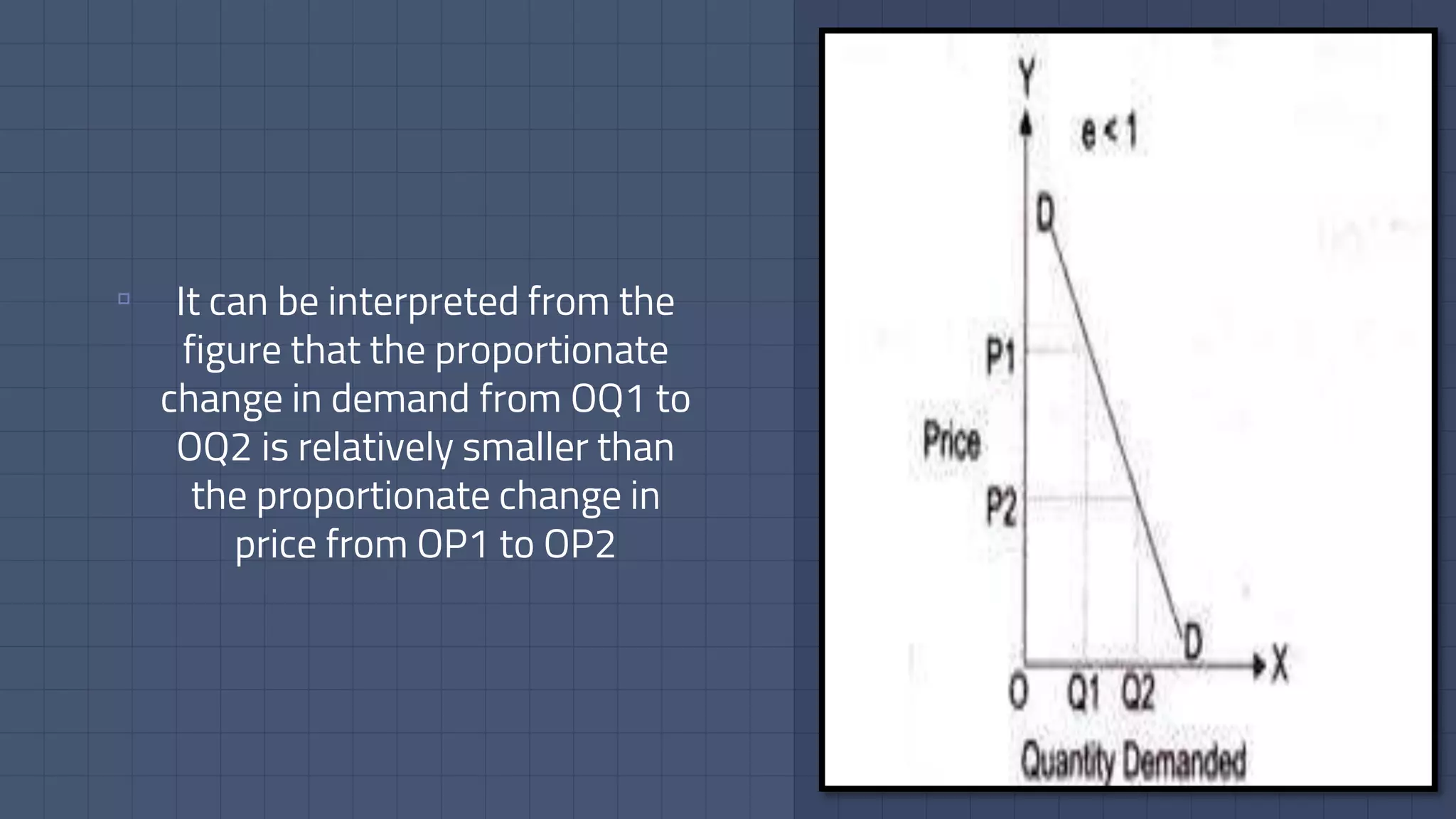

Downloaded 15 times

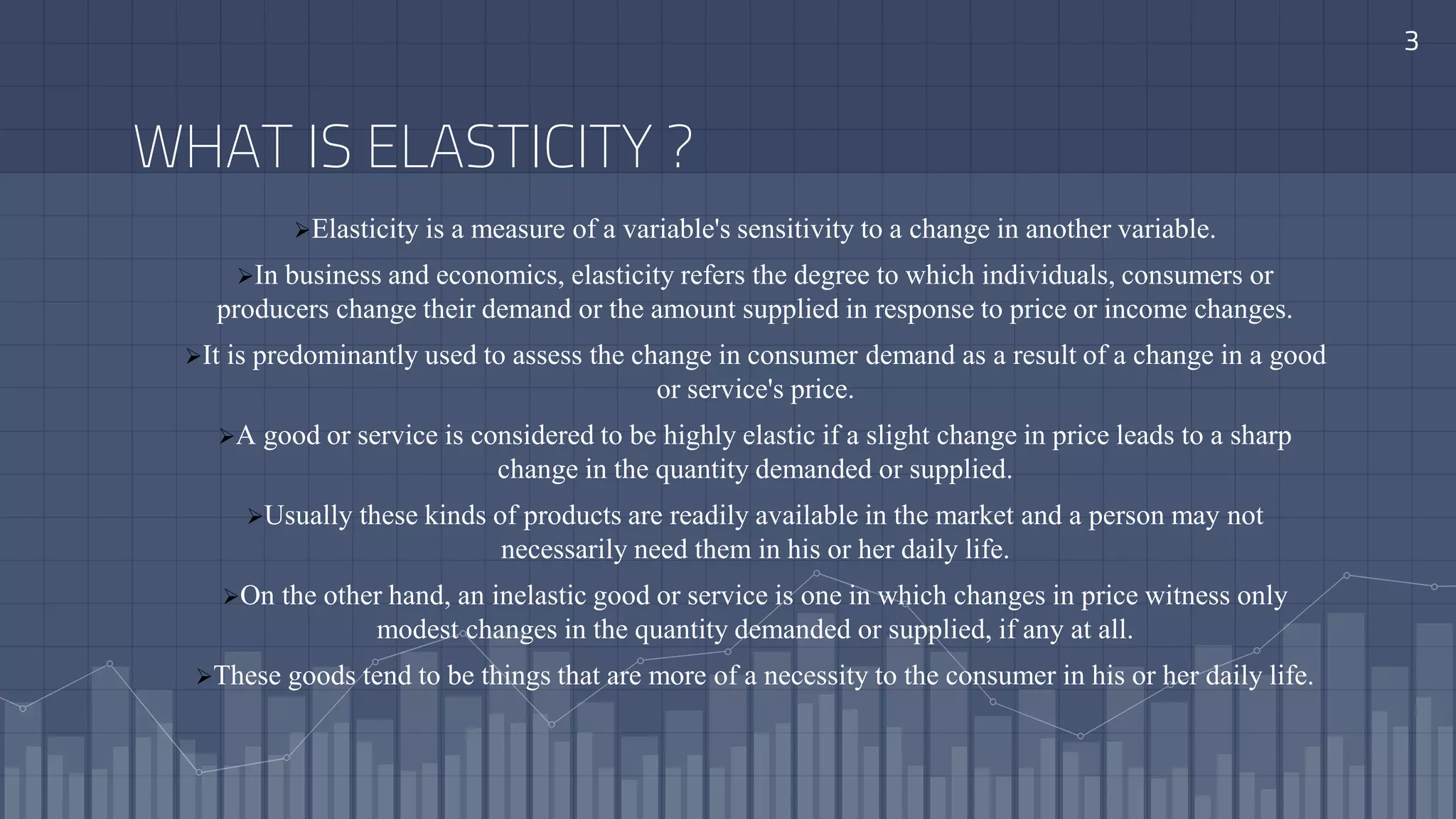

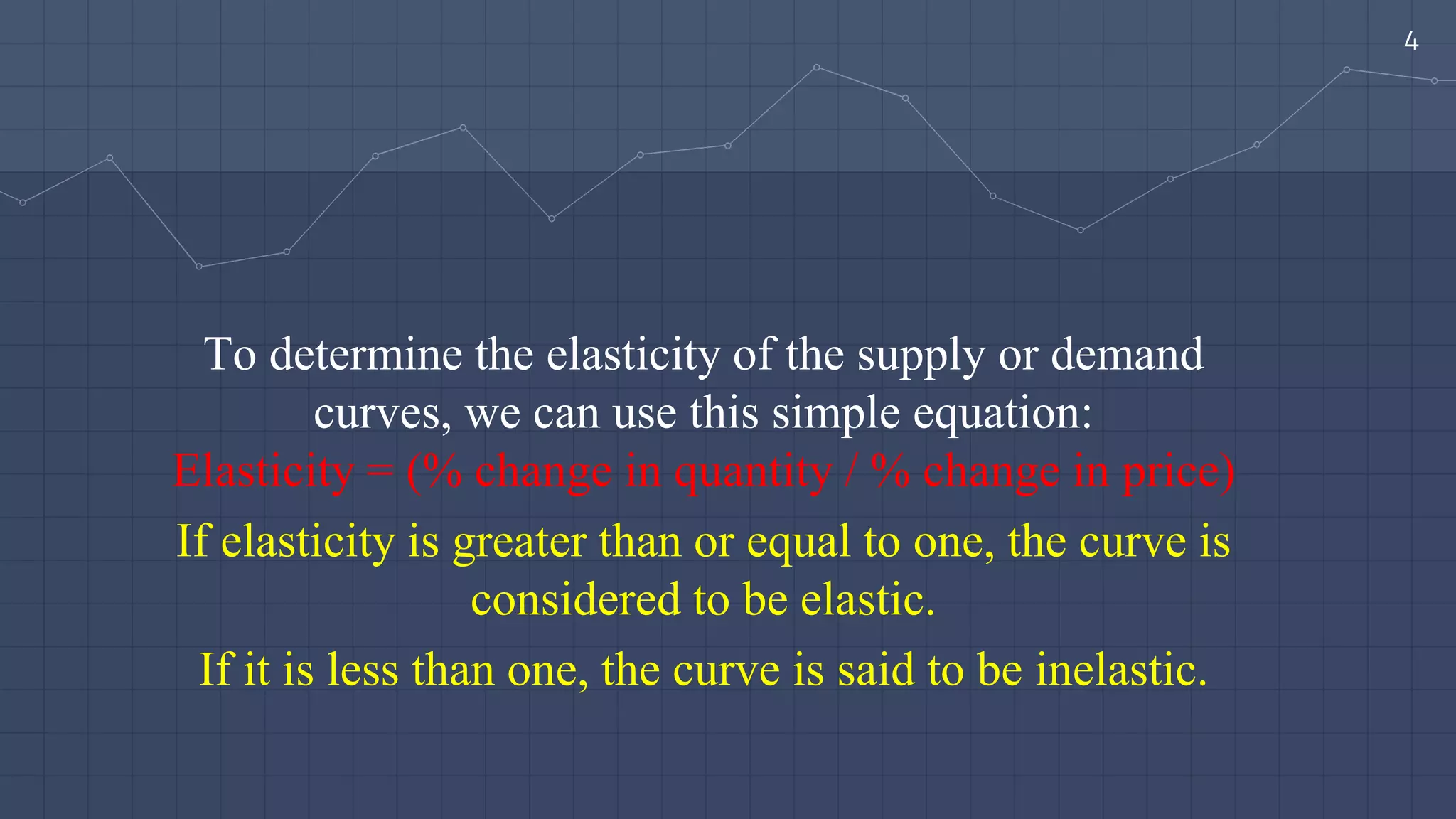

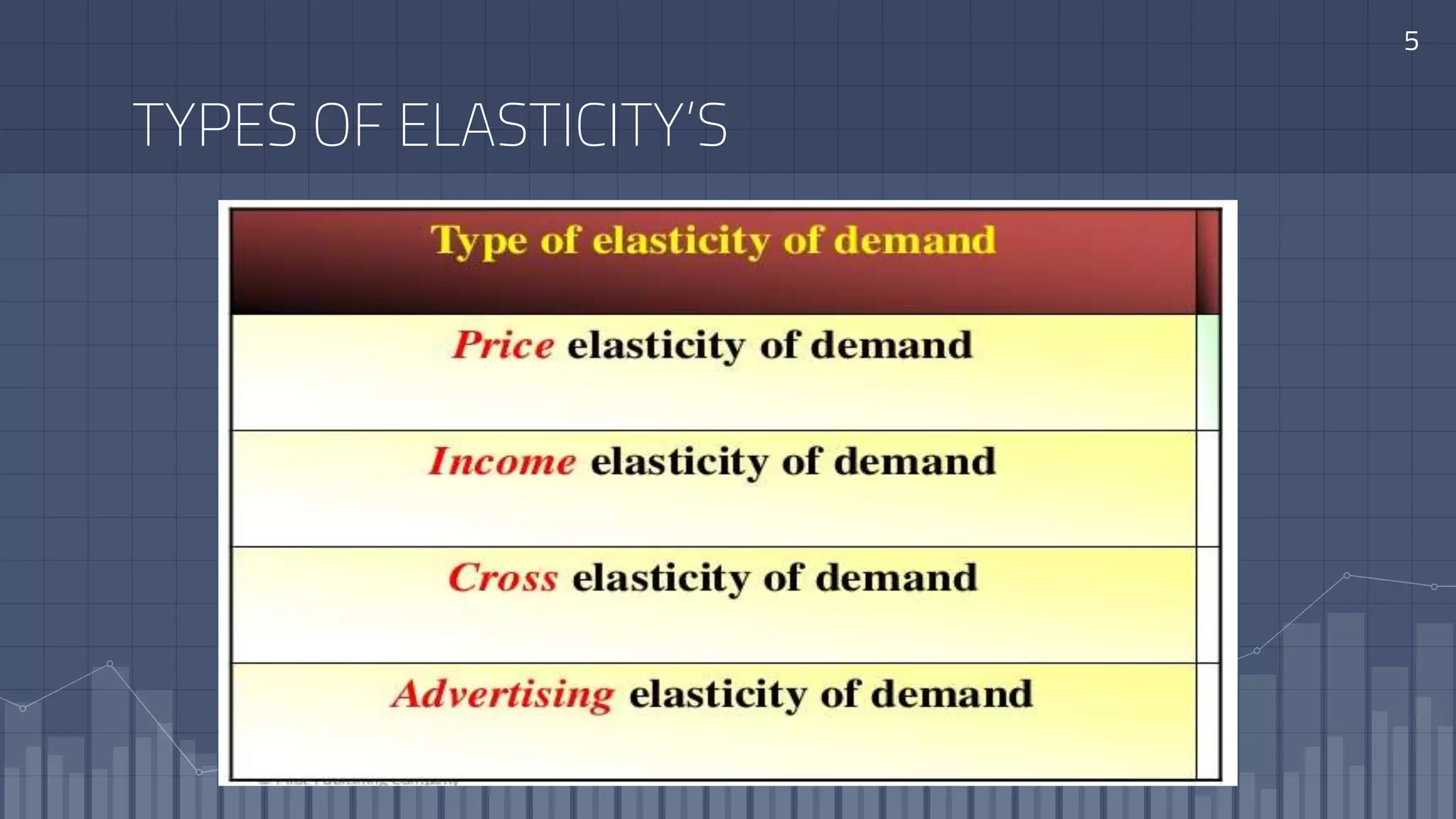

