to be

hired in non-senior positions and/or non-investment team roles1

; Appendix 1 has our results on this disparity

(iii) Data is stable and consistent: Firms more consistently disclose the leaders on the website versus other team

members, so data availability is an issue for a total view. In addition, turnover is significantly higher at the

junior level, even on the investment team, as firms have different policies (e.g. 2-year programs).

III. Demographic Variable Estimation

For each of the individuals, we measured the following:

(i) Gender

(ii) Race / Ethnicity: We used the same definitions as the 2010 US census, which the large public tech firms also

follow in their diversity monitoring. Categories are the following:

1 CNBC (http://www.cnbc.com/2015/03/27/waiting-for-pao-verdict-where-are-women-at-top-vc-funds.html);

Fortune (http://fortune.com/2014/02/06/venture-capitals-stunning-lack-of-female-decision-makers/)

5.

5

a. “White” refers to a person having origins in any of the original peoples of Europe, the Middle East, or

North Africa

b. “Black or African American” refers to a person having origins in any of the Black racial groups of Africa

c. “Asian” refers to a person having origins in any of the original peoples of the Far East, Southeast Asia, or

the Indian subcontinent

d. “Hispanic” refers to people who identify their origin as Hispanic, Latino or Spanish

e. “Other” includes Native Hawaiian, Other Pacific Islander, American Indian or Alaskan Native

(iii) Age: We calculated age based on publicly available date-of-birth information. In instances where the date-of-

birth wasn’t available, we estimated age with LinkedIn by taking high school graduation year minus 18 or

college graduation year minus 22 and used 6/30 as the month/day. NOTE: We were only able to find a data

point for age for 532 individuals (97% of total).

IV. Ranking Methodology

The ranking methodology combines 3 variables:

(i) A gender diversity score

(ii) A race diversity score

(iii) An age score

For the gender diversity score and the ethnic diversity score, we use a diversity index based on probability to measure the

degree of concentration when individuals are classified into types. Simply stated, we create a diversity score based on the

probability that two investment team leaders taken at random from a VC firm will represent the same type. This approach

uses the same principal as the Simpson index (ecology) and Herfindahl index (economics)2

and has already been used in

population diversity studies3

.

Gender Diversity Score

The gender diversity score is calculated using the probability that any two individuals selected at random will be the same

gender. This is calculated as follows:

𝑃" =

1

𝑁(𝑁 − 1)

× 𝑀 𝑀 − 1 + 𝑊 𝑊 − 1

Pg = probability that two people randomly selected are the same (i.e. randomly select two men or two women)

N = total senior investment team members at a firm

M = number of men

W = number of women

Therefore, for a firm with 2 men and 2 women, the probability of randomly picking two people that are the same is:

𝑃" =

1

4(4 − 1)

× 2 2 − 1 + 2 2 − 1 = 33.3%

The gender score is simply 1 – this calculated probability, multiplied by 10 (for a scale of 0 to 10), or in the above example,

6.7.

𝐺𝑒𝑛𝑑𝑒𝑟

𝐷 𝑖𝑣𝑒𝑟𝑠𝑖𝑡𝑦

𝑆 𝑐𝑜𝑟𝑒 = 1 − 𝑃" ×10

The benefit of this methodology is that absolute diversity (i.e. agnostic to gender) is valued. In other words, a firm with only

men will receive a probability of picking 2 people at random that are the same of 100% which would translate into a gender

score of 0, but a firm with only women would also receive a gender score of 0. The higher the score, the better the diversity

profile.

Ethnic Diversity Score

The ethnicity score is based on the same principle as the gender score, only expanded to all the racial/ethnic categories:

White, Asian, Black, Latino/Hispanic, Other.

𝑃B =

1

𝑁(𝑁 − 1)

× 𝑊 𝑊 − 1 + 𝐴 𝐴 − 1 + 𝐵 𝐵 − 1 + 𝐻 𝐻 − 1 + 𝑂 𝑂 − 1

2 Diversity Index: https://en.wikipedia.org/wiki/Diversity_index#Simpson_index

3 USAToday: http://usatoday30.usatoday.com/news/nation/census/county-by-county-diversity.htm

6.

