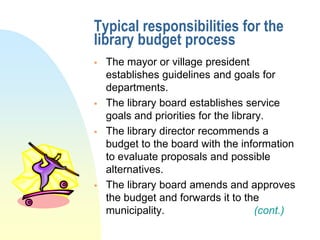

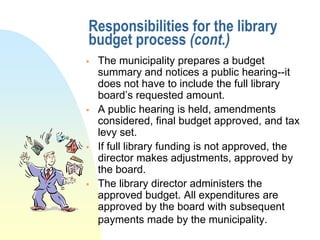

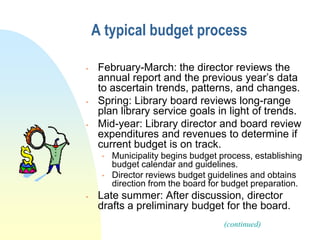

The document discusses the library budgeting process, including how budgets are prepared, presented, and approved. It outlines typical responsibilities like the library board establishing priorities, the director recommending a budget, and the municipality holding public hearings. The summary also notes that budgets establish a framework for operations and allow for planning, tracking funds, and public input.

![Defense Against the Dark Arts

#1: Maintenance of effort (MOE)

Funding from the library's municipality

for a given year may not be lower than

the average funding for the previous

three years [s. 43.15(4)(c)5]

Capital funding should not be included

County payments may not be included

for city, village, town, or joint libraries

For joint libraries, MOE is the total

received from all municipalities

MOE is required for system

participation](https://image.slidesharecdn.com/budgethardtimes-120208105921-phpapp02/85/To-Budget-or-to-Budge-It-16-320.jpg)