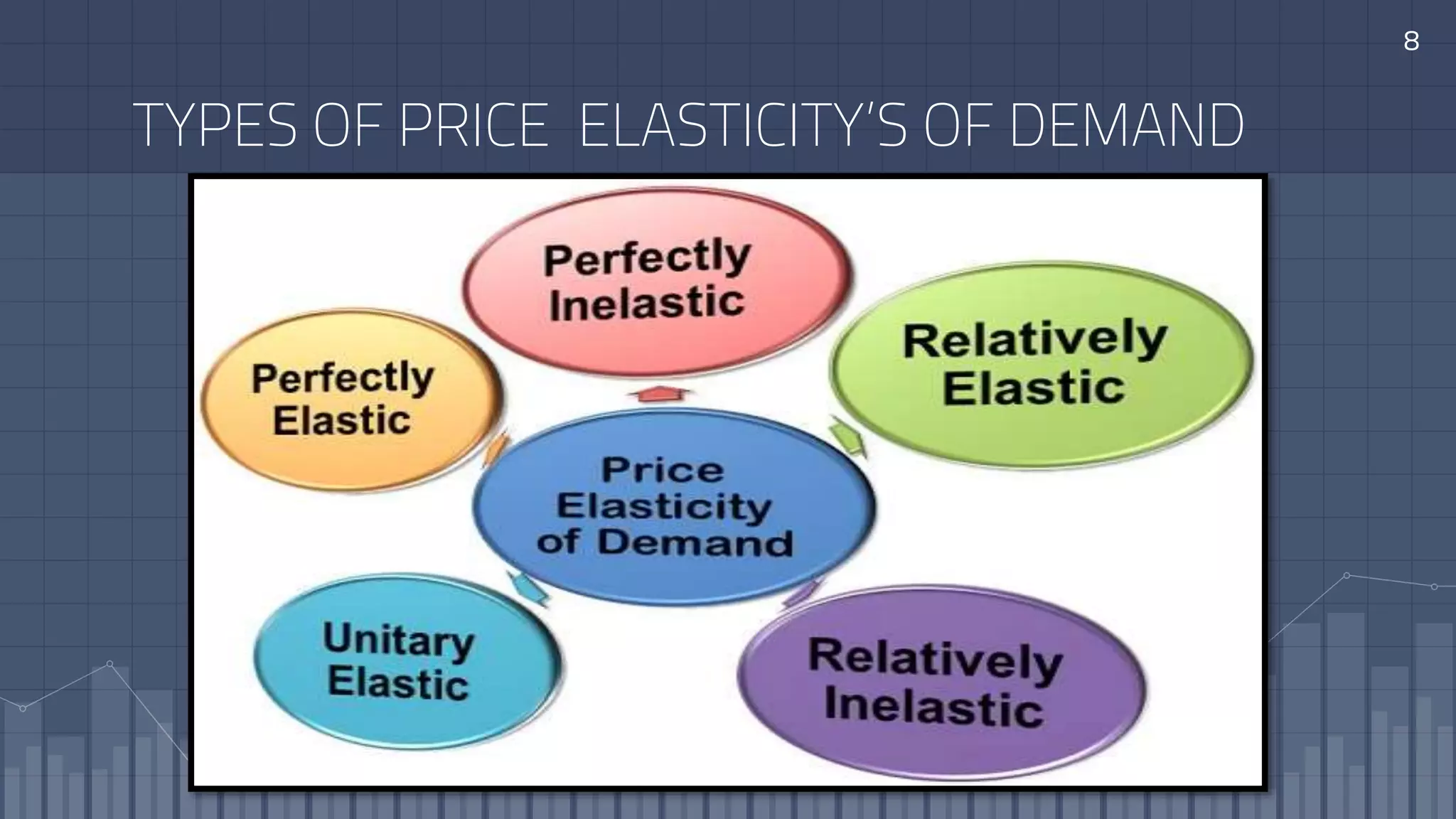

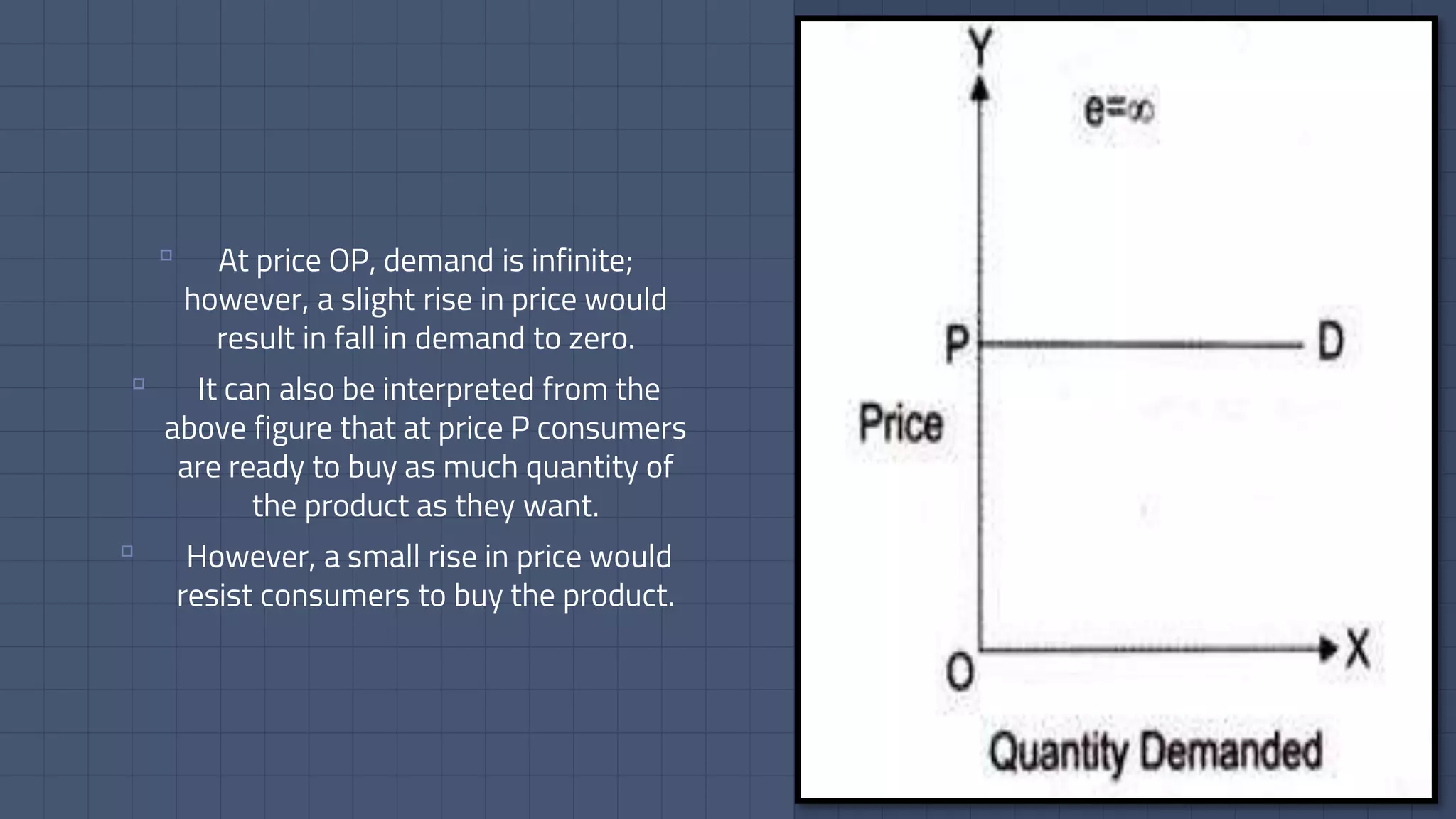

The document discusses the concept of elasticity in economics. It defines elasticity as a measure of how sensitive a variable is to changes in another variable. There are different types of elasticity including price elasticity of demand, income elasticity of demand, and cross elasticity of demand. Price elasticity of demand refers to how much demand for a good changes when its price changes. Income elasticity of demand refers to how demand changes with changes in consumer income. Demand can be perfectly elastic, perfectly inelastic, relatively elastic, or relatively inelastic depending on the responsiveness of quantity demanded to price changes. Factors like availability of substitutes, income level, and time impact price elasticity. Income elastic goods see larger increases