6

Pr = probability that two people randomly selected are the same (e.g. randomly select two While individuals)

N = total senior investment team members

W = number of White individuals

A = number of Asian individuals

B = number of Black individuals

H = number of Latino/Hispanic individuals

O = number of individuals with racial/ethnic category of “Other”

In this case, the ethnic diversity score is also 1 – this calculated probability, multiplied by 10 (for a scale of 0 to 10).

𝐸𝑡ℎ𝑛𝑖𝑐

𝐷 𝑖𝑣𝑒𝑟𝑠𝑖𝑡𝑦

𝑆 𝑐𝑜𝑟𝑒 = 1 − 𝑃" ×10

Below is an example of the Ethnic Diversity Score across a hypothetical 10 person firm with varying allocations.

W A B H O N Pr Score

2 2 2 2 2 10 11% 8.9

4 2 2 2 0 10 20% 8.0

6 2 2 0 0 10 38% 6.2

8 2 0 0 0 10 64% 3.6

10 0 0 0 0 10 100% 0

Note that while the 1st

orientation has a perfectly equal balance, there is always some chance that the two randomly selected

individuals will be the same (resulting in a score of 8.9 instead of intuitively a ‘perfect’ score); this is not an issue because for

similarly-sized firms, the score will still be better than the less diverse firms with similar headcount. For this reason we have

attempted to create sub-lists based on size (discussed below).

Age Score

The Age Score assigns a value to each senior investment team member based on his/her age.

To figure out what ages receive a perfect score, we looked at how old partners who did the best deals were when they

invested in those deals’ Series A or Series B, the earliest venture rounds where product-market fit is not readily apparent. To

do this, we looked at VentureSource’s list of top venture outcomes (defined as largest exits via M&A or IPO of VC-backed

companies) and compiled a list of all the partners who led the rounds in the corresponding Series A and/or B of these

outcomes. The results can be seen in the cumulative distribution function (CDF) below and the table with deals used can be

seen in Appendix 3.

Looking at this chart, 60% of the Series A’s and B’s of the largest exists were done by partners between the age of 35 and 46

(20% and 80%, respectively).

–

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65

CDF

of

Ages

@

Series

A/B

of

Best

Deals

20%:

35

yrs

80%:

46

yrs

Median:

41

7.

7

For the age score, we assigned any individual with the age between 35 and 46 to a perfect score of 10. Before 35 (to a

minimum of 22) and after 46 (to a maximum of 65) a decreased score was given. In order to give more “future credit” to

those younger than 35, we decreased the scores below 35 linearly and after 46 exponentially (i.e. a score 1 year outside the

alley on the low end, 34, will be higher than the score 1 year outside the alley on the high end, 47). A firm’s age score is

simply the average of the age scores of the individuals.

The argument for considering age is that younger partners are:

(i) More likely to be connected to newer technology

(ii) More likely to be connected to younger founders

(iii) More likely to be hungrier in their career

Note that this is purely conjecture to explain the data.

Composite Score: The Composite Score is the simple average between the Gender Diversity Score, Ethnic Diversity Score

and the Age Score. Calculating the composite score this way reflects the position that gender, ethnicity and age are equally

relevant variables in evaluating a fund’s future relevance.

Ultimately when comparing firms, we also grouped firms of similar size together and considered two approaches to do so,

presented on the first two pages of this document:

(i) By AUM:

a. Funds up to $250M AUM

b. Funds from $251M to $1.0B AUM

c. Funds with greater than $1.0B AUM

(ii) By Headcount of “senior investment team” members:

a. Funds with 5 people or less

b. Funds with 6-10 people

c. Funds with over 10 people

We submitted data points to firms in a request for comment to allow firms the ability to fact check the information.

–

2.0

4.0

6.0

8.0

10.0

22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65

Score

Ascribed

to

Each

Age

8.

8

Appendix 1: Investment Team Leadership vs. Full Team

The first three bars are based on data collected:

(i) Senior Investment Team: Representation of main data collected. Includes General Partners, Partners, Managing

Directors, Venture Partners etc. on the investment team

(ii) Junior Investment Team: Other members of the investment team such as Principals, VPs, Associates, Analysts,

Advisers, etc.

