Downloaded 224 times

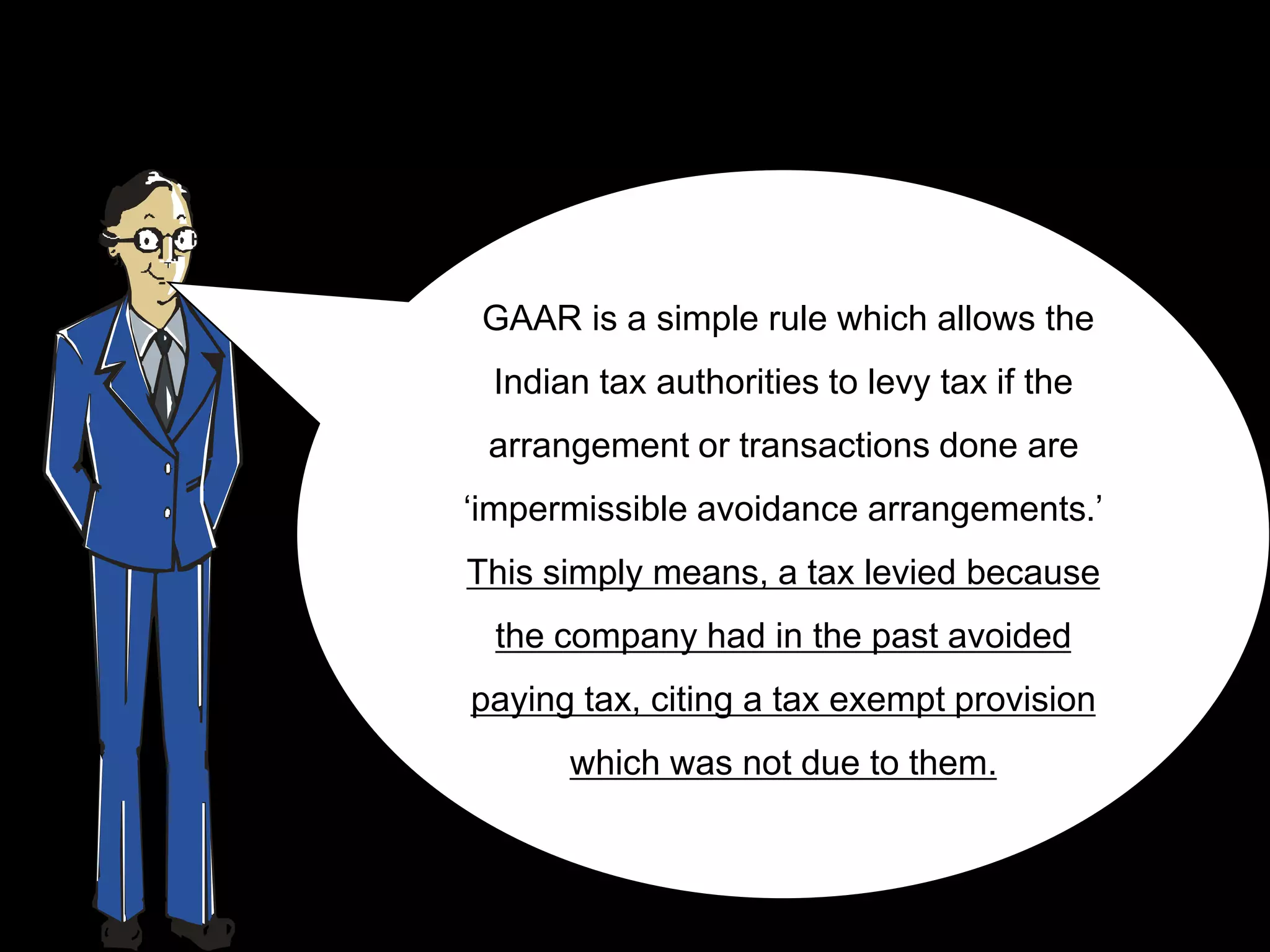

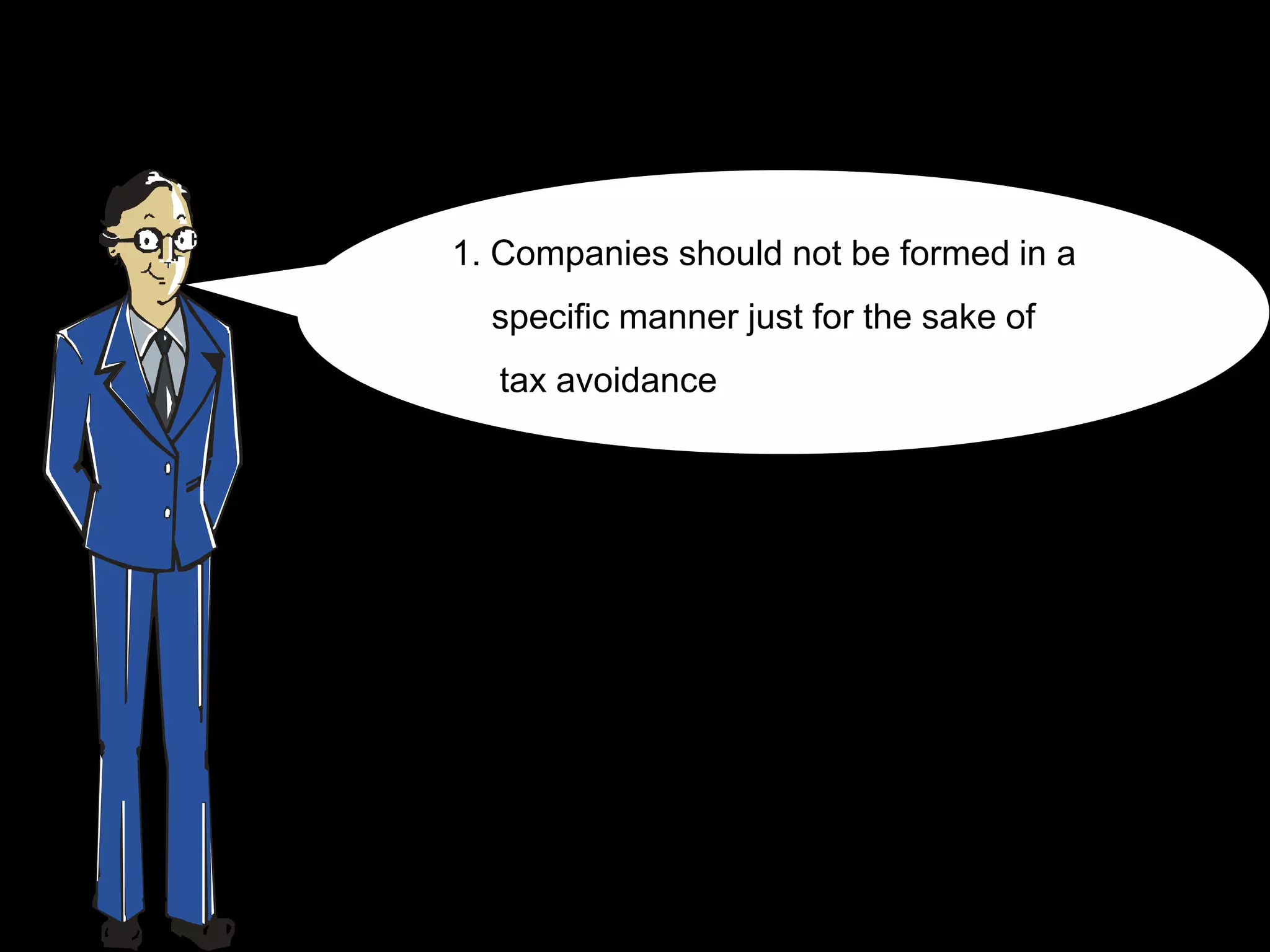

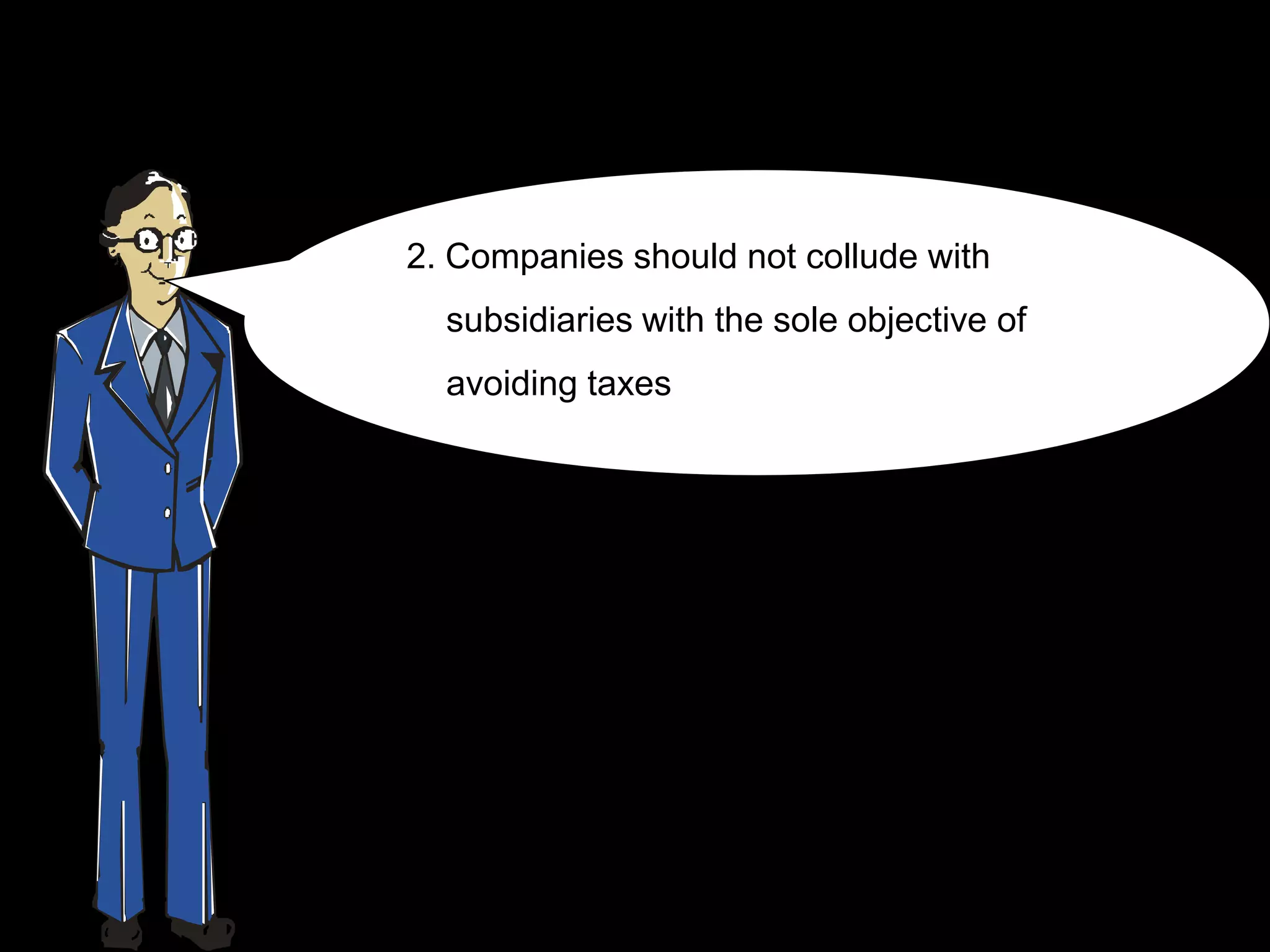

