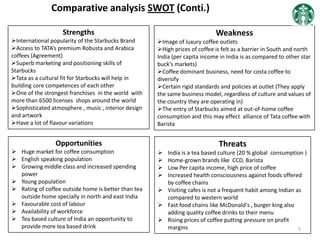

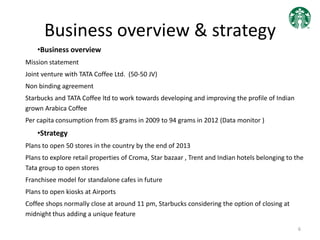

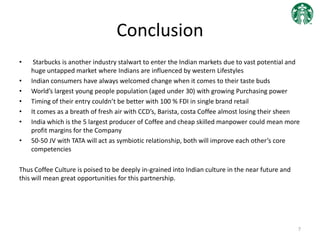

Starbucks' entry into the Indian coffee market through a joint venture with Tata aims to capitalize on the growing coffee consumption among younger consumers and the liberalization of FDI in retail. Despite facing challenges from strong domestic competitors like Café Coffee Day and Barista, Starbucks can leverage its global brand reputation and innovative marketing strategies. The partnership with Tata allows for better sourcing of coffee while addressing the cultural dynamics of the Indian market.