(iii) Non-investment team: Generally includes operational / support roles such as finance, legal, etc.

NOTE: Categories (ii) and (iii) have an issue of data availability (i.e. not all firms show their finance team) and should be

considered more “directional”.

Regarding gender, it is clear that women are hired more frequently into the junior ranks but do not have the same presence on

the senior team. Further, many more women exist outside of the team. The US population estimates for 2020 is shown on

the far right – both the VC community and the tech industry is far from the 50/50 split.

Regarding race, the senior investment team in venture capital is 78% white which is less diverse than the large tech

companies and significantly worse than the US population estimates for 2020.

92%

80%

60%

89%

77%

49%

8%

20%

40%

11%

23%

51%

Senior

Investment

Team Junior

Investment

Team Non-‐Investment

Team Y-‐Combinator

(W'14) Large

Tech

Avg.

(Leaders) US

in

2020

Gender

Distribution

%

Men %

Women

78%

63%

86%

70%

60%

20%

32%

13%

21%

6%

1%

2%

1%

2%

12%

1%

2%

1%

3%

19%

0%

3%

Senior

Investment

Team Junior

Investment

Team Non-‐Investment

Team Large

Tech

Avg.

(Leaders) US

in

2020

Race/Ethnic

Distribution

%

White %

Asian Black Hispanic Other

/

2+

9.

9

An updated scatter-plot of % women and % minorities can be found below. The vast majority of funds are below where the

US will be, and the magnitude of the disparity is largest when looking at representation of women vs. the US (i.e. firms are

very far away from 50%).

–

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

– 20% 40% 60% 80% 100%

% Women

% Minority

Felicis

Trinity

Mayfield

KPCB

Floodgate,

Cowboy,

Social Capital

Khosla

Scale

Canaan

US 2020:

51% Women

US 2020:

39% Minorities

Storm

Aspect

Tech Giants

10.

10

Appendix 2: US and Tech Giant Comps

The US Census data broken out is shown below.

The array of corresponding statistics for the leadership of large tech firms is below:

Our 2020

Designation Classification 2013 Stats %s

White

alone

(non-‐Hispanic) White 62.6% 199,400 59.6%

Black

or

African

American

alone Black 13.2% 41,594 12.4%

American

Indian

/

Alaskan

Native

alone Other

/

2+ 1.2% 2,432 0.7%

Asian

alone Asian 5.3% 19,255 5.8%

Native

Hawaiian

and

other

pacific

islander

alone Other

/

2+ 0.2% 595 0.2%

Two

or

more Other

/

2+ 2.4% 7,678 2.3%

Hispanic

or

Latino Hispanic 15.1% 63,551 19.0%

100.0% 334,505 100.0%

White 62.6% 59.6%

Asian 5.3% 5.8%

Black 13.2% 12.4%

Hispanic 15.1% 19.0%

Other

/

2+ 3.8% 3.2%

Total 100.0% 100.0%

US

Ethnic

Score 44% 41%

Male 155.7 165,036 49%

Female 160.8 169,467 51%

316.5 334,503 100%

US

Gender

Score 50% 50%

72% 75% 75% 77% 77% 77% 78% 83% 89% 92%

28% 25% 25% 23% 23% 23% 22% 17% 11%

8%

AAPL LNKD AMZN YHOO FB Tech AVG GOOG MSFT YC Founders

(W'14)

Senior VCs

Gender

% Men % Women

63% 65% 71% 70% 71% 72% 73% 78% 78%

37% 35% 29% 30% 29% 28% 27% 22% 22%

AAPL LNKD MSFT Tech AVG AMZN GOOG FB YHOO YC Founders

(W'14)

Senior VCs

Ethnicity

% White % Minority

12.

12

We have a total of 127 datapoints across the 50 of the largest exits

above for which we have the actual or estimated age of the partner at

the time of the Series A or B.

