The document is a report about Ras Al Khaimah in the United Arab Emirates that was published in 2015 by Oxford Business Group. It contains information about the economy, finance, industry, construction, real estate, transport, energy, health, education, and tourism sectors. The report includes statistics, overviews of key industries and sectors, interviews with local leaders, and listings of companies and contact information.

![www.oxfordbusinessgroup.com/country/uae-ras-al-khaimah

22

Land lease and production sharing deals provided to GCC investors should aid small-scale farmers

PROFILE ANALYSIS

The GCC region’s plans

for investment in Africa

are facilitated by the

widespread recognition on

the continent that FDI is a

way to provide employment

and further development

through both capital and

skills transfer.

The current phase of GCC investment in Africa

appears set to address many of the earlier struc-

tural weaknesses and, in the process, help develop

a more viable long-term investment environment

in many parts of the continent. This includes shifts

on the foreign investor side, and also locally among

African governments and key stakeholders. Coun-

tries like Zambia and Kenya are devising terms for

land use that could help stabilise conditions on the

ground. Leases in Zambia are likely to be provided

for no more than 25 years, and will come with a

requirement that crops produced on the land be

split up to 50-50 between exports and the local

market. Likewise in Kenya, there will likely be land

leases as opposed to outright sales.

BECOMING PARTNERS: Africa’s appetite for for-

eign direct investment (FDI) remains strong. FDI is

more widely recognised in Africa as a way to help

provide employment opportunities and develop

“expertise technologies and capital for improving

infrastructure such as roads, education and health

facilities”, as noted by the Centre for Interna-

tional Governance Innovation. Local stakeholders

in Kenya have shown themselves to be “willing to

accept and participate in land leases, provided

they include certain provisions”, such as 15-year

maximums, and that they be “renewable subject to

mutual negotiation”. This involvement would con-

trast with the historical trend in which landowners

were typically excluded from negotiations.

Helping to ensure a greater degree of trust

among local communities will provide for more

sustainable investments in agriculture, and will

have positive knock-on effects for other sectors as

well. In Kenya, for example, public-private partner-

ships (PPPs) received a boost in 2013 with the PPP

Act coming into force, “in order to strengthen the

legal and regulatory framework for PPPs… [and]

remove duplication and overlap”.

Incentives being promoted to lure back inves-

tors after an at-times rocky start include the Kenya

Investment Authority signing a double tax agree-

ment (DTA) with Qatar in April 2014. The deal will

protect investors from tax on repatriated profits

after they have already paid in their country of

investment. A “reciprocal agreement” was also

signed that is meant to “guarantee Kenyan and

Qatari businesspeople of rights to their assets

in the two countries”. Kenya that month also had

a draft DTA with Iran and the UAE, and a memo-

randum of understanding was signed between

KenGen and Nebras Power Company of Qatar.

In early 2014 African representatives presented

land lease and production sharing deals to GCC

investors as a means to aid small-scale farmers

and to also ensure food supplies for locals. Ghana,

for its part, has offered tax-free agreements for

investment in agriculture in the country’s north,

with the premise of sharing part of the produced

crops with the domestic market. But much is still to

be done in terms of regulation. Kenya, for instance,

STRATEGIC SOURCING: Along with sourcing from

Eastern Europe and farther afield in South Amer-

ica and Asia, GCC investors began looking more to

Africa – East Africa in particular – where available

farmland was seen as a way to provide domestic

populations with reliable sources of key agriculture

products. Countries targeted in the first phase

included Sudan, Ethiopia, Mali, Mauritania, Mozam-

bique and Tanzania, along with the North African

countries of Morocco and Egypt.

Many African investment destinations them-

selves, however, suffer from profound food

insecurity and political risks. Indeed, the Horn and

Sahel regions of the continent are the most fam-

ine-prone places on the planet. This has presented

foreign investors with a steep learning curve when

it comes to navigating African markets and relying

on those destinations for strategic commodities.

Local concerns over land rights and food security

presented serious operational and reputational

risks for Gulf investors. Early risks relating to land

use were due in large part to the absence of ade-

quate land ownership regulation, with Oxfam

reporting that up to 90% of land in sub-Saharan

Africa was unregistered, placing local residents at

greater risk of being displaced for new projects.

LOCAL GAINS: Many African governments have

shifted their emphasis to boosting local benefit, a

trend that is likely to reach beyond agriculture in

the coming years. This presents new challenges

for investors; however, it can present longer-term

benefits and opportunities as well. In a model for

how this can be achieved, the UAE’s Al Dahra Hold-

ing enforces a 50-50 sharing formula, according to

Khadim Al Darei, its vice-chairman, in a statement

given to local media in early 2014. According to Al

Darei, Al Dahra has avoided some of the problems

encountered by other foreign investors by actively

creating jobs for locals and sharing its produce.](https://image.slidesharecdn.com/eb75dd27-86ed-46d0-b1bd-1c1eb9053e8b-151121124901-lva1-app6891/85/The-Report_Ras-Al-Khaimah_2015-24-320.jpg)

![www.oxfordbusinessgroup.com/country/uae-ras-al-khaimah

44

While the UAE’s central

bank recently released

reforms aimed at increasing

Basel III compliance, many

of the nation’s banks

already have high capital

adequacy ratios and would

not be greatly affected.

