Download as PDF, PPTX

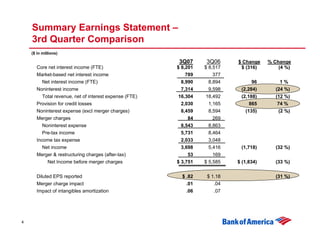

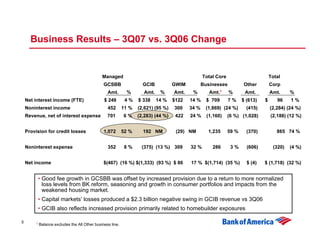

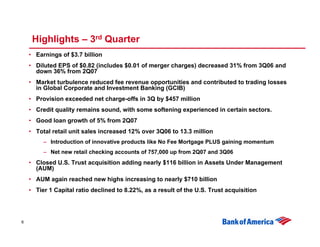

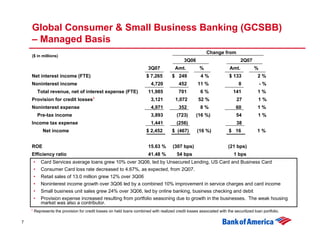

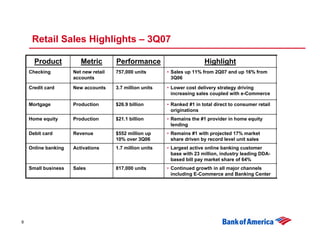

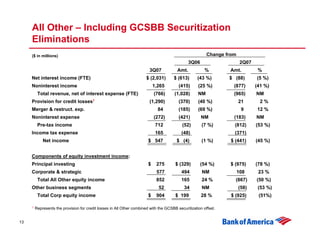

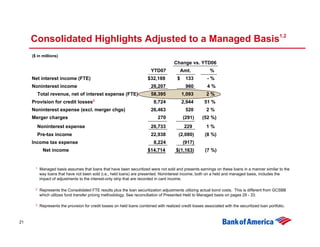

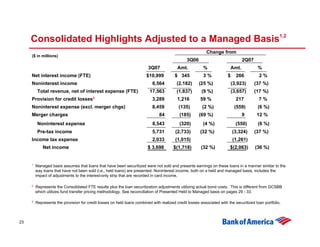

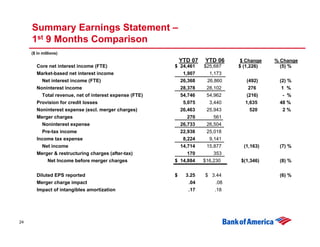

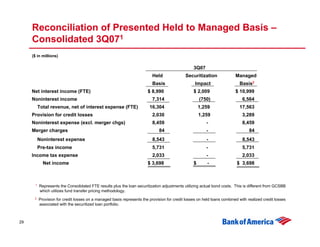

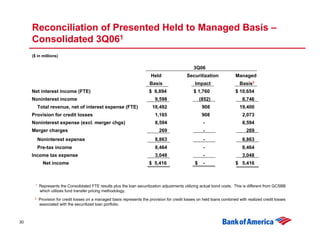

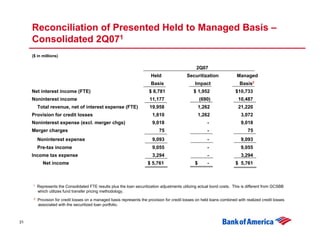

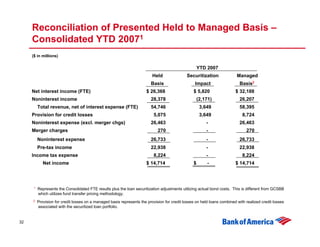

- Bank of America reported third quarter 2007 results with net income of $3.7 billion, down 32% from the third quarter of 2006. Earnings per share were $0.82. - Revenues declined 12% due to a 24% drop in noninterest income driven by losses in Global Corporate and Investment Banking from market turbulence. - The provision for credit losses increased 74% to $2.03 billion reflecting increased consumer loan loss rates and impacts from the weakened housing market.