Download as PDF, PPTX

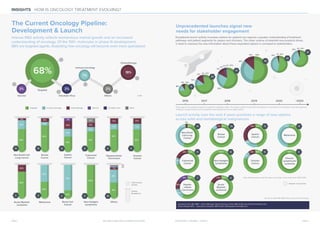

The oncology treatment landscape is rapidly evolving with over 100 molecules in phase III development, where 68% are targeted agents, indicating increased specialization in oncology. Exceptional launch activity expected over the next four years will offer diverse options across both solid and hematological malignancies, underscoring the need for enhanced stakeholder engagement. Understanding treatment pathways and patient segments is crucial for payers and clinicians amidst the growth of options for patient care.

![Cells and Organs of immune system [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/cellsandorgansofimmunesystemautosaved-260123152717-ea0cb261-thumbnail.jpg?width=640&height=640&fit=bounds)

![Hypothalamus short notes on location, function and disorders by Dr. Neha [PT]...](https://cdn.slidesharecdn.com/ss_thumbnails/hypothalamusbydr-260124142231-2b48143d-thumbnail.jpg?width=640&height=640&fit=bounds)