Name Fund Investment Series Deal

Date Age

@

Deal

1. Jim

Breyer Accel

Partners Facebook Series

A 5/1/05 43

2. Reid

Hoffman Greylock

Partners Facebook Series

A 5/1/05 37

3. Peter

Thiel Founders

Fund Facebook Series

B 4/1/06 38

4. David

Sze Greylock

Partners Facebook Series

B 4/1/06 43

5. Paul

Madera Meritech

Capital

Partners Facebook Series

B 4/1/06 49

6. Ron

Conway SV

Angel Facebook Series

B 4/1/06 55

7. John

Doerr Kleiner

Perkins

Caufield

&

Byers Google Series

A 6/7/99 47

8. Michael

Moritz Sequoia

Capital Google Series

A 6/7/99 44

9. Jim

Goetz Sequoia

Capital WhatsApp Series

A 4/8/11 45

10. Brian

Pokorny SV

Angel Twitter Series

A 7/1/07 26

11. Ron

Conway SV

Angel Twitter Series

A 7/1/07 56

12. George

Zachary Charles

River

Ventures Twitter Series

A 7/1/07 40

13. Fred

Wilson Union

Square

Ventures Twitter Series

A 7/1/07 45

14. Chris

Sacca Lowercase

Capital Twitter Series

A 7/1/07 31

15. Marc

Andreessen Andreessen

Horowitz Twitter Series

A 7/1/07 36

16. Mike

Maples

Jr. Floodgate Twitter Series

A 7/1/07 38

17. Steve

Anderson Baseline

Ventures Twitter Series

A 7/1/07 37

18. Bijan

Sabet Spark

Capital Twitter Series

B 5/1/08 38

19. Joi

Ito MIT

Media

Lab Twitter Series

B 5/1/08 41

20. Harry

Weller NEA Groupon Series

A 1/1/08 37

21. Kevin

Efrusy Accel

Partners Groupon Series

B 12/1/09 36

22. Fred

Wilson Union

Square

Ventures Zynga Series

A 1/15/08 46

23. Andy

Russell Pilot

Group Zynga Series

A 1/15/08 36

24. Rich

Levandov Avalon

Ventures Zynga Series

A 1/15/08

25. Brad

Feld Foundry

Group Zynga Series

A 1/15/08 42

26. Peter

Thiel Founders

Fund Zynga Series

A 1/15/08 40

27. Reid

Hoffman Greylock

Partners Zynga Series

A 1/15/08 40

28. Brian

Pokorny SV

Angel Zynga Series

A 1/15/08 27

29. John

Doerr Kleiner

Perkins

Caufield

&

Byers Zynga Series

B 7/18/08 57

30. Sandy

Miller Institutional

Venture

Partners Zynga Series

B 7/18/08 58

31. Vinod

Khosla Khosla

Ventures Cerent Series

B 4/1/97 42

32. Dan

Ciporin Canaan

Partners LendingClub Series

A 8/23/07 48

33. Jeff

Crowe Norwest

Venture

Partners LendingClub Series

A 8/23/07 49

34. Rebecca

Lynn Canvas

Venture

Fund LendingClub Series

B 3/19/09 36

35. Jeff

Clavier SoftTech

VC FitBit Series

A 10/10/08 40

36. Jon

Callaghan True

Ventures FitBit Series

A 10/10/08 39

37. Brad

Feld Foundry

Group FitBit Series

B 9/10/10 44

38. Aydin

Senkut Felicis

Ventures Fitbit Series

B 9/10/10 39

39. Mark

Kvamme Sequoia

Capital LinkedIn Series

A 11/1/03 42

40. Josh

Kopelman First

Round

Capital LinkedIn Series

A 11/1/03 32

41. David

Sze Greylock

Partners LinkedIn Series

B 10/1/04 41

42. Dave

Flanagan Intel

Capital Clearwire Series

A 6/1/04 34

43. Seth

Neiman Crosspoint Chromatis

Networks Series

A 10/1/98 44

44. Vinod

Khosla Khosla

Ventures Siara

Systems Series

A 11/15/98 43

45. Promod

Haque Norwest

Venture

Partners Siara

Systems Series

A 11/15/98 50

46. Michael

Marks Riverwood

Capital GoPro Series

