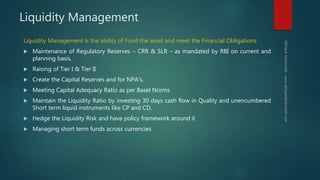

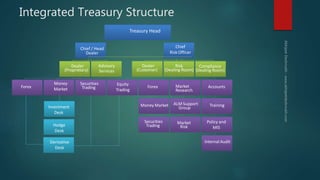

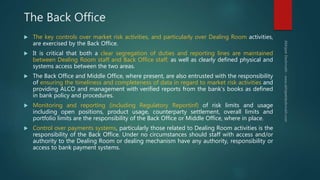

The document discusses the role and evolution of treasury management within banks, emphasizing its importance in managing cash flows, liquidity, and risk while adapting to regulatory changes over time. It outlines the functions of the treasury department, including funds management, liquidity management, and asset-liability management, and highlights critical processes for monitoring and risk evaluation. Additionally, it details the structure of an integrated treasury and the responsibilities of different office levels in ensuring effective management of financial operations.