A series of recent

regulations issued by the

Insurance Authority in

February 2015 place limits

on the types of investments

insurance firms can make

and are designed to limit

losses from the equities

market.

Insurance firms can invest up to 30% of total assets in real estate

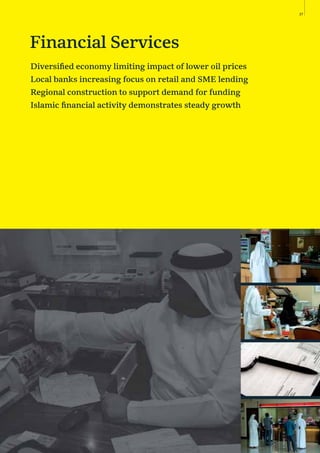

FINANCIAL SERVICES ANALYSIS

Regulatory changes in the UAE’s banking and insur-

ance industries have picked up in recent years. In

the banking sector, new regulations in line with

Basel III standards are set to stabilise and protect

banks, setting new capital and liquidity standards,

while changes to the insurance sector are to limit

investment losses in the UAE’s equities markets.

INSURANCE: In February 2015 the Insurance

Authority issued a series of new regulations for

Islamic and conventional insurers operating in the

UAE, including limits on what kinds of investments

firms can make in capital markets. These regulate

the financial, technical, investment and accounting

operations of both traditional and takaful (Islamic

insurance) providers, in order to reduce investment

income losses suffered in recent years.

The new rules were unveiled against a backdrop

ofincreasingvolatilityinlocalequitymarkets,which

have been hit hard by falling oil prices that plunged

by more than 50% between mid-2014 and January

2015. In turn, the Dubai Financial Market’s gen-

eral index dropped by 25% between October 2014

and February 2015, while the Abu Dhabi Exchange

benchmark index fell by 11% over the same period.

Insurance companies have also been affected —

Ras Al Khaimah’s United Insurance Company (UIC),

for example, reported a 9.7% drop in assets in 2014,

from Dh314.4m ($85.6m) to Dh283.9m ($77.3m).

To mitigate the sector’s market risk exposure, the

new regulations limit insurance firms’ investments

in different instruments and sectors. Under the

new rules, insurers can invest a maximum of 30%

of their total investment assets in real estate. The

threshold for investment in equity instruments for

listed and unlisted companies in the UAE is also set

at 30%, with a limit of 10% for any single stock, fund

or instrument. Meanwhile, investment in foreign

equity instruments is capped at 20%, with exposure

to a single counterparty established at 10% or less.

Importantly, insurance companies are permitted

to invest up to 100% of their funds in government

securities or instruments issued by the government

of the UAE or one of the emirates. They are also

required to deposit at least 5% of their assets with

banks in the UAE. In addition, the new regulations

allow insurers to invest up to 30% in loans secured

by life policies issued by the company itself, and

allocate as much as 1% to financial derivatives, up to

30% in secured loans and deposits with non-lend-

ers, and another 10% in other invested assets.

According to Sultan Al Mansouri, UAE minister of

economy and chairman of the IA, the new rules will

ensure solvency of insurance firms and their ability

to meet all liabilities, though their impact will not be

known until year-end results for 2015 are released.

BANKS: Banks are also adapting to new regula-

tory changes. The central bank moved to roll out

a series of reforms aimed at Basel III compliance

in September 2014, publishing its “Financial Sta-

bility Report 2013”, which proposed revisions to

the existing regulatory framework. Requirements

include a minimum capital adequacy ratio of 8% of

risk-weighted assets, with Tier 1 capital and core

Tier 1 capital to comprise 6% and 4.5%, respectively.

New liquidity regulations emphasise the need for

each bank to have a proper liquidity risk manage-

ment framework to minimise stress on existing

banks. These capital reforms are unlikely to have a

significant impact on UAE banks.

In September 2014 law firm Al Tamimi & Co. noted

that “many of the UAE local banks already have

high level[s] of capital adequacy, [and] the Basel III

changes may not substantially impact the require-

ments of capital profile of the local banks.” RAK-

BANK, for example, had a Tier 1 capital adequacy

ratio of 26.5% at end-2014, down from 29% in 2013

but above the Basel III limit, allowing “ample room

for growth”, according to its 2014 annual report.

Prioritising balance sheet health for banks and insurers

Regulatoryrewrite](https://image.slidesharecdn.com/eb75dd27-86ed-46d0-b1bd-1c1eb9053e8b-151121124901-lva1-app6891/85/The-Report_Ras-Al-Khaimah_2015-46-320.jpg)

![www.oxfordbusinessgroup.com/country/uae-ras-al-khaimah

102 HEALTH OVERVIEW

RAK’s pharmaceutical

industry is thriving in

the wake of

unprecedented new

demand across

both the UAE and GCC.