A 5/5/11 59

47. Ned

Gilhuly Sageview

Capital GoPro Series

A 5/5/11 50

48. John

Ball Steamboat

Ventures GoPro Series

A 5/5/11 47

49. Chris

Rust Cyphort GoPro Series

A 5/5/11 45

50. Lip-‐Bu

Tan Walden

International GoPro Series

A 5/5/11 51

51. Kevin

Compton Kleiner

Perkins

Caufield

&

Byers ONI

Systems Series

A 12/1/97 39

52. Jon

Feiber Mohr

Davidow ONI

Systems Series

A 12/1/97 40

53. Felda

Hardymon Bessemer

Venture

Partners Sirocco

Systems Series

A 4/27/99 51

54. Roger

Evans Greylock

Partners Sirocco

Systems Series

A 4/27/99 49

55. Barry

Eggers Lightspeed

Venture

Partners Sirocco

Systems Series

A 4/27/99 35

56. Jim

Goetz Sequoia

Capital Palo

Alto

Networks Series

A 1/1/06 40

57. Asheem

Chandna Greylock

Partners Palo

Alto

Networks Series

A 1/1/06 41

58. Harry

Weller NEA Vonage Series

B 11/24/03 33

59. Thomas

Bredt Menlo

Ventures XROS Series

A 1/15/99 57

60. Randy

Komisar Kleiner

Perkins

Caufield

&

Byers Nest

Labs Series

A 9/21/10 54

61. Rob

Coneybeer Shasta

Ventures Nest

Labs Series

A 9/21/10 40

62. Bill

Maris Google

Ventures Nest

Labs Series

B 8/1/11 35

63. Peter

Nieh Lightspeed

Venture

Partners Nest

Labs Series

B 8/1/11 45

64. Larry

Kubal Labrador

Ventures Pandora

Media Series

A 1/1/00 47

65. Doug

Barry Selby

Ventures Pandora

Media Series

A 1/1/00 36

66. Larry

Marcus Walden

International Pandora

Media Series

A 1/1/00 48

67. Dave

Strohm Greylock

Partners DoubleClick Series

A 6/10/97 48

68. Deepak

Kamra Canaan

Partners DoubleClick Series

A 6/10/97 40

69. Ray

Rothrock Venrock DoubleClick Series

A 6/10/97 39

70. Todd

Dagres Spark

Capital Qtera Series

A 8/12/98 37

71. Todd

Brooks Mayfield

Fund Qtera Series

B 4/19/99 38

72. Jason

Stoffer Maveron Zulily Series

A 12/17/09 32

73. Eric

Carlborg August

Capital Zulily Series

B 8/4/10 45

74. Gus

Tai Trinity

Ventures Zulily Series

B 8/4/10 44

75. Gordon

Ritter Emergence

Capital Veeva

Systems Series

B 6/5/08 43

76. Dave

Strohm Greylock

Partners Cygnus

Solutions Series

A 2/15/97 48

77. John

Johnston August

Capital Cygnus

Solutions Series

A 2/15/97 41

78. Matthew

Howard Norwest

Venture

Partners FireEye Series

A 1/1/05 40

79. Gaurav

Garg Sequoia

Capital FireEye Series

A 1/1/05 38

80. Joe

Horowitz Icon

Ventures FireEye Series

B 8/23/06

81. Paul

Barber JMI

Equity ServiceNow Series

A 7/5/05 42

82. Alex

Finkelstein Spark

Capital Wayfair Series

A 6/21/11 34

83. Neeraj

Agrawal Battery

Ventures Wayfair Series

A 6/21/11 38

84. Michael

Kumin Great

Hill

Partners Wayfair Series

A 6/21/11 37

85. Ian

Lane HarvourVest Wayfair Series

A 6/21/11 33

86. Phil

Siegel Austin

Ventures HomeAway Series

A 1/1/05 39

87. Jeff

Brody Redpoint

Ventures HomeAway Series

A 1/1/05 43

88. Todd

Chaffee Institutional

Venture

Partners HomeAway Series

B 1/1/06 45

89. John

Moragne Trident

Capital HomeAway Series

B 1/1/06 45

90. Berry

Cash InterWest CIENA Series

A 4/1/94 52

91. David

Cowan Bessemer

