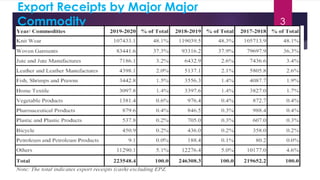

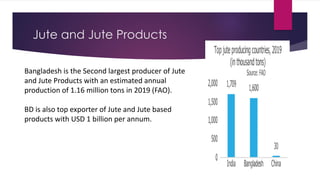

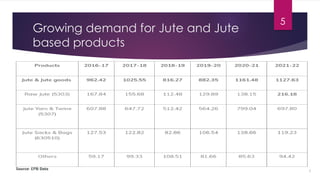

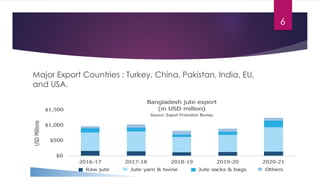

The document provides an overview of Bangladesh's jute and shrimp industries, highlighting production statistics, export markets, and challenges faced in both sectors. Bangladesh is a leading producer and exporter of jute, with a significant global market potential for sustainable products; however, the shrimp sector is struggling due to quality issues and competition. Recommendations for improvement include adopting advanced farming techniques, enhancing the supply chain, and pursuing geographical indication certification for black tiger shrimp to boost the industry.

![ Recalibrating the shrimp industry of Bangladesh to enter the Vannamei market. In order to

ameliorate the ailing shrimp industry, Bangladesh can introduce the commercialization of the

non-native Vannamei production in the country. In this regard, India’s footsteps can be

followed. Until 2009, Monodon was the most widely cultured shrimp in the country, but soon

after, the Indian government approved the experimental trial of Vannamei production due to

constant difficulty in sourcing specific pathogen-free (SPF) shrimp broomsticks.

Commercialization of Vannamei production commenced in 2012. Currently, India has 176,000

hectares of area under shrimp cultivation, out of which 91 % accounts for Vannamei

production, 8% for Monodon, and only 1% for Macro brachium Rosenbergii. [11] The growth of

shrimp farming after the introduction of Vannamei has been no less than phenomenal. Shrimp

production shot up to 805,000 MT in 2019 compared to the 150,000 MT annual production prior

to the introduction of Vannamei shrimp.

25](https://image.slidesharecdn.com/topicjuteandfishindustryoverview-241203171541-de299a74/85/Topic_Jute-and-Fish-Industry-Overview-pdf-25-320.jpg)

![ Finally, after 15 years of pressure from shrimp exporters to allow the production of Vannamei

shrimp in the country, the Bangladesh government approved two pilot projects in 2020, that

would carry out Vannamei production on a trial basis in order to measure the success rate. Under

the supervision of the Department of Fisheries and Bangladesh Fish Research Institute, Sushila, a

non-governmental organization in Khulna along with MU Seafood and Agri-Business Enterprise in

Chattogram commenced production of the non-native shrimp. 1 million Vannamei post-larvae

were imported from Thailand in 2021 to start the trail. According to the Director of Bangladesh

Frozen Foods Exporters Association, Das, Vannamei production rate under a controlled

environment has been 8,901 kg per hectare, whereas Monodon production rate on average is

800-1000 kg/ hectare, with traditional and extensive farms being as low as 200-300 kg/ hectare.

[13] Currently, the shrimp industry is awaiting the government’s approval to start commercial

production of the species which will require another three to four years before production can

commence.

26](https://image.slidesharecdn.com/topicjuteandfishindustryoverview-241203171541-de299a74/85/Topic_Jute-and-Fish-Industry-Overview-pdf-26-320.jpg)