Growth in private health care should bolster pharma sales in 2015

the federal government in rolling out such a system.

“Once mandatory medical insurance is in place here,

we will have new challenges. We will need to prevent

abuse through data collection and the establishment

of gate keepers,” Siddiqui told OBG.

PHARMACEUTICALS: RAK’s pharmaceutical indus-

try is thriving in the face of unprecedented new de-

mand across both the UAE and GCC, with Julphar now

one of the largest pharmaceutical manufacturers in

the Gulf region. Established in RAK in 1980 and ini-

tially offering just five products, the company has ex-

panded its operations to comprise 12 manufacturing

facilities that today produce over 1m boxes of medi-

cine per day. Eleven of these are based in RAK, and in

2013 the company opened a 12th facility in Ethiopia

as part of its global expansion strategy.

Julphar currently produces a total of 213 differ-

ent pharmaceutical products that are distributed to

over 40 countries. Julphar is noted for its production

of large batches of crude insulin made using crystals

derived from recombinant DNA technology, and man-

ufactured at its facilities in RAK.

The company reported steady growth in 2014, with

total sales revenues reaching Dh1.43bn ($389.25m), a

5.2% increase year-on-year, driven by 7.5% growth in

private market sales. Gross profits rose 3.4% to reach

Dh848.2m ($230.9m), operating profits rose 1.1%

to Dh238.5m ($64.9m), and net profits rose 2.9% to

reach Dh234.7m ($63.9m).

It is expected that the growth in private health

care will further bolster sales in 2015; according to

officials at SKSH, the hospital plans to capitalise on

Julphar’s close proximity in its pharmaceutical pro-

curement, which should make a significant impact on

mid-term sales and revenues. “We are fortunate that

the emirate contains such a large pharmaceutical

manufacturing facility. We expect a very strong col-

laborationwith[Julphar]inthecomingyears,”Myung-

Whun Sung, CEO of SKSH, told OBG.

OUTLOOK: With an expanding portfolio of specialty

care,risingpublicandprivateinvestmentandexpend-

iture, and an intensifying government focus on med-

ical tourism, RAK’s health care segment is expected

to see significant expansion in the coming years. The

entrance of SKSH into the emirate’s health landscape

is perhaps the most promising development to date,

and should see an increasing number of national and

foreign patients flock to RAK in the coming years. At

thesametime,newspecialtyservicesonofferatboth

SKSH and RAK Hospital will serve a growing number

of patients suffering from increasing prevalence of

non-communicable diseases.

Although a mandatory medical insurance scheme

has yet to be rolled out and there remain shortages in

health care providers, the mid-term forecast is nev-

ertheless optimistic given increased investment and

demand. Ongoing expansion at RAKMHSU and RAK

FTZ is expected to alleviate the most pressing human

resources concerns, while the planned introduction

of universal health insurance should help hospi-

tals expand the scale and scope of their operations.

Health Authority announced plans to implement its

own mandatory health insurance legislation, with the

aim of creating an integrated health network based

on a sustainable financing system.

The Dubai Health Insurance Law No. 11/2013 went

into effect in January 2014, mandating all employers

in Dubai to provide health insurance coverage for

employees, although companies were given rolling

deadlines to comply: those with more than 1000 em-

ployees had until October 2014 to roll out health care

plans; companies with 100-999 employees had to

provide coverage as of July 2015; and companies with

fewer than 100 employees must comply by June 2016.

In the Northern Emirates, plans for mandatory

health coverage were announced in 2004 and again

in 2007, but have yet to be rolled out, despite warn-

ings from stakeholders that the system cannot ex-

pand without such policies. “Private, for-profit health

care is technology and capital intensive. You need

to have enough money to keep up with technology,

which can cost hundreds of millions of dollars, but

who is bringing this capital to the table? We have to

encourage investment in health care because of the

returns that it offers,” Siddiqui told OBG.

In October 2014, sources at the MoH told leading

UAE daily The National that plans were under way

to introduce mandatory coverage in the Northern

Emirates in the near term, although further details

have yet to be unveiled. Stakeholders in RAK were

nonetheless heartened to hear the news, with many

calling for improvements to existing record-keeping

practises in order to reduce the challenges facing

SOURCE: RAK DED

Pregnant Nursing services Maternity & childcare Dental Treatment

Emirati 6248 224,061 22,865 7830 155,545

Non-Emirati 7067 401,697 28,670 16,270 344,065

Patients in primary health care centres by service & nationality, 2014](https://image.slidesharecdn.com/eb75dd27-86ed-46d0-b1bd-1c1eb9053e8b-151121124901-lva1-app6891/85/The-Report_Ras-Al-Khaimah_2015-104-320.jpg)