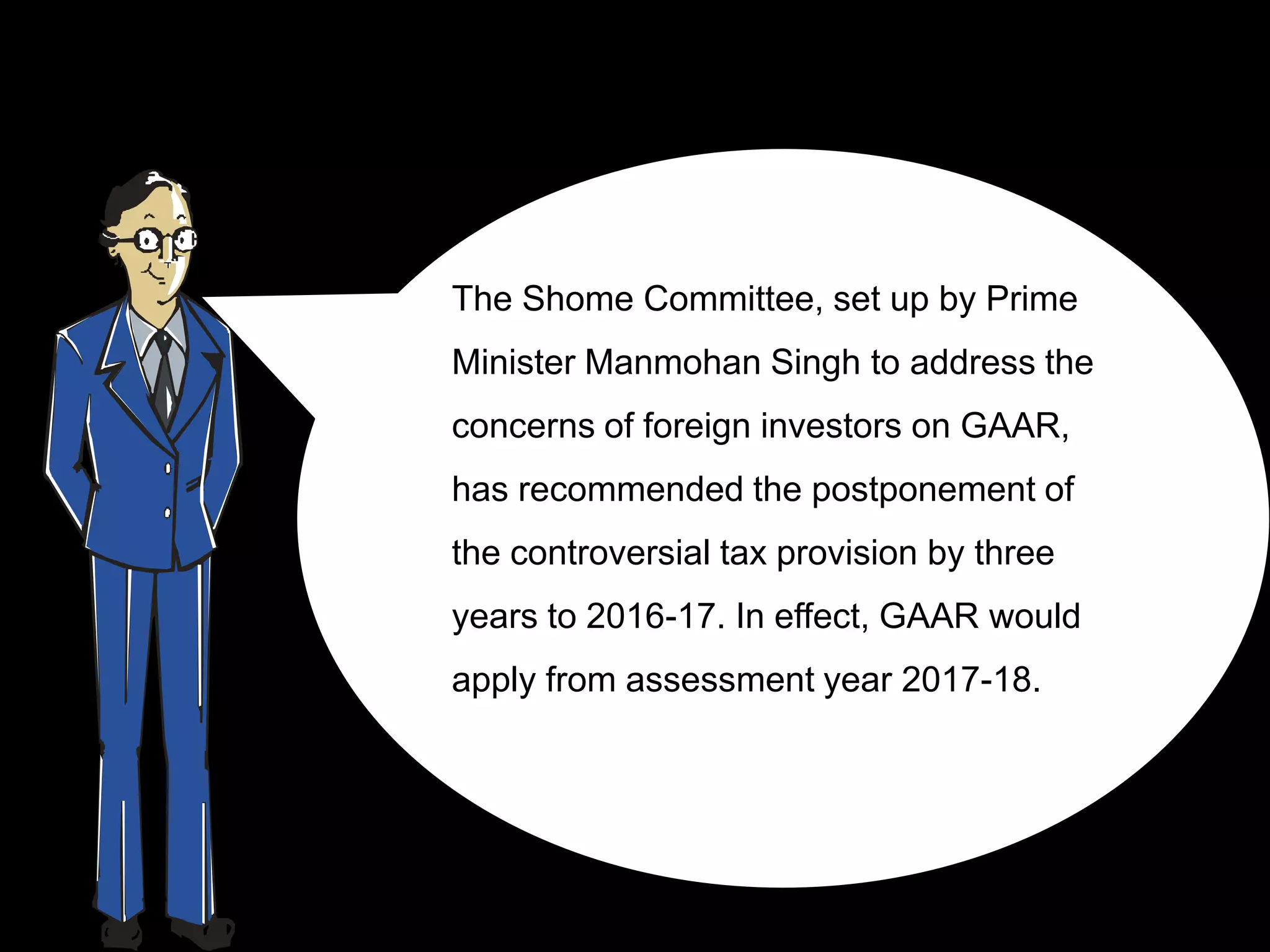

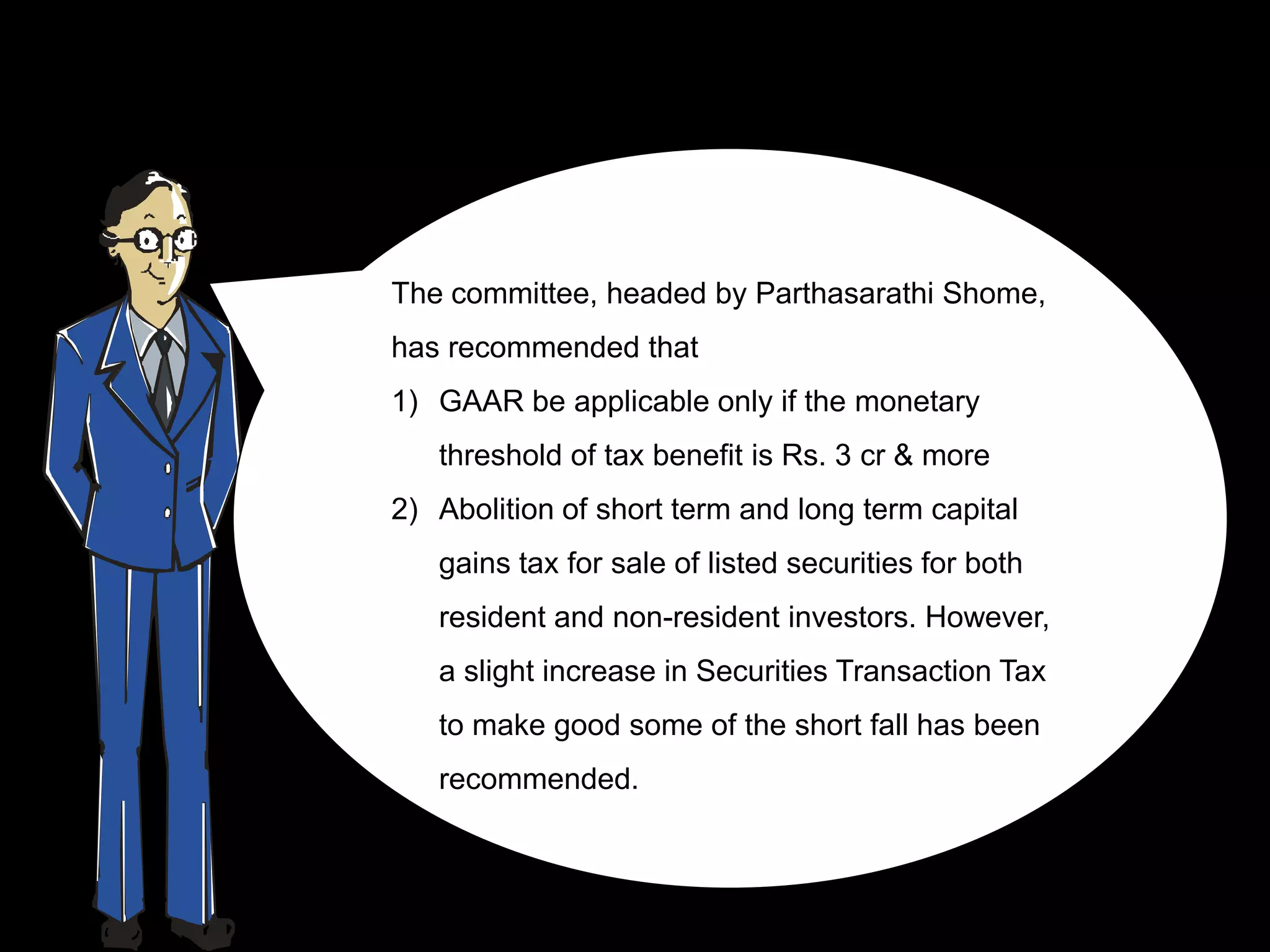

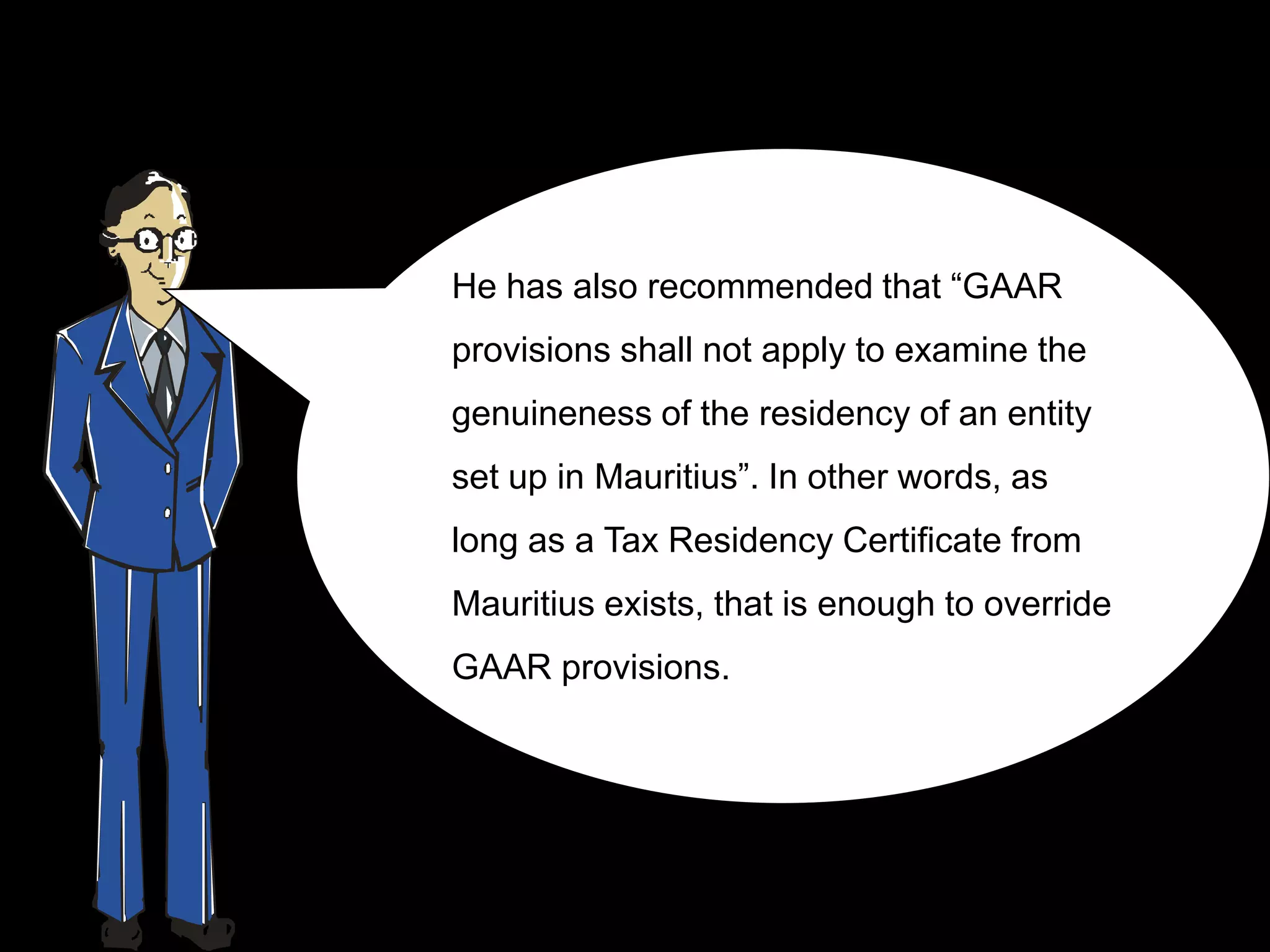

The document discusses India's General Anti-Avoidance Rules (GAAR). It summarizes that GAAR allows Indian tax authorities to levy tax on "impermissible avoidance arrangements" where companies avoid taxes by citing exemptions not intended for them. However, GAAR implementation has been postponed until 2016-2017 due to concerns about lack of clarity negatively impacting investor sentiment. A committee recommended further postponing GAAR and increasing the tax benefit threshold to address these concerns.