Download to read offline

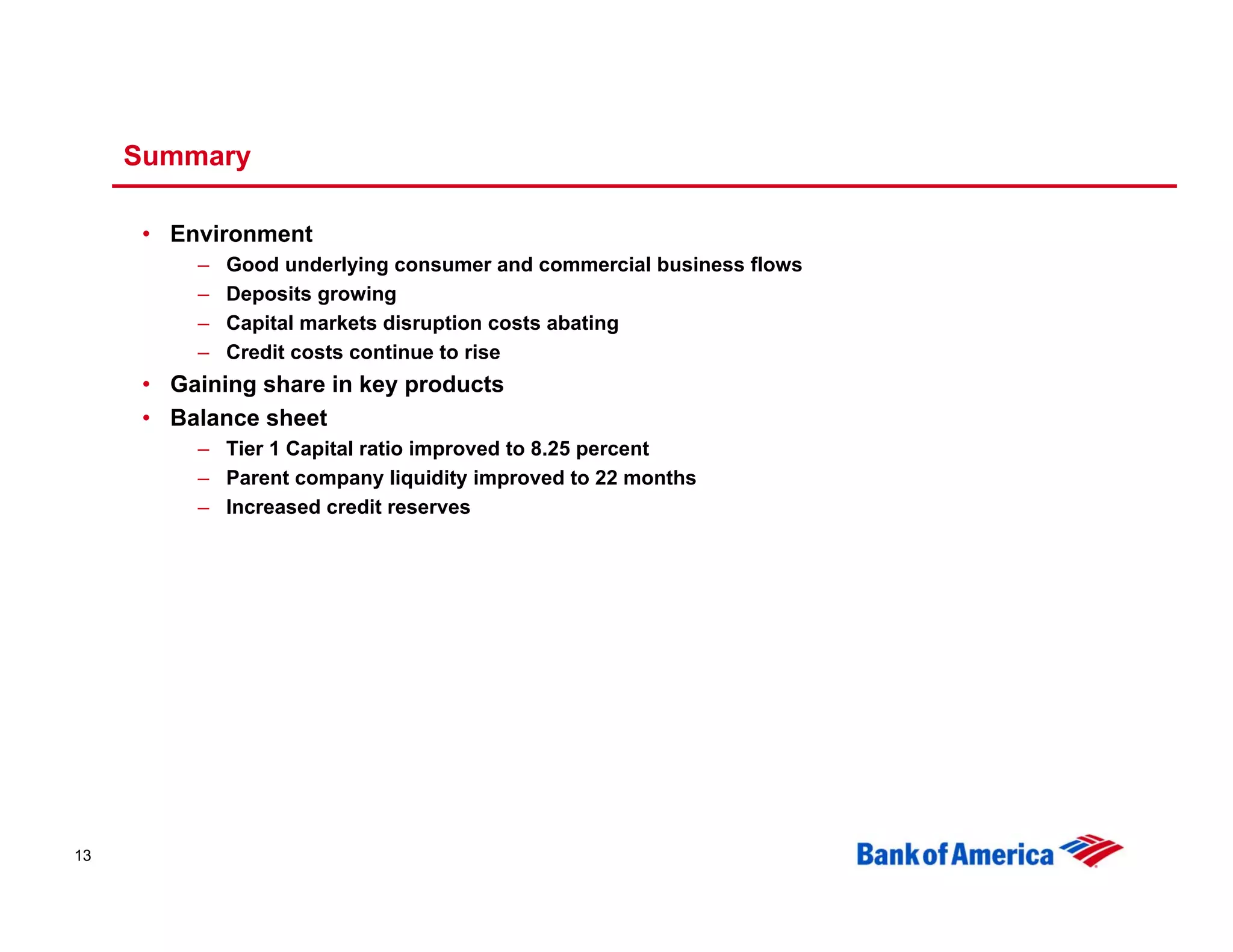

Bank of America reported second quarter 2008 results. Key highlights included diluted EPS of $0.72, record quarterly revenue of $20.3 billion, and net income of $3.41 billion. Credit costs increased significantly to $5.83 billion due to weakness in the housing market. Revenue growth was driven by higher net interest income, though partially offset by lower noninterest income and higher expenses.