Venture

Partners CIENA Series

B 12/1/94 28

92. Scott

Tobin Battery

Ventures Akamai

Technologies Series

A 12/14/98 27

93. Todd

Chaffee Institutional

Venture

Partners Akamai

Technologies Series

A 12/14/98 38

94. Andrew

Schwab 5am

Ventures Ikaria Series

A 9/26/05 33

95. Robert

Nelsen ARCH

Venture

Partners Ikaria Series

A 9/26/05 41

96. Bryan

Roberts Venrock Ikaria Series

A 9/26/05 37

97. Forest

Baskett,

PhD NEA Tableau

Software Series

A 1/1/04 60

98. Robert

Nelsen ARCH

Venture

Partners Juno

Therapeutics Series

A 12/3/13 50

99. Bong

Koh Venrock Juno

Therapeutics Series

A-‐2 12/3/13 40

100. David

Hornik August

Capital Splunk Series

A 12/1/04 36

101. Thomas

Neustaetter JK&B

Capital Splunk Series

B 1/1/06 53

102. Antonio

Rodriguez Matrix

Partners Oculus

VR Series

A 6/17/13 38

103. Santo

Politi Spark

Capital Oculus

VR Series

A 6/17/13 46

104. Joe

Lonsdale Formation

8 Oculus

VR Series

A 6/17/13 30

105. Brian

Singerman Founders

Fund Oculus

VR Series

A 6/17/13 34

106. Chris

Dixon Andreessen

Horowitz Oculus

VR Series

B 12/12/13 40

107. Scott

Sandell NEA Fusion-‐io Series

A 3/31/08 43

108. Chris

Schaepe Lightspeed

Venture

Partners Fusion-‐io Series

B 4/7/09 43

109. Blake

Modersitzki Pelion

Venture

Partners Fusion-‐io Series

B 4/7/09 39

110. Fred

Wilson Union

Square

Ventures Etsy Series

A 11/1/06 45

111. Josh

Stein Draper

Fisher

Jurvetson Box Series

A 10/1/06 32

112. Winston

Fu US

Venture

Partners Box Series

B 1/23/08 41

113. Steve

Jurvetson Draper

Fisher

Jurvetson TradeX

Technologies Series

B 3/1/98 30

114. Ping

Li Accel

Partners Nimble

Storage Series

A 12/21/07 35

115. Jim

Goetz Sequoia

Capital Nimble

Storage Series

A 12/21/07 42

116. Barry

Eggers Lightspeed

Venture

Partners Nimble

Storage Series

B 12/24/08 45

117. Andrew

Marcuvitz Matrix

Partners Broadband

Access

Systems Series

A 7/1/98

118. Vinod

Khosla Khosla

Ventures Juniper

Networks Series

A 6/11/96 41

119. Seth

Neiman Crosspoint Juniper

Networks Series

B 8/5/96 42

120. Andy

Rachleff Benchmark

Capital Juniper

Networks Series

B 8/5/96 37

121. Geoff

Yang Redpoint

Ventures Juniper

Networks Series

B 8/5/96 36

122. Peter

Barris NEA Juniper

Networks Series

B 8/5/96 43

123. Michael

Moritz Sequoia

Capital Green

Dot

Corp. Series

A 1/1/03 48

124. Douglas

Leone Sequoia

Capital Rackspace

Hosting Series

B 3/27/00 41

125. George

Still Norwest

Venture

Partners Rackspace

Hosting Series

B 3/27/00 41

126. Bryan

Roberts Venrock Castlight

Health Series

A 8/1/09 41

127. Roelof

Botha Sequoia

Capital Youtube Series

A 11/1/05 33

128. Jim

Swartz Accel

Partners Avici

Systems Series

A 5/1/97

129. Matt

Gorin Contour

Venture

Partners OnDeck

Capital Series

A 1/1/06

130. Matt

Harris Bain

Capital

Ventures OnDeck

Capital Series

A 1/1/06 33

131. David

Weiden Khosla

Ventures OnDeck

Capital Series

B 1/1/07 34

132. James

Robinson

III RRE

Ventures OnDeck

Capital Series

B